Digital Labeling Machines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

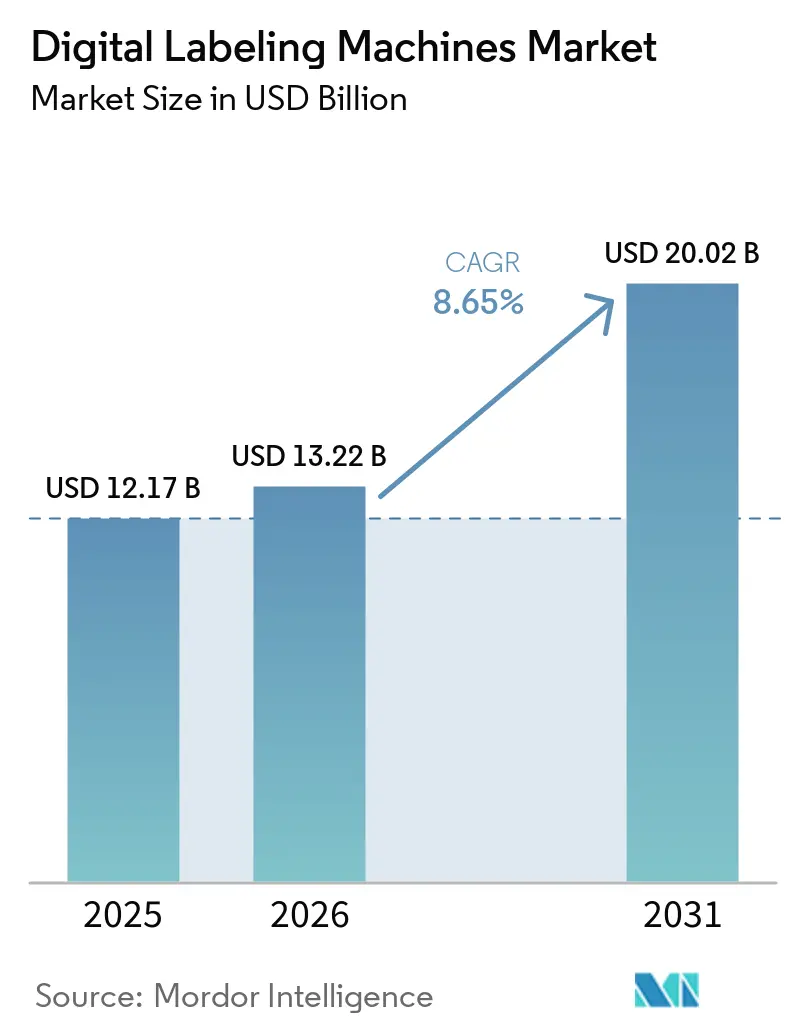

| Market Size (2026) | USD 13.22 Billion |

| Market Size (2031) | USD 20.02 Billion |

| Growth Rate (2026 - 2031) | 8.65% CAGR |

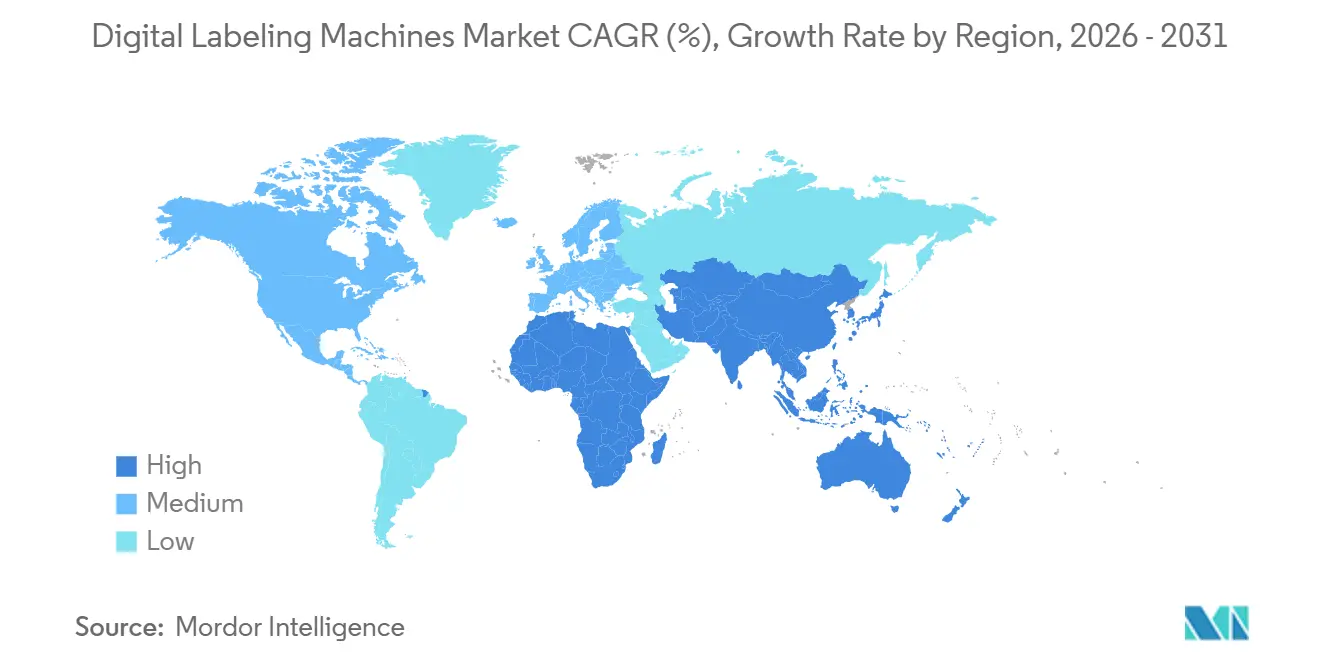

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Labeling Machines Market Analysis by Mordor Intelligence

The digital labeling machines market size was valued at USD 12.17 billion in 2025 and was estimated to grow from USD 13.22 billion in 2026 to reach USD 20.02 billion by 2031, at a CAGR of 8.65% during the forecast period (2026-2031). A decisive shift toward on-demand, variable-data workflows is unfolding as brands pursue serialization compliance, versioned promotions, and hyper-localized packaging. Regulatory rules requiring end-to-end traceability are driving accelerated equipment replacement, while e-commerce fulfillment models rely on real-time label generation to keep parcel flows moving. Converters are equally motivated by economics, such as digital presses eliminating plate costs, reducing changeover downtime, and slashing waste, which is critical as median run lengths keep falling. Competitive vendors are enlarging software stacks that automate color management and data handling, turning presses into workflow hubs rather than isolated hardware.

Key Report Takeaways

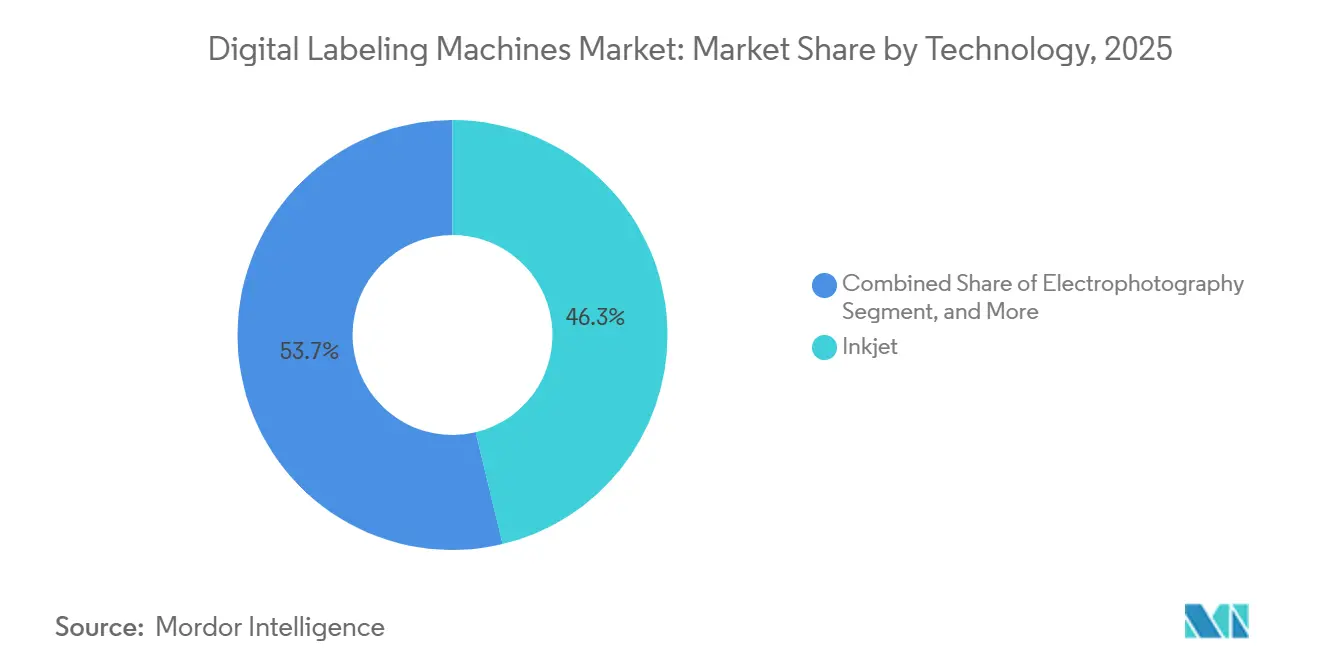

- By technology, inkjet systems led with 46.27% of the digital labeling machines market share in 2025, whereas hybrid configurations that blend digital heads with flexographic stations are forecast to advance at an 8.91% CAGR through 2031.

- By machine type, print-and-apply platforms accounted for 40.85% of the digital labeling machines market share in 2025, while desktop and benchtop units represent the fastest-growing segment with an 8.82% CAGR.

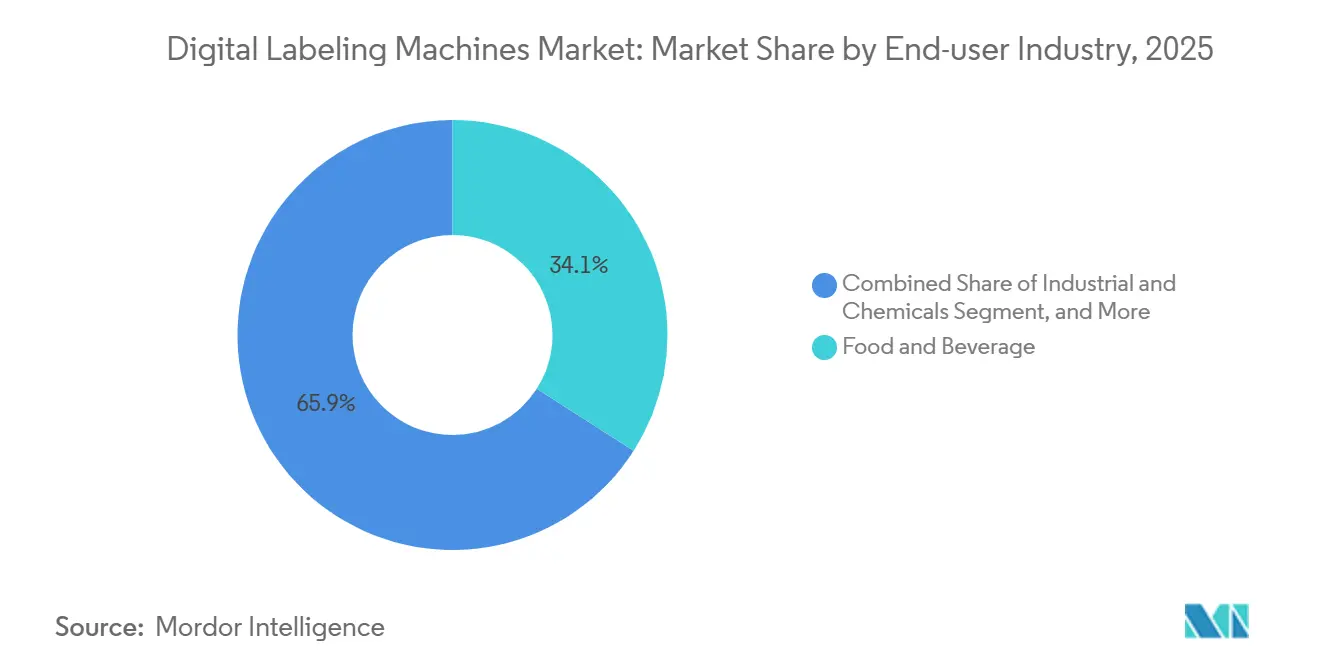

- By end user, food and beverage applications contributed 32.13% of the digital labeling machines market share in 2025, yet e-commerce and logistics are projected to expand at an 8.77% CAGR during 2026-2031.

- By geography, Asia-Pacific held the largest position at 38.44% of the digital labeling machines market share in 2025, and Africa is poised to record the highest regional growth at 9.13% over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Digital Labeling Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Push for Traceability and Serialization in Food and Pharma Supply Chains | +1.8% | Global, Europe and North America lead, Asia-Pacific following | Medium term (2-4 years) |

| Rising Demand for Variable Data Printing in Packaging | +1.5% | Global, focused in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Increasing Adoption of Just-In-Time Labeling in E-Commerce Fulfillment | +1.3% | Global, Asia-Pacific core, spill-over to North America, Europe | Short term (≤ 2 years) |

| Shift From Analog to Digital Printing for Shorter Label Runs | +1.1% | Global, craft beverage and personal care hot spots | Medium term (2-4 years) |

| Proliferation of Smart Labels Integrating NFC/RFID | +0.9% | Global, mature economies first | Long term (≥ 4 years) |

| Surging Investments in Sustainable Water-Based Inkjet Technology | +0.7% | Europe and North America drive, Asia-Pacific trails | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Push for Traceability and Serialization in Food and Pharma Supply Chains

Pharmaceutical directives such as the United States Drug Supply Chain Security Act and the European Union Falsified Medicines Directive require every finished-dose unit to carry a unique identifier that can be verified at each hand-off, something flexographic lines struggle to deliver without pre-printed roll stock. Digital presses meet the mandate by printing serialized two-dimensional codes on demand at commercial line speeds, allowing contract packagers to avoid idle inventory when batch numbers change mid-campaign. Similar dynamics play out in high-risk food categories following Section 204 of the FDA Food Safety Modernization Act, which extended lot-level traceability to fresh produce, seafood, and dairy. The ability to encode harvest date, origin farm, and cold-chain touchpoints in real time is now table stakes for exporters. European Union Farm to Fork policy uses the same compliance lever, nudging small olive-oil and cheese cooperatives toward desktop inkjet units that fit inside cramped packing sheds.[1]European Commission, “Farm to Fork Strategy,” ec.europa.eu Collectively, these statutes shorten the replacement cycle for legacy flexographic equipment and keep the digital labeling machines market on a steep growth trajectory.

Rising Demand for Variable Data Printing in Packaging

Brand managers are leveraging variable-data print streams to run micro-targeted promotions and embed QR codes that link shoppers to localized content, such as recipe videos or loyalty apps. Median job sizes have collapsed from 50,000 impressions in 2020 to 12,000 in 2025, crossing the point at which digital presses deliver a lower per-unit cost once plates, wash-ups, and setup labor are factored in. Craft brewers have become repeat buyers, spinning out seasonal labels for dozens of small-batch SKUs without carrying a warehouse of obsolete stock. Pharmaceutical marketers extend the paradigm to patient-centric leaflets that dynamically adjust dosage language by destination country. Even cosmetics in South Korea are pivoting to benchtop units to print 500-label bursts tied to influencer drops that must ship within 72 hours.

Increasing Adoption of Just-In-Time Labeling in E-Commerce Fulfillment

Automated fulfillment centers now position industrial print-and-apply heads directly over conveyor runs, generating shipping, customs, and return labels for each parcel as it is inducted into ZPL.AI. Real-time carrier selection means the label cannot be pre-printed because route and duty status are calculated milliseconds before application. Operators report an 8-12% reduction in logistics costs from eliminating pre-printed rolls and reducing mis-shipments. Barcode first-read rates above 99.7% are normal, aided by thermal-transfer ribbons optimized for high-speed scanning. As cross-border e-commerce swells, the same engine must also apply CE marks, WEEE symbols, and recycling pictograms on demand, further locking in the digital approach.

Shift From Analog to Digital Printing for Shorter Label Runs

Among converters serving artisanal beverage brands, plate charges of USD 1,500 per color push owners toward digital alternatives once expected quantities slip below 10,000 impressions. Break-even moves even lower, to near 5,000 impressions, as rising labor costs and wasted substrates during registration push the analog tally higher. Seasonality compounds the math. A juice exporter in Europe used a newly installed digital press to release 22 flavor variants within one harvest year, parlaying time-to-shelf speed into a 6.2% price premium. Pharmaceutical trial batches see even leaner series, often just 200-2,000 units, making digital workflow a necessity as protocol text evolves with each investigator update.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Investment and Total Cost of Ownership Versus Conventional Flexo | -0.8% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Limited Printhead Durability at High Speeds | -0.6% | Global, high-volume food lines | Short to Medium term (≤ 3 years) |

| Supply Chain Vulnerability of Electronic Components for Digital Presses | -0.4% | Global, Asia-Pacific hubs most exposed | Short term (≤ 2 years) |

| Skill Gap in Digital Workflow Integration in Emerging Markets | -0.3% | Asia-Pacific, Africa, South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Investment and Total Cost of Ownership Versus Conventional Flexo

Entry-level digital presses start around USD 75,000, while a workhorse industrial configuration can exceed USD 450,000, outstripping comparable flexographic machines by a ratio of 2:1 for the same web width. Consumables cost more than water-based or UV-curable inkjet fluids, which are priced between USD 180 and USD 320 per liter, compared with USD 45-90 per kilogram for flexographic ink sets.[2]Siegwerk, “Sustainable Ink Technologies,” siegwerk.com Printhead replacement is the hidden bill, USD 8,000-15,000 every two years at continuous-shift operation, while anilox rolls in flexo lines last five or more years with periodic re-engraving. Converters, therefore, weigh multi-year paybacks heavily. Subscription models are emerging, such as HP’s pay-per-print bundle that folds service, heads, and ink into a monthly fee, but wide adoption is still preliminary.

Limited Printhead Durability at High Speeds

Piezoelectric heads operating above 100 m/min experience accelerated wear due to nozzle clogging and mechanical fatigue. Real-world audits show lifespans dropping to 18-30 months in three-shift beverage plants, well below the 5-year design spec. Thermal heads in desktop units experience similar erosion when printing high-coverage graphics on abrasive-textured paper. Manufacturers are countering with ceramic or silicon carbide nozzle plates that add hardness, yet each new metallurgical step nudges acquisition prices upward. Preventive protocols, including automated purging and humidity-controlled standby modes, mitigate failures but add USD 12,000-18,000 in extra hardware and new training hurdles for operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Inkjet Dominance Balanced by Hybrid Expansion

Inkjet captured the largest slice in 2025 at 46.27%, buoyed by water-based chemistry that meets European volatile organic compound limits without exhaust-air treatment. Hybrid lines that graft an inkjet bridge onto a flexographic base are forecast to grow 8.91% per year through 2031, enabling converters to overlay serialized or promotional data while still deploying opaque whites and metallics from analog decks.[3]Siegwerk, “Sustainable Ink Technologies,” siegwerk.com Electrophotography maintains a foothold in premium wine and cosmetics labels, valued for finely screened halftones, yet its reliance on specially coated films constrains its spread. Thermal transfer remains favored in pharma and logistics, where monochrome barcodes suffice.

Inkjet’s runway also owes to chemistry gains such as AQUAFUZE, which eliminates corona treating on polyethylene films, extending applicability to snack pouches and stand-up bags without extra surface prep. Conversely, electrophotographic units like HP Indigo presses require a primer-coated substrate, which adds USD 0.08-0.14 per square meter, lifting the cost per thousand impressions. Hybrid suppliers exploit this delta, selling retrofit kits at 40% of a stand-alone press’s ticket, thus easing converters’ capital anxiety. As a result, the digital labeling machines market size for hybrid solutions is projected to outpace single-technology lines in the back half of the decade, even though the installed base today tilts heavily toward pure inkjet.

By Machine Type: Print-And-Apply Leadership, Desktop Units Surge

Print-and-apply systems led with 40.85% of revenue in 2025, as beverage and dairy plants embed applicators into high-speed packaging loops where ±1 mm accuracy keeps downstream robotics synchronized. Uptime matters more than color nuance in these zones, prompting vendors to add predictive algorithms that forecast ribbon-out events and printhead drift. Desktop and benchtop units, however, are racing ahead at an 8.82% CAGR, fueled by craft breweries, direct-to-consumer cosmetics, and Amazon Marketplace sellers who bring labeling in-house to escape long converter lead times.

Stand-alone digital presses, roughly 28% of 2025 turnover, still dominate mid-volume trade shops that process dozens of small jobs daily, yet they face competition from in-line modules such as Domino’s N610i bridge. These bolt-on kits deliver serialization without retiring legacy flexo towers, preserving sunk capital. Price pressure is intense at the low end, where Afinia and Colordyne drive sub-USD 5,000 price points that compress payback periods to under a year when printed volumes reach just a few thousand labels per week.

By End-User Industry: Food and Beverage as Anchor, E-Commerce the Rocket

Food and beverage brands accounted for 32.13% of 2025 sales and remain the throughput backbone for many service bureaus, as regulatory dates, batch codes, and regional artwork revisions keep volumes predictable. Even so, e-commerce and logistics display the steepest runway, rising 8.77% annually on the back of parcel growth and retailer push toward omnichannel agility. Healthcare and pharmaceuticals leverage digital heads for DSCSA compliance and for patient-friendly labels that scale font size dynamically without preserving multiple SKUs. Personal care capitalizes on the same flexibility for influencer tie-ins, while industrial chemical suppliers avoid inventory scrap each time GHS pictogram rules refresh.

Fulfillment nodes processing 50,000 parcels per day are standardizing on thermal-transfer architectures that swap ribbons mid-shift without stopping conveyors, a feature critical to maintaining sortation cadence. On the opposite extreme, boutique cosmetics houses in Japan upgrade to 1200-dpi inkjet to recreate photographic skin tones and metallic embellishments once monopolized by offset presses. Such dispersion of needs underlines why the digital labeling machines market continues to bifurcate between rugged monochrome workhorses and boutique full-color units.

Geography Analysis

Asia-Pacific accounted for 38.44% of global revenue in 2025, with China’s National Medical Products Administration driving compulsory serialization and India’s food export rules requiring lot-level visibility. Japan extends the case through NFC-enabled cosmetic labels that combine consumer engagement with anti-counterfeiting features. Local integrators report that more than 1,000 AccurioLabel systems have already been installed regionally, suggesting deeper adoption. North America accounted for 26% of turnover, underpinned by high e-commerce activity and DSCSA deadlines requiring pharmaceutical packagers to deploy variable-data engines at bottle-filling speed. Craft brewing culture compounds demand by pumping out seasonal label cycles monthly.

Europe accounted for a notable share in 2025, restrained by saturated converter density yet boosted by volatile-organic-compound rules that penalize solvent stacks, hence tilting orders toward water-based inkjet. African demand is smaller in absolute value yet outpaces all regions at a 9.13% CAGR. Multinational beverage, detergent, and personal-care brands now prefer to print labels close to the point of sale to avoid currency swings and import duties, driving fresh installations from Kenya to Côte d’Ivoire.[4]Star Labels Africa, “Digital Label Printing in Africa,” starlabelsafrica.com South America and the Middle East round out the map at 14%, with Brazil’s pharmaceutical exporters and the United Arab Emirates’ logistics hubs anchoring spend amid macro volatility.

Europe, catalyzed by the 2025 Packaging and Packaging Waste Regulation, invests in presses capable of updating recyclability logos by product line and batch. Luxury wine, spirits, and cosmetics brands in France and Italy deploy hybrid presses to marry digital personalization with tactile foils, elevating consumer engagement while staying compliant with circular-economy mandates. The digital labeling machines market benefits from EU grants for eco-design projects, further underwriting hardware upgrades.

Competitive Landscape

The digital labeling machines market demonstrates moderate concentration, with the top five vendors, HP, Epson, Domino, Avery Dennison, and CCL Industries, collectively capturing a significant share of revenue in 2025. These leading players are focusing on vertical integration to strengthen their market positions. For instance, HP is enhancing its offerings by incorporating workflow software, Domino is leveraging Brother’s expertise in head technology, and Avery Dennison is investing in smart-label silicon to gain greater control over the bill of materials, thereby improving operational efficiency and cost management.

Hybrid-press innovators such as Gallus and Mark Andy are targeting converters hesitant to fully transition away from analog decks. These companies offer retrofit kits that are approximately 60% less expensive than investing in a brand-new full-digital production line, making them an attractive option for cost-conscious buyers. On the other hand, desktop disruptors like Afinia, Colordyne, and AstroNova are focusing on the lower-tier market by introducing machines priced under USD 5,000. These affordable solutions are equipped with app-driven color calibration features, which simplify the operation process and make them particularly appealing to first-time buyers who are new to digital labeling technology.

Differentiation is narrowing around ink chemistry and head longevity. Ricoh’s Gen6 ceramic nozzles earn notoriety for extending duty cycles by roughly one-third, while Fujifilm’s AQUAFUZE line widens the media window by sidestepping corona treatment. Smart labels are emerging as the next battleground; for instance, Avery Dennison’s USD 75 million stake in Wiliot points to ecosystem plays that wrap sensing, cloud, and analytics around a modestly priced label. Software-only entrants such as ZPL.ai further unsettle hardware incumbents by decoupling job preparation from a single OEM, fostering hardware agnosticism.[5]ZPL.ai, “Cloud-Based Label Design and Fulfillment Platform,” zpl.ai Regional players still flourish because service responsiveness and spare-part proximity trump a global brand when presses run around the clock.

Digital Labeling Machines Industry Leaders

Avery Dennison Corp.

Videojet Technologies (Danaher)

CCL Industries Inc.

Markem-Imaje (Dover)

Domino Printing Sciences (Brother)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Flint Group Digital Xeikon has globally launched its Ecolyne digital label press model, now available on a subscription basis. This strategic move aims to provide converters and commercial printers a lower-risk gateway into digital label production, eliminating the burden of a significant upfront investment.

- April 2026: Avery Dennison completed the phase-one pilot of Wiliot Bluetooth tags embedded in temperature-sensitive vaccine cartons, proving real-time cold-chain visibility across three continents.

- April 2026: HP and ePac Flexible Packaging began commissioning the first batch of HP Indigo 25K presses under their USD 50 million partnership launched in 2025, with commercial production slated for Jul 2026.

- September 2025: Domino shipped the initial ten units of its N730i press to European pharmaceutical packagers seeking 1200-dpi serialization at 75 m-per-minute throughput.

Global Digital Labeling Machines Market Report Scope

The Digital Labeling Machines Market is the global industry focused on the development, manufacturing, and commercialization of digitally controlled equipment used to print, encode, and apply labels to products, packaging, and shipping materials across various industries. These machines utilize advanced digital printing technologies, such as inkjet, electrophotography, thermal transfer, direct thermal, and hybrid systems, to deliver high-quality, variable-data, on-demand labeling solutions with improved efficiency, greater customization, and reduced setup time compared to conventional labeling methods.

The Digital Labeling Machines Market Report is Segmented by Technology (Inkjet, Electrophotography, Thermal Transfer and Direct Thermal, and Hybrid), Machine Type (Print-and-Apply Systems, Stand-alone Digital Label Presses, In-line Labeling Modules, and Desktop/Benchtop Units), End-user Industry (Food and Beverage, Healthcare and Pharmaceuticals, Personal Care and Cosmetics, Industrial and Chemicals, and E-commerce and Logistics), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). Market Forecasts are Provided in Terms of Value (USD).

| Inkjet |

| Electrophotography |

| Thermal Transfer and Direct Thermal |

| Hybrid |

| Print-and-Apply Systems |

| Stand-alone Digital Label Presses |

| In-line Labeling Modules |

| Desktop/Benchtop Units |

| Food and Beverage |

| Healthcare and Pharmaceuticals |

| Personal Care and Cosmetics |

| Industrial and Chemicals |

| E-commerce and Logistics |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Technology | Inkjet | |

| Electrophotography | ||

| Thermal Transfer and Direct Thermal | ||

| Hybrid | ||

| By Machine Type | Print-and-Apply Systems | |

| Stand-alone Digital Label Presses | ||

| In-line Labeling Modules | ||

| Desktop/Benchtop Units | ||

| By End-user Industry | Food and Beverage | |

| Healthcare and Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Industrial and Chemicals | ||

| E-commerce and Logistics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the digital labeling machines market and how fast is it growing?

The digital labeling machines market size stands at USD 12.17 billion for 2025 and is projected to reach USD 20.02 billion by 2031 with an 8.65% CAGR, according to Mordor Intelligence.

Which technology leads global installations of digital labeling equipment?

Inkjet leads with 46.27% share in 2025 because its water-based and UV-ink chemistries meet volatile organic compound limits without exhaust treatment.

Which end-user vertical is expanding fastest?

E-commerce and logistics is the fastest-growing vertical, expected to advance at an 8.77% CAGR through 2031 as fulfillment nodes shift to real-time parcel labeling.

Why are hybrid digital-flexographic presses gaining popularity?

Hybrid setups allow converters to print opaque whites and metallics flexographically while adding variable data digitally, reducing changeovers and capital risk.

What limits broader adoption of digital labeling in emerging markets?

High upfront capex, ongoing printhead replacement costs, and limited operator skills in digital workflow integration slow roll-outs among small converters.

How concentrated is vendor competition?

The top five manufacturers hold 42% of revenue, indicating moderate concentration where regional specialists still compete effectively alongside global leaders.

Page last updated on: