Digital Check Scanning Solutions Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

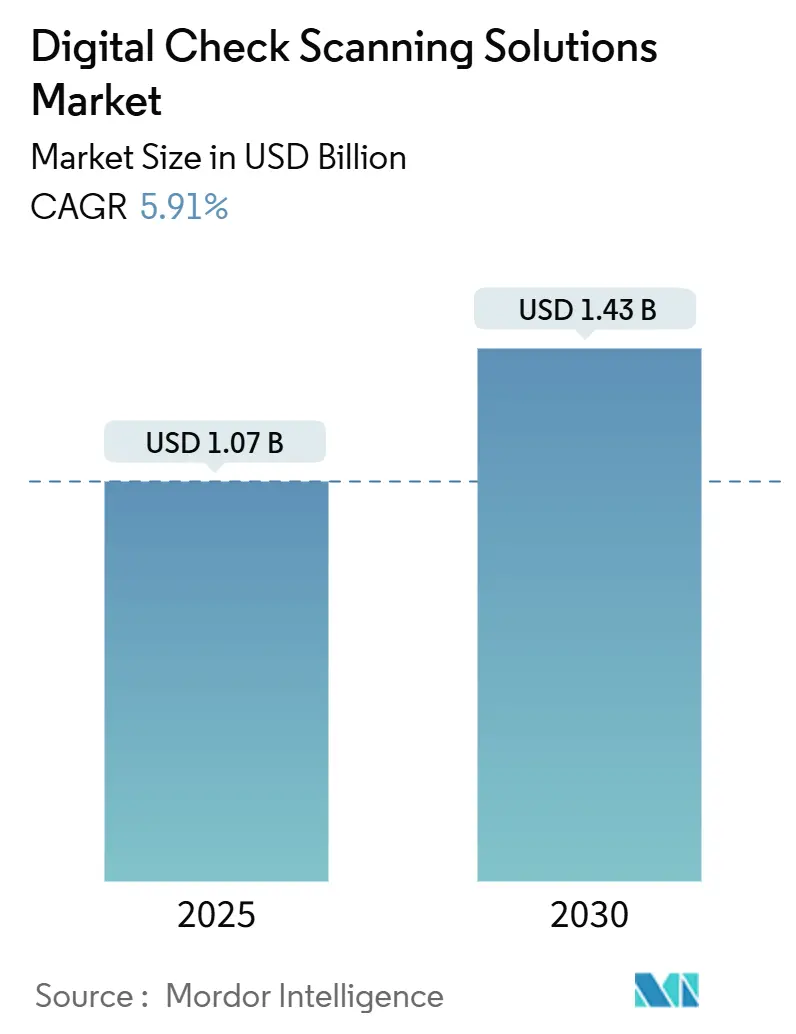

| Market Size (2025) | USD 1.07 Billion |

| Market Size (2030) | USD 1.43 Billion |

| Growth Rate (2025 - 2030) | 5.91% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Check Scanning Solutions Market Analysis by Mordor Intelligence

The digital check scanning solutions market size stands at USD 1.07 billion in 2025 and is forecast to reach USD 1.43 billion by 2030, reflecting a 5.91% CAGR across the period. Maturing branch-transformation programs, strict truncation mandates and the need for real-time fraud analytics keep capital flowing into image-based processing even as total check volumes contract. Institutions accelerate upgrades to multi-feed and mobile capture platforms to balance high-volume branch workflows with consumer self-service, while cloud-hosted deployments gain traction because they lower IT overhead and embed always-current fraud models. Vendor strategies center on open, API-free architectures that slipstream into teller, treasury and mobile apps without core-system dependencies, reducing deployment risk and shortening payback cycles. Consolidation among hardware and software specialists continues as manufacturers seek scale and cross-sell opportunities in integrated cash and check automation.

Key Report Takeaways

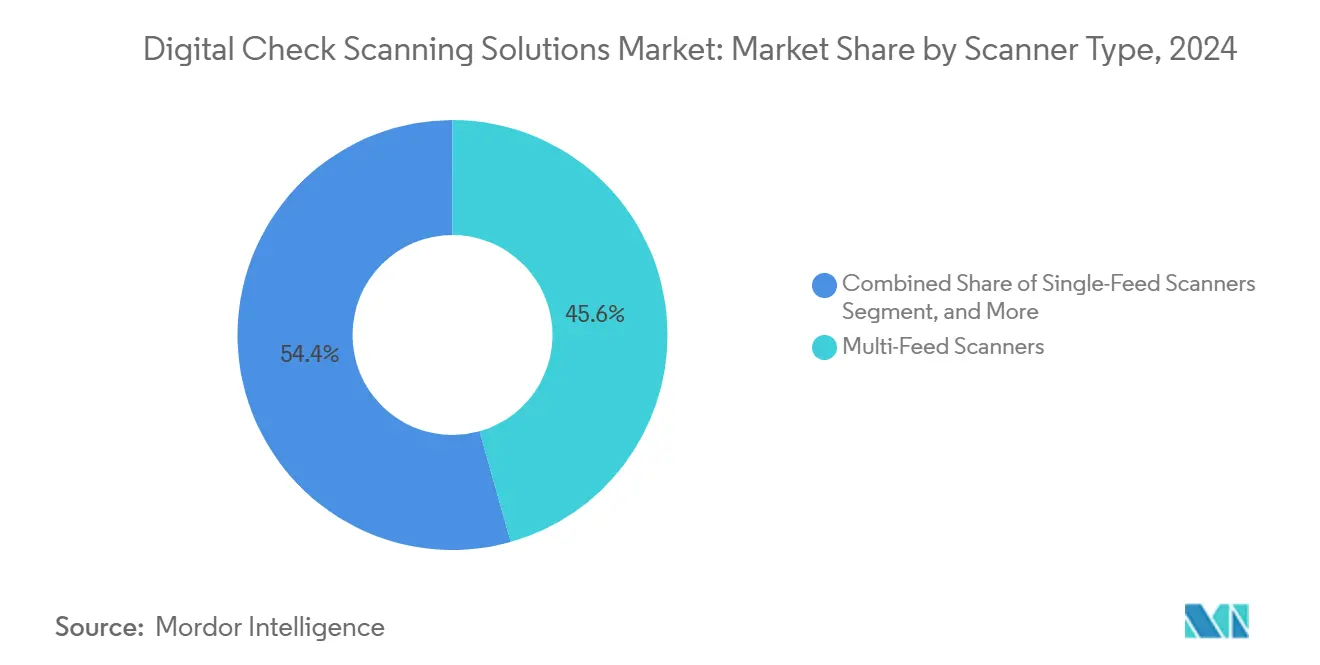

- By scanner type, multi-feed scanners led with 45.63% revenue share in 2024; mobile/smart-device scanners are forecast to expand at a 6.43% CAGR through 2030.

- By end user, commercial banks held 54.32% of the digital check scanning solutions market share in 2024, while corporate/SME treasury segments are projected to grow at a 6.31% CAGR through 2030.

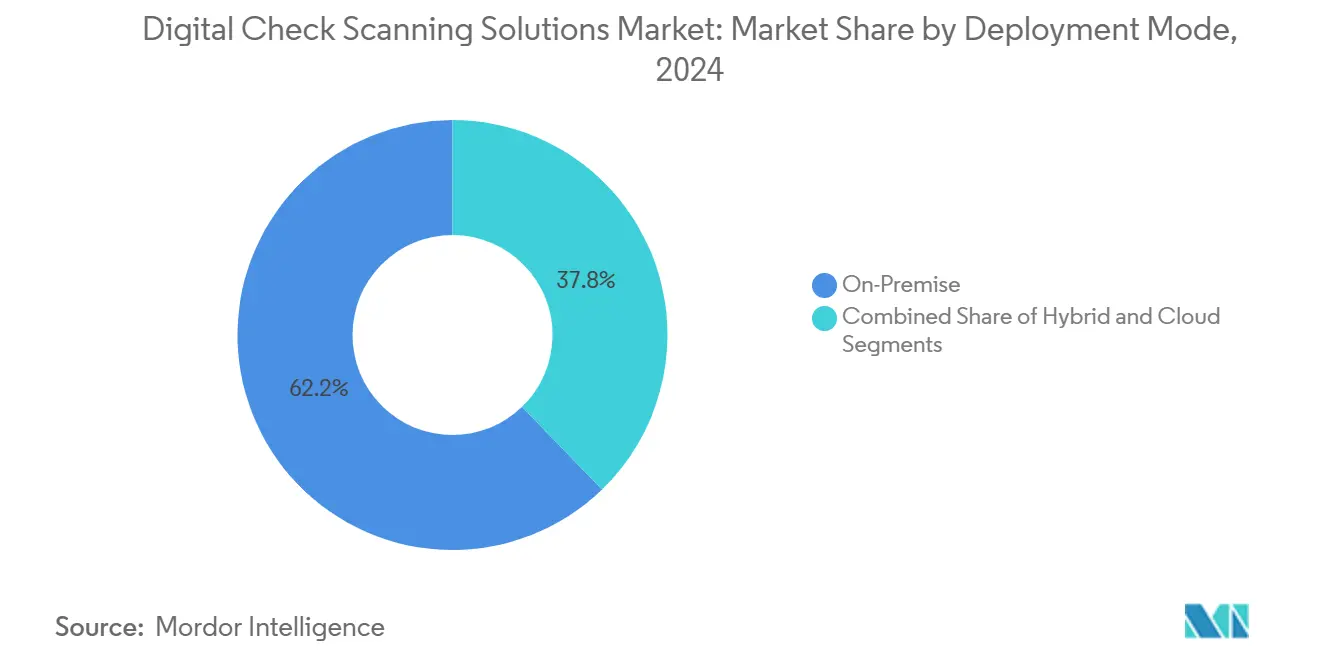

- By deployment mode, on-premise implementations accounted for 62.24% share of the digital check scanning solutions market size in 2024; cloud-hosted solutions are anticipated to rise at a 7.34% CAGR through 2030.

- By Application, Branch/Teller Capture accounted for 39.81% share of the digital check scanning solutions market size in 2024; Mobile Deposit is anticipated to rise at a 6.13% CAGR through 2030.

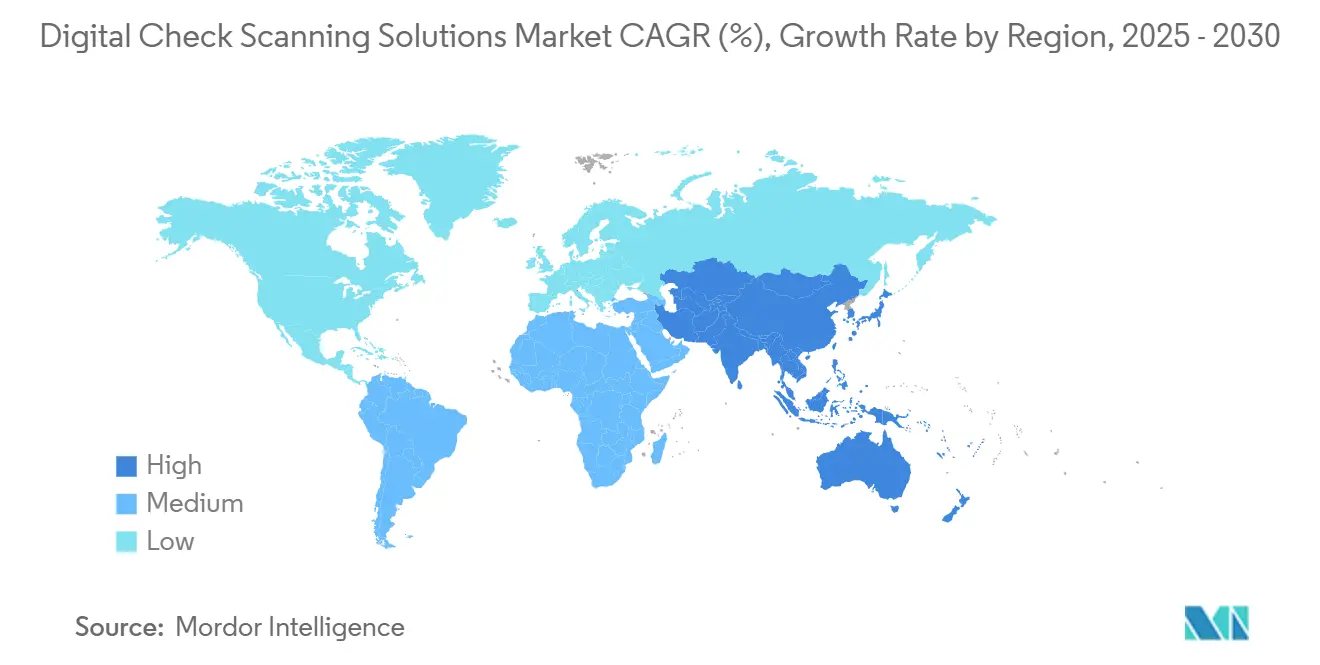

- By geography, North America captured 36.74% revenue share of the digital check scanning solutions market in 2024, whereas Asia-Pacific is set to register a 6.87% CAGR through 2030.

Global Digital Check Scanning Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift toward branch-less "phygital" banking | +1.8% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Mandated truncation rules and Check 21-type regulations expanding outside U.S. | +1.2% | North America core, expanding to Asia-Pacific and EU | Long term (≥ 4 years) |

| SME demand for multi-feed scanners to cut lockbox fees | +0.9% | North America and EU, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Cloud-native RDC platforms bundling hardware subscriptions | +1.1% | Global, led by North America | Medium term (2-4 years) |

| AI-powered fraud analytics embedded in scanners | +0.7% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Rise of instant payments pushing back-office image capture upgrades | +0.4% | EU leading, North America and Asia-Pacific following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid shift toward branch-less “phygital” banking

Banks re-imagine retail footprints around roaming tellers and self-service zones that unbundle transactional tasks from the counter. Scanners that operate wirelessly and interact with tablets or lobby kiosks let staff originate deposits wherever customers stand, compressing queue times and raising cross-sell opportunities. [1]Panini S.p.A., “EverneXt Wireless Capture,” panini.comCredit-union adopters such as Royal Credit Union rely on unified Day 1/Day 2 platforms to centralize image exchange, trimming back-office labor and accelerating funds availability. Because API-free firmware communicates through browser calls, institutions sidestep core-upgrade projects and tighten time-to-value. Check 21 rules give legal cover for truncated images, so smaller banks comfortably retire legacy transports. As every branch turns into a miniature processing hub, the digital check scanning solutions market gains volume even in pockets where foot traffic falls.

Mandated truncation rules and Check 21-type regulations expanding outside the U.S.

Two decades of Check 21 experience prove that digital images cut fraud and float, encouraging similar statutes across Europe, Asia and Latin America. [2]Digital Check Corp., “20 Years of Check 21,” digitalcheck.com The European Instant Payments Regulation obliges banks to settle in seconds, a goal that hinges on reliable image capture for those transactions that still originate on paper. Japan folds image-based standards into broader banking digitization, tightening interoperability with cash-less platforms. U.S. Treasury upgrades to the Treasury Check Verification System (TCVS) provide extra payee analytics that overseas regulators monitor as a model for their own rollouts. Each new jurisdiction written into law anchors multi-year equipment refresh cycles, cushioning the digital check scanning solutions market against domestic volume attrition.

SME demand for multi-feed scanners to cut lockbox fees

Mid-sized corporates scrutinize lockbox charges that can reach USD 0.20 per cleared item; internalizing deposits saves thousands monthly and shrinks DSO. Love’s Travel Stops processes roughly 45 000 checks every month via automated treasury workstations, illustrating the ROI of in-house capture. [3]GTreasury, “Love’s Travel Stops Treasury Automation,” gtreasury.com Multi-feed scanners strike the sweet spot of 100–1 000 items per batch, fitting treasury desks that require speed but not the bulk of back-office transports. Banks enhance stickiness by bundling remote deposit capture portals that reconcile batches against receivables files, leaving SMEs with real-time cash visibility. Because regulations already sanction remote capture, adoption cycles are measured more by cash-management priorities than by compliance hurdles, channeling a steady stream of hardware orders.

Cloud-native RDC platforms bundling hardware subscriptions

Vendors now ship scanners on a pay-per-month basis that combines device, maintenance, SOC 2 reporting and analytic upgrades in one invoice, replacing sporadic capex with opex. Community banks gain enterprise-grade defenses without hiring data-science teams: Alogent Shield continually refines risk models across a consortium data lake and pushes them to every tenant. Subscription refresh guarantees new feeders every 36 months, so institutions never fall behind image-quality thresholds demanded by clearinghouses. Because pricing flexes with item counts, banks that experience organic check decline stay cost-aligned, preserving margins. Certifications such as Digital Check’s SOC 2 Type 2 reassure examiners that cloud storage meets audit expectations. This design unlocks latent demand from Tier-3 banks that previously postponed replacements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining overall paper-check volumes in mature markets | -1.4% | North America and EU primarily | Long term (≥ 4 years) |

| Capital spending freezes at Tier-2/3 banks | -0.8% | Global, concentrated in smaller institutions | Short term (≤ 2 years) |

| High false-reject rates in mobile auto-capture driving user churn | -0.6% | Global, affecting consumer segments | Medium term (2-4 years) |

| Cyber-risk and data-sovereignty concerns for cloud RDC | -0.3% | Global, varying by regulatory environment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Declining overall paper-check volumes in mature markets

U.S. federal directives will remove paper benefits checks by September 2025, wiping out a sizable workload for lockbox operators. Consumer migration to P2P wallets and instant transfers accelerates secular decline; volumes have dropped 75% since 2000 according to Federal Reserve postings. Banks respond by optimizing scanners for premium corporate and real-estate items where alternate rails remain sparse, but aggregate feed duty cycles slide, sometimes shortening refresh cycles. Vendors hedge with feature-rich firmware that commands higher ASPs per unit sold. Yet the unavoidable glide path of check displacement subtracts 1.4 percentage points from the forecast CAGR, tempering otherwise healthy hardware shipments.

Capital spending freezes at Tier-2/3 banks

Rising cost-of-funds and tighter net-interest margins compel community banks to defer branch equipment upgrades. Boards route scarce budgets toward digital-account origination or compliance fixes, leaving scanner fleets to age past five-year duty lives. Field technicians report upticks in misfeeds and image failures that push re-clear volumes higher, but CFOs still ration capex. Vendors counter with lease-to-own plans and remote firmware assist that stretch useful life, yet adoption lags compared with credit-union peers who treat scanning as a member-service differentiator. The spending drought is most acute in rural regions where branch density is high and return-on-assets thin, lopping another 0.8 points off the digital check scanning solutions market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Scanner Type: Multi-feed dominance meets mobile acceleration

Multi-feed devices held 45.63% of the digital check scanning solutions market share in 2024 and remain the backbone for branch counters and remittance floors that still process bulky trays. Batch-mode throughput above 100 dpm keeps teller lines short and allows daylight processing windows to shrink, saving overtime expense. Conversely, mobile and smart-device capture posts a 6.43% CAGR, the fastest among all form factors, thanks to app-embedded image optimization and camera optics that rival desktop resolution. Mobile’s rise does not cannibalize multi-feed in corporate settings because SMEs often deploy a mix: a feeder for back-office clean-up and smartphones for ad-hoc field deposits. Single-feed scanners, cheaper and compact, secure niche wins at medical offices and property-management firms that endorse fewer than 100 items weekly.

Heading into 2030, the digital check scanning solutions market size for multi-feed models will still outstrip others, yet its growth lags the mobile subset because remote work trends favor bring-your-own-device paradigms. API-free firmware lets operators connect feeders directly to browser-based apps; this has cut integration time by 60% in recent bank pilots, buoying replacement demand. Meanwhile, smartphone capture benefits from AI routines that straighten skew and detect folded corners in milliseconds, a capability previously limited to hardware ASICs. Together these sub-segments reinforce the sector, illustrating how hardware and software co-evolve rather than displace each other within the digital check scanning solutions market.

By End User: Commercial banks lead while corporate treasury accelerates

Commercial banks commanded 54.32% of the digital check scanning solutions market size in 2024, reflecting continual investments in fraud analytics and Day 2 automation to protect float income. Regulation compels them to maintain image quality sufficient for clearinghouse thresholds, so even declining volumes do not exempt them from refresh cycles roughly every four years. In contrast, corporate and SME treasuries will expand at a 6.31% CAGR through 2030 as AP/AR departments repatriate processing to avoid lockbox surcharges. Treasury managers cite same-day funds availability and ERP reconciliation speed as the pivot points that justify hardware purchases.

Credit unions, while smaller, adopt unified platforms that fold teller, mobile and ATM capture into one image flow; this multiplies efficiencies and elevates deposit cut-off times for members. Government and utility billers, forced by the 2025 federal paper-check sunset, procure high-speed transports with MICR-reject lanes to expedite the migration window. Retail and hospitality merchants integrate scanners at the point-of-sale to sidestep nightly armored cash pickups, keeping labor costs flat despite minimum-wage hikes. Collectively, this mix diversifies the digital check scanning solutions market, shielding revenue against over-exposure to any single vertical.

By Deployment Mode: Cloud acceleration challenges on-premise dominance

On-premise deployments owned 62.24% of the digital check scanning solutions market size in 2024 because incumbents already possessed hardened data centers and preferred deterministic latency for large image files. Nonetheless, cloud-hosted models will clock a 7.34% CAGR through 2030 as SOC 2 and PCI DSS attestations allay data-sovereignty anxiety. Early movers note 30% lower total cost of ownership owing to elastic compute that scales down during weekends when deposit traffic ebbs. Hybrid topologies, where Day 1 capture stays local while Day 2 archival shifts to the cloud, keep sensitive MICR fields behind the firewall yet cut tape-backup expense.

In future RFPs, CFOs elevate opex predictability over outright control, tilting awards toward subscription bundles that fuse scanner leases, hot-swap spares and AI updates. Hardware-as-a-service also compresses refresh cycles to under three years, enlarging the recurring-revenue pool vendors record. As financial watchdogs from Canada to Singapore publish guidance endorsing cloud, conservative banks gradually pivot, narrowing the share gap with on-premise. This reallocation of workloads fuels additional analytics demand, embedding stickiness in the digital check scanning solutions market.

By Application: Branch capture leads while mobile deposit surges

Branch-teller capture accounted for 39.81% of 2024 revenue, affirming that physical locations still anchor many community banks and serve complex transactions such as cashier’s checks and large commercial deposits. High-speed feeder lanes let tellers complete over-the-counter deposits without handing items to back-office clerks, shaving processing times and freeing staff for advisory conversations. Mobile deposit remains the star growth story at 6.13% CAGR, repeating its post-pandemic trajectory as consumers expect 24/7 self-service. Remote desktop capture fills the gap for professional service firms that prefer keyboard entry for invoice codes linked to checks, while lockbox/back-office sites continue to run enterprise transports for wholesale remittance.

Advances in AI algorithms now flag duplicate presentments, forged signatures and altered payee names before images exit the device memory, reducing downstream exceptions. As image-quality thresholds tighten, software modules dynamically instruct smartphone users to retake blurry shots, decreasing false rejects that historically frustrated adoption. Branch devices adopt similar adaptive capture to offset mixed-condition items like crumpled envelopes from night drops. Each application relies on the same developer toolkit, yet optimized UI skins, so financial institutions maintain one codebase, slashing lifetime maintenance. This architectural harmony underpins sustained value in the digital check scanning solutions market even when aggregate item counts decline.

Geography Analysis

North America generated 36.74% of 2024 revenue thanks to two decades of Check 21 compliance, dense branch networks and the 2025 Treasury mandate eliminating federal paper disbursements, which collectively sustain replacement cycles. Mega-banks handle billions in mobile deposits yearly and require horizontally scalable fraud engines that ingest images from multiple channels simultaneously. Canada mirrors those needs as Interac e-Transfer adoption soars yet commercial checks remain embedded in B2B workflows. Mexico’s modernized SPEI platform pressures banks to synchronize image capture with instant credit, nudging institutions toward cloud-ready scanners.

Europe trails in base value but posts mid-single-digit growth as the Instant Payments Regulation compels real-time settlement. Certain markets such as France and Italy still rely on cheques for notarial and property transactions, demanding secure imaging even as retail usage fades. Scandinavian banks, nearly check-free, procure niche devices for cross-border trade instruments, illustrating how regulatory heterogeneity preserves pockets of demand. Pan-regional SEPA reachability requirements push banks to consolidate image archives for audit, injecting fresh software revenue into the digital check scanning solutions market.

Asia-Pacific offers the fastest runway with a 6.87% CAGR because banks leapfrog legacy capture straight into mobile and cloud. Japan’s megabanks overhaul branch platforms to support all-digital passbooks yet retain image feeds for municipal payments still paid by check. In India and Indonesia, neobanks bundle mobile capture to court SMEs that skipped branch banking altogether, proving the scalability of subscription scanners. China, though leaning on QR codes, keeps corporate cheque volumes substantial in state-owned-enterprise commerce, safeguarding demand for high-feed transports. Across ASEAN, regulatory sandboxes accelerate approvals for AI-driven fraud detection, shortening sales cycles for vendors equipped with pre-certified models. These cross-currents collectively reinforce a geographically balanced growth profile in the digital check scanning solutions market.

Competitive Landscape

Competition is moderate: top hardware producers Digital Check, Panini and Canon enjoy volume economies, while software-first firms Mitek and Alogent monetize AI layers atop generic OEM devices. Digital Check’s cumulative 1.5 million scanners shipped underscores manufacturing reach and post-warranty parts availability that smaller rivals find difficult to match. Panini differentiates with EverneXt’s open firmware that accepts driverless USB connections, appealing to cost-sensitive IT teams. Canon leverages optical heritage to offer configurable lighting that reduces MICR misreads in poorly printed items.

Software houses exploit cloud to out-iterate hardware cycles. Mitek appears in 99% of U.S. banks for mobile capture, giving it anonymized sample sets to train deepfake detection-an advantage that widens barriers to entry. Alogent links teller, ATM, mobile and RDC into one orchestration layer, pitching Day 2 consolidations that can reclaim two FTEs per mid-size institution. Joint ventures signal convergence: Avivatech combines Digital Check’s engineering with Benchmark Technology’s branch-automation stack, bundling scanners, cash recyclers and software under one SKU. Meanwhile, niche players target specialty workflows such as law-firm trust accounts or casino cage deposits, proving white-space still exists.

Pricing remains rational; list discounts hover near 15% for major banks but stay firmer for credit-unions purchasing through resellers. Intellectual-property moats around image-enhancement ASICs, MICR read-heads and patented endorsement printers limit knock-off threats. Yet the real contest migrates to SaaS layers where continuous model refresh sustains annuity revenue. Players who knit identity verification, liveness detection and voice biometrics into deposit rails stand to capture premium margins. Those dynamics, plus vendor consolidation, shape the next phase of the digital check scanning solutions market.

Digital Check Scanning Solutions Industry Leaders

Digital Check Corp.

Panini S.p.A.

Canon Inc.

Epson (Seiko Epson Corporation)

ARCA S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Digital Check and Benchmark Technology Group launched Avivatech to bundle cash and check automation under one integrated platform.

- March 2025: U.S. Treasury activated Executive Orders 14247 and 14249, confirming the phase-out of paper benefits checks by Sept 30, 2025.

- February 2025: Alogent released Alogent Shield, an AI fraud-mitigation suite drawing on cloud-based consortium data for real-time risk scoring.

- February 2025: Royal Credit Union implemented Alogent Unify, merging Day 1 and Day 2 processing workflows into a single platform,

Global Digital Check Scanning Solutions Market Report Scope

| Single-Feed Scanners |

| Multi-Feed Scanners |

| Teller/TTP Capture Scanners |

| Mobile/Smart-Device Scanners |

| Commercial Banks |

| Credit Unions and Co-ops |

| Retail and Hospitality Merchants |

| Corporate / SME Treasury |

| Government and Utilities |

| On-Premise |

| Cloud-Hosted |

| Hybrid |

| Branch/Teller Image Capture |

| Remote Deposit Capture (Desktop) |

| Mobile Deposit (Consumer and SMB) |

| Back-Office / Lockbox Processing |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Scanner Type | Single-Feed Scanners | ||

| Multi-Feed Scanners | |||

| Teller/TTP Capture Scanners | |||

| Mobile/Smart-Device Scanners | |||

| By End User | Commercial Banks | ||

| Credit Unions and Co-ops | |||

| Retail and Hospitality Merchants | |||

| Corporate / SME Treasury | |||

| Government and Utilities | |||

| By Deployment Mode | On-Premise | ||

| Cloud-Hosted | |||

| Hybrid | |||

| By Application | Branch/Teller Image Capture | ||

| Remote Deposit Capture (Desktop) | |||

| Mobile Deposit (Consumer and SMB) | |||

| Back-Office / Lockbox Processing | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the digital check scanning solutions market in 2025?

The market is valued at USD 1.07 billion in 2025 and is set to rise to USD 1.43 billion by 2030.

Which scanner type dominates current deployments?

Multi-feed scanners hold 45.63% of global share, serving high-volume branch and remittance environments.

Why are cloud-hosted deployments gaining popularity?

SOC 2 certifications and subscription pricing cut total cost of ownership by about 30%, encouraging banks to shift workloads off-premise.

What regulatory change is most influential for 2025?

U.S. Executive Orders 14247/14249 mandate elimination of federal paper checks by September 2025, driving urgent upgrades.

Which region offers the fastest growth through 2030?

Asia-Pacific is projected to expand at 6.87% CAGR as banks modernize and mobile capture adoption surges.

How are vendors addressing fraud risk?

Providers embed AI suites such as Alogent Shield and Mitek Digital Fraud Defender to detect duplicates, forgeries and deepfakes in real time.

Page last updated on: