Binding Machines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

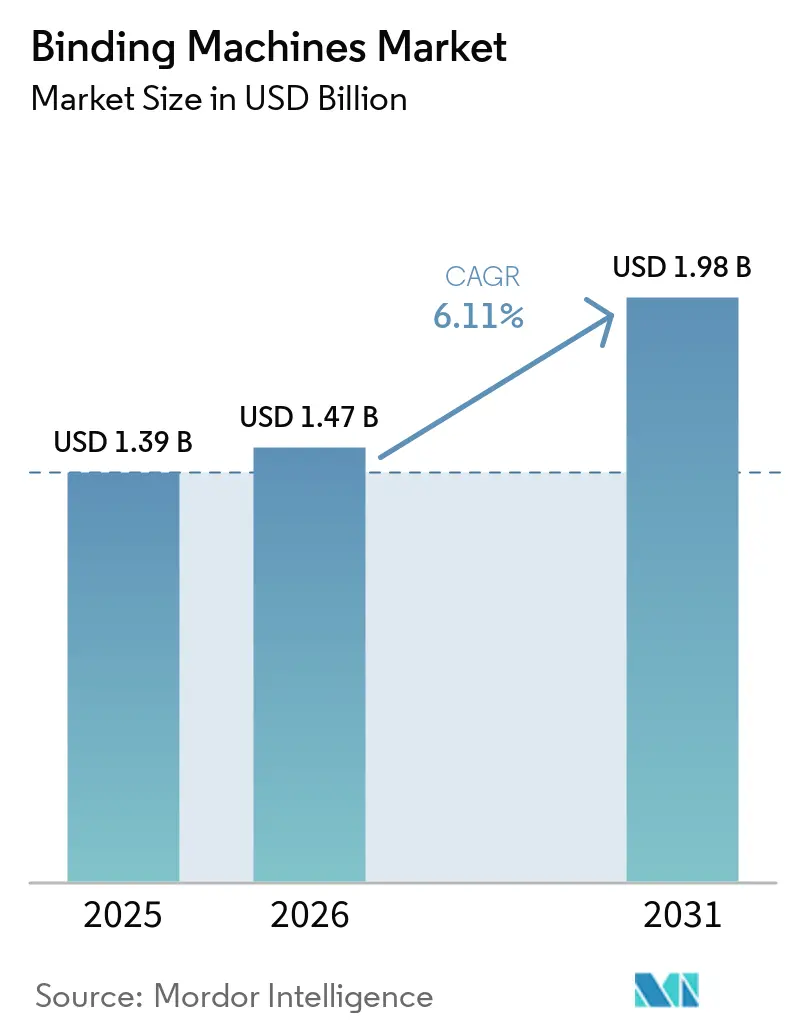

| Market Size (2026) | USD 1.47 Billion |

| Market Size (2031) | USD 1.98 Billion |

| Growth Rate (2026 - 2031) | 6.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Binding Machines Market Analysis by Mordor Intelligence

The binding machines market size is expected to increase from USD 1.39 billion in 2025 to USD 1.47 billion in 2026 and reach USD 1.98 billion by 2031, growing at a CAGR of 6.11% over 2026-2031. Improvements in adhesive chemistry, a pivot toward automated thermal systems, and consolidation among European wire-binding vendors are helping vendors capture value even as routine office comb-binding volumes taper. Demand is shifting toward higher-margin applications such as tamper-evident legal binding, photobook production, and inline finishing on digital presses, which offsets the volume slide in entry-level manual machines. Portfolio diversification is another visible trend; large incumbents are acquiring companies in adjacent office-technology categories to hedge against slower unit growth in the core binding machines market. Regionally, North America remains the single largest value pool, but Asia-Pacific is adding the most incremental revenue through school-construction programs and wage-driven automation upgrades.

Key Report Takeaways

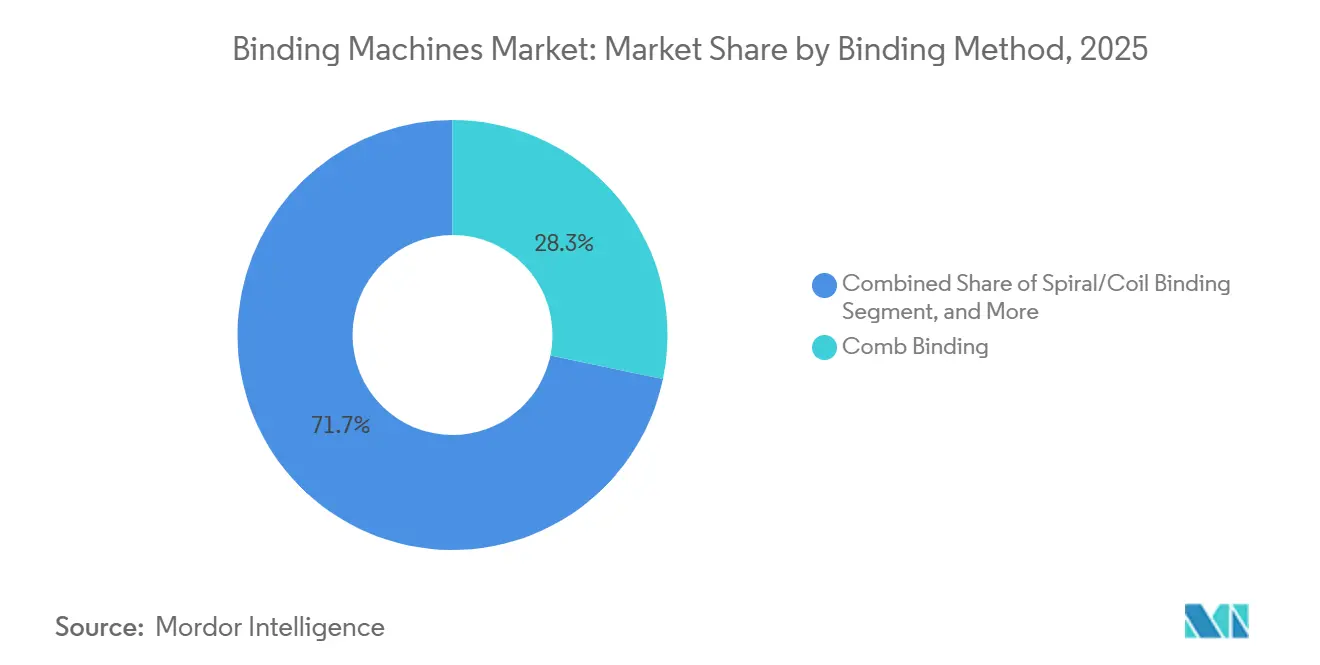

- By binding method, comb binding led with 28.28% of the binding machines market share in 2025, while thermal systems using EVA and PUR adhesives are advancing at a 6.58% CAGR through 2031.

- By operation mode, manual equipment held 45.51% of the market share in 2025, whereas fully automatic systems are projected to expand at a 7.05% CAGR between 2026 and 2031.

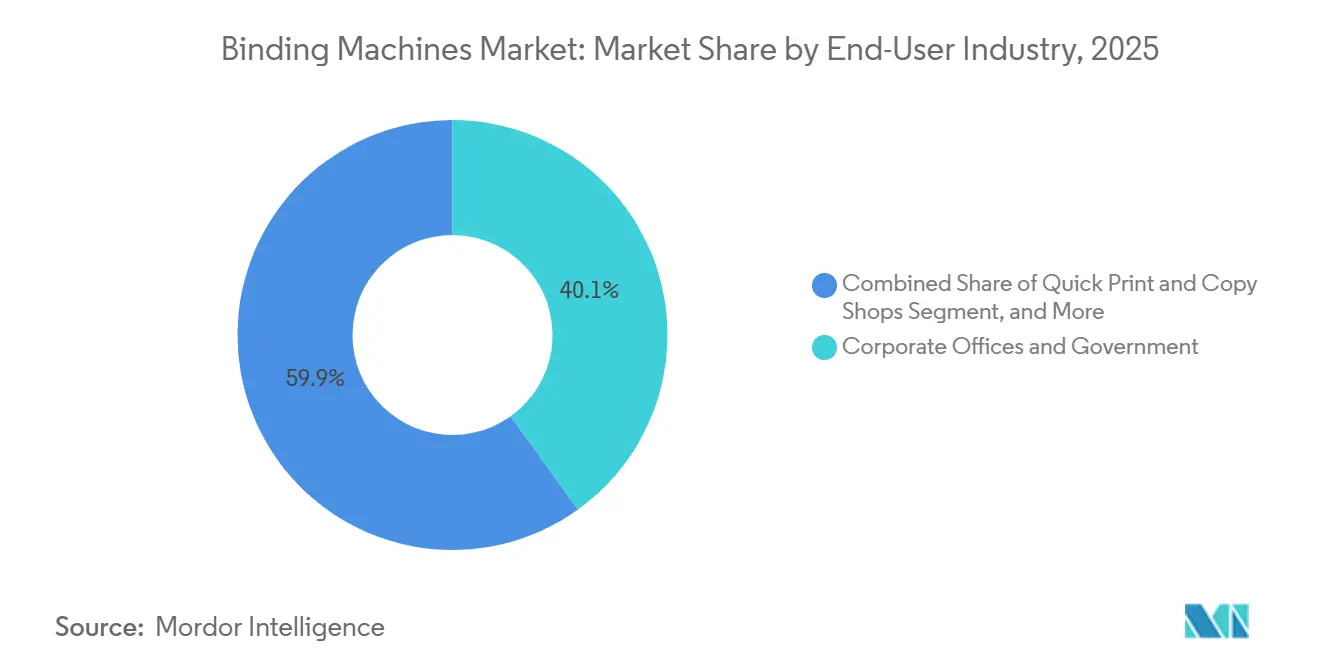

- By end-user industry, corporate offices and government agencies commanded 40.08% of the binding machines market share in 2025, yet quick-print and copy shops are forecast to register the highest CAGR at 6.93% through 2031.

- By distribution channel, specialty dealers and resellers captured 35.34% of the share in 2025, while online retail is on track for 6.24% CAGR growth up to 2031.

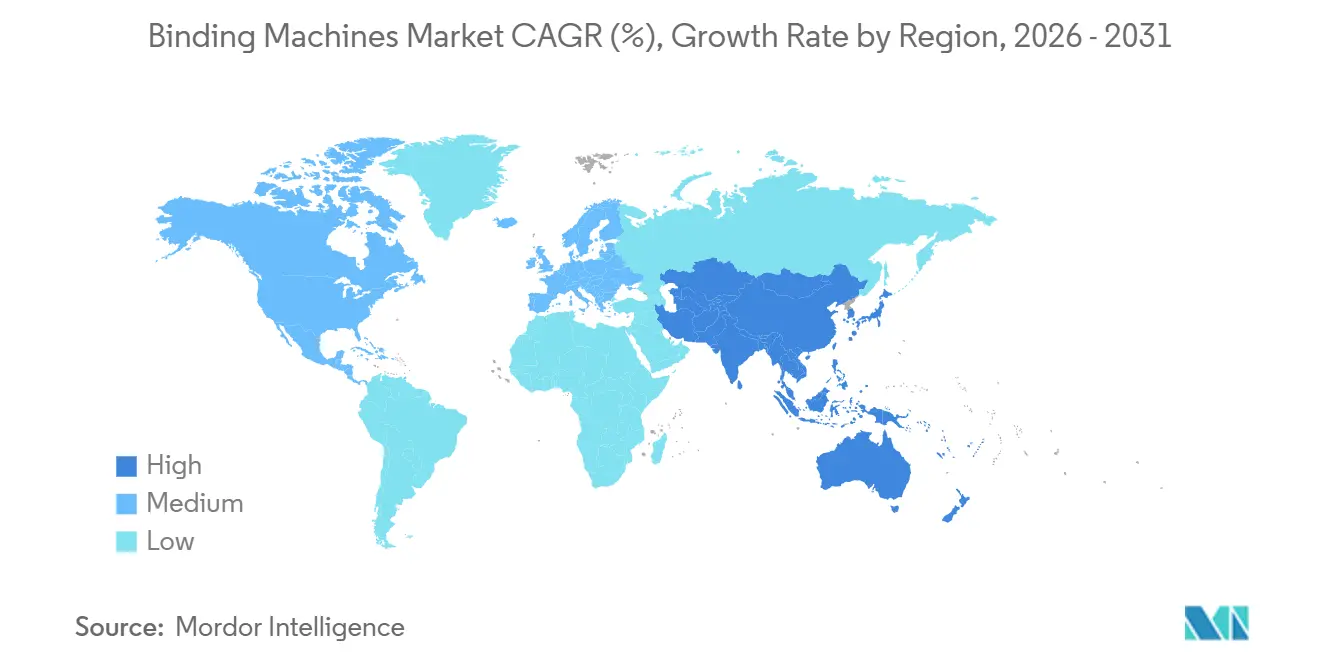

- By geography, North America dominated the binding machines market with 33.13% market share in 2025, and Asia-Pacific is projected to post a 7.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Binding Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Automated and Electric Binding Solutions | +1.2% | North America, Europe | Medium term (2-4 years) |

| Growth of On-Demand and Self-Publishing Services | +1.0% | North America, Asia-Pacific | Medium term (2-4 years) |

| Expansion of Educational Infrastructure Worldwide | +0.9% | Asia-Pacific, Middle East and Africa | Long term (≥ 4 years) |

| Rising Adoption of Office Automation Hardware | +0.8% | North America, Europe | Short term (≤ 2 years) |

| Adoption of Sustainable and Recyclable Consumables | +0.5% | Europe, North America | Medium term (2-4 years) |

| Niche Demand for Tamper-Evident Binding in Legal Sector | +0.3% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift Toward Automated and Electric Binding Solutions

Commercial print shops and quick-copy centers are automating finishing lines to shrink labor costs and cut turnaround times. Fully automatic PUR binders that connect directly to digital presses now process more than 500 cycles each hour, driving per-book labor down by up to one-third. Fastbind’s 2025 ONE Series introduced touchscreen controls and automatic thickness sensing, helping mid-volume users move away from manual thermal units.[1]Fastbind, “ONE Series Thermal Binding Machines,” FASTBIND.COM Automation also supports workplace safety because electric punching lowers repetitive-strain incidents, an occupational-health focus across Europe and North America. In markets where hourly wages surpass USD 20, the investment pays back in less than two years when weekly volumes exceed 500 books. The trend is gaining traction in China and India as rising wages narrow the historical labor-cost advantage.

Growth of On-Demand and Self-Publishing Services

Self-publishers and digital storefronts require highly flexible binding that handles single-copy runs and variable page counts without sacrificing durability. Kindle Direct Publishing and other platforms route thousands of micro-orders a day to automated perfect binders that must ship within 24 hours. Photobook kiosks prefer PUR because it resists cracking on glossy paper, a quality consumers expect for wedding albums and travel books. Quick-print shops increase revenue by bundling personalized covers and specialty laminates, and by encouraging investment in multi-mode machines that switch between comb, wire, and thermal setups in minutes. Asia-Pacific is witnessing strong uptake as disposable incomes rise and gift-oriented print products gain popularity.

Expansion of Educational Infrastructure Worldwide

Government spending on new schools drives volumes for lower-cost manual and semi-automatic machines. India’s National Education Policy and similar initiatives in Indonesia and several African nations are funding libraries, administration centers, and student resource rooms that all require document finishing equipment. Universities in Southeast Asia are upgrading thesis-binding centers, a process that often replaces aging comb units with semi-automatic wire punch systems. Over the next four years, the procurement pipeline in Asia-Pacific and parts of the Middle East keeps this driver firmly positive, even though initial deployments skew toward cost-sensitive manual models.

Rising Adoption of Office Automation Hardware

Enterprises are migrating binding devices into managed fleet contracts that bundle printers, laminators, and shredders. Usage data harvested from cloud portals schedules preventive maintenance and auto-reorders consumables, improving uptime for centralized reprographic hubs. ACCO Brands reported rising service-contract revenue in Q1 2026, confirming the pivot from transactional equipment sales to subscription models. Corporate hybrid-work policies have trimmed per-employee print volumes, yet consolidated print rooms still handle aggregate demand, supporting a modest equipment refresh cycle that favors electric punch comb and wire binders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Digital Documentation and E-Signature Uptake | -1.5% | North America, Europe | Short term (≤ 2 years) |

| High Capital Cost of Fully Automatic Systems for SMEs | -0.8% | Asia-Pacific, South America | Medium term (2-4 years) |

| Supply-Chain Volatility for Steel and Plastic Components | -0.6% | Global | Short term (≤ 2 years) |

| Growing Refurbished Equipment Market Depressing New Sales | -0.5% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Digital Documentation and E-Signature Uptake

Electronic signatures already cover 95% of corporate contract workflows in North America, eroding the need to print, collate, and bind physical documents.[2]DocuSign, “Corporate E-Signature Adoption,” DOCUSIGN.COM Regulatory frameworks such as ESIGN in the United States and eIDAS in Europe accept digital records as legally equivalent to paper copies, removing a key reason offices once retained bound originals. Collaborative cloud platforms further replace paper manuals with searchable PDFs and shared digital workspaces. Government bodies and universities still rely on physical archiving in some cases, but their migration pace is accelerating, keeping this restraint front-loaded in the forecast horizon.

High Capital Cost of Fully Automatic Systems for SMEs

Entry pricing for industrial PUR binders exceeds USD 50,000, a barrier for many small copy shops and regional publishers. Although leasing schemes exist, higher interest rates and strict credit scoring exclude marginal borrowers. Where wage costs remain low, particularly in South America and parts of Southeast Asia, operators find it cheaper to run manual or semi-automatic machines even if throughput is modest. Until component prices ease or low-cost Asian brands reach maturity, this cost hurdle will continue to cap penetration in the SME segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Binding Method: Thermal Systems Gain on Durability Demands

Thermal binding techniques using EVA and PUR adhesives are projected to post the fastest growth at 6.58% from 2026-2031, fueled by photobook kiosks, on-demand publishers, and corporate presentations that require lay-flat spines and strong adhesion. PUR formulas cure through moisture rather than cooling, delivering up to 60% higher pull strength than EVA, which guarantees longevity for high-gloss photo papers. Machines such as the Duplo DPB-500 process more than 500 books an hour to meet quick-turn workflows, while desktop models priced around EUR 4,500 (USD 5,040) serve small studios. Comb binding retained a 28.28% share in 2025 because plastic combs cost as little as USD 0.10 each and allow easy page replacement, an advantage valued in training manuals and internal reports.

The ongoing shift toward digital presses has heightened interest in PUR, as it handles coated stocks produced by HP Indigo or Xerox iGen devices. Although PUR consumables cost about three times as much as EVA, operators use one-third as much adhesive per book, narrowing the cost gap. Wire binding remains essential for legal submissions and regulatory filings that require tamper-evident security, while spiral and coil binding dominate calendars and notebooks thanks to 360-degree rotation. Perfect binding and saddle-stitch cover softcover books and catalogs in commercial runs, and book-sewing persists in high-end hardcover production.

By Operation Mode: Automation Driven by Labor Economics

Manual machines accounted for 45.51% of the market in 2025, driven by sub-USD 500 pricing and simplicity, but their throughput is limited to roughly 20 books per hour. Semi-automatic units ranging from INR 180,000 to INR 350,000 (USD 2,160-4,200) speed punching or crimping for mid-volume users such as university print rooms. Fully automatic systems are forecast to grow at 7.05% through 2031 because quick-print shops and commercial printers value labor savings and consistent quality.

A C.P. Bourg BB3202 PUR binder linked inline to a digital press can run lights-out shifts, trimming per-unit labor by up to 35%. Labor-cost math drives the automation uptick, at an hourly wage of USD 20, a USD 50,000 system pays for itself within 18 months when weekly volumes exceed 500 units. Meanwhile, educational institutions with intermittent usage continue to rely on affordable manual machines. Automation adoption in China and India is poised to accelerate as wage inflation shortens payback periods.

By End-User Industry: Quick-Print Shops Capture On-Demand Surge

Quick-print and copy shops are on pace for the highest growth, a 6.93% CAGR to 2031, as wedding albums, corporate events, and personalized gifts shift toward same-day fulfillment. These operators invest in machines that toggle between comb, wire, and thermal modes, enabling them to handle diverse client requests without extensive setup downtime. Corporate offices and government agencies still represent 40.08% of demand, sustained by routine internal communication needs, yet digital workflows are eroding their volume base.

Commercial printers deploy inline perfect binders connected to high-speed presses to capture longer runs of magazines and catalogs, prioritizing speed over flexibility. Educational institutions continue to favor manual and semi-automatic platforms for thesis and dissertation finishing, funded by national infrastructure programs in the Asia-Pacific. Specialty segments, such as hobbyists and kiosk photobook outlets, provide small but consistent demand, emphasizing the heterogeneous nature of the binding machines market.

By Distribution Channel: E-Commerce Pressures Dealer Margins

Specialty dealers and resellers accounted for 35.34% of revenue in 2025, as they bundle training, maintenance, and consumables. However, buyers increasingly research and transact online, pushing e-commerce platforms toward a forecast CAGR of 6.24% through 2031. Bruneau.nl carried 127 SKUs in 2025, with transparent pricing that narrows dealer margins.[3]Bruneau, “Binding Machines Catalog,” BRUNEAU.NL Direct sales teams focus on high-value corporate and commercial-print accounts that require custom configurations, while office-supply superstores still move entry-level units even as store footprints contract.

E-commerce growth is most pronounced in North America and Europe owing to next-day logistics networks. In the Asia-Pacific region, Alibaba and Shopee are expanding their business-to-business catalogs, accelerating the shift to online. Dealers still offer a service advantage for complex installations, but manual and semi-automatic units remain vulnerable to price competition on digital storefronts.

Geography Analysis

North America accounted for 33.13% of the binding machines market in 2025, driven by its mature corporate sector and a dense network of quick-print centers. Many legacy manual units installed in the 1990s are now approaching obsolescence, creating a steady replacement pipeline. Electronic signature penetration at 95% has trimmed office binding volumes, yet demand from photobook producers and self-publishers partially offsets the decline. The United States remains the region’s anchor market, supported by a large commercial-print industry and diversified corporate spending.

Asia-Pacific is forecast to expand at a 7.12% CAGR through 2031, the fastest among all regions. India’s education infrastructure drive under the National Education Policy finances equipment for libraries and administrative hubs in more than one million schools. Chinese printers are migrating from manual to automated machines to win export business that requires PUR binding for coated paper. Japan and South Korea contribute steady replacement volumes, while Indonesia, Vietnam, and Thailand show rapid greenfield growth tied to emerging middle-class consumption of personalized print goods.

Europe maintains a stable share propelled by commercial-print hubs in Germany, France, and the United Kingdom. The European Union’s circular-economy agenda boosts demand for bio-based adhesives, encouraging vendors to develop recyclable consumables. Consolidation is reshaping the regional landscape following Plockmatic Group's June 2025 acquisition of Renz, creating a stronger platform for wire-binding products. The Middle East and Africa show nascent growth led by school construction in Gulf Cooperation Council states and parts of sub-Saharan Africa.[4]Ministry of Education, “National Education Policy 2020 Implementation Status,” EDUCATION.GOV.IN In South America, Brazil and Argentina sustain baseline demand despite macro-economic volatility, with spending concentrated in education and government segments.

Competitive Landscape

The market is moderately concentrated. Companies like ACCO Brands (owner of GBC and Renz), Fellowes, and James Burn International together dominate the manual and semi-automatic categories through entrenched dealer networks and consumable programs. The January 2026 acquisition of EPOS by ACCO Brands underscores diversification away from low-growth legacy office products. Plockmatic Group’s purchase of Renz consolidates two European specialists, expanding access to inline finishing systems for digital presses.[5]Plockmatic Group, “Plockmatic Group Acquires Renz GmbH,” PLOCKMATIC.COM

Niche players such as Fastbind, Duplo, and Morgana compete on technology by offering dual EVA-PUR capability, automatic thickness detection, and cloud-based fleet analytics. Chinese manufacturers like Zhejiang Yunguang Machinery and Shanghai Loretta Machinery undercut incumbents in price-sensitive markets, accelerating commoditization in the lower tiers. Refurbished-equipment suppliers depress new-unit sales by selling remanufactured manual binders at 30-50% discounts, especially appealing to cost-conscious schools and small offices.

Long-term opportunities exist in developing security-focused, tamper-evident solutions and sustainable consumables that comply with stringent European regulations. Companies that can effectively integrate binding processes into high-speed digital print lines while also supporting eco-friendly adhesives are well-positioned to capitalize on premium margins. As the binding machine industry continues to evolve, these capabilities will become increasingly critical for vendors seeking to maintain a competitive edge.

Binding Machines Industry Leaders

ACCO Brands (GBC)

Duplo Corporation

Fellowes Brands

James Burn International (JBI)

Vivid Laminating Technologies Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: ACCO Brands completed its acquisition of EPOS, diversifying into premium audio peripherals amid slowing demand for legacy binding equipment.

- June 2025: Duplo has acquired Bar Graphic Machinery (BGM), a leading UK manufacturer of high-performance finishing equipment for the labels and packaging sector.

- August 2025: Plockmatic Group acquired Renz GmbH, strengthening its ring-wire portfolio and enabling cross-sales of automated inline finishing systems.

- January 2025: Heidelberger Druckmaschinen AG opened its 175th anniversary year by outlining a growth strategy targeting over EUR 300 million (USD 353 million) in additional sales by 2029, with the digital printing addressable market expected to expand from EUR 5 billion (USD 5.8 billion) to EUR 7.5 billion (USD 8.84 billion).

Global Binding Machines Market Report Scope

The Binding Machines Market encompasses the global industry that manufactures, distributes, and sells machines and equipment used to assemble, fasten, and finish printed or written documents into organized bound formats. These machines are utilized across commercial, institutional, and industrial environments to improve document presentation, durability, storage, and professional appearance.

The Binding Machines Market Report is Segmented by Binding Method (Comb Binding, Wire Binding, Spiral/Coil Binding, Thermal Binding, Perfect Binding, Saddle Stitch and Book Sewing, and Tape and Velo Binding), Operation Mode (Manual, Semi-Automatic, and Fully Automatic), End-User Industry (Corporate Offices and Government, Commercial Print and Publishing Houses, Quick Print and Copy Shops, Educational Institutions, and Other End-User Industries), Distribution Channel (Direct Sales and OEM, Specialty Dealers and Resellers, Office Supply Superstores, and Online Retail/E-commerce), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Comb Binding |

| Wire Binding |

| Spiral/Coil Binding |

| Thermal Binding |

| Perfect Binding |

| Saddle Stitch and Book Sewing |

| Tape and Velo Binding |

| Manual |

| Semi-Automatic |

| Fully Automatic |

| Corporate Offices and Government |

| Commercial Print and Publishing Houses |

| Quick Print and Copy Shops |

| Educational Institutions |

| Other End-user Industries |

| Direct Sales and OEM |

| Specialty Dealers and Resellers |

| Office Supply Superstores |

| Online Retail/E-commerce |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Binding Method | Comb Binding | |

| Wire Binding | ||

| Spiral/Coil Binding | ||

| Thermal Binding | ||

| Perfect Binding | ||

| Saddle Stitch and Book Sewing | ||

| Tape and Velo Binding | ||

| By Operation Mode | Manual | |

| Semi-Automatic | ||

| Fully Automatic | ||

| By End-User Industry | Corporate Offices and Government | |

| Commercial Print and Publishing Houses | ||

| Quick Print and Copy Shops | ||

| Educational Institutions | ||

| Other End-user Industries | ||

| By Distribution Channel | Direct Sales and OEM | |

| Specialty Dealers and Resellers | ||

| Office Supply Superstores | ||

| Online Retail/E-commerce | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current binding machines market size and where will it stand by 2031?

The market is valued at USD 1.47 billion in 2026 and is projected to reach USD 1.98 billion by 2031, reflecting a 6.11% CAGR, according to Mordor Intelligence.

Which binding method is growing the fastest?

Thermal binding, particularly PUR-based systems, is forecast to expand at 6.58% through 2031 due to demand for durable, lay-flat photo and corporate books.

Why are fully automatic binding systems gaining traction?

Labor savings, faster throughput, and inline integration with digital presses make automatic machines attractive where hourly wages top USD 20.

How will e-commerce affect traditional binding equipment dealers?

Online platforms offering transparent pricing and broad product ranges are expected to grow at 6.24% CAGR, tightening margins for specialty dealers.

Which region offers the highest growth potential?

Asia-Pacific is projected to record a 7.12% CAGR to 2031, supported by school-construction programs and automation upgrades in China and India.

What is a key technological trend shaping competitive dynamics?

Dual EVA-PUR capability combined with cloud-based fleet management is allowing vendors to capture premium segments that demand both flexibility and uptime.

Page last updated on: