Printed Circuit Board Inspection Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

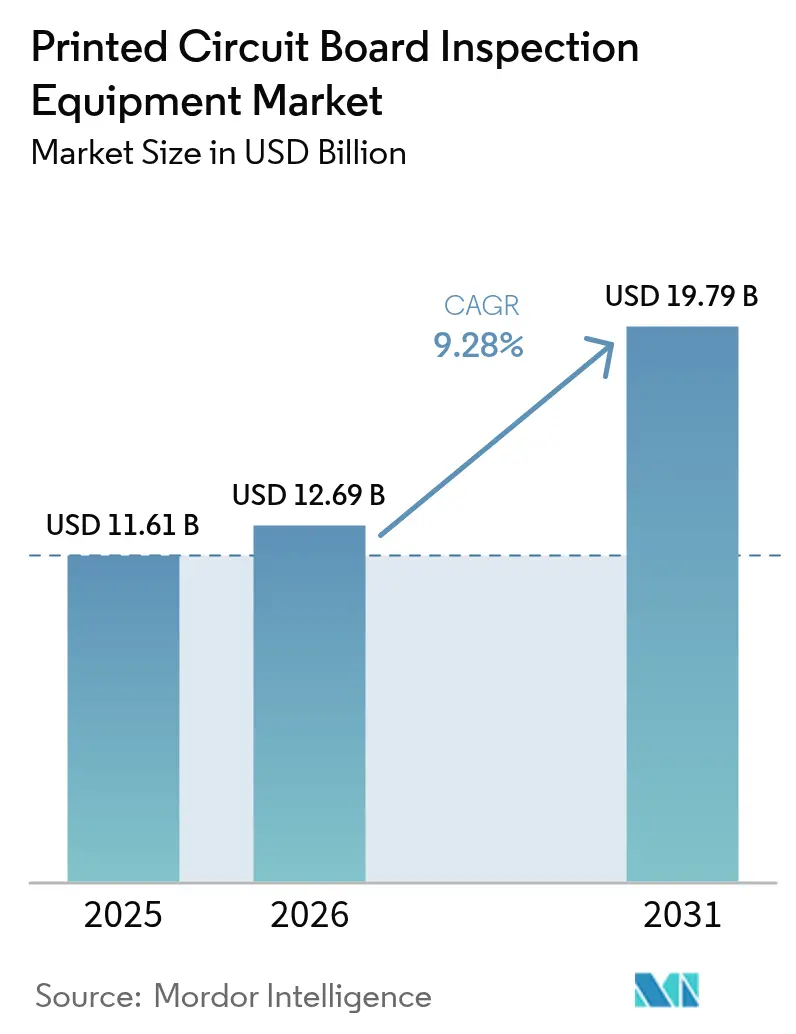

| Market Size (2026) | USD 12.69 Billion |

| Market Size (2031) | USD 19.79 Billion |

| Growth Rate (2026 - 2031) | 9.28% CAGR |

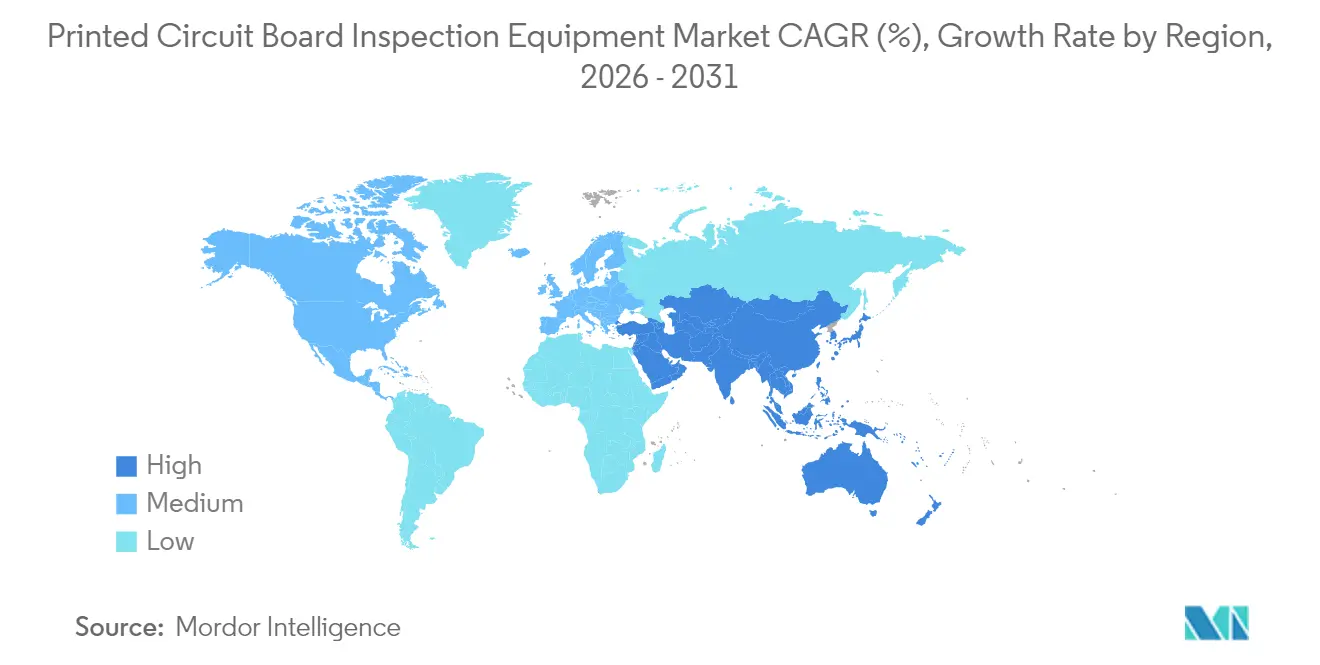

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Printed Circuit Board Inspection Equipment Market Analysis by Mordor Intelligence

printed circuit board inspection equipment market size in 2026 is estimated at USD 12.69 billion, growing from 2025 value of USD 11.61 billion with 2031 projections showing USD 19.79 billion, growing at 9.28% CAGR over 2026-2031. Rapid miniaturization, zero-defect mandates in automotive and medical electronics, and sub-micron tolerance requirements in advanced packaging are reshaping investment priorities. Inline automatic optical inspection (AOI) platforms dominate current demand, yet 3D AOI and 3D X-ray systems are accelerating because volumetric imaging, coplanarity measurement, and micro-void detection are now essential for high-density interconnect and chiplet substrates. Electronics manufacturers are also shifting toward pay-per-inspection service models that align equipment costs with throughput, while artificial-intelligence-enabled defect classification reduces false calls and lifts effective capacity. Asia-Pacific leads revenue generation, and automotive electronics is the quickest-expanding end-user segment as electric vehicles (EVs) add USD 1,500-2,000 of electronic content per unit.

Key Report Takeaways

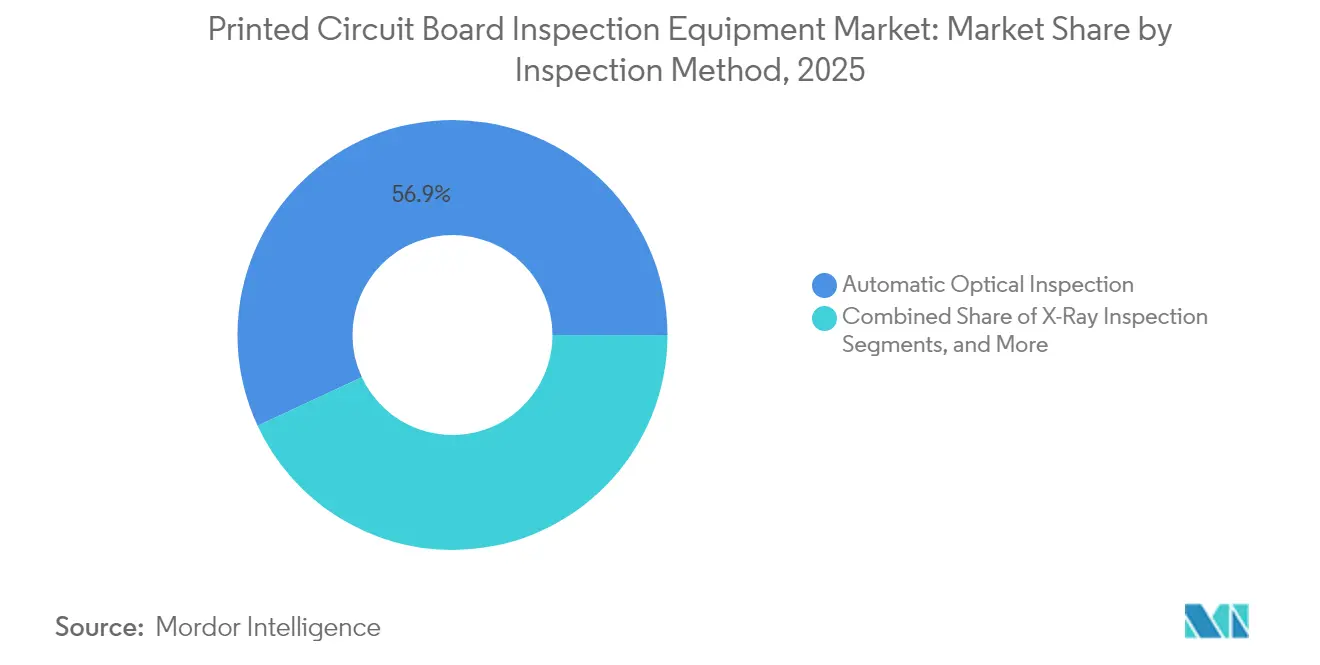

- By inspection method, automatic optical inspection held 56.93% of 2025 revenue; X-ray inspection is poised for the fastest growth with an 10.74% CAGR through 2031.

- By system type, inline platforms led with 60.72% share in 2025, while their own segment also records the highest forecast CAGR at 11.68% to 2031.

- By technology, 2D AOI accounted for 48.02% of 2025 sales; 3D AOI is the quickest-growing technology with a 10.03% CAGR to 2031.

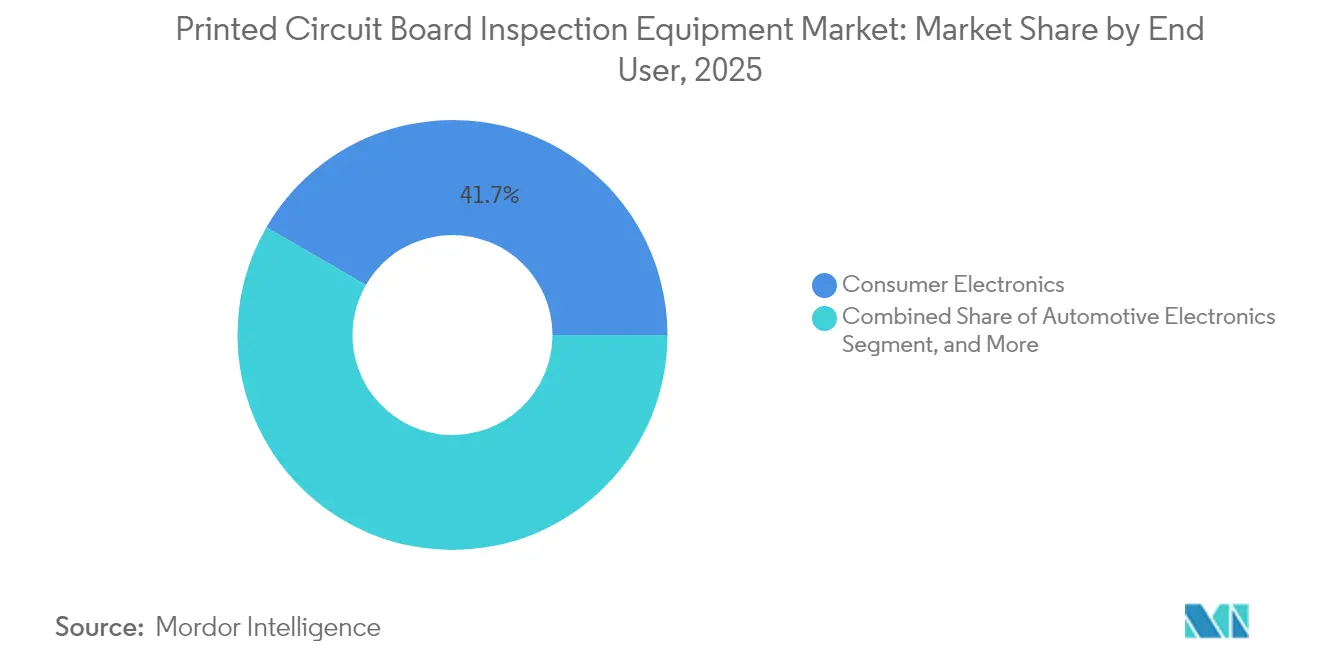

- By end user, consumer electronics contributed 41.65% of demand in 2025; automotive electronics is rising most rapidly at a 9.72% CAGR through 2031.

- By PCB type, rigid boards captured 51.74% of value in 2025; high-density interconnect boards are expanding at a 10.24% CAGR to 2031.

- By geography, Asia-Pacific generated 37.88% of global revenue in 2025 and is advancing at an 11.12% CAGR, the fastest regional pace to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Printed Circuit Board Inspection Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Miniaturization and Higher Component Densities in Electronics | +2.10% | Global, with APAC core and spill-over to North America | Medium term (2-4 years) |

| Rising Adoption of Industry 4.0 Smart Manufacturing Lines | +1.80% | Global, early gains in Germany, Japan, South Korea | Short term (≤ 2 years) |

| Growth in Automotive Electronics and Electric Vehicles | +2.30% | North America, Europe, APAC automotive hubs | Long term (≥ 4 years) |

| Deployment of Advanced AI-Enabled Defect Classification Reducing False Calls | +1.60% | Global, with early adoption in Taiwan, China, United States | Short term (≤ 2 years) |

| Pay-Per-Inspection and Equipment-as-a-Service Business Models Lowering CapEx Barriers | +1.20% | Global, strongest uptake in North America and Europe | Medium term (2-4 years) |

| Demand for Sub-Micron 3D Inspection in Advanced Packaging and Chiplet PCBs | +1.50% | APAC core (Taiwan, South Korea), spill-over to United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Miniaturization and Higher Component Densities in Electronics

Component pitch in smartphones has already tightened to 0.3 mm, forcing manufacturers to retire manual visual checks in favour of AOI systems able to resolve features below 20 µm. Microvias between 50 µm and 150 µm, blind or buried via stacks, and copper pillars beneath redistribution layers are invisible to 2D grayscale imaging.

Taiwan’s Industrial Technology Research Institute demonstrated a deep-UV 20 nm-resolution prototype in 2024 that identifies micro-cracks in chiplet substrates.[1]Industrial Technology Research Institute, “20-Nanometer Resolution AOI Prototype,” itri.org.tw As a single defect on a USD 5,000 data-center GPU substrate now drives scrap cost, inline 3D inspection at 15 s per board is economically justified.

Growth in Automotive Electronics and Electric Vehicles

Global EV output climbed to 14 million units in 2024 and is expected to surpass 40 million units by 2030. Each EV integrates power modules, battery-management boards, and driver-assistance controllers that collectively triple PCB content versus internal-combustion vehicles.

Tier-1 suppliers have moved to 100% inline X-ray inspection to meet IATF 16949 reliability standards, while ISO 26262 mandates electronic traceability of inspection results for safety-related assemblies.[2]International Organization for Standardization, “ISO 26262: Road Vehicles – Functional Safety,” iso.org Increased inspection intensity lifts demand for both 3D AOI and 3D computed tomography (CT) platforms.

Rising Adoption of Industry 4.0 Smart Manufacturing Lines

Closed-loop feedback systems are transforming electronics manufacturing by tightly integrating solder-paste inspection (SPI), automated optical inspection (AOI), and reflow ovens into a single data-driven workflow. In these next-generation lines, OPC UA serves as the common communication layer, allowing machines from different vendors to exchange defect locations, process parameters, and quality metrics within a few hundred milliseconds. This rapid, standardized data flow enables inspection stations to act immediately on what they detect sending precise coordinate-level feedback to printers or placement machines so they can adjust pressure, alignment, or stencil parameters before small deviations turn into systemic defects.

A 2024 Fraunhofer case study illustrates the impact: automotive manufacturers using real-time SPI-to-printer feedback saw a 42% reduction in solder-related defects and achieved changeovers 30% faster because operator interventions were replaced by automated parameter tuning. Instead of inspection equipment functioning solely as a pass/fail checkpoint, it becomes an active process optimizer that continuously corrects upstream variations.

Deployment of Advanced AI-Enabled Defect Classification Reducing False Calls

Convolutional neural networks (CNNs) are reshaping automated inspection by learning visual patterns directly from large, diverse (“ensemble”) image sets rather than relying on manually tuned rules. By training on varied examples of each defect type different board designs, lighting conditions, solder volumes, and pad geometries these models generalize far better than traditional rule-based vision systems. In practice, they are reaching classification accuracies around 95% and reducing false calls by as much as 40%, a shift that meaningfully improves both quality and line efficiency.

Toolkits such as NVIDIA’s TAO Toolkit make this approach more accessible to manufacturing teams. With transfer learning and pre-trained base models, plants can fine-tune an inspector-specific network using relatively small datasets on the order of a few hundred images per defect class rather than collecting tens of thousands from scratch. This drastically shortens the deployment cycle: what once required months of data curation, labeling, and model engineering can now be completed in weeks, often without deep in-house AI expertise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Investments for Advanced AOI and AXI Systems | -1.40% | Global, acute in emerging markets and small-to-medium enterprises | Short term (≤ 2 years) |

| Shortage of Skilled Technicians for System Programming and Maintenance | -0.90% | Global, most severe in North America and Europe | Medium term (2-4 years) |

| Rapid Technology Obsolescence Leading to Compressed ROI Cycles | -0.70% | Global, particularly impacting early adopters | Medium term (2-4 years) |

| Radiation Safety Compliance Costs for High-Power X-Ray Inspection Lines | -0.50% | Global, stringent in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Investments for Advanced AOI And AXI System

Prices for a laser-triangulation 3D AOI platform range from USD 150,000 to 400,000, whereas a sub-micron CT X-ray system commands a price tag exceeding USD 600,000. These high costs pose significant challenges for companies, particularly those operating in cost-sensitive markets, as they require substantial upfront investments. Between 2022 and 2024, rising interest rates pushed the weighted average cost of capital up by 150 to 200 basis points, further straining financial resources by elongating payback periods and causing delays in equipment orders.[3]International Monetary Fund, “World Economic Outlook 2024,” imf.org This financial pressure has led many businesses to reassess their capital allocation strategies. While equipment-as-a-service offerings transform capital expenditure into operational expenditure (OPEX), enabling companies to reduce initial financial burdens, their adoption remains largely confined to mature economies. This limited uptake is attributed to factors such as the availability of advanced infrastructure, favorable regulatory environments, and higher levels of technological readiness in these regions.

Shortage Of Skilled Technicians for System Programming and Maintenance

According to SEMI's 2024 workforce survey, 62% of electronics plants in North America and Europe grapple with inspection-technician vacancies, with these positions remaining unfilled for an average of 120 days. This shortage highlights a critical gap in the availability of skilled labor necessary for maintaining operational efficiency in the electronics manufacturing industry. While AI has streamlined the rule-writing process, it has not eliminated the need for human expertise. Tasks such as model validation, continuous learning, and hardware calibration still require specialized skills that are not easily replaceable.[4]SEMI, “Workforce Survey 2024,” semi.org

The lack of qualified personnel for these roles can significantly impact production timelines, as the onboarding and training of new talent often take considerable time. Consequently, this reliance on specialized talent can prolong ramp-up timelines for new production lines by as much as 12 months, posing challenges for manufacturers aiming to scale operations or introduce new technologies efficiently.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Inspection Method: X-Ray Systems Move Ahead on Hidden Joints

Automatic optical inspection delivered 56.93% of 2025 revenue, demonstrating the breadth of tasks addressable by 2D and emerging 3D optics. X-ray inspection, however, is forecast to expand at an 10.74% CAGR through 2031 as ball-grid arrays, QFNs, and SiP modules proliferate. Computed-tomography units visualize voiding in micro-bumps and through-silicon vias at 1 µm voxel resolution, replacing destructive cross-sectioning. Optical-only stations remain cost-effective for components above 0.5 mm pitch, but their addressable share will narrow as 0.3 mm pitch becomes mainstream. Solder-paste inspection is fully integrated into surface-mount lines to catch stencil defects early, reducing downstream rework by more than 80%.

X-ray adoption draws support from semiconductor packaging trends that push chiplet architectures onto PCB assembly floors. Vendors such as Comet and Waygate now offer CT scanners tailored for high-throughput board lines, merging semiconductor-class resolution with conveyorized handling. Optical stations still dominate low-risk consumer products, yet even in smartphones volumetric checks are rising for under-display cameras and folded flex tails. Overall, x-ray growth lifts the printed circuit board inspection equipment market by unlocking inspection windows unreachable by visible light.

By System Type: Inline Platforms Capture Throughput Economics

Inline systems held 60.72% of 2025 demand and are projected to progress at a 11.68% CAGR, the fastest among all form factors. Their conveyor integration enables 100% board coverage at 15-30 s per piece without interrupting flow. Closed-loop feedback with printers and placement machines converts defect detection into immediate process correction, a capability that offline stations cannot match. Pay-per-inspection agreements further tilt economics toward inline purchases by treating inspection as a variable cost tied to low volume.

Offline and benchtop stations continue to serve engineering labs, first-article inspections, and low-volume medical, and avionics builds where flexibility outweighs speed. Yet their installed base is slowly declining as contract manufacturers consolidate multiple tasks into single inline nodes. The printed circuit board inspection equipment market therefore leans on inline platforms not only for scale but also for data granularity needed in smart-factory environments.

By Technology: 3D AOI Surges on Coplanarity Control

Two-dimensional AOI generated 48.02% of 2025 revenue because grayscale algorithms are mature and inexpensive. Three-dimensional AOI is forecast to grow at a 10.03% CAGR, driven by laser-triangulation and structured-light modules that measure height and volume to ±5 µm. The International Electrotechnical Commission released IPC-9716 in 2024, standardizing test patterns and benchmark metrics that confirm 30-40% lower false-call rates when 3D data feed convolutional neural networks.

3D X-ray (CT) complements 3D AOI by exposing hidden voids and through-vias that optical paths cannot see. Although CT carries premium pricing, producers of chiplet-based accelerators and high-bandwidth memory stacks accept the cost because a single escaped defect can scrap USD 5,000 in materials. Consequently, 3D modalities add depth to the printed circuit board inspection equipment market’s value proposition and expand its addressable spend beyond legacy 2D solutions.

By End User: Automotive Electronics Accelerates on EV Uptake

Consumer electronics accounted for 41.65% of the 2025 value, led by smartphones, tablets, and wearables produced in Asia-Pacific mega-factories. Automotive electronics is rising faster, with a 9.72% CAGR, as EV battery packs, traction inverters, and power-distribution units raise PCB count per vehicle. Zero-defect policies and ISO 26262 traceability rules compel tier-1 suppliers to adopt 100% inspection, increasing unit demand for both AOI and CT X-ray.

Industrial and energy electronics use AOI to guarantee 15-20-year reliability of inverters and grid converters. Aerospace and defense segments rely on offline CT and acoustic microscopy for root-cause analysis under AS9100 standards. Medical device makers follow FDA 21 CFR 820 rules, favouring documented calibration and traceability over high throughput. These sectors collectively balance the printed circuit board inspection equipment market by diversifying demand beyond high-volume consumer products.

By PCB Type: HDI Boards Drive 3D Adoption

Rigid PCBs captured 51.74% of 2025 revenue due to broad use in automotive and industrial applications. High-density interconnect (HDI) boards, however, are growing at a 10.24% CAGR. Their microvias, stacked vias, and thin copper features are impossible to validate with 2D grayscale alone, making 3D AOI essential. A 2024 IEEE study showed 65% fewer defect escapes in 0.3 mm-pitch assemblies when 3D AOI replaced 2D algorithms.

Flexible and rigid-flex boards support foldable phones, wearables, and avionics but introduce inspection challenges because transparent substrates and curved geometries create reflection artifacts. Vendors now offer adaptive lighting and bending fixtures to counter these issues. Advanced packaging substrates for chiplets require 1 µm CT scans, a niche covered by a handful of suppliers. Collectively, emerging board types add high-margin volume to the printed circuit board inspection equipment market by demanding multimodal inspection in a single line.

Geography Analysis

Asia-Pacific delivered 37.88% of global revenue in 2025 and is expected to expand at an 11.12% CAGR to 2031. China alone accounts for 28% of worldwide electronics manufacturing and hosts contract assemblers such as Foxconn and Luxshare Precision that mandate inline AOI across smartphone, laptop, and wearable lines. South Korea and Taiwan specialize in HDI substrates for memory modules and data-center accelerators, while Japan maintains a premium niche in automotive and industrial electronics that justifies early adoption of CT inspection. Government programs like China’s Made in China 2025 and South Korea’s K-Semiconductor Strategy subsidize smart-factory tools, further lifting regional demand.

North America and Europe jointly held roughly 44.62% of 2025 turnover. The United States CHIPS and Science Act allocate USD 52 billion for semiconductor and advanced-packaging plants, many of which will source inspection equipment for substrate and interposer lines. Germany, France, and Italy are upgrading automotive electronics capacity, installing CT X-ray to safeguard battery-pack and power-module quality. Regulatory regimes such as FDA 21 CFR 820 for medical devices and AS9100 for aerospace secure a baseline of offline CT and acoustic microscopy sales.

The Middle East, Africa, and South America contribute smaller shares but demonstrate patchy growth. Israel’s defense and medical-device sector insist on IPC Class 3 traceability, prompting CT purchases. Saudi Arabia and the United Arab Emirates have launched domestic electronics programs as part of diversification agendas, adding mid-tier AOI demand. Brazil and Argentina assemble consumer electronics and industrial controls for regional consumption, favouring cost-competitive 2D AOI units yet gradually incorporating Industry 4.0 data collection. These emerging hubs collectively enlarge the printed circuit board inspection equipment market footprint beyond traditional strongholds.

Competitive Landscape

The top five equipment vendors hold roughly 45% combined revenue, giving the market a moderate concentration. Nordson, Koh Young, and Omron leverage extensive service networks and bundled solutions that link printers, AOI, and reflow ovens. KLA and Camtek migrate semiconductor CT platforms into board assembly, offering 1 µm voxel resolution that addresses chiplet substrates. Regional specialists ViTrox, Mirtec, and Saki provide rapid customization and localized support that resonate with contract manufacturers on thin margins.

AI-enabled defect classification is the dominant competitive theme. Koh Young filed 37 deep-learning patents in 2024 for edge inference at 60 fps. Nordson’s YESTech Orion 3D AOI launched in March 2025 with NVIDIA Jetson Orin, lowering false calls by 35%. Disruptors Pemtron and Unicomp open their software stacks, allowing customers to train propriety neural networks via transfer learning, thereby reducing vendor lock-in. Price competition intensifies in mature 2D AOI after the release of IPC-9716 test metrics that make performance comparisons transparent.

Equipment-as-a-service and cloud analytics emerge as differentiators. Viscom now offers subscription pricing that converts CapEx into OPEX and aligns cash flow with board volume. Predictive-maintenance algorithms bundled into CT systems forecast X-ray tube wear and reduce unplanned downtime. Such service-centric models create recurring revenue for suppliers and raise switching costs, enhancing customer retention while widening the printed circuit board inspection equipment market opportunity.

Printed Circuit Board Inspection Equipment Industry Leaders

Nordson YESTECH Inc

Cognex Corporation

Vision Engineering Inc.

ViTrox Corp Bhd

Omron Electronics LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Nordson Corporation launched the YESTech Orion 3D AOI with NVIDIA Jetson Orin, delivering real-time classification at 60 fps and cutting false calls by 35%.

- February 2025: Koh Young Technology announced a USD 45 million expansion of its Incheon plant, adding 15,000 m² of capacity for 3D AOI production.

- January 2025: Omron Corporation partnered with Siemens Digital Industries to integrate VT-X950 3D AOI outputs into Siemens Opcenter for closed-loop process control.

- December 2024: ViTrox Corporation unveiled the V810 Ultra 3D AOI with 5 µm height resolution, priced 25% below peer offerings.

Global Printed Circuit Board Inspection Equipment Market Report Scope

The Printed Circuit Board Inspection Equipment Market Report is Segmented by Inspection Method (Automatic Optical Inspection, X-Ray Inspection, Solder Paste Inspection, Other Specialized Methods), System Type (Inline Systems, Offline or Benchtop Systems), Technology (2D AOI, 3D AOI, 2D X-Ray, 3D or CT X-Ray), End User (Consumer Electronics, Automotive Electronics, Industrial and Energy Electronics, Aerospace and Defense, Medical Device Manufacturers), PCB Type (Rigid PCBs, Flexible and Rigid-Flex PCBs, High-Density Interconnect PCBs, Advanced Packaging Substrates), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Automatic Optical Inspection (AOI) |

| X-Ray Inspection (AXI) |

| Solder Paste Inspection (SPI) |

| Other Specialized Methods (Acoustic, Laser, Thermography) |

| Inline Systems |

| Offline / Benchtop Systems |

| 2D AOI |

| 3D AOI |

| 2D X-Ray |

| 3D / CT X-Ray |

| Consumer Electronics Manufacturers |

| Automotive Electronics Manufacturers |

| Industrial and Energy Electronics |

| Aerospace and Defense |

| Medical Device Manufacturers |

| Rigid PCBs |

| Flexible and Rigid-Flex PCBs |

| High-Density Interconnect (HDI) PCBs |

| Advanced Packaging Substrates |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Inspection Method | Automatic Optical Inspection (AOI) | |

| X-Ray Inspection (AXI) | ||

| Solder Paste Inspection (SPI) | ||

| Other Specialized Methods (Acoustic, Laser, Thermography) | ||

| By System Type | Inline Systems | |

| Offline / Benchtop Systems | ||

| By Technology | 2D AOI | |

| 3D AOI | ||

| 2D X-Ray | ||

| 3D / CT X-Ray | ||

| By End User | Consumer Electronics Manufacturers | |

| Automotive Electronics Manufacturers | ||

| Industrial and Energy Electronics | ||

| Aerospace and Defense | ||

| Medical Device Manufacturers | ||

| By PCB Type | Rigid PCBs | |

| Flexible and Rigid-Flex PCBs | ||

| High-Density Interconnect (HDI) PCBs | ||

| Advanced Packaging Substrates | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the printed circuit board inspection equipment market?

The market is valued at USD 12.69 billion in 2026.

How fast is the printed circuit board inspection equipment market expected to grow?

It is projected to expand at a 9.28% CAGR, reaching USD 19.79 billion by 2031 over 2026-2031.

Which region leads demand for PCB inspection tools?

Asia-Pacific generated 37.88% of global revenue in 2025 and is forecast to grow the fastest at an 11.12% CAGR through 2031.

Why are 3D AOI systems gaining traction?

3D AOI measures height, coplanarity, and solder-paste volume with micron-level accuracy, reducing defect escapes in HDI and chiplet boards.

What drives inspection demand in automotive electronics?

Electric vehicles add up to USD 2,000 of electronic content per car and require zero-defect reliability, prompting 100% inline inspection.

How are vendors lowering capital barriers for customers?

Pay-per-inspection and equipment-as-a-service models shift costs from CapEx to OPEX, making advanced tools accessible to more manufacturers.

Page last updated on: