Background Check Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

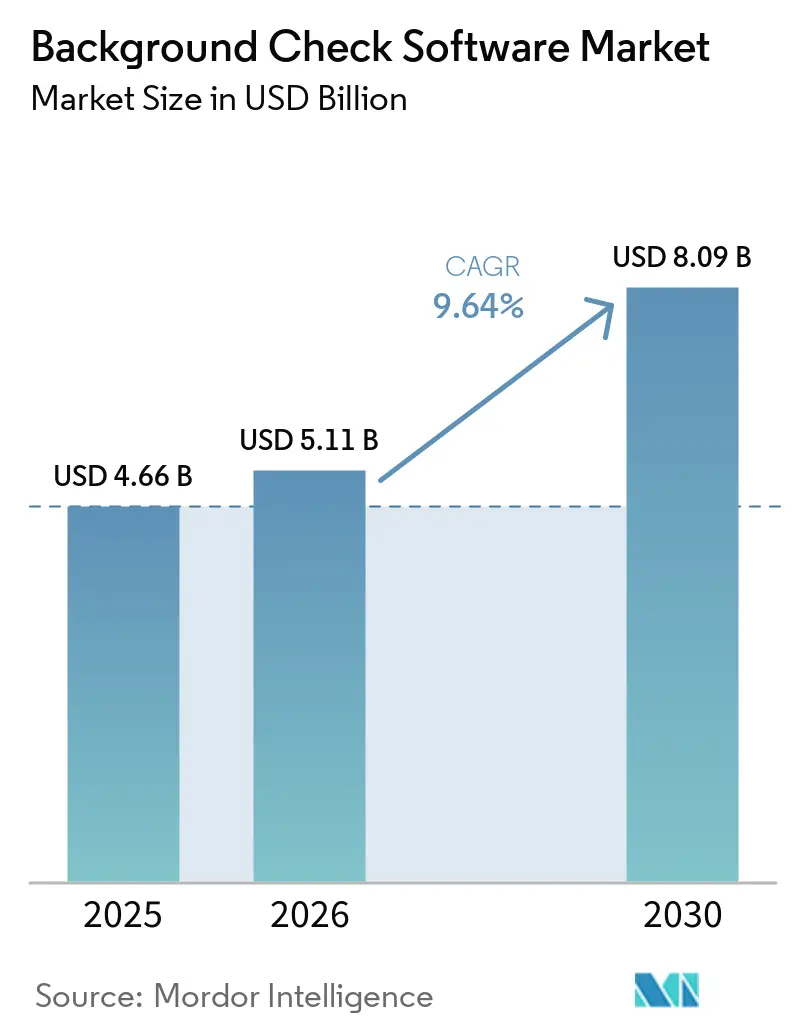

| Market Size (2026) | USD 5.11 Billion |

| Market Size (2030) | USD 8.09 Billion |

| Growth Rate (2026 - 2031) | 9.64% CAGR |

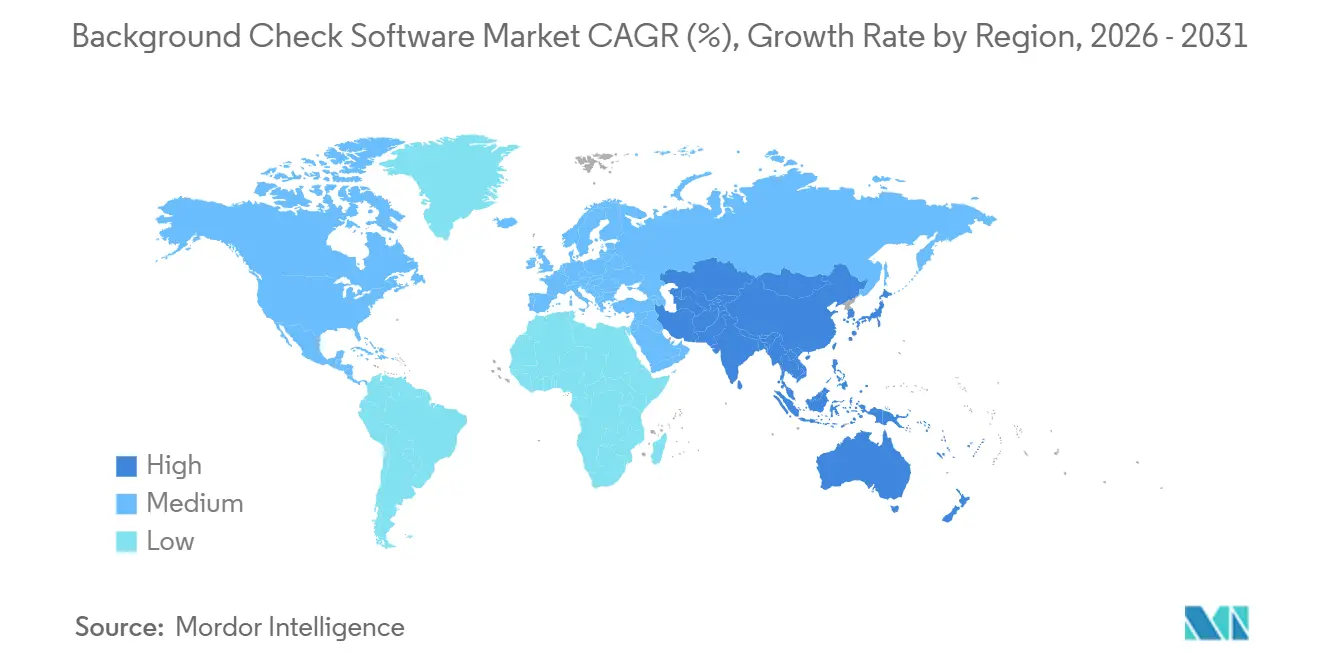

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Background Check Software Market Analysis by Mordor Intelligence

The background check software market size is expected to grow from USD 4.66 billion in 2025 to USD 5.11 billion in 2026 and is forecast to reach USD 8.09 billion by 2031 at 9.64% CAGR over 2026-2031. Distributed hiring after the pandemic has transformed pre-employment screening into a business-critical workflow, while the October 2024 CFPB circular expanded the addressable pool of candidates by classifying gig-platform contractors as Fair Credit Reporting Act (FCRA)-covered workers. Intensifying global privacy enforcement raised vendor compliance costs but simultaneously elevated screening accuracy and data-security requirements, which favor well-capitalized platforms. Investments in explainable artificial intelligence, purpose-built data centers, and low-latency application-programming interfaces (APIs) have become central competitive differentiators as employers demand real-time decisions. At the same time, moderate market consolidation, exemplified by First Advantage’s purchase of Sterling Check, has not eliminated fragmentation, leaving space for niche providers.

Key Report Takeaways

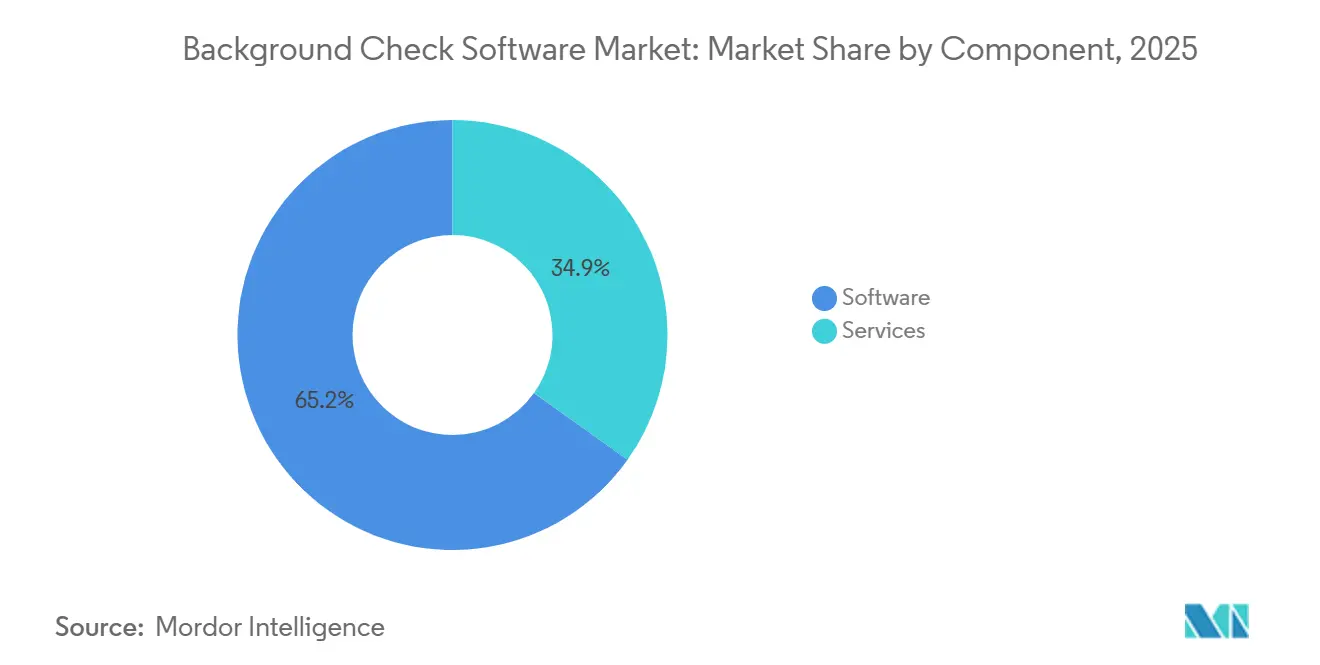

- By component, software accounted for 65.15% of 2025 revenue while services are advancing at a 10.40% CAGR through 2031.

- By check type, employment and pre-hire screening led with 36.45% of the background check software market share in 2025, whereas watch-list and adverse-media scans are projected to climb at a 12.25% CAGR to 2031.

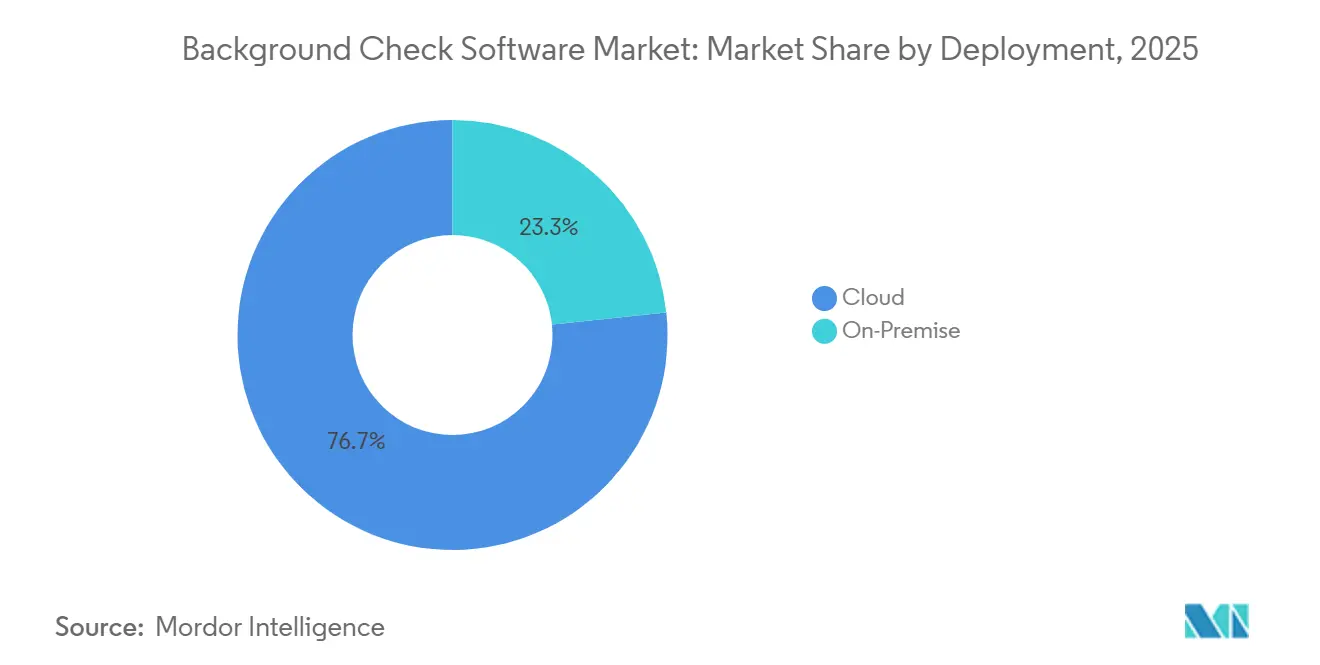

- By deployment, cloud solutions captured 76.67% of 2025 revenue and are expanding at an 11.70% CAGR, whereas on-premise implementations are trending lower.

- By organization size, large enterprises held 58.75% revenue share in 2025, but small and medium enterprises are forecast to post a 10.90% CAGR between 2026-2031.

- By end-use industry, information technology and telecommunications commanded 26.56% of 2025 revenue, while healthcare and life-sciences represent the fastest trajectory at an 11.50% CAGR through 2031.

- By geography, North America contributed 41.50% revenue share during 2025, and Asia-Pacific is pacing the field at a 12.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Background Check Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Gig‑Economy and Remote Hiring Demand | +2.1% | Global, with concentration in North America and Asia‑Pacific | Medium term (2–4 years) |

| Increasing Regulatory Mandates (FCRA, GDPR) | +1.8% | North America and Europe, with spillover into Asia‑Pacific | Short term (≤ 2 years) |

| Cyber‑Security Worries Driving ID Verification Tie‑Ins | +1.5% | Global, led by BFSI and government sectors | Medium term (2–4 years) |

| HR‑Tech Consolidation Pushing Embedded Screening APIs | +1.3% | North America and Europe | Short term (≤ 2 years) |

| AI‑Powered Adverse‑Media Scans Cutting Turnaround Time | +1.2% | Global, with early adoption in BFSI and healthcare | Long term (≥ 4 years) |

| Blockchain‑Based Credential Wallets Gaining Traction | +0.9% | Asia‑Pacific core, with pilot programs in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Gig-Economy and Remote Hiring Demand

Platform employers processed more than 68 million screens in the United States during 2025, up 34% from two years earlier, after FCRA obligations were extended to ride-hailing and delivery contractors.[1]Consumer Financial Protection Bureau, “Circular on Fair Credit Reporting Act Obligations for Gig-Platform Operators,” CFPB.gov Integrated APIs now connect screening engines to onboarding portals so power-users can cut time-to-hire from roughly two weeks to fewer than 48 hours. Multijurisdictional compliance logic embedded in modern products automatically applies local ban-the-box and privacy rules, easing the operational burden on lean human-resources teams. Adoption is spreading fastest among software-as-a-service start-ups that hire fully remote staff across several states. These trends enlarge the background check software market by pulling in non-traditional worker categories and by raising the frequency of rescreens as contractors flow in and out of projects.

Increasing Regulatory Mandates (FCRA, GDPR)

The U.S. Federal Trade Commission issued 23 consent decrees for FCRA non-compliance during 2025, doubling the prior biennium and raising average settlement values to nearly USD 5 million.[2]Federal Trade Commission, “FCRA Consent Decrees 2024-2025,” FTC.gov In Europe, Article 22 of the General Data Protection Regulation compels human review of automated decisions, compelling vendors to insert explainability layers that add one business day but reduce error rates. The U.K. Information Commissioner’s January 2025 guidance now requires explicit candidate consent for most criminal-records processing. Compliance outlays have reached 8-11% of mid-tier vendor revenue yet simultaneously create scale advantages for well-funded providers able to spread audit costs across large client bases. These pressures are likely to keep raising adoption of platforms that package legal templates, audit trails, and jurisdiction-aware workflows out of the box.

Cyber-Security Worries Driving ID Verification Tie-Ins

Identity-theft complaints registered with the U.S. Federal Trade Commission passed 1.1 million in 2024, prompting employers, in particular financial institutions, to require biometric liveness checks in addition to Social Security number matching. Partnerships with specialists such as Onfido and Jumio allow background-screening vendors to layer document-authentication and selfie-verification steps that meet the June 2025 NIST Digital Identity Guidelines.[3]National Institute of Standards and Technology, “Digital Identity Guidelines Update,” NIST.gov Early adopters report 30-40% reductions in impersonation-driven fraud. The same APIs also enable post-hire continuous monitoring that re-validates identity when employees access sensitive systems. Heightened threat awareness is therefore expanding spend per transaction and widening the functional footprint of the background check software market.

HR-Tech Consolidation Pushing Embedded Screening APIs

Applicant-tracking-system vendors concluded 17 mergers and acquisitions across 2024-2025, bundling recruiting, payroll, and onboarding into unified suites. Workday alone doubled its roster of pre-integrated screeners to 14 by mid-2025. Employers are migrating toward providers that return candidate status calls in under 200 milliseconds so recruiters never leave the native interface. Continuous monitoring, delivered through the same real-time API, can command 30-40% price premiums. As suites swallow once-stand-alone modules, vendors offering ultra-low-latency, developer-friendly endpoints enjoy a tangible growth tailwind.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Data‑Privacy Laws Limiting Data Sharing | -1.4% | Europe and Asia‑Pacific, with emerging impact in South America | Short term (≤ 2 years) |

| High Solution Cost for SMEs in Emerging Markets | -1.1% | Asia‑Pacific, Middle East, Africa, South America | Medium term (2–4 years) |

| Litigation Risk from Biased AI Algorithms | -0.8% | North America, with spillover to Europe | Medium term (2–4 years) |

| Fragmented Global Criminal‑Record Databases | -0.7% | Global, most acute in Asia‑Pacific and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Data-Privacy Laws Limiting Data Sharing

India’s Digital Personal Data Protection Act bars cross-border transfer of criminal-record data without consent and regulator sign-off, forcing multinational vendors to add regional data centers and local partnerships. China’s Personal Information Protection Law demands candidate opt-outs for automated profiling, effectively banning opaque AI scoring models. Similar frameworks in Brazil and South Korea threaten fines ranging from 2% of annual revenue to USD 50 million per infraction. These decentralized regimes fragment data-flows, inflate engineering overhead, and restrict the universal API vision many global clients expect, thereby slowing the attainable growth rate of the background check software market.

High Solution Cost for SMEs in Emerging Markets

Enterprise-grade packages priced at USD 25-75 per screen in developed economies equate to USD 60-180 when indexed to purchasing-power-parity wages in parts of Southeast Asia and Sub-Saharan Africa. In markets where 35-40% of firms lack corporate credit cards, invoice-based billing stretches cash cycles and inflates vendor working-capital needs. Local competitors in India now sell manual courthouse checks for USD 5-10, undercutting multinational SaaS providers that rely on higher automation. Price elasticity therefore narrows the accessible funnel of small and medium customers and restrains revenue realization in the fastest population-growth regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Scale as Monitoring Becomes Routine

Services are poised for a 10.40% CAGR through 2031, closing the gap with software’s 65.15% revenue base in 2025. Enterprise buyers lean on managed offerings when navigating adverse-action notices, multi-country privacy rules, and quarterly criminal rescreens. Hybrid bundles that combine natural-language-processing algorithms with analyst validations blur the old boundary between bits and bodies, but they also lift average selling prices. Among gig-economy platforms that require sub-one-minute decisions, however, high-throughput APIs maintain a software lead. The widening menu supports upsell paths that enlarge the background check software market while giving vendors recurring subscription visibility. In monetization terms, enhanced services lift gross profit even as margins stay below pure software because analyst capacity can be flexed to meet seasonality.

Ongoing automation does not spell the end of human intervention. Complex disputes, international checks, and professional-license verifications still require manual research, which entrenches the services line. Vendors that orchestrate task routing between machine learning and case managers achieve the shortest turnaround benchmarks. Such orchestration is emerging as a brand differentiator just as real-time monitoring converts what once was a pre-hire cost center into a career-long compliance layer.

By Check Type: Watch-List Scans Overtake Legacy Packages

Employment and pre-hire packages held 36.45% revenue share in 2025, but the fastest lane is global watch-list and adverse-media scans projected at a 12.25% CAGR thanks to updated anti-money laundering (AML) rules. Financial institutions now require real-time sanction vetting for every contractor, magnifying demand for daily refreshes of politically exposed persons (PEP) data. At the same time, credit reports face a shrinking niche after 11 U.S. states limited or banned their use.

Criminal-history searches remain large but are hampered when county courts lack digital record feeds, so turnaround can stretch to one week. Identity-verification layers such as biometric liveness checks are now table stakes. Education and license attestations are benefiting from blockchain projects where issuers place tamper-proof credentials on distributed ledgers, cutting verification cycles from days to minutes. The cumulative effect reallocates budget toward content that updates continuously, nudging the background check software market toward subscription economics.

By Deployment: Cloud First, Hybrid Second, On-Premise Last

Cloud captured 76.67% revenue share during 2025 and is rising at an 11.70% CAGR as subscription pricing eliminates capital expenditure and slashes implementation lead times. Multi-tenant architecture allows vendors to amortize infrastructure across thousands of tenants, producing per-check prices under USD 15 for basic criminal searches. Data-residency laws prompted regional builds in Frankfurt, Singapore, and São Paulo, ensuring compliance with GDPR, India’s DPDP Act, and Brazil’s LGPD. Government and defense agencies still mandate classified data remain on-premise, but even those clients now pilot FedRAMP-authorized clouds for lower-sensitivity workloads. Hybrid deployment is, therefore, the compromise model gaining traction, where fingerprints reside on agency hardware and education verifications run in the cloud. This shift makes elastic computing a lever for every vendor to protect margins as query volumes soar.

On-premise solutions, by contrast, demand dedicated servers and 24-month upgrade cycles, limiting functional parity and placing them on a slow glide path to de-emphasis. Customers that once favored on-premise because of control are increasingly convinced by cloud providers’ stronger security certifications and single-tenant enclaves. Taken together, the superiority of pay-per-use economics cements cloud as the default that will continue to expand the background check software market size for the rest of the decade.

By Organization Size: SMEs Close the Feature Gap

Large enterprises controlled 58.75% of 2025 revenue, but SME uptake is rising at 10.90% CAGR. Three forces drive the shift: modular SaaS plans priced under USD 100 per month, self-serve dashboards that mimic consumer e-commerce usability, and API libraries that connect to payroll or onboarding apps with only a few lines of code. Remote hiring renders startup compliance loads comparable to those of multinationals, since a five-person company might employ staff in three countries. Vendors respond with role-based templates that auto-populate permissible content according to location, removing the policy-writing burden from small HR teams. The result enlarges the overall background check software market by activating a long tail of small buyers once priced out of professional screening.

Large enterprises still negotiate bespoke service-level agreements, discounted volume tiers, and global continuous-monitoring bundles, ensuring they remain the biggest revenue stack. However, as SMEs turn from paper-based reference calls to digital screens, the combined long-tail spending rivals traditional accounts, persuading vendors to double down on self-serve interfaces and community support forums.

By End-Use Industry: Healthcare Emerges as the Growth Engine

Information technology and telecommunications retained a 26.56% revenue grip in 2025 thanks to high freelancer churn and heightened cyber-security mandates. Yet healthcare and life-sciences are on track for an 11.50% CAGR through 2031 amid sharper enforcement of clinician-license validation and a looming physician shortfall. Hospitals now budget for quarterly sanction checks on existing staff, not just new hires, which multiplies transaction counts per employee. Banks and insurers remain evergreen users, compelled by FINRA Rule 3110 and Know-Your-Customer obligations to scrutinize both frontline staff and external consultants. Government and public-sector agencies have revived continuous-vetting pilots to shrink backlogs that exceeded 200,000 cases in 2025. Manufacturing, retail, and education fill out the backdrop with more episodic but still material demand, especially where supply-chain security or child-safety laws apply.

Healthcare’s outsized appetite for credentialing solutions that integrate primary-source verification, immunization status, and sanctions monitoring elevates its share of incremental revenue. Given that turnover among allied health professionals is running in the mid-teens percentage, each re-verification cycle adds steady volume to the background check software market.

Geography Analysis

North America contributed 41.50% of background check software market revenue in 2025, supported by FCRA litigation settlements that totaled USD 1.2 billion in 2024-2025. Vendors invest in dispute-resolution portals and consumer notice workflows to reduce class-action exposure. Canada’s proposed Bill C-27 would mandate algorithmic-impact assessments, forcing transparency into model weights and training data. Mexico’s 2025 outsourcing reform reclassified large segments of contract labor, swelling the screening universe and driving double-digit transaction growth. Looking forward, a forthcoming U.S. Federal Trade Commission commercial-surveillance rule could curtail third-party data-broker feeds, pressuring platforms that rely heavily on external data sources.

Asia-Pacific is the highest-velocity region, forecast to expand at a 12.85% CAGR through 2031. India’s Digital Personal Data Protection Act obliges explicit consent for cross-border data transfers and pushed leading vendors to erect in-country data centers. China’s Personal Information Protection Law forces the replacement of opaque scoring with explainable AI, compelling code refactoring but also opening a premium tier for transparency. Japan’s 2024 amendment to its Act on the Protection of Personal Information created an adequacy list that simplifies data flows from the United States and Europe, accelerating multinational rollouts. Indonesia and Vietnam, deeply mobile-first, rely on selfie and near-field-communication ID capture because broadband desktops remain rare outside urban cores.

Europe occupies a middle position where strict GDPR Article 22 clauses enlarge human-review overhead, lengthening turnaround yet increasing accuracy. The United Kingdom may diverge from some GDPR consent mechanics post-Brexit, creating dual frameworks. Germany’s works-council approval requirement for programs covering beyond 20% of staff represents a structural adoption barrier. Meanwhile, the Middle East and Africa witness early adoption tied to national digital-identity systems such as the Emirates ID revamp, which can slash verification times to minutes. South Africa’s Protection of Personal Information Act still leaves the continent fragmented, but multinationals upgrade policies there to global standards, setting a beachhead for wider African expansion.

Competitive Landscape

The five largest vendors together controlled roughly 38% of background check software market revenue in 2025, a share that signals moderate concentration with plentiful room for challengers. First Advantage’s USD 2.8 billion acquisition of Sterling Check created a 40,000-client giant yet introduced integration complexity around harmonizing technology stacks and overlapping sales teams. HireRight, Checkr, and Accurate Background maintain share through expansive global coverage and proprietary databases that slash courthouse dependency. Growth-stage players such as Certn and Onfido compete on AI-driven identity verification, adversarial-attack detection, and blockchain credential wallets.

Technology arms-races now focus on natural-language models capable of parsing thousands of media sources and surfacing context-rich risk flags in seconds. Checkr’s 2025 patent filing for continuous identity verification using biometric liveness detection aims to transition screening from a point-in-time event to an always-on service. Continuous monitoring remains an underpenetrated opportunity, covering fewer than 12% of U.S. employees. Vendors that roll out subscription plans at sub-USD 10 per worker per month are courting mid-market customers that historically rejected re-screening as too costly. Legal risk from biased models looms large, highlighted by a March 2025 California class action that alleged disproportionate flagging of minority candidates, prompting Equal Employment Opportunity Commission scrutiny; vendors are now releasing fairness dashboards as a defensive feature.

Regional expansion remains an equally fierce battleground. Multinationals build or rent data centers in India, Brazil, and the European Union to meet residency rules, while local entrants leverage field networks to capture county-level court records unavailable online. Partnerships with applicant-tracking-system ecosystems, especially Workday, SuccessFactors, and Greenhouse, channel new customer inflows; placement on a top marketplace can shift hundreds of enterprise accounts per year. Finally, midsize consolidators continue to shop for niche add-ons, particularly healthcare-credentialing specialists, to round out vertical modules and push the background check software industry toward scale without yet tipping into oligopoly.

Background Check Software Industry Leaders

First Advantage Corporation

HireRight Holdings Corporation

Asurint, LLC

Accurate Background, LLC

Checkr, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Checkr announces a strategic partnership with SAP SuccessFactors to embed real-time background screening inside the talent-acquisition module for more than 8,000 enterprise clients, and the integration is expected to process 2 million checks annually.

- March 2026: HireRight completes the USD 180 million purchase of a European identity-verification specialist, adding biometric-liveness technology and 1,200 new enterprise customers across Germany, France, and the United Kingdom.

- March 2026: PeopleCheck receives commendation from the Australian Privacy Commissioner for privacy-by-design features that automatically delete candidate data 90 days after hiring in line with Australia’s Privacy Act 1988.

- February 2026: HireRight integrated with Workday, embedding real-time screening inside the Workday human-capital-management suite.

Global Background Check Software Market Report Scope

The Background Check Software Market pertains to the industry segment offering digital solutions that streamline, automate, and enhance the process of verifying the credentials, history, and trustworthiness of individuals and organizations. This market includes software platforms that facilitate employment screening, criminal record checks, identity verification, credit history analysis, and compliance monitoring. The increasing adoption of Background Screening solutions across recruitment, financial verification, and regulatory compliance processes is supporting sustained market growth. These solutions serve businesses across sectors such as human resources, financial services, healthcare, and government.

The Background Check Software Market Report is Segmented by Component (Software, and Services), Check Type (Employment/Pre-Hire Screening, Criminal History Check, Identity and SSN Verification, Credit and Financial History, Education and License Verification, Global Watch-List and Adverse-Media Scan, and Other Check Types), Deployment (Cloud, and On-Premise), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-Use Industry (IT and Telecommunication, BFSI, Healthcare and Life-Sciences, Government and Public Sector, Manufacturing, Retail and E-Commerce, Education, and Other End-Use Industries), and Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Employment / Pre-Hire Screening |

| Criminal History Check |

| Identity and SSN Verification |

| Credit and Financial History |

| Education and License Verification |

| Global Watch-List and Adverse-Media Scan |

| Other Check Types |

| Cloud |

| On-Premise |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| IT and Telecommunication |

| BFSI |

| Healthcare and Life-Sciences |

| Government and Public Sector |

| Manufacturing |

| Retail and E-Commerce |

| Education |

| Other End-Use Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Check Type | Employment / Pre-Hire Screening | |

| Criminal History Check | ||

| Identity and SSN Verification | ||

| Credit and Financial History | ||

| Education and License Verification | ||

| Global Watch-List and Adverse-Media Scan | ||

| Other Check Types | ||

| By Deployment | Cloud | |

| On-Premise | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By End-Use Industry | IT and Telecommunication | |

| BFSI | ||

| Healthcare and Life-Sciences | ||

| Government and Public Sector | ||

| Manufacturing | ||

| Retail and E-Commerce | ||

| Education | ||

| Other End-Use Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the background check software market in 2031?

The background check software market is forecast to reach USD 8.09 billion by 2031, growing at a 9.64% CAGR during 2026-2031.

Which deployment model is growing fastest?

Cloud deployments are expanding at an 11.70% CAGR (2026-2031) as multi-tenant SaaS models significantly reduce upfront costs.

Which check type will see the highest growth?

Global watch-list and adverse-media scans are expected to grow at a 12.25% CAGR, driven by stricter AML regulations requiring real-time sanctions screening.

Why is Asia-Pacific considered the most attractive region?

Asia-Pacific is projected to register a 12.85% CAGR through 2031, supported by India's DPDP Act, China's PIPL, and rapid gig-economy expansion.

How concentrated is vendor competition?

The top five vendors account for ~38% of total revenue, indicating a moderately concentrated yet competitive market landscape.

Which end-use industry is poised for the fastest adoption?

Healthcare and life sciences are expected to grow at an 11.50% CAGR through 2031, driven by tighter credentialing and frequent license verification requirements.

Page last updated on: