Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

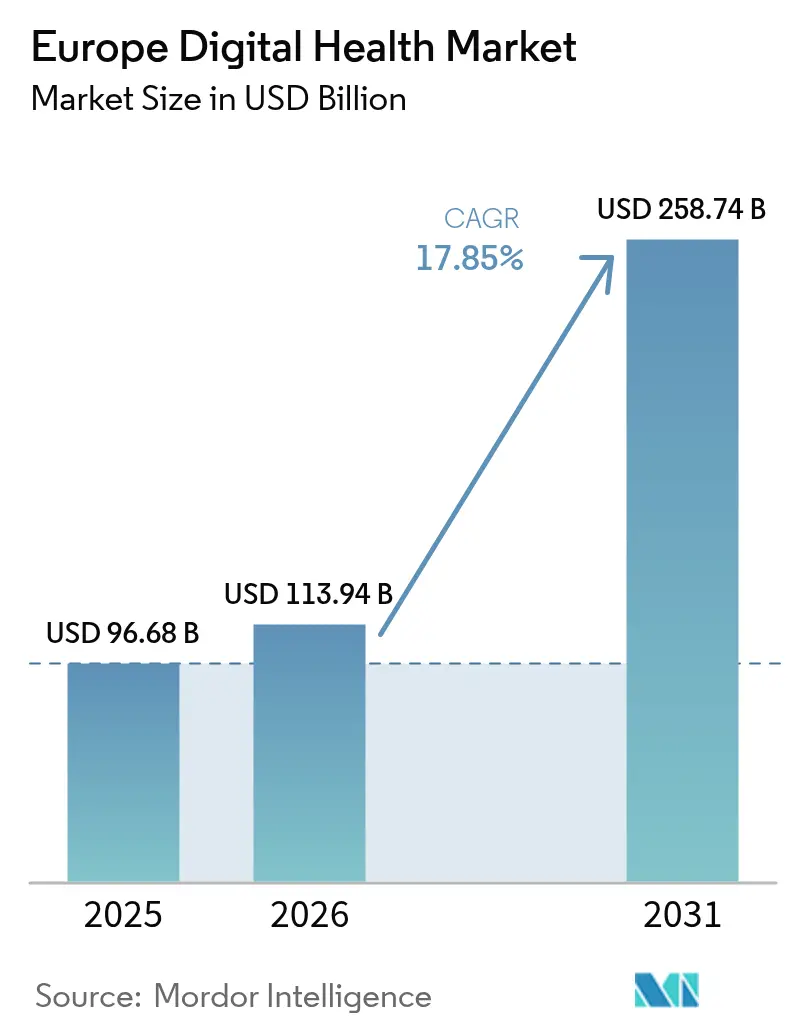

| Base Year Market Size (2025) | USD 96.68 Billion |

| Market Size (2026) | USD 113.94 Billion |

| Market Size (2031) | USD 258.74 Billion |

| Growth Rate (2026 - 2031) | 17.85% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Digital Health Market Analysis by Mordor Intelligence

Europe digital health market size in 2026 is estimated at USD 113.94 billion, growing from 2025 value of USD 96.68 billion with 2031 projections showing USD 258.74 billion, growing at 17.85% CAGR over 2026-2031. Demand gains stem from post-pandemic telemedicine normalization, swift regulatory harmonization under the European Health Data Space, and record-level public funding for AI-enabled care delivery. Germany’s DiGA reimbursement pathway, France’s PECAN fast-track, and the United Kingdom’s GBP 3.4 billion NHS technology budget are accelerating enterprise-class platform rollouts. Cloud infrastructure already underpins more than half of all deployments, signaling a shift away from bespoke on-premise solutions toward scalable ecosystems that meet divergent country rules. Competitive intensity remains high because clinical use cases still favor best-of-breed applications, yet platform vendors are consolidating through partnerships aimed at cross-border interoperability.

Key Report Takeaways

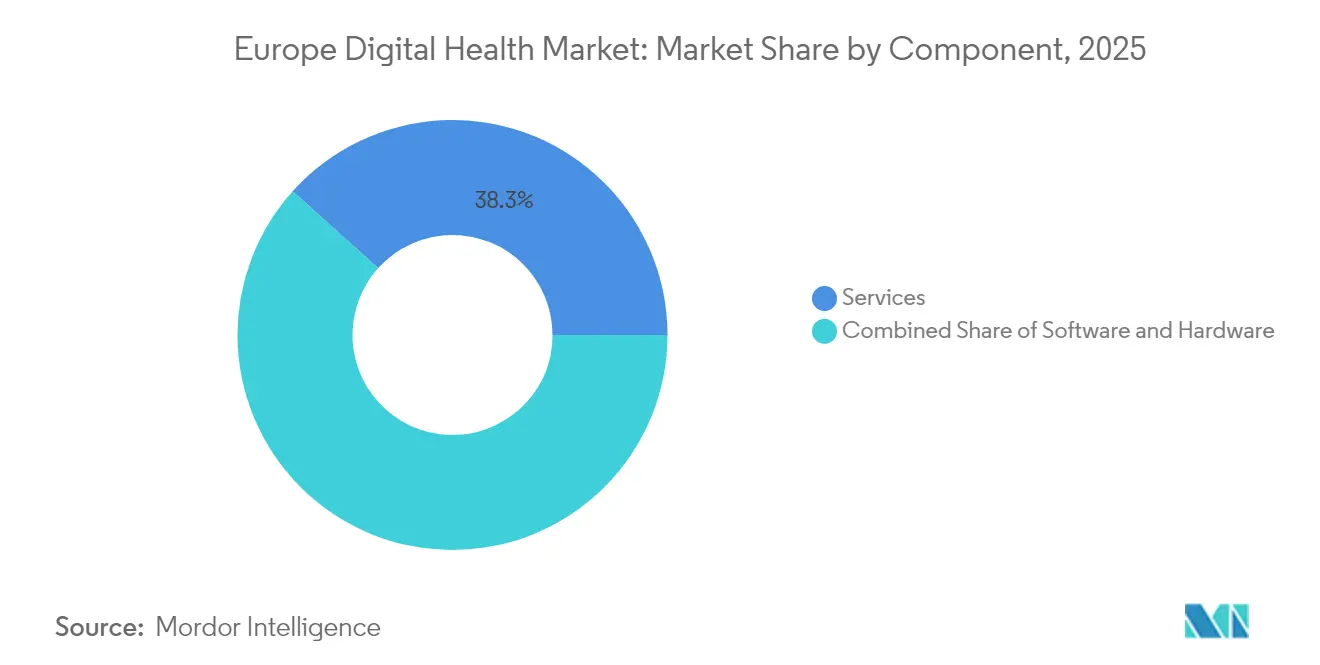

- By component, services led with 38.34% revenue share in 2025; software is projected to expand at an 18.6% CAGR through 2031.

- By technology, telehealth held 46.55% of Europe digital health market share in 2025, while mHealth is set to grow at 18.78% CAGR to 2031.

- By end user, patients and consumers accounted for 42.10% of Europe digital health market size in 2025; payers show the highest CAGR at 18.55% for 2026-2031.

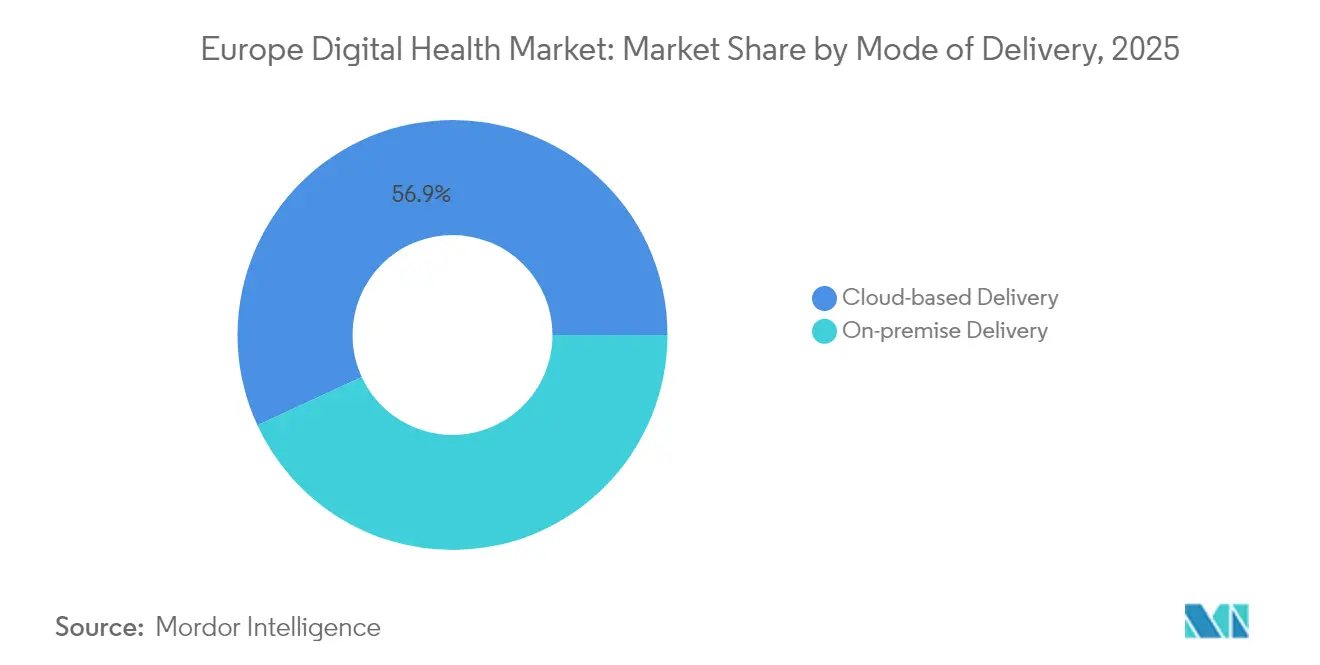

- By mode of delivery, cloud-based models captured 56.90% of Europe digital health market share in 2025; on-premise deployments are forecast to rise at 18.95% CAGR.

- By application, chronic disease management led with 28.25% revenue share in 2025, whereas fitness and wellness applications are poised for 19.18% CAGR through 2031.

- Germany, France, and the United Kingdom together represented 57.45% of 2025 revenue, with Germany alone holding 23.10% of Europe digital health market size.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Digital Health Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Funding & Regulatory Push | +3.2% | EU-27, with strongest impact in Germany, France | Medium term (2-4 years) |

| Ageing Population Driving Chronic-Care Demand | +4.1% | Global, with highest intensity in Germany, Italy, Spain | Long term (≥ 4 years) |

| Telehealth Normalisation Post-Covid-19 | +2.8% | EU-27, Nordic countries leading adoption | Short term (≤ 2 years) |

| Cross-Border Eprescription & eID Interoperability | +1.9% | EU-27, early gains in Netherlands, Estonia, Finland | Medium term (2-4 years) |

| Germany's "Hospital-At-Home" Reimbursement Model | +1.4% | Germany, with spillover to Austria, Netherlands | Medium term (2-4 years) |

| MDR-Compliant AI Software Demand | +2.7% | EU-27, with early adoption in Germany, UK, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Funding & Regulatory Push

Europe’s coordinated policy regime now couples multi-billion-euro grants with mandatory interoperability. Horizon Europe has earmarked EUR 13 billion for digital activities between 2025-2027, with EUR 67.5 million ring-fenced for AI-assisted healthcare [1]European Commission, “European Health Data Space Regulation,” ec.europa.eu. The new European Health Data Space obliges providers to offer standardized electronic records from March 2025, positioning compliant software firms for continent-wide scale. Early alignment to these requirements is already visible in Germany’s electronic patient record upgrade and France’s Health Data Hub expansion.

Ageing Population & Chronic-Care Demand

European demographics skew older: chronic diseases now absorb more than 70% of health spending, while the region faces a projected 1.8 million clinician shortfall by 2030. National budgets are pivoting to remote patient monitoring programs that relieve hospital capacity. Italy’s Recovery and Resilience Plan alone allocates EUR 15.62 billion to community-based digital care, accelerating the roll-out of home telemetry platforms that handle high-risk cardiac, diabetic, and respiratory cohorts.

Telehealth Normalisation Post-COVID-19

Teleconsultations have stabilized at 1.4 visits per capita versus 0.6 pre-pandemic across OECD Europe [2]OECD, “Health at a Glance: Europe 2024,” oecd.org . Regulatory frameworks now embed virtual visits inside core benefits, removing pilot status. France mandates full Social Security reimbursement for accredited providers, while the United Kingdom adds remote follow-up metrics to hospital funding contracts. Vendors that merge video, messaging, and AI triage into a single interface gain purchaser preference as systems seek long-term productivity savings.

Cross-Border ePrescription & eID Interoperability

MyHealth@EU services already allow citizens from 14 member states to redeem ePrescriptions across borders. The European Electronic Health Record Exchange Format widens scope to imaging and laboratory results by 2026, creating new revenue pools for secure identity and consent-management solutions. Early adopters in Estonia and Finland demonstrate pharmacy cost reductions and fewer prescription errors, building the case for pan-EU deployment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR-Driven Data-Privacy Complexity | -2.1% | EU-27, with highest compliance costs in Germany, France | Short term (≤ 2 years) |

| High Upfront Digitalisation Costs For SMEs | -1.8% | EU-27, particularly affecting Southern and Eastern Europe | Medium term (2-4 years) |

| Fragmented Reimbursement Across EU-27 | -1.6% | EU-27, with highest impact in Southern and Eastern Europe | Long term (≥ 4 years) |

| Digital-Skill Gaps In Clinical Workforce | -1.3% | EU-27, with acute shortages in Germany, Netherlands, Nordic countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GDPR-Driven Data-Privacy Complexity

Strict personal-health-data rules add procurement friction. The European Parliament estimates GDPR has generated EUR 53 billion in cumulative compliance costs for SMEs engaged in digital transformation. Every new remote-monitoring launch must implement data minimization, patient consent, and immutable logging. Emerging AI-based devices also face dual oversight under the forthcoming EU AI Act, lengthening certification timelines and increasing legal spend.

High Upfront Digitalisation Costs for SMEs

Infrastructure, integration, and training packages often exceed the capital capacity of smaller clinics. Germany’s Krankenhauszukunftsfonds disbursed EUR 4.3 billion to upgrade hospital IT, yet many facilities still postpone full deployments because matching funds and skilled staff are scarce. Access to venture finance has tightened: European digital-health start-ups raised USD 1.1 billion in 2023 versus USD 3 billion in 2021, slowing innovation diffusion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Dominate While Software Accelerates

Services retained 38.34% revenue in 2025 because Europe’s heterogeneous health-system landscape requires extensive customization and change management. Yet software revenue is set to grow at an 18.6% CAGR, signalling migration toward configurable platforms that minimize repetitive consulting engagements. Hardware continues to post steady orders for connected sensors and imaging peripherals, aided by EU funding schemes that subsidize device upgrades eligible for hospital modernisation grants.

The component mix reflects a transitional phase where hospitals replace siloed applications with unified interoperability suites. Siemens Healthineers’ Teamplay Digital Health Platform added AI diagnostic modules and discharge-planning tools in 2024, enabling providers to license new functionality without extra integration overhead . Such plug-in ecosystems reduce total cost of ownership and accelerate multi-country rollouts. Continued software expansion is expected to raise software’s share of Europe digital health market size to over 32% by 2031.

By Technology: Telehealth Leadership Faces mHealth Disruption

Telehealth accounted for 46.55% of Europe digital health market size in 2025 thanks to permanent reimbursement codes and clinician familiarity with video workflows. mHealth, however, is projected to deliver the fastest 18.78% CAGR as smartphone penetration exceeds 90% and payers reimburse evidence-based digital therapeutics. Analytics and digital health systems gain momentum as AI image reconstruction and clinical-decision support are mandated under several hospital-investment frameworks.

Consumer uptake fuels the shift: Philips SmartSpeed Precise MRI, powered by dual AI engines, shortens scan times by 3× and improves image clarity by 80%. Simultaneously, Omron’s acquisition of Luscii extends remote-monitoring capabilities to 150 disease pathways, allowing clinicians to adjust regimens using real-time data feeds. These cross-device integrations intensify technology competition, particularly in chronic-care verticals.

By End User: Patient Empowerment Reshapes Demand

Patients and consumers held 42.10% of 2025 revenue, benefiting from direct-to-customer subscription models and nationwide appointment-booking portals. Payers are poised for the strongest 18.55% CAGR as value-based contracting rewards platforms that prove cost offsets and carbon-footprint reductions. Providers still command sizable budget authority, but funding is increasingly ring-fenced for solutions demonstrating measurable productivity gains.

Germany’s Digital Health Care Act (DVG) lets certified apps secure reimbursement for roughly 90% of the insured population, setting a template for other jurisdictions. Evidence from remote-monitoring trials shows 97% lower CO₂ emissions than in-clinic screening while maintaining quality outcomes. As environmental reporting grows compulsory, payers prefer digital pathways that meet both clinical and sustainability targets, expanding uptake throughout the Europe digital health industry.

By Mode of Delivery: Cloud Infrastructure Anchors Scalability

Cloud-based solutions captured 56.90% of Europe digital health market share in 2025 as providers embraced elastic compute, managed security, and rapid feature release cycles. On-premise models, though smaller, are forecast to post 18.95% CAGR because high-risk AI and genomic datasets often remain within sovereign data centers to satisfy GDPR and forthcoming AI-Act stipulations.

Philips broadened its Imaging Cloud on Amazon Web Services in February 2025, giving European clinicians remote access to radiology studies on a single federated platform. Hybrid architectures that cache sensitive data locally but orchestrate analytics in the cloud are gaining traction, fulfilling the European Health Data Space security tiers. Vendors able to deliver identical user experiences across both deployment modes win multi-country tenders.

By Application: Chronic Disease Platforms Take the Lead

Chronic disease management generated 28.25% of revenue in 2025 and remains a cornerstone of national e-health roadmaps. Fitness and wellness apps are set for the swiftest 19.18% CAGR, buoyed by wearable sensors that translate activity data into preventive care insights. Remote patient monitoring, diagnostics, medication adherence, and hospital workflow solutions round out the portfolio.

The European Cancer Imaging Initiative will provide more than 100,000 anonymized cases and at least 50 AI algorithms by 2025, fast-tracking diagnostic AI adoption. Hospital workflow modules likewise gain momentum: Siemens’ Luminos Q.namix integrates dose tracking and staffing dashboards to raise radiology productivity. Integration depth across these applications underpins a holistic continuum-of-care approach.

Geography Analysis

Germany sustained its leadership with 23.10% of Europe digital health market share in 2025, underpinned by 64 DiGA-approved applications that generated over EUR 125 million in reimbursable revenue. The Krankenhauszukunftsfonds finances cybersecurity and interoperability upgrades for 1,900 hospitals, anchoring demand through 2027. Electronic patient records (ePA) became mandatory on an opt-out basis in January 2025, creating a nationwide data backbone that accelerates vendor scale-up.

The United Kingdom recorded the highest 19.25% CAGR outlook to 2031, supported by a GBP 3.4 billion NHS technology envelope focused on a unified patient record and ambient-voice clinical documentation pilots. Regulatory sandboxes administered by the Medicines and Healthcare products Regulatory Agency streamline AI device approval, fostering a vibrant start-up pipeline. However, departmental restructuring of NHS England in 2025 may create interim funding volatility.

France, Italy, and Spain illustrate different adoption curves. France formalized teleconsultation billing and launched the PECAN fast track that reimburses evidence-based apps within six weeks. Italy’s EUR 15.62 billion community-care digitalization plan targets 1,350 local health hubs, yet regional skill gaps slow execution. Spain relies heavily on EU structural funds for e-prescription expansion, while Nordic states maintain near-universal electronic record use, enabling early pilots in cross-border data exchange.

Competitive Landscape

Europe’s vendor ecosystem is fragmented: the top five suppliers control under 20% of total revenue, leaving ample room for regional specialists. Market leaders leverage multi-modal AI portfolios, compliance expertise, and cloud alliances to secure framework agreements. Siemens Healthineers’ Teamplay Connect added wound-management and discharge modules in December 2024, strengthening its platform moat. Philips counters with AI-augmented SmartSpeed MRI and imaging cloud distribution on AWS, ensuring modality breadth and rapid update cycles.

Device manufacturers increasingly acquire software IP: Omron’s 2024 purchase of Luscii gives it instant scale in remote-monitoring protocols across 70% of Dutch hospitals. Start-ups differentiate through vertical depth—exemplified by digital therapeutics for mental health and metabolic disease—yet must navigate complex multi-country reimbursement. Platforms that embed pre-configured GDPR and AI-Act controls gain procurement preference, shrinking the addressable market for point solutions.

Consolidation is expected as funding tightens: cross-border mergers allow firms to pool regulatory talent and achieve the ISO-certified design controls required by high-risk AI legislation. Meanwhile, telecom operators and cloud hyperscalers partner with hospital groups to deliver edge-compute services, signaling non-traditional entrants’ interest in capturing infrastructure layers of the Europe digital health market.

Europe Digital Health Industry Leaders

Koninklijke Philips NV

AMD Global Telemedicine Inc.

Allscripts Healthcare Solutions Inc.

International business Machinery Corporation (IBM)

Cerner Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Philips expanded its radiology informatics cloud on AWS to European data centers, providing remote diagnostic reading capabilities with integrated AI post-processing.

- December 2024: Siemens Healthineers unveiled Luminos Q.namix, a fluoroscopy and radiography platform with AI-guided workflows and dual configuration options.

- April 2024: Omron Healthcare completed its acquisition of Luscii, adding multi-condition remote-monitoring software deployed in 70% of Netherlands hospitals.

Europe Digital Health Market Report Scope

As per the scope of the report, digital health refers to tools and services that make use of information and communication technologies (ICTs) to improve the prevention, diagnosis, treatment, monitoring, and management of health-related disorders, as well as to track and manage unhealthy lifestyle choices. The Europe digital health market is segmented by Component (Hardware, Software, and Other Components), Technology (Telehealthcare, Mobile Health, Health Analytics, and Digital Health Systems), Mode of Delivery (On-premise Delivery and Cloud-based Delivery), and Geography (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe). The report offers the value (in USD million) for the above segments.

By Component

| Hardware |

| Software |

| Services |

By Technology

| Telehealth |

| mHealth |

| Health Analytics |

| Digital Health Systems |

By End User

| Healthcare Providers |

| Payers |

| Patients & Consumers |

By Mode of Delivery

| On-premise Delivery |

| Cloud-based Delivery |

By Application

| Chronic Disease Management |

| Remote Patient Monitoring |

| Fitness & Wellness |

| Diagnostics & Imaging |

| Medication Management |

| Hospital Workflow Management |

Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Component | Hardware |

| Software | |

| Services | |

| By Technology | Telehealth |

| mHealth | |

| Health Analytics | |

| Digital Health Systems | |

| By End User | Healthcare Providers |

| Payers | |

| Patients & Consumers | |

| By Mode of Delivery | On-premise Delivery |

| Cloud-based Delivery | |

| By Application | Chronic Disease Management |

| Remote Patient Monitoring | |

| Fitness & Wellness | |

| Diagnostics & Imaging | |

| Medication Management | |

| Hospital Workflow Management | |

| Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How big is the Europe Digital Health Market?

The Europe Digital Health Market size is expected to reach USD 113.94 billion in 2026 and grow at a CAGR of 17.85% to reach USD 258.74 billion by 2031.

Which component segment is growing fastest?

Software is forecast to expand at an 18.6% CAGR, reflecting a move toward configurable platforms across the region.

Who are the key players in Europe Digital Health Market?

Koninklijke Philips NV, AMD Global Telemedicine Inc., Allscripts Healthcare Solutions Inc., International business Machinery Corporation (IBM) and Cerner Corporation are the major companies operating in the Europe Digital Health Market.

How large is Germany’s share of the Europe digital health market?

Germany accounts for 23.10% of total 2025 revenue, anchored by its DiGA reimbursement framework.

Page last updated on: