Label And Packaging Printers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 10.24 Billion |

| Market Size (2030) | USD 13.90 Billion |

| Growth Rate (2025 - 2030) | 6.30% CAGR |

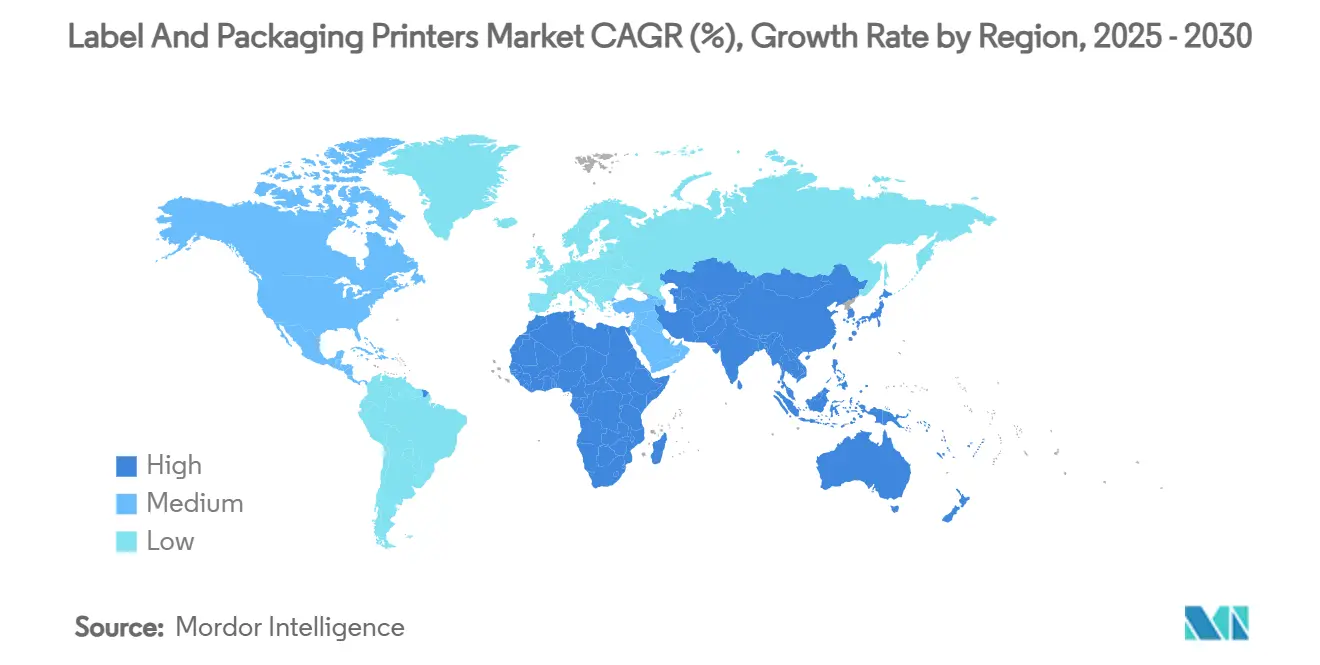

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

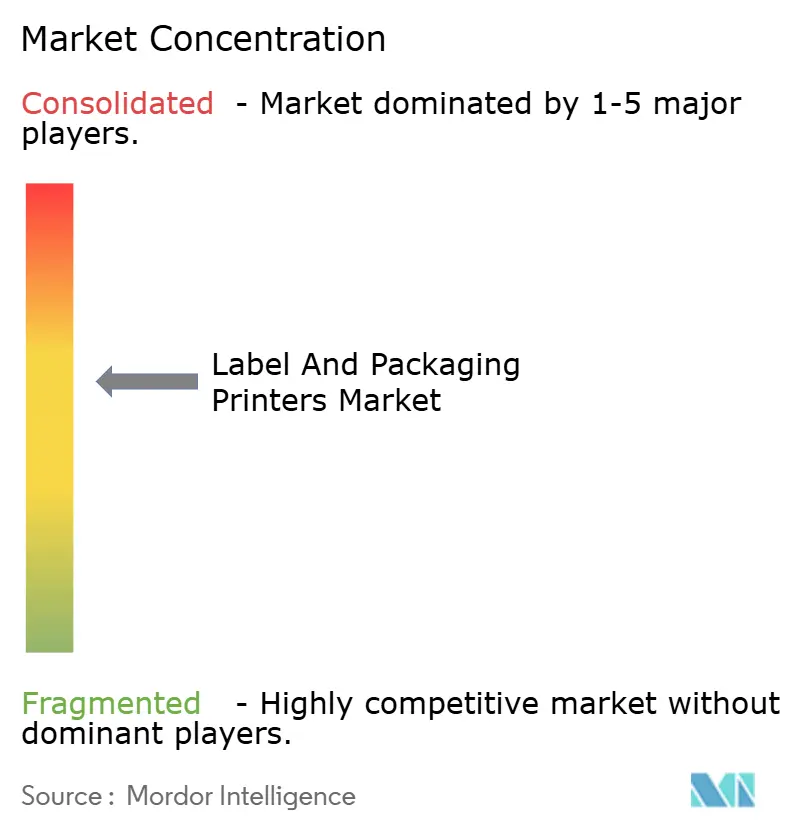

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Label And Packaging Printers Market Analysis by Mordor Intelligence

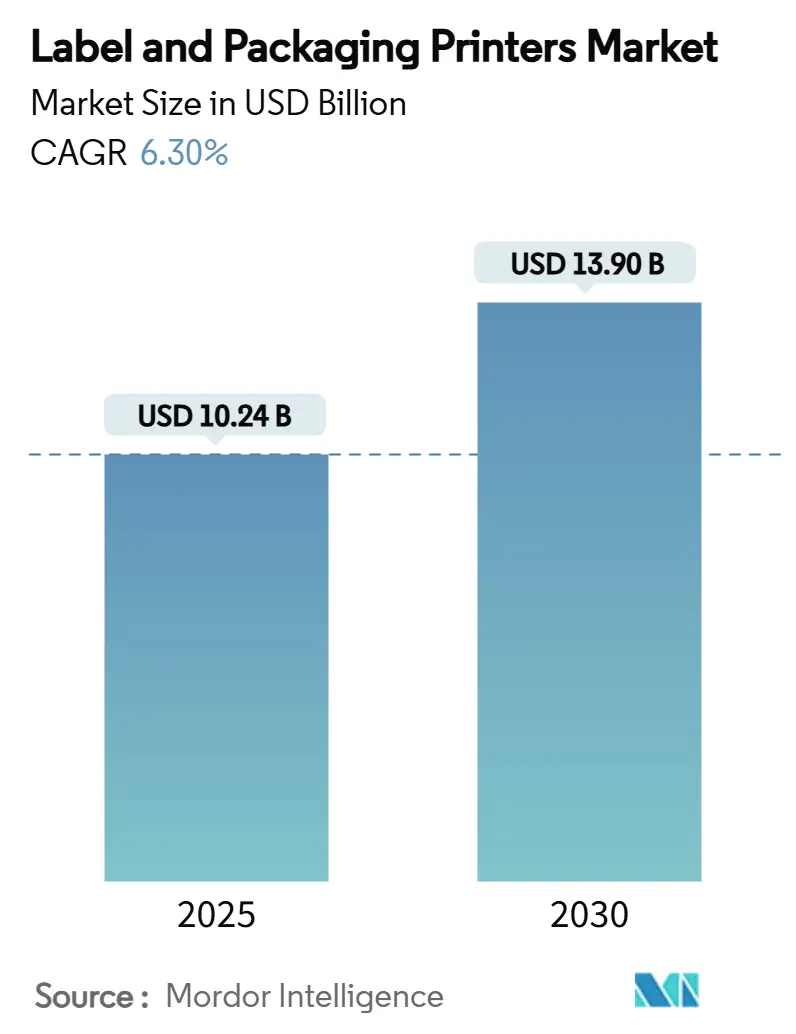

The label and packaging printers market is valued at USD 10.24 billion in 2025 and is forecast to reach USD 13.90 billion by 2030, registering a 6.30% CAGR over the period. Consistent demand for accurate product identification, the shift toward smart, connected labels, and tightening regulations on food-safe inks underpin this growth trajectory. Rapid e-commerce expansion is pulling investment toward digital, on-demand printing fleets that shorten fulfillment lead times. At the same time, corporate sustainability targets and government mandates are accelerating the transition to water-based, low-migration ink systems, prompting capital upgrades across print shops. Competitive intensity remains moderate; global incumbents continue to widen their technology portfolios, while smaller firms are consolidating to absorb rising compliance costs.

Key Report Takeaways

- By printer type, high-end digital presses are projected to expand at a 7.47% CAGR through 2030.

- By printing technology, flexographic printing led with 35.81% revenue share in 2024.

- By end-user industry, e-commerce is forecast to grow at 7.58% CAGR through 2030.

- By geography, Asia-Pacific commanded 40.67% share in 2024 and is set to record a 7.74% CAGR to 2030.

Global Label And Packaging Printers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global shift to digital printing for cost-effective short runs and product personalization | +1.8% | North America and Europe, building in Asia-Pacific | Medium term (2-4 years) |

| Global e-commerce growth driving demand for on-demand shipping and barcode labeling | +1.5% | Asia-Pacific and North America | Short term (≤ 2 years) |

| Adoption of RFID/NFC-ready smart label printers across logistics and retail | +1.2% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Craft beverage and small food brands insourcing label production to cut lead times | +0.9% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Global adoption of food-safe, water-based inkjet systems for flexible packaging | +0.7% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global shift to digital printing for cost-effective short runs and product personalization

Digital presses eliminate plates and lengthy change-overs, making small batches economically viable and enabling SKU proliferation. Canon reports steady gains in commercial printing thanks to twin electrophotographic and inkjet platforms that flex across run-lengths and substrates [1]Canon Inc., “Annual Report 2024,” canon.com. Faster artwork change cycles let brands localize promotions without carrying excess inventory. A peer-reviewed study found digitized ink-metering systems cut ink usage 52% and power consumption 37%, lowering costs while shrinking the carbon footprint. The performance gains resonate with mid-sized converters that previously relied on trade shops. Widespread roll-out is most visible in Western Europe, where environmental regulations penalize waste-heavy analog production

Global e-commerce growth driving demand for on-demand shipping and barcode labeling

Parcel volumes continue to climb, and every package needs a legible, regulation-compliant label. Zebra Technologies generated USD 410 million in Q3 2024 asset-tracking revenue, underscoring the indispensability of thermal barcode printers in omnichannel logistics [2]Zebra Technologies Corporation, “Q3 2024 Earnings Release,” zebra.com. Fulfillment centers value printers that handle paper, film, and linerless stocks without downtime, given the multiplicity of last-mile conditions. Cross-border sellers must apply multilingual and region-specific compliance icons, necessitating variable-data engines that operate close to pick-pack lines. Strategic acquisitions—such as Multi-Color Corporation’s purchase of RFID specialist Starport Technologies—highlight how traditional graphics printers are integrating smart modules to future-proof e-commerce workflows [3]Multi-Color Corporation, “Starport Technologies Acquisition Announcement,” mcclabel.com.

Adoption of RFID/NFC-ready smart label printers across logistics and retail

Supply chains increasingly demand real-time visibility, pushing converters toward hybrid machines that insert RFID inlays during label construction. Starport Technologies’ assets give Multi-Color Corporation the capability to create encoded labels in one pass, trimming labor and shrinkage costs. NFC tags are also migrating into premium spirits and cosmetics for authentication and consumer engagement. Pharmaceutical mandates such as Europe’s FMD have nudged early adoption, yet electronics and apparel retailers are fast followers. Upfront capital is significant because RFID units require embedded antennas, curing stations, and verification scanners, but total cost of ownership drops once reuse and analytics benefits are realized. Established vendors with global service networks benefit as small converters shy away from the complexity.

Craft beverage and small food brands insourcing label production to cut long lead times

Independent breweries and specialty food makers introduce seasonal variants every few weeks. In-house desktop presses let them print just-in-time, avoid plate fees, and iterate designs rapidly. Canon’s water-based inkjet range targets this niche, complying with indirect food-contact standards while delivering photographic quality on textured paper. The shift is particularly pronounced in the United States, where the number of craft breweries exceeded 9,000 by 2024. Variable-information capability helps these firms manage batch codes and best-by dates without outsourcing. European artisanal cheesemakers and charcuterie producers follow a similar pattern, aligning labeling agility with Protected Designation of Origin requirements.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital investment in high-speed digital presses remains a barrier to SME adoption globally | -0.8% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Global volatility in ink and substrate prices affects total cost of ownership for printers | -0.6% | Global, with regional variations in commodity exposure | Short term (≤ 2 years) |

| Worldwide regulatory push to reduce PVC shrink-sleeve use due to recyclability concerns | -0.5% | Europe and North America leading, expanding globally | Long term (≥ 4 years) |

| Global shortage of skilled operators limits efficiency in hybrid press environment | -0.4% | Global, most acute in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High capital investment in high-speed digital presses remains a barrier to SME adoption globally

A single high-volume inkjet line can exceed USD 1 million, putting it beyond the reach of typical small converters. OECD research confirms that SMEs adopt advanced production technology more slowly when financing tools and advisory programs are limited. Heidelberg derives more than 50% of its turnover from packaging presses and offsets risk by offering subscription models that bundle hardware, software, and consumables. By contrast, micro-brands often rely on outsourced print brokers or equipment leasing, inflating per-label costs in the long run. The widening technology gap can lead to market consolidation, as scale players outcompete on unit economics.

Global volatility in ink and substrate prices affects total cost of ownership for printers

Substrate prices move with energy and petrochemical markets, while certain pigments depend on scarce minerals whose supply chains are geopolitically exposed. When aluminum recyclers highlight plastic label contamination as a cost burden, converters face added scrutiny over adhesive and facestock choices. Print shops hesitate to lock long contracts for fear of margin erosion. Water-based and vegetable-oil inks sometimes carry premium prices because specialty feedstocks are sourced from limited suppliers. Geographic disparities aggravate the issue; operators close to resin plants in the Gulf Coast enjoy cost advantages over import-reliant Asian converters during freight disruptions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

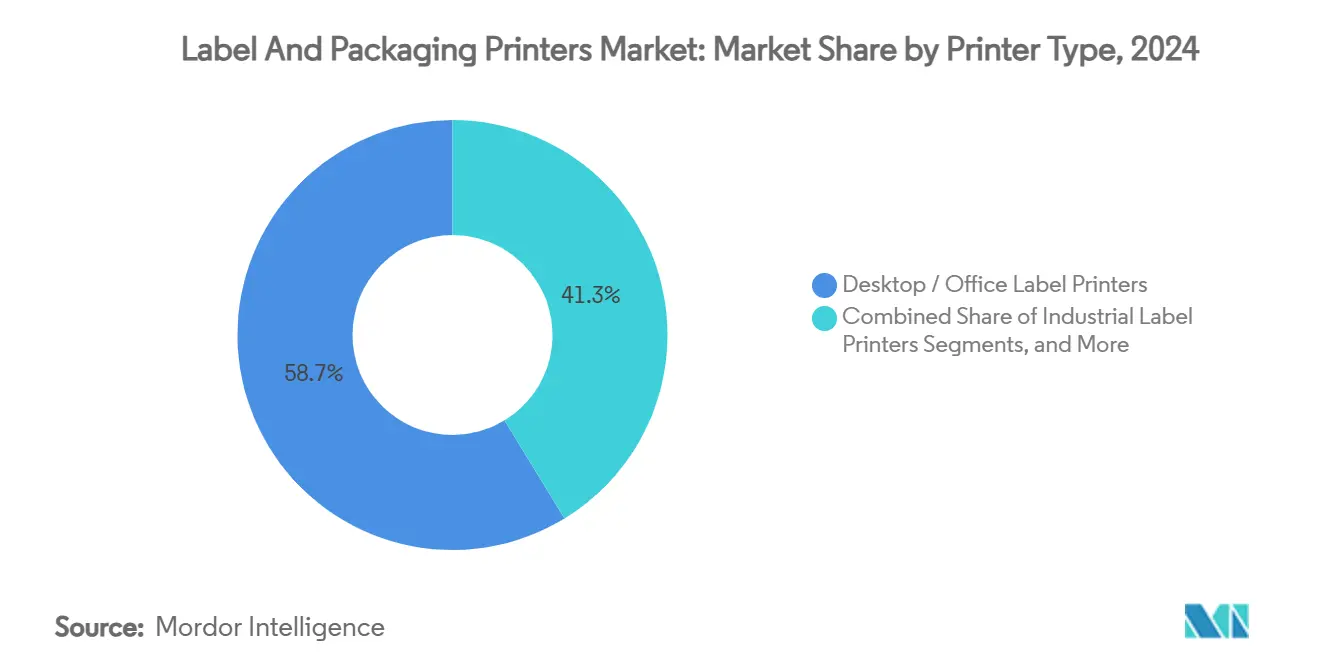

By Printer Type: Desktop Dominance Drives Volume Growth

Desktop and office units commanded 58.72% of the label and packaging printers market share in 2024, reflecting the widespread need for distributed, mid-volume labeling across healthcare, retail, and warehouse environments. These devices integrate easily with enterprise resource planning systems and require little operator training, translating into fast deployment cycles. The label and packaging printers market benefits when start-ups adopt these compact models before scaling production. Despite the prevalence of desktop machinery, high-end digital presses are forecast to register a 7.47% CAGR to 2030, propelled by increasing demand for high-resolution graphics and personalization in premium packaged goods. Vendors such as AstroNova expanded portfolios with the TrojanLabel T2-PRO, designed for converters seeking full-color short runs on specialty stocks.

A clear bifurcation is emerging: desktops address transactional labeling where cost per print is paramount, whereas industrial presses serve brand-critical displays where differentiation adds value. Economic re-shoring further elevates desktop volumes, as manufacturers print compliance labels on-site to avoid overseas delays. The shift aligns with enterprise digitization strategies that put printers at network edge points. Conversely, the label and packaging printers market size for high-speed systems is set to expand as luxury segments and OTC pharmaceuticals add augmented-reality codes that require near-perfect registration. Established manufacturers are bundling workflow automation and cloud maintenance to justify price premiums, an approach that resonates with converters chasing uptime and labor savings.

By Printing Technology: Flexographic Leadership Faces Digital Disruption

Flexographic lines held 35.81% revenue within the label and packaging printers market in 2024, buoyed by their efficiency over long production runs and decades of operator familiarity. Anilox roll improvements and low-solvent UV inks keep flexo relevant when runs exceed 100,000 linear meters. However, digital inkjet lines are projected to grow at a 7.92% CAGR, eroding flexo’s dominance in segments that value SKU agility. Hybrid presses that merge flexo priming with inline inkjet embellishment are gaining traction, offering best-of-both flexibility without multiple passes.

Electrophotography retains niches that demand tight color tolerance and opaque whites. Thermal transfer remains indispensable for harsh-environment rating plates in automotive and aerospace sectors because the resin ribbon chemistry survives solvents and extreme temperatures. Direct thermal stocks, devoid of ribbons, suit short-life shipping labels although rising phenol restrictions spur research into alternative coatings. As legislation curbs solvent exposure, water-based piezo inkjet lines receive attention from converters servicing baby food, ready-meal, and nutraceutical clients. Capital expenditure hesitancy lingers, yet financing programs and click-charge models lower entry barriers, keeping the label and packaging printers market on its digital trajectory.

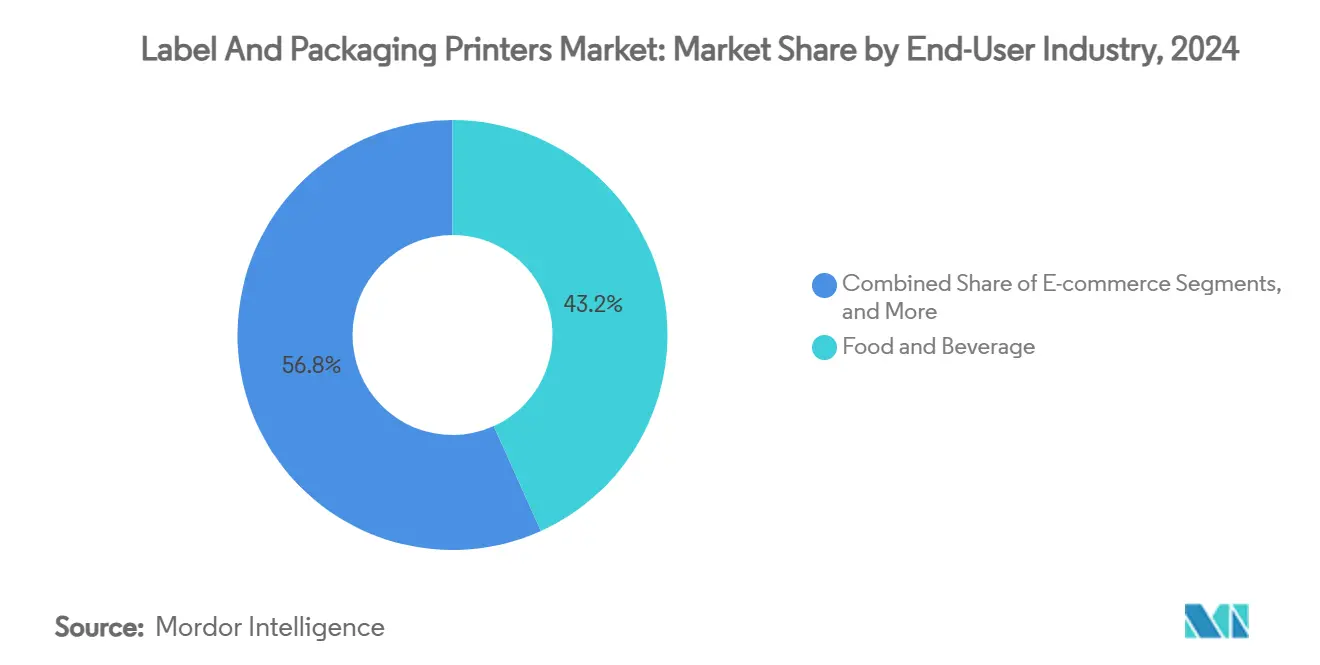

By End-User Industry: Food and Beverage Dominance Reflects Regulatory Complexity

The food and beverage segment captured 43.24% of label and packaging printers market revenue in 2024, underscoring the sector’s stringent traceability mandates and high SKU churn. Nutrition facts revisions, allergen disclosures, and multilingual labeling push converters toward digital workflows that enable late-stage customization. Craft beverage producers leverage tactile stocks and variable illustrations to differentiate seasonal releases, driving premium unit economics for printers. The label and packaging printers market size dedicated to e-commerce applications is projected to rise fastest, supported by a 7.58% CAGR through 2030 as parcel flows swell.

Pharmaceutical players demand serialization, tamper-evidence, and Braille features, steering equipment investment into vision inspection and precise die-cutting. Cosmetics brand owners prioritize metallic foils and haptic varnishes that justify investment in multi-process embellishment units. Industrial users require durable chemical-resistant labels, sustaining demand for resin ribbons and high-temperature curing. While other verticals show lower absolute volume, they collectively diversify substrate requirements, encouraging equipment vendors to design modular platforms that handle paper, BOPP, PET, and bio-plastic webs without lengthy changeovers.

Geography Analysis

Asia-Pacific held 40.67% of 2024 revenue, and the region is set to log a 7.74% CAGR through 2030, anchored by export-oriented manufacturing and the world’s largest online retail community. China’s GB 4806.1 food-contact rules spur replacement of legacy solvent presses with water-based lines, while consumer packaged goods giants install hybrid flexo-inkjet units to service 618 and Singles’ Day peaks. India’s toluene ban under FSSAI pushes converters toward compliant chemistries, and local tax stamps accelerate demand for variable-data laser overprinters. Japan and South Korea, dominated by electronics exports, specify ultra-fine barcode tolerances, sustaining investment in precision desktop thermal units.

North America remains a technology bellwether thanks to stringent FDA oversight and fast-moving craft beverage sectors. The US-Mexico-Canada Agreement’s country-of-origin labeling adds serialization layers to cross-border trade. Canadian bilingual packaging drives investment in duplex print engines that toggle English and French copy on demand. Mexico’s maquiladora hubs favor industrial printers that integrate directly with MES platforms to print compliance labels as products exit assembly lines.

Europe’s policy landscape is oriented toward carbon reduction and circularity. The bloc’s recycling framework encourages mono-material flexible packaging, which requires inks that withstand hot-washing without contaminating polymer regrind. Germany’s automotive suppliers run RFID-enabled labels for parts traceability, while Italy’s premium fashion houses adopt NFC tags for authenticity. The United Kingdom, diverging post-Brexit, mirrors many EU rules yet maintains distinct guidelines for nutritional formats, prompting converters to adopt artwork management suites capable of jurisdictional version control. Eastern European economies, notably Poland and the Czech Republic, attract FDI in packaging, triggering demand for mid-tier flexo lines.

Competitive Landscape

The label and packaging printers market features a midpoint concentration where the top five vendors account for an estimated 60% of global revenue. HP posted USD 4.5 billion in 2024 printing turnover, cementing leadership in desktop thermal and entry-production inkjet platforms. Canon’s dual-technology strategy captures both electrophotographic and inkjet segments, widening customer retention options across commercial and packaging workflows. Zebra Technologies dominates automatic identification with USD 1.255 billion Q3 2024 net sales and continues to embed cloud analytics that lock-in consumable volumes.

Strategic alliances focus on end-to-end workflow orchestration. Heidelberg bundles workflow software, color management, and predictive maintenance in subscription models to offset capital-spending hesitancy. AstroNova augmented its TrojanLabel lineup through MTEX know-how, bridging high-resolution label and light packaging applications. Mergers among regional converters indicate horizontal consolidation, as firms achieve purchasing leverage over inks and substrates while broadening customer bases. Technology roadmaps converge on sustainability, automation, and connectivity themes, steering R&D toward water-based inks, AI-driven print quality control, and machine-as-a-service contracts.

Entry barriers are rising in niche arenas such as smart labels, where in-line RFID encoding demands capital, patents, and compliance knowledge. Component suppliers collaborate with press OEMs to qualify chip inlays and high-frequency antennas. Consumable ecosystems remain critical; vendors offer proprietary inksets and ribbons, ensuring recurring revenue. After-sales support differentiates players in Asia-Pacific and Latin America, where local technicians and spare-part logistics dictate uptime. Price competition persists in commoditized desktop segments, yet premium graphic segments emphasize value-added service contracts over headline hardware discounts.

Label And Packaging Printers Industry Leaders

HP Inc.

Bobst Group SA

Mark Andy Inc.

Gallus – Heidelberger Druckmaschinen AG

Domino Printing Sciences plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Heidelberger Druckmaschinen AG forecast FY 2025/26 sales of EUR 2,350 million (USD 2,543.2 million) and an adjusted EBITDA margin up to 8%, driven by packaging solutions and digital press orders.

- March 2025: Canon Inc. reiterated water-based inkjet development as a pillar of its commercial printing expansion in its 2024 annual report.

- February 2025: HP Inc. reported Q1 FY 2025 printing revenue of USD 4.3 billion and raised its Future Ready cost-saving target to USD 1.9 billion.

- November 2024: HP Inc. closed FY 2024 with USD 4.5 billion printing revenue and 19.6% operating margin, emphasizing commercial label and packaging opportunities.

Global Label And Packaging Printers Market Report Scope

| Industrial Label Printers |

| Desktop / Office Label Printers |

| Mobile and Portable Label Printers |

| Print-and-Apply Systems |

| High-End Digital Presses |

| Flexographic |

| Offset Lithography |

| Gravure |

| Screen |

| Digital Inkjet |

| Digital Electrophotography |

| Thermal Transfer and Direct Thermal |

| Food and Beverage |

| Pharmaceuticals and Healthcare |

| Personal Care and Cosmetics |

| E-commerce |

| Industrial |

| Other End User industry (Retails and Supermarket, Chemicals, among others) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Printer Type | Industrial Label Printers | |

| Desktop / Office Label Printers | ||

| Mobile and Portable Label Printers | ||

| Print-and-Apply Systems | ||

| High-End Digital Presses | ||

| By Printing Technology | Flexographic | |

| Offset Lithography | ||

| Gravure | ||

| Screen | ||

| Digital Inkjet | ||

| Digital Electrophotography | ||

| Thermal Transfer and Direct Thermal | ||

| By End-User Industry | Food and Beverage | |

| Pharmaceuticals and Healthcare | ||

| Personal Care and Cosmetics | ||

| E-commerce | ||

| Industrial | ||

| Other End User industry (Retails and Supermarket, Chemicals, among others) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the label & packaging printers market and its expected growth?

The market stands at USD 10.24 billion in 2025 and is projected to reach USD 13.90 billion by 2030, driven by a 6.30% CAGR.

Which printer type holds the largest revenue share today?

Desktop and office label printers account for 58.72% of 2024 revenue because they meet distributed, mid-volume labeling needs across retail, healthcare, and logistics operations.

Why are high-end digital presses growing faster than other printer categories?

Brands need premium graphics and on-demand personalization; as a result, high-end digital presses are forecast to expand at a 7.47% CAGR through 2030.

What regulations are having the biggest impact on technology choices?

Food-contact rules such as FDA 21 CFR Parts 174-176 and China’s GB 4806.1 are pushing converters toward water-based, low-migration inkjet systems.

Which region leads the label & packaging printers market?

Asia-Pacific commands 40.67% of 2024 revenue and is projected to post a 7.74% CAGR to 2030 thanks to its manufacturing scale and fast-growing e-commerce sector.

Page last updated on: