4D Printing In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 43.78 Million |

| Market Size (2031) | USD 137.33 Million |

| Growth Rate (2026 - 2031) | 25.69% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

4D Printing In Healthcare Market Analysis by Mordor Intelligence

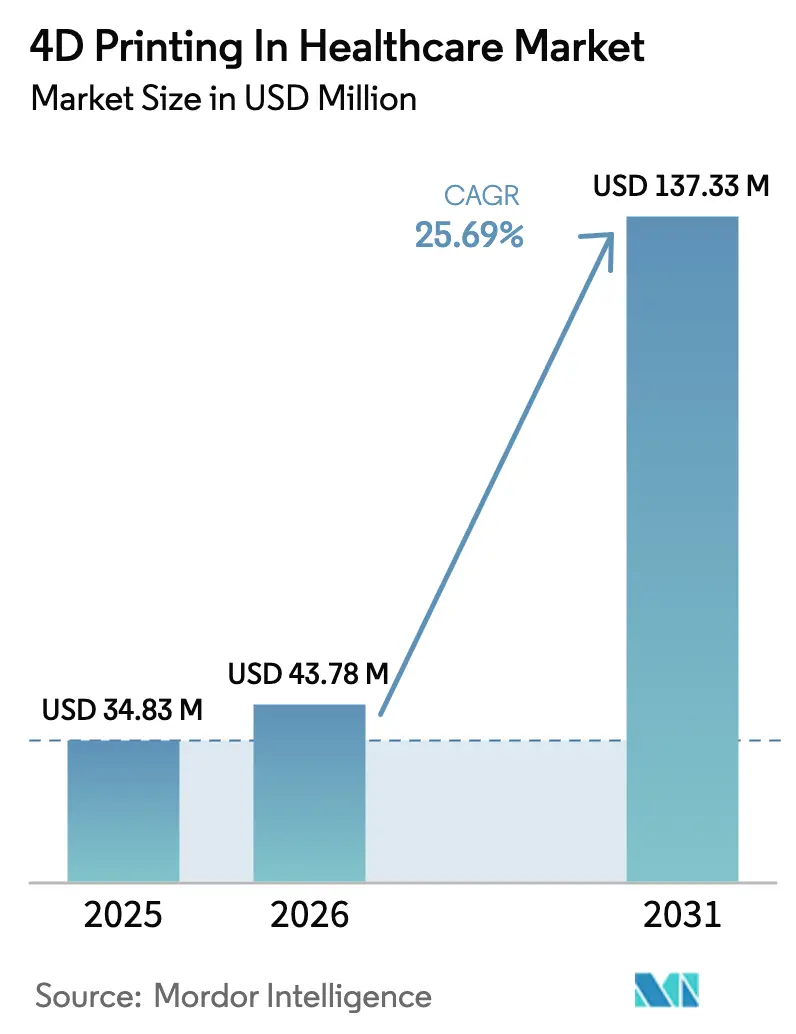

The 4D Printing In Healthcare Market size is expected to grow from USD 34.83 million in 2025 to USD 43.78 million in 2026 and is forecast to reach USD 137.33 million by 2031 at 25.69% CAGR over 2026-2031.

Transplant-organ scarcity, rapidly maturing AI-enabled design suites, and the shift toward programmable biomaterials that remodel in vivo are amplifying demand. Direct Ink Writing platforms now deposit living cells and stimuli-responsive hydrogels in a single build, compressing bench-to-bedside timelines. Government programs such as the ARPA-H PRINT initiative, which earmarks USD 500 million to bioprinted-organ research through 2029, validate public-sector confidence in fourth-dimensional technologies. Meanwhile, FDA 510(k) clearances for temperature-activated bone scaffolds and patient-specific cranio-maxillofacial implants are lowering regulatory barriers. Venture investors funneled more than USD 1 billion into bioprinting start-ups during 2025 alone, accelerating clinical translation and nudging hospitals to establish point-of-care manufacturing labs.

Key Report Takeaways

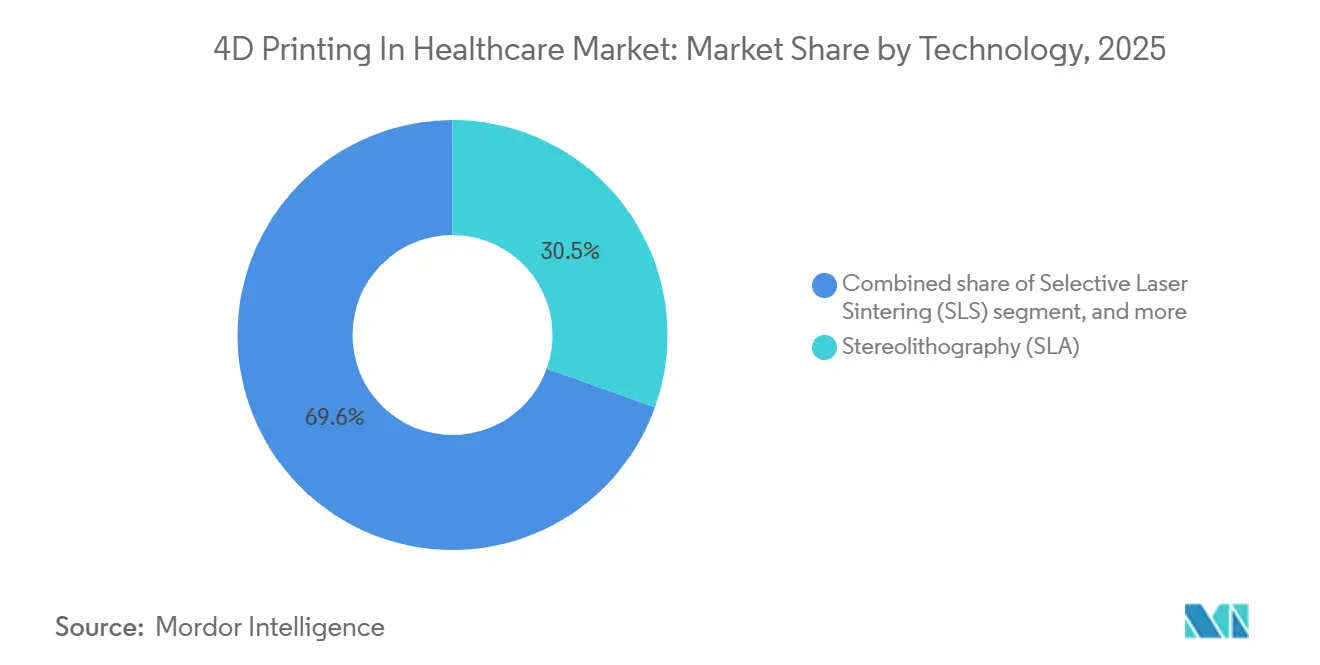

- By technology, stereolithography led the 4D printing in healthcare market with 30.45% market share in 2025; Direct ink writing is advancing at a 26.76% CAGR through 2031.

- By application, tissue engineering & regenerative medicine commanded 38.32% revenue share in 2025, whereas Cancer Therapeutics is projected to expand at 27.54% CAGR to 2031.

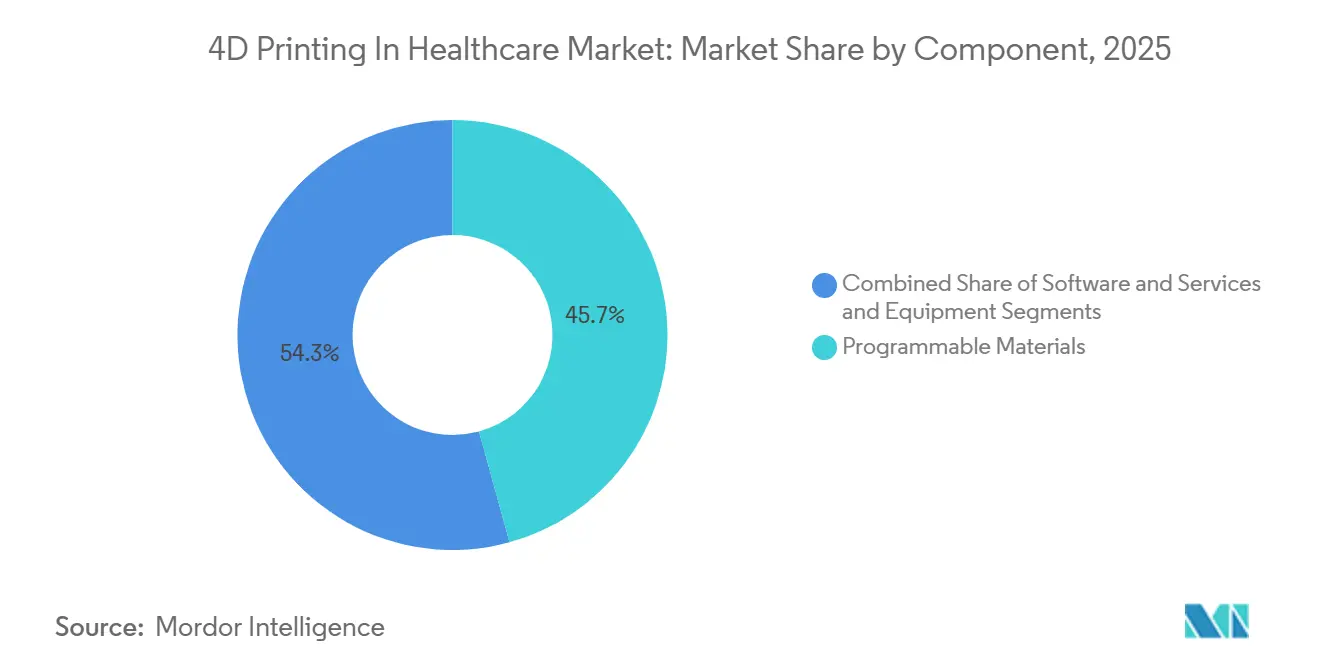

- By Component, programmable materials accounted for 45.73% of component spending in 2025 and are set to maintain a 26.43% CAGR through 2031.

- By end-user, research institutes & academic labs captured 41.34% share in 2025; Pharmaceutical & biotech companies record the highest projected CAGR at 27.43% over 2026-2031.

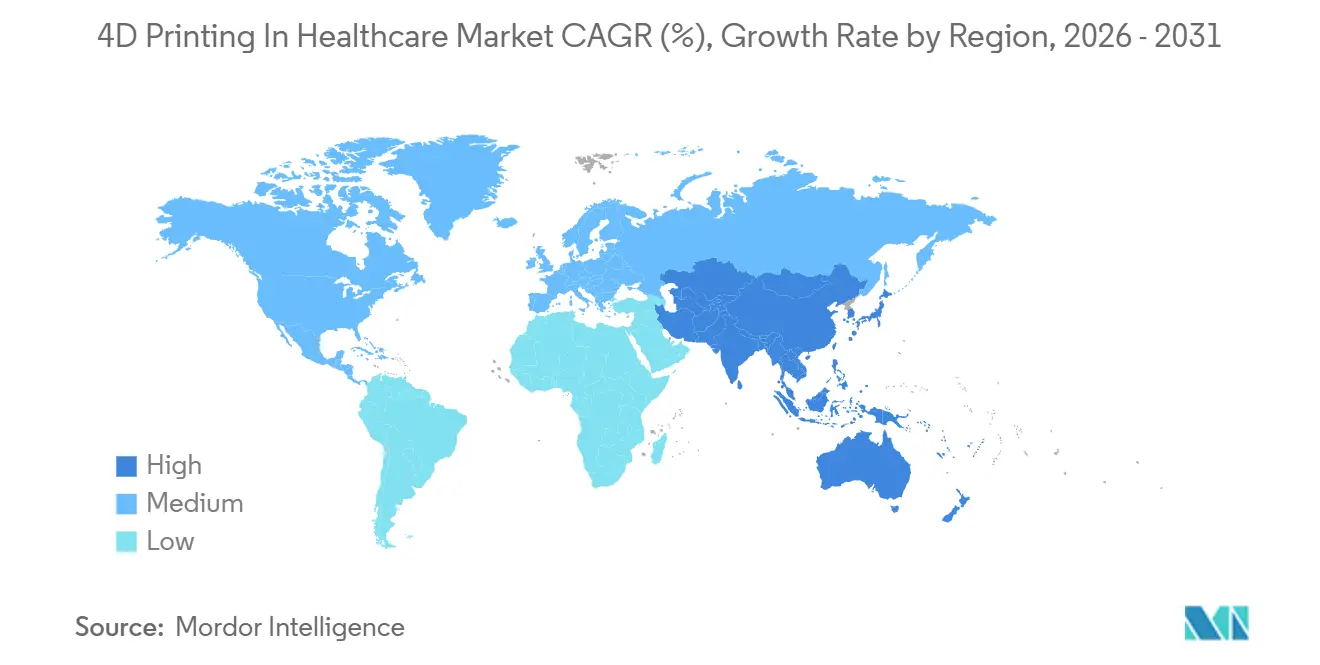

- By geography, North America held 39.76% of revenue in 2025, while Asia-Pacific is forecast to grow at 26.56% CAGR, the fastest regional pace, through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global 4D Printing In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Organ Transplant Shortages | +5.2% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Rising Bioprinting R&D Investments | +4.8% | North America, Asia-Pacific | Medium term (2-4 years) |

| Shift Toward Personalized Medicine | +4.3% | Global, early adoption in North America and Western Europe | Medium term (2-4 years) |

| Breakthroughs in Smart Biomaterials | +3.9% | Global, R&D hubs in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Artificial Intelligence Enabled Design Automation | +3.7% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Expansion of Point-of-Care Manufacturing | +3.8% | North America, Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Organ Transplant Shortages

Only 130,000 solid-organ procedures take place worldwide each year, meeting just 10% of global demand. In the United States, 103,223 patients were on transplant waiting lists in December 2024, and 17 people died daily while awaiting organs[1]United Network for Organ Sharing, “Data Reports,” unos.org. These deficits are pushing federal agencies to bankroll bioprinting; ARPA-H’s PRINT program began disbursing USD 500 million in March 2024 to companies engineering transplantable tissues. United Therapeutics and 3D Systems aim to begin first-in-human lung-scaffold trials in 2026, potentially validating printed organs for clinical transplantation. Pediatric shortages are even more severe, motivating research into constructs that grow with young recipients to reduce the lifetime costs of immunosuppression.

Rising Bioprinting R&D Investments

Aspect Biosystems closed a USD 115 million Series B in January 2025 and secured a CAD 200 million federal partnership to scale vascularized-tissue production. Europe-based 4D Medicine attracted GBP 3.4 million in August 2024 for its degradable “4Degra” platform, while Berlin’s Cellbricks raised EUR 5 million in September 2024 for modular bioinks. South Korea named T&R Biofab a national R&D priority for 2025, funding extracellular-matrix bioinks and airway implants. China’s 14th Five-Year Plan offers fast-track approvals for bioprinted devices, catalyzing venture inflows that topped RMB 190 billion in 2025. These capital infusions are building GMP suites that bridge research prototypes to commercial supply.

Shift Toward Personalized Medicine

Bioprinted tumor organoids now guide patient-specific chemotherapy regimens, curbing trial-and-error dosing and toxicity. Hospitals fabricate cranio-maxillofacial implants directly from CT scans within 24 hours, shrinking OR time by 20 minutes on average across the U.S. Veterans Affairs network. Smart orthotics, printed with embedded sensors, adjust stiffness in real time to match gait, replacing static braces. The European Medicines Agency’s September 2025 horizon scan on Engineered Living Materials underscores that adaptive implants require new classification rules[2] European Medicines Agency, “Engineered Living Materials Horizon Scan,” ema.europa.eu. As regulatory clarity grows, demand for truly individualized devices is expected to accelerate.

Breakthroughs in Smart Biomaterials

PrintBio gained FDA 510(k) clearance in May 2025 for a temperature-triggered bone scaffold that conforms to irregular defects. ROKIT Healthcare unveiled an AI-guided skin-regeneration system in October 2025 that tailors bioink recipes to diabetic-wound profiles. T&R Biofab’s decellularized “deCelluid” bioink has Korean approval for vascular and airway grafts, marking a rare regulatory nod for ECM-based materials. Multi-responsive hydrogels under development release oncology drugs at acidic tumor pH, thereby limiting systemic exposure. Collectively, these materials expand clinical possibilities beyond inert plastics.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital and Material Expenditure | -2.1% | Global, acute in emerging markets and smaller institutions | Short term (≤ 2 years) |

| Regulatory and Standards Ambiguity | -1.8% | Global, fragmented across North America, EU, Asia | Medium term (2-4 years) |

| Limited Long-Term Clinical Evidence | -1.6% | Global, limiting reimbursement | Long term (≥ 4 years) |

| Data Security and IP Concerns | -1.3% | Global, heightened in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Material Expenditure

A hospital-grade multi-material printer plus incubators and bioreactors can exceed USD 500,000, sidelining smaller clinics. Smart polymers and ECM bioinks cost 3-5 times as much as standard thermoplastics, squeezing margins. T&R Biofab’s decellularization workflow adds quality-control steps, elevating unit costs. Lack of reimbursement codes forces providers to justify case-by-case payments. Leasing and subscription programs lower entry barriers but transfer servicing risks to vendors.

Regulatory and Standards Ambiguity

Neither the FDA nor the EMA has issued 4D-specific rules, leaving firms to shoehorn adaptive devices into static-implant categories. Japan’s dual-approval path for AI-embedded platforms adds paperwork, while Latin American agencies are only drafting additive manufacturing guidelines. Absent ISO standards tailored to living-cell viability and stimuli response, quality systems default to general ASTM 52900 protocols that omit key safety checkpoints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Direct Ink Writing Gains on Versatility

Direct Ink Writing captured the fastest growth trajectory at 26.76% CAGR, reflecting its capability to co-deposit cells, hydrogels, and thermoplastics without UV curing. This flexibility positions the technology to command a larger slice of the 4D printing in healthcare market over the forecast horizon. Stereolithography accounted for 30.45% of 4D printing market share in 2025 because its high resolution suits dental and cranio-maxillofacial implants, yet its dependence on photoinitiators limits live-cell viability.

ROKIT Healthcare’s INVIVO system demonstrates clinical scalability by printing skin and cartilage constructs in South American hospitals. FDA clearance of PrintBio’s shape-memory bone scaffold endorsed stimuli-responsive polymers for orthopedics. Selective Laser Sintering and Fused Deposition Modeling remain relevant in load-bearing implant prototypes, but neither supports living-cell deposition without costly post-processing. PolyJet and Material Jetting, valued for their gradient structures, are penetrating the wearable orthotics market, whereas Digital Light Processing is consolidating in dental aligners.

By Application: Cancer Therapeutics Accelerates

Cancer Therapeutics is projected to post the highest CAGR of 27.54%, buoyed by tumor organoids that pre-screen regimens and by personalized vaccine scaffolds under development. Tissue Engineering & Regenerative Medicine accounted for 38.32% of revenue in 2025, underscoring its status as the most mature segment of the 4D printing in healthcare market.

VivoSim Labs (formerly Organovo) showcased Phase 2 liver fibrosis data that corroborate the use of printed tissues as drug-metabolism stand-ins. Hospitals deploying point-of-care printers fabricate patient-specific cranial implants in under 24 hours, shrinking backlog queues. Drug-delivery capsules that uncoil in acidic tumor microenvironments are under Phase I review, while smart orthotics that adapt stiffness to gait patterns represent untapped white space for athletic rehabilitation.

By Component: Programmable Materials Dominate Spending

Programmable Materials accounted for 45.73% of 2025 expenditure and are set to expand at 26.43% CAGR, outpacing equipment investments. Their adaptive properties allow implants to remodel alongside healing tissue, cutting revision-surgery rates and thereby capturing a premium share of the 4D printing in healthcare market.

T&R Biofab’s FDA-approved ECM ink and PrintBio’s thermally triggered scaffold validate regulatory pathways for complex chemistries. Equipment remains the second-largest outlay, with multi-material printers priced above USD 500,000. Software & Services are growing as AI modules from Autodesk and Materialise integrate directly with hospital PACS networks, shortening design iterations by 90%.

By End User: Pharma & Biotech Surge

Academic laboratories held 41.34% of the 4D printing in healthcare market size in 2024. Multidisciplinary teams combine materials science, cell biology and computational modeling to develop organ-scale constructs that meet pre-clinical milestones. Their publications spur partnerships with device companies seeking translational know-how. Pharmaceutical and biotech firms, forecast to expand at 27.43% CAGR, integrate 4D platforms into drug-screening workflows, enabling dynamic tumor models that better predict in-vivo efficacy.

Hospitals adopt compact printers for on-demand surgical guides and adaptive implants, particularly in orthopedic oncology where margins and timing are critical. Contract manufacturers bridge capability gaps for community hospitals, providing ISO-compliant production as a service and broadening downstream access to the 4D printing in healthcare market.

Geography Analysis

North America contributed 39.76% of 2025 revenue, anchored by FDA clearances for custom cranio-maxillofacial implants and ARPA-H’s USD 500 million PRINT grants. United Therapeutics and 3D Systems plan first-in-human lung-scaffold trials in 2026, which could validate the use of transplantable organs. Canada’s CAD 200 million investment in Aspect Biosystems underscores the government's commitment.

Asia-Pacific is the fastest-growing region, with a 26.56% CAGR. South Korea funds T&R Biofab’s ECM vascular bioinks, while ROKIT Healthcare prepares FDA access for its cartilage platform. China’s express approval pathway under its 14th Five-Year Plan and RMB 190 billion VC inflows further energize adoption. Japan’s PMDA cybersecurity rules offer a balanced framework for AI-driven devices[3]Pharmaceuticals and Medical Devices Agency, “AI-Device Cybersecurity Guidance,” pmda.go.jp.

Europe ranks second in 2025 revenue, yet reimbursement fragmentation slows uptake despite the EMA’s call for harmonized standards. Latin America and the Middle East remain early-stage; ROKIT Healthcare’s deployments in Chile and Argentina show potential, but capital and regulatory gaps persist.

Competitive Landscape

The market is moderately fragmented: legacy additive-manufacturing leaders 3D Systems and Stratasys compete with specialist bioprinting firms such as VivoSim Labs and CELLINK’s BICO Group. Partnerships are proliferating; 3D Systems and United Therapeutics co-develop lung scaffolds, while equipment vendors acquire bioink start-ups to offer vertical stacks. Start-ups like T&R Biofab and ROKIT Healthcare leverage government designations to scale rapidly in Asia and South America.

Patent races now center on stimuli-responsive materials and AI design algorithms. CMOs position themselves as indispensable intermediaries, offering GMP capacity and regulatory expertise attractive to pharma clients. Data-security mandates are prompting vendors to integrate encryption and role-based access controls, adding a cybersecurity layer to competitive differentiation.

4D Printing In Healthcare Industry Leaders

Stratasys Ltd

3D Systems Corp

Organovo Holdings Inc.

Cellink (BICO Group)

Poietis SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: ROKIT Healthcare unveils AI-driven skin-regeneration platform at Plastic Surgery The Meeting.

- May 2025: PrintBio obtains FDA clearance for 3DMatrix DynaFlex shape-memory scaffold.

- April 2025: Organovo rebrands as VivoSim Labs to focus on bioprinted tissue models.

- January 2025: Aspect Biosystems secures USD 115 million Series B to scale vascularized-tissue production.

Global 4D Printing In Healthcare Market Report Scope

4D printing in healthcare aims to construct complex forms that can transform their properties upon response to internal or external stimuli to repair, replace, or regrow diseased or damaged tissues, cells, and organs.

The market for 4D printing in healthcare is segmented by technology, application, component, end user, and geography. By technology, the market is segmented into stereolithography, selective laser sintering (SLS), polyjet, and fusion deposition modeling (FDM). The market is segmented into tissue engineering, drug delivery, and patient-specific implant by application. By component, the market is divided into software and services, equipment, and programmable material. By end user, the market is segmented into hospitals and clinics, research institutes, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa and South America. The report covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers value (USD) for all the above segments.

| Stereolithography (SLA) |

| Selective Laser Sintering (SLS) |

| PolyJet / Material Jetting |

| Fused Deposition Modelling (FDM) |

| Direct Ink Writing (DIW) |

| Digital Light Processing (DLP) |

| Multi-Jet Fusion (MJF) |

| Tissue Engineering & Regenerative Medicine |

| Drug & Cell Delivery Systems |

| Patient-Specific Implants & Prosthetics |

| Surgical Instruments & Guides |

| Wearable / Smart Orthotics |

| Dental & Cranio-Maxillofacial |

| Cancer Therapeutics |

| Software & Services |

| Equipment (4D Printers & Ancillary) |

| Programmable Materials |

| Hospitals & Clinics |

| Research Institutes & Academic Labs |

| Pharmaceutical & Biotech Companies |

| Contract Manufacturing Organizations (CMOs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Stereolithography (SLA) | |

| Selective Laser Sintering (SLS) | ||

| PolyJet / Material Jetting | ||

| Fused Deposition Modelling (FDM) | ||

| Direct Ink Writing (DIW) | ||

| Digital Light Processing (DLP) | ||

| Multi-Jet Fusion (MJF) | ||

| By Application | Tissue Engineering & Regenerative Medicine | |

| Drug & Cell Delivery Systems | ||

| Patient-Specific Implants & Prosthetics | ||

| Surgical Instruments & Guides | ||

| Wearable / Smart Orthotics | ||

| Dental & Cranio-Maxillofacial | ||

| Cancer Therapeutics | ||

| By Component | Software & Services | |

| Equipment (4D Printers & Ancillary) | ||

| Programmable Materials | ||

| By End User | Hospitals & Clinics | |

| Research Institutes & Academic Labs | ||

| Pharmaceutical & Biotech Companies | ||

| Contract Manufacturing Organizations (CMOs) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

Which technology is growing fastest in 4D printing for healthcare?

Direct Ink Writing is advancing at 26.76% CAGR due to its ability to co-print living cells, hydrogels, and thermoplastics without UV exposure.

What is the main driver behind adopting 4D printing for organs?

Chronic shortages in transplantable organs, with only 10% of global demand met, are steering investment toward bioprinted alternatives.

Why are programmable materials critical to this field?

Shape-memory polymers and stimuli-responsive hydrogels let implants conform, remodel, or release drugs in vivo, raising clinical success rates despite higher material costs.

Which region leads current revenue, and which is growing fastest?

North America leads with 39.76% revenue share, while Asia-Pacific posts the highest 26.56% CAGR through 2031.

How are pharmaceutical companies using 4D printing?

Drug makers outsource organoid production to CMOs and integrate in-house printers to screen therapies on patient-specific tissues, speeding preclinical phases.

What regulatory changes are anticipated?

Both FDA and EMA are expected to release 4D-specific guidance within four years as adaptive implants mature, aiming to harmonize classification and post-market surveillance.

Page last updated on: