Wet Glue Labels Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

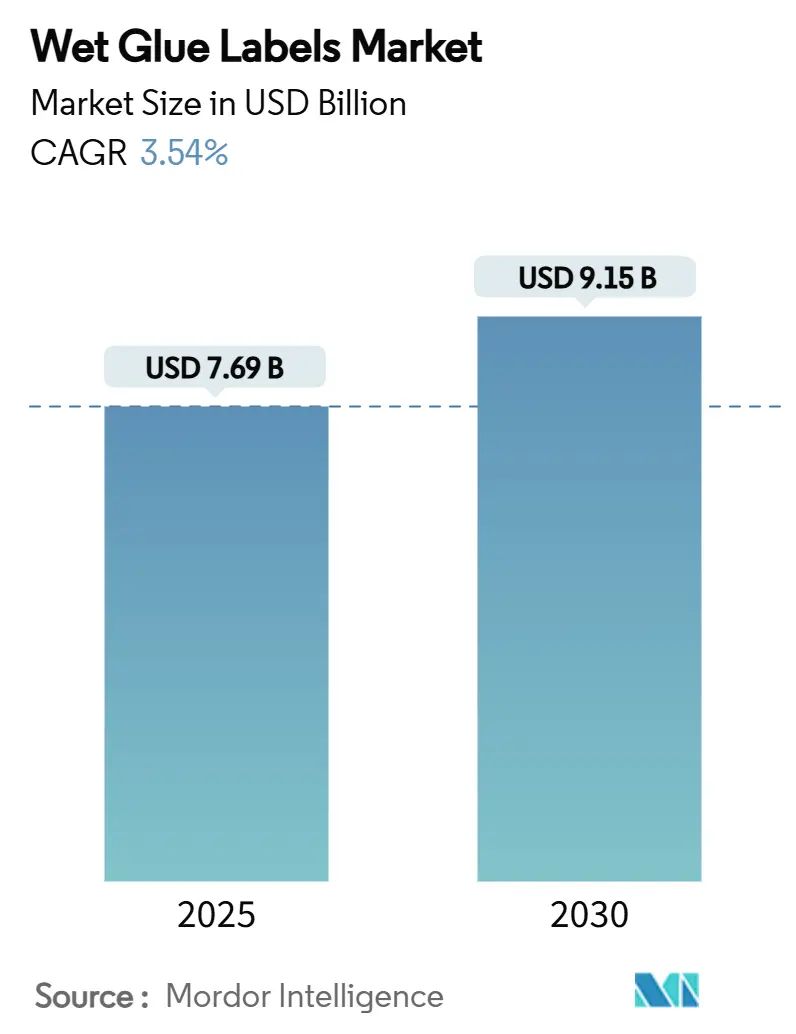

| Market Size (2025) | USD 7.69 Billion |

| Market Size (2030) | USD 9.15 Billion |

| Growth Rate (2025 - 2030) | 3.54% CAGR |

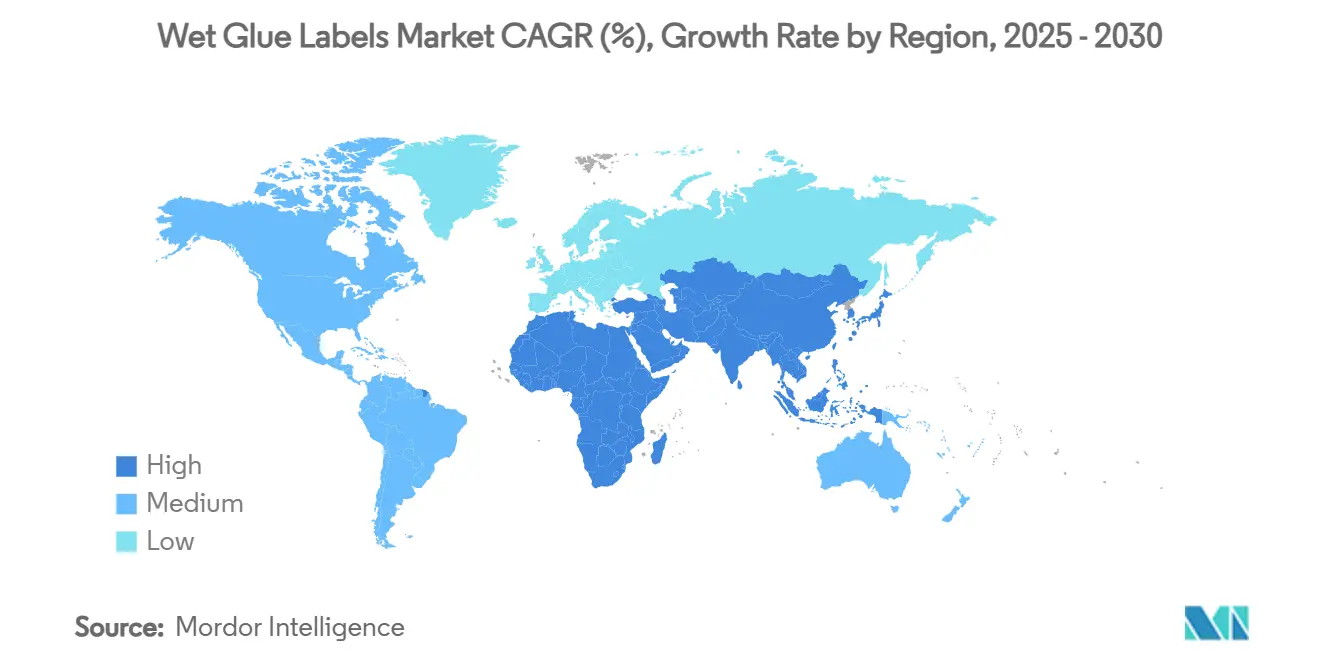

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wet Glue Labels Market Analysis by Mordor Intelligence

The wet glue labels market size stands at USD 7.69 billion in 2025 and is projected to reach USD 9.15 billion by 2030, expanding at a CAGR of 3.54%. This outlook underscores a maturing landscape in which traditional cut-stack technology holds ground through low unit costs in large-volume runs, even as pressure-sensitive and sleeve alternatives gain traction. Solid demand from beverage fillers that operate returnable-glass lines, brand owners’ rising interest in hybrid print workflows, and the push for casein-free adhesive chemistry collectively anchor the wet glue labels market amid shifting substrate and regulatory dynamics. Convergence between offset, gravure, and downstream digital over-print modules is boosting customization capability for promotional SKUs without eroding the cost advantage that defines the wet glue labels market. Meanwhile, tightening wastewater and formaldehyde rules in the United States and the European Union are elevating compliance costs, nudging smaller converters toward consolidation with larger peers that already run advanced treatment and emission-reduction systems.

Key Report Takeaways

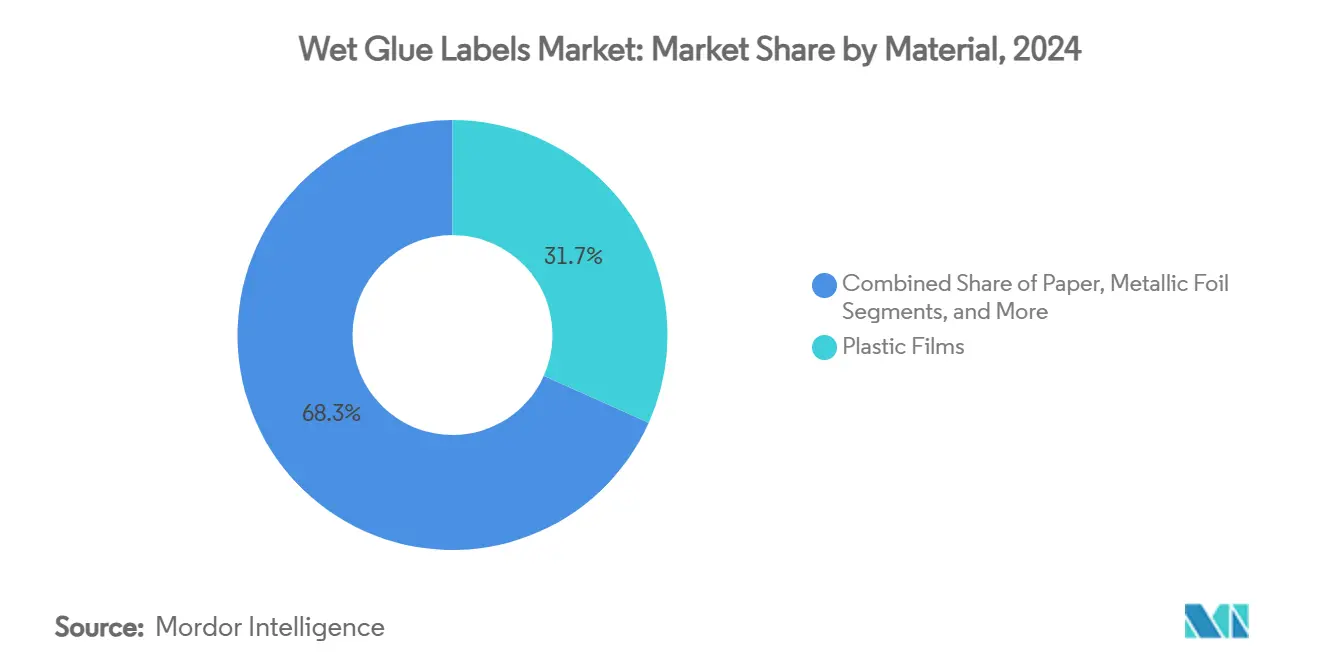

- By material, plastic films captured 31.69% share of the wet glue labels market in 2024.

- By adhesive type, water-based products captured 53.48% share of the wet glue labels market in 2024.

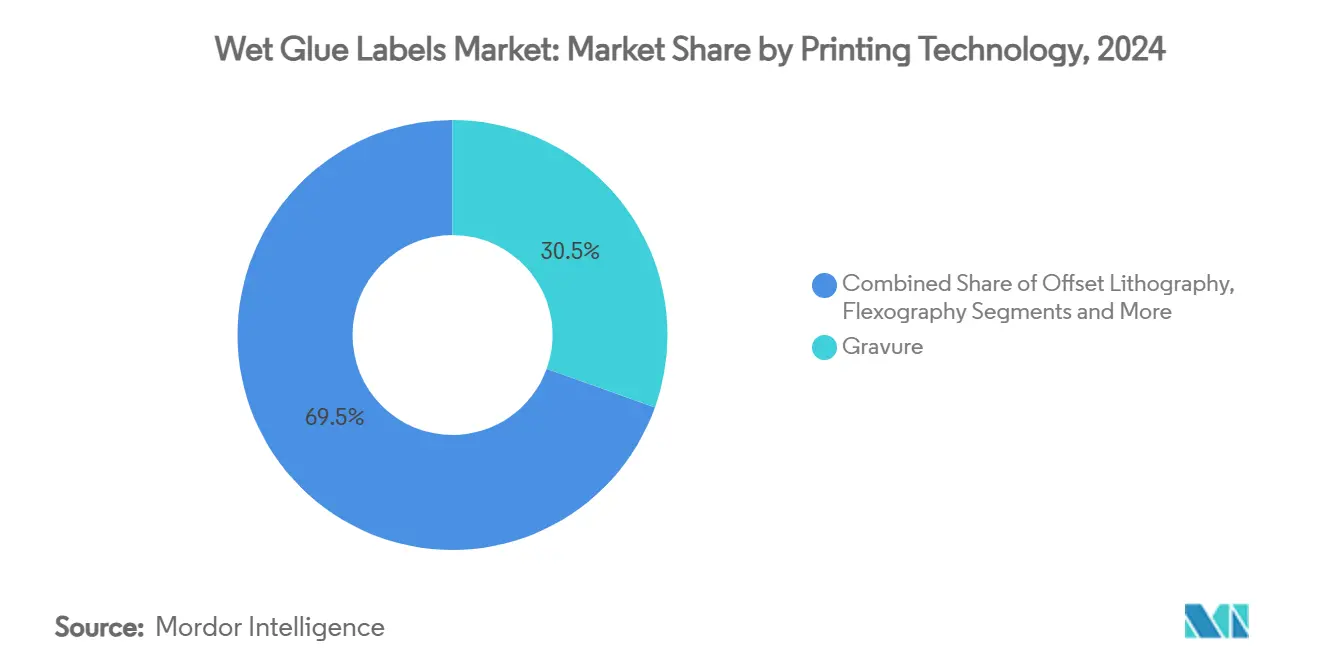

- By printing technology, the wet glue labels market for digital printing is projected to grow at 5.16% CAGR between 2025 to 2030.

- By end-use, beverages captured 39.83% share of the wet glue labels market in 2024.

- By geography, the wet glue labels market for the Middle East and Africa region is projected to grow at 5.35% CAGR between 2025 to 2030.

Global Wet Glue Labels Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging beer and CSD production drives high-speed wet-glue lines | +0.8% | Asia-Pacific core, spill-over to Latin America | Medium term (2–4 years) |

| Cost advantage over PSL and sleeve labels in emerging markets | +0.6% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Offset and gravure upgrades enable mass customization | +0.4% | Global, early gains in Europe and North America | Short term (≤ 2 years) |

| Returnable-glass reuse needs easy wash-off labels | +0.3% | Europe and North America core, expanding to APAC | Medium term (2–4 years) |

| Bio-based, casein-free adhesives meet recycling mandates | +0.5% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Hybrid cut-stack + digital over-print for short-run promos | +0.2% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Beer and CSD Production Drives High-Speed Wet-Glue Lines

Constellation Brands recorded 9% growth in its beer division during fiscal 2024, with flagship Modelo posting high single-digit depletion gains.[1]Constellation Brands, “Fiscal 2024 Fourth-Quarter Results,” cbrands.com Brewers continue to favor high-speed wet-glue machinery that exceeds 1,000 bottles/minute on glass, securing steady demand for base labels that withstand pasteurization. Molson Coors’ operations across North America and Europe highlight how legacy brewers retain cut-stack capacity to balance output surges without adding more expensive pressure-sensitive lines. As emerging breweries in Southeast Asia scale, they replicate this capital-efficient template, reinforcing the wet glue labels market’s relevance in high-throughput beverage corridors. Integration of inline vision systems is improving registration accuracy, keeping waste below 2% of web length and therefore protecting gross margins.

Cost Advantage Over PSL and Sleeve Labels in Emerging Markets

In cost-sensitive consumer sectors across Indonesia, Nigeria, and Brazil, wet-glue production still delivers 15–25% lower applied-label cost than pressure-sensitive alternatives thanks to cheaper cut-stack paper and centralized adhesive preparation. Local line operators’ familiarity with glue pot calibration offsets higher labor content, while regionally sourced starch and dextrin adhesives reduce foreign-exchange exposure. During commodity up-cycles, processors can throttle adhesive solids by 2–3 percentage points without jeopardizing tack, a flexibility unattainable with pre-coated liners. Consequently, converters positioned in Tier-2 cities continue reinvesting in wet-glue capacity, extending the wet-glue labels market footprint across fast-moving goods such as carbonated soft drinks, affordable spirits, and basic condiments.

Offset and Gravure Upgrades Enable Mass Customization

Bobst Group’s Printing and Converting division tallied CHF 497.2 million in H1 2024 sales, buoyed by new offset modules showcased at drupa that enable variable imaging directly on cut-stack labels. Line-level retrofits now allow plate changes in under four minutes, unlocking SKU proliferation without sacrificing throughput. Gravure cylinders with electro-mechanical engraving deliver 12-micron highlight control, broadening color gamut for craft brewers and premium water brands seeking differentiated shelf presence. As brand teams push for seasonal designs, hybrid workflows route base litho sheets through digital over-print units, trimming minimum order quantities to 5,000 sheets. This evolution keeps the wet glue labels market closely aligned with on-shelf marketing tactics previously dominated by PSL graphics.

Returnable-Glass Reuse Needs Easy Wash-Off Labels

European draft beer networks rely on returnable bottles completing 30–40 trip cycles, demanding labels that release fully during an 80 °C caustic wash. Water-based adhesive systems exhibit complete fiber release within four minutes, beating many no-label-look films that leave residue. Legislators under the EU Circular Economy Action Plan are widening deposit-return schemes, a shift that multiplies the glass pool requiring wash-off label performance. North American dairies experimenting with refillable quart bottles mirror this trajectory, adopting casein-reduced glues that balance wet-tack with alkaline solubility. These specifications reinforce the wet glue labels market as the de facto choice where reuse economics align with sustainability mandates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift to pressure-sensitive and sleeves | -1.2% | Global, accelerated in developed markets | Medium term (2–4 years) |

| Skilled-operator and waste issues on glue lines | -0.4% | Global, particularly acute in developed markets | Short term (≤ 2 years) |

| Stricter wastewater limits on casein/formaldehyde | -0.6% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Wet-strength pulp supply volatility | -0.3% | Global, concentrated in paper-dependent segments | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift to Pressure-Sensitive and Sleeves

Avery Dennison’s Materials Group continues to scale intelligent linerless films that carry NFC chips, creating experience-rich packaging that wet-glue cannot replicate. Shelf marketers praise 360-degree sleeve graphics for delivering billboard-like shelf impact, particularly in ready-to-drink cocktails where flavor differentiation hinges on visual pop. Unit costs for thin PET liners have fallen 8% since 2023, narrowing the historical price gap with cut-stack worksheets. Luxury spirits in Western Europe are transitioning en masse, siphoning volume away from the wet glue labels market in discretionary categories. Although lower-cost tiers still prize cut-stack economics, the aspirational drift in consumer packaging is a medium-term drag on market growth.

Skilled-Operator and Waste Issues on Glue Lines

Wet-glue application demands precise viscosity control (2,600–3,200 cP), and mis-tuning can push scrap rates above 4%. H.B. Fuller’s 2024 report cited raw-material inflation and operational inefficiency as hurdles for converters maintaining manual glue mixing stations.[2]H.B. Fuller Company, “Form 10-K 2024,” hbfuller.comDeveloped markets battling labor shortages see churn among skilled line mechanics, inflating overtime costs, and eroding competitiveness against automated PSL applicators. Start-up and shut-down cycles also generate adhesive sludge requiring disposal under hazardous-waste codes, adding compliance overhead. These pain points cumulate to a 40 basis-point margin penalty for small-scale converters relying on legacy gear.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Performance Films Dominate Even as Paper Gains Momentum

Plastic films represented 31.69% of the wet glue labels market share in 2024, supported by superior moisture resistance demanded by beer, soft drink, and condiment processors. Polypropylene and polyethylene films maintain tensile strength above 150 MPa, ensuring label integrity in cold-chain logistics spanning Southeast Asia. Durability metrics anchor films in mid-tier beverage packages that weather condensation during distribution. In parallel, paper substrates are advancing at a 5.21% CAGR because brand owners are recalibrating toward recyclable fiber content to meet retailer scorecard goals. Mills supplying one-sided-coated kraft paper are expanding calendar rolls to augment brightness to 90 ISO, narrowing aesthetic gaps with films. Graphic Packaging’s USD 9.428 billion 2023 sales underscore corporate resources marshaled to create barrier-coated papers that withstand pasteurization without detaching.

Momentum behind sustainability is also driving trials of sugarcane-fiber labels that improve life-cycle analysis scores by cutting greenhouse gas intensity by 12 % versus virgin pulp. Mondi has redirected EUR 1.2 billion toward machinery that laminates aqueous dispersion barriers onto paper, positioning its Advantage product line to capture incremental share in European returnable-glass circuits.[3]Mondi Group, “2024 Investor Day Presentation,” mondigroup.comSecond-generation mechanical pulps integrating lignin stabilization impart wet tensile retention beyond 25 minutes in a 65 °C soak, a property vital for multi-trip bottles. As recycling mandates strengthen, converters forecast that paper could exceed 35 % share by 2030, signaling a decisive, though gradual, material rebalancing within the wet glue labels market.

By Adhesive Type: Water-Based Formulas Retain Scale Leadership

Water-based systems held 53.48% share of the wet glue labels market size in 2024 on the back of universal availability, favorable price-to-performance ratios, and established wash-off behavior in alkaline baths. Standard dextrin-casein blends cost under USD 1.30/kg and cure at ambient conditions, enabling simple pot-life management on legacy labelers across Latin America. Regulatory headwinds against formaldehyde, however, are steering R&D pipelines toward soy albumin and corn starch hydrolysate solutions. Bio-based adhesives, growing at 5.04% CAGR, now achieve 16 N/25 mm bond strength, closing historic performance gaps. FEICA’s technical note, released in August 2024, provides a blueprint for ensuring re-pulpability thresholds below 150 µm macro-stickies, accelerating uptake among European converters.

Hot-melt formulations, albeit niche, preserve relevance in spirits bottling lines requiring instant tack on high-recycled-content glass. They run at wheel temperatures above 140 °C and reduce set-time to under one second, a necessity on 72,000 bph monoblocs. Solvent-based variants continue their retreat amid VOC caps under California’s Rule 1168. Looking ahead, hybrid water-dispersed systems fortified with 4 % natural latex are in pilot at multinational soft-drink plants, offering a middle ground on cost and green-label compliance. These trends together illustrate the adaptive chemistry landscape safeguarding the competitive posture of the wet glue labels market.

By Printing Technology: Gravure Anchors Volume, Digital Captures Agility

Gravure processes secured 30.47% revenue within the wet glue labels market in 2024, powered by unmatched ink-transfer uniformity at micron-level cell depths ideal for vibrant beer labels. Cylinder replacement cost amortizes effectively when runs exceed 2 million impressions, a scale common to multinational CSD brands. However, plate-fee economics are less attractive for boutique beverage arrays with 15,000-case rotations, opening room for digital heads that avoid tooling altogether. HP’s Indigo 6K platform now prints 97 % of Pantone colors on wet-strength paper with a 1,600 dpi native resolution, and the 5.16% CAGR forecast for digital reflects widening penetration into localized marketing pushes.

Offset lithography remains the workhorse for mid-runs between 150,000 and 800,000 sheets, with quick-change sleeves slashing make-ready by 35 %. Flexography retains a foothold in commodity rice wine and soy sauce labels in China thanks to its forgiving ink viscosity and straightforward clean-down. Converters dispatch core runs through gravure or offset, then top-coat special editions digitally, thereby maximizing asset utilization while delivering SKU differentiation. Such hybridization cements the wet glue labels market as a flexible ecosystem rather than a monolithic legacy process.

By End-Use Industry: Beverages Reign, Pharmaceuticals Accelerate

The beverages category controlled 39.83% share of the wet glue labels market size in 2024, underpinned by large global brewers and soda bottlers whose glass lines have already absorbed capital for cut-stack machinery. Constellation Brands’ ongoing volume gains in the high-end US beer segment reiterate that high-throughput glass bottling remains a prime application. Labeling speed tolerance, which can exceed 1,100 bpm, and caustic-wash recyclability keep wet-glue ahead of PSL in this arena. Parallel momentum in craft sodas and flavored waters is renewing engineering spend on labelers that perform quick-hitch changeovers for 12-oz to 16-oz formats.

Pharmaceuticals, advancing at 4.92% CAGR, leverage wet-glue labels for tamper-evident sealing on vials and ampoules that undergo terminal sterilization. Enhanced wet-strength papers withstand autoclave conditions of 121 °C for 15 minutes without edge lift, fulfilling EU GMP Annex 1. Serialisation coding modules integrated onto offset presses are fortifying supply-chain traceability against counterfeit risks, an area where cut-stack still provides a controlled, secure print environment. Food, personal care, and household chemical segments maintain steady demand, each valuing the cost-per-impression benefit that helps brands keep unit economics competitive in price-elastic categories.

Geography Analysis

Asia-Pacific dominated the wet glue labels market with a 36.74% revenue share in 2024, propelled by entrenched beer and CSD filling lines operating across China, Vietnam, and India. China’s megabreweries regularly execute 50,000 bph runs, locking in large demand for cut-stack sheets sourced from domestic mills clustered in Jiangsu and Zhejiang. Huhtamaki India posted INR 24,813,200,000 (USD 298 million) turnover in FY 2023, highlighting the packaging supply chain scale underpinning Indian wet-glue demand. Meanwhile, Japan’s sophisticated food processors, though facing a 4.1% decline in 2023 output, continue specifying high-opacity labels for premium soy sauce and sake, ensuring niche value capture.

The Middle East and Africa region is projected to log the fastest 5.35% CAGR through 2030. Saudi and UAE beverage joint ventures are outfitting new bottling halls with European-sourced Krones Solomatic labelers because the technology’s capex is one-third lower than equivalent PSL lines at identical speeds. Nigeria’s soft-drink plants in Agbara and Aba are following suit to balance currency volatility with proven wet-glue economics. Government-led diversification drives, notably Egypt’s SCZone reforms, include packaging clusters that extend regional substrate supply, further raising the wet glue labels market’s footprint.

North America maintains steady cut-stack consumption in beer, malt beverages, and private-label food jars despite the broader shift to sleeves in ready-to-drink cocktails. Canadian canola-based casein alternatives are being trialed at US Midwest converters, a move sparked by EPA formaldehyde scrutiny. Europe’s share stabilizes through regulatory-compliant wash-off labels compatible with deposit-return infrastructure, especially in Germany and the Nordics. South America leverages cost advantages as Argentine paper mills ramp bleached eucalyptus pulp capacity, improving label stock availability for local wine and condiment sectors. Collectively, these regional patterns demonstrate how the wet glue labels market derives resilience from diverse macro-economic and regulatory conditions even as alternate technologies mount pressure.

Competitive Landscape

Competitive intensity in the wet glue labels market remains moderate, with no single company commanding more than 10% global revenue. Multi-Color Corporation operates 108 plants worldwide, using its gravure hubs in Kuala Lumpur and Bangkok to bundle region-specific print services for global drinks giants. CCL Industries’ acquisition of Polish converter Kryolan in 2024 enhanced its European cold-glue portfolio and added 450 million m² of annual paper-label capacity, signaling renewed interest from tier-one players in reinforcing cut-stack coverage. Regional specialists such as Egypt-based Al-Ezz Packaging differentiate on turnaround speed and language-specific artwork services that multinationals occasionally struggle to localize.

Technology investments form a central axis of competition. Mondi’s EUR 1.2 billion organic growth pledge includes a new extrusion-coating line in Czechia set to produce repulpable barrier papers suited for wet-glue beer labels, extending first-mover advantage in sustainable substrates. Bobst’s drupa-launched G440 gravure press integrates inline inkjet modules, empowering converters to emboss variable data at 11,000 sph. Partnerships between adhesive suppliers and equipment OEMs are catalyzing pre-validated glue formulations that slash customer qualification lead times from six weeks to ten days.

Environmental compliance is a differentiator. Converters that invested early in regenerative thermal oxidizers and membrane bioreactors are winning procurement bids tied to Scope 3 reduction targets released by beverage conglomerates. Smaller shops encountering capex hurdles often pivot into niche specialties such as gold-foil wet-glue capsules for fortified wines, effectively carving defensible micro-segments. Collectively, the field continues to favor actors that integrate regulatory foresight, hybrid print technology, and supply-chain reliability into their service proposition.

Wet Glue Labels Industry Leaders

Multi-Color Corporation

CCL Industries Inc.

Fort Dearborn Company

Huhtamaki Oyj

Skanem AS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Stora Enso reported 9% sales increase to EUR 2,362 million in Q1 2025, with its new consumer packaging board line in Oulu, Finland, ramping toward full capacity by 2027.

- January 2025: EPA published a comprehensive occupational exposure assessment for formaldehyde, detailing inhalation ranges from 9.34×10-6 to 14 ppm across adhesive manufacturing.

- August 2024: Bobst Group disclosed CHF 828.2 million H1 2024 sales and premiered gravure-digital hybrid solutions at drupa aimed at short-run mass customization.

- July 2024: Mondi Group announced a EUR 1.2 billion organic growth program targeting flexible and corrugated packaging, including wet-glue compatible barrier substrates.

- June 2024: FEICA 2024 Conference agenda released with focus on CLP regulation changes and sustainable adhesive solutions.

Global Wet Glue Labels Market Report Scope

| Paper |

| Plastic Films |

| Metallic Foil |

| Others |

| Water-based |

| Hot-Melt |

| Solvent-based |

| Bio-based Adhesives |

| Offset Lithography |

| Gravure |

| Flexography |

| Digital |

| Food |

| Beverages |

| Personal Care and Cosmetics |

| Pharmaceuticals |

| Industrial and Chemicals |

| Logistics and Retail |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Thailand | ||

| Indonesia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Material | Paper | ||

| Plastic Films | |||

| Metallic Foil | |||

| Others | |||

| By Adhesive Type | Water-based | ||

| Hot-Melt | |||

| Solvent-based | |||

| Bio-based Adhesives | |||

| By Printing Technology | Offset Lithography | ||

| Gravure | |||

| Flexography | |||

| Digital | |||

| By End-use Industry | Food | ||

| Beverages | |||

| Personal Care and Cosmetics | |||

| Pharmaceuticals | |||

| Industrial and Chemicals | |||

| Logistics and Retail | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Thailand | |||

| Indonesia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current market size of wet-glue labels?

The wet glue labels market size is USD 7.69 billion in 2025.

How fast is the wet-glue labels market expected to grow?

The market is forecast to expand at a 3.54% CAGR, reaching USD 9.15 billion by 2030.

Which region leads the wet-glue labels market?

Asia-Pacific holds the largest share at 36.74% thanks to dense beverage production capacity.

Which end-use industry dominates demand for wet-glue labels?

Beverages account for 39.83% of market demand due to high-speed glass bottling lines.

Why are bio-based adhesives gaining traction in wet-glue labels?

Regulatory pressure on formaldehyde emissions and the need for recycling-friendly chemistries is driving adoption of bio-based, casein-free formulations.

What technological trend is shaping wet-glue label production?

Hybrid workflows that combine traditional cut-stack printing with digital over-print modules are enabling mass customization for short-run promotions without sacrificing cost efficiency.

Page last updated on: