Document Scanner Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.06 Billion |

| Market Size (2031) | USD 8.95 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

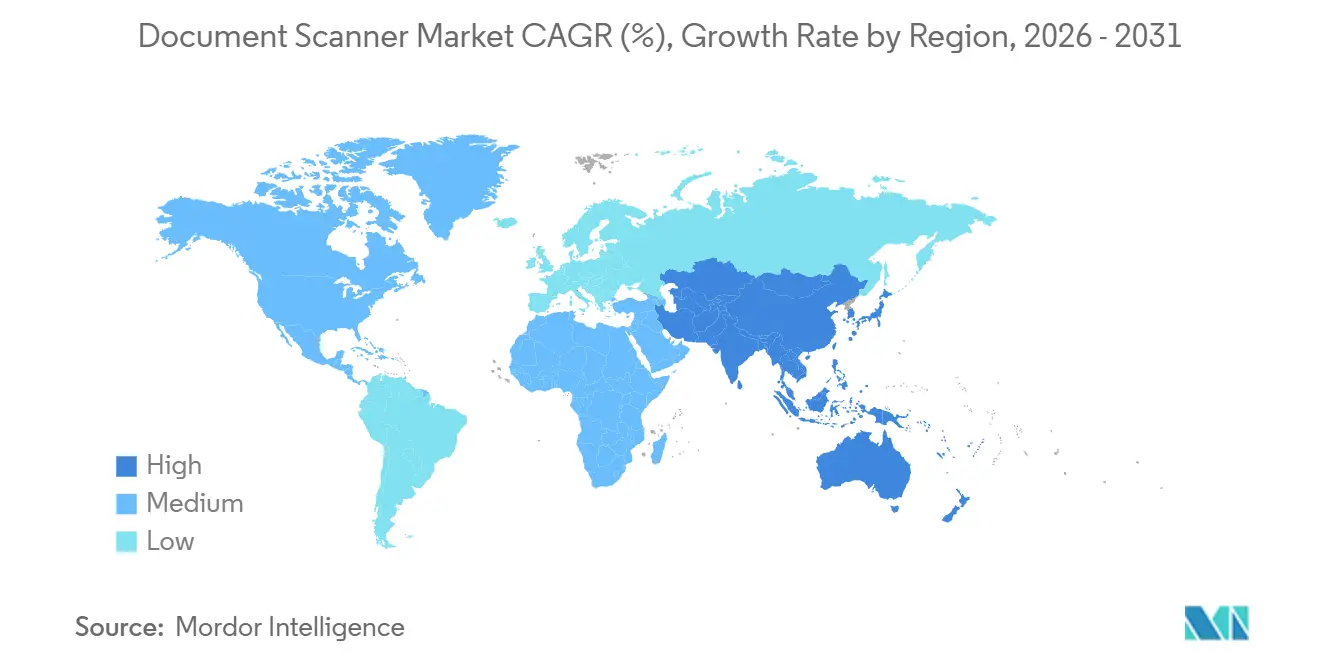

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Document Scanner Market Analysis by Mordor Intelligence

The document scanner market size is projected to be USD 6.73 billion in 2025, USD 7.06 billion in 2026, and reach USD 8.95 billion by 2031, growing at a CAGR of 4.86% from 2026 to 2031. Government e-records deadlines, hybrid-work adoption, and cloud-based workflow automation are recasting procurement priorities and shifting demand toward portable, wireless, and AI-enhanced capture devices. Agencies racing to comply with the U.S. National Archives’ electronic-records rule are driving multi-year archive projects, while small and medium enterprises favor scanner-as-a-service bundles that eliminate upfront capital expenditure. Vendors now embed machine-learning quality controls that boost OCR accuracy, turning hardware into an on-ramp for cloud content-management subscriptions. Asia-Pacific’s public-sector digitization campaigns add volume scale, even as mobile-camera apps cannibalize entry-level flatbeds and falling office paper volumes compress the low-end addressable pool.

Key Report Takeaways

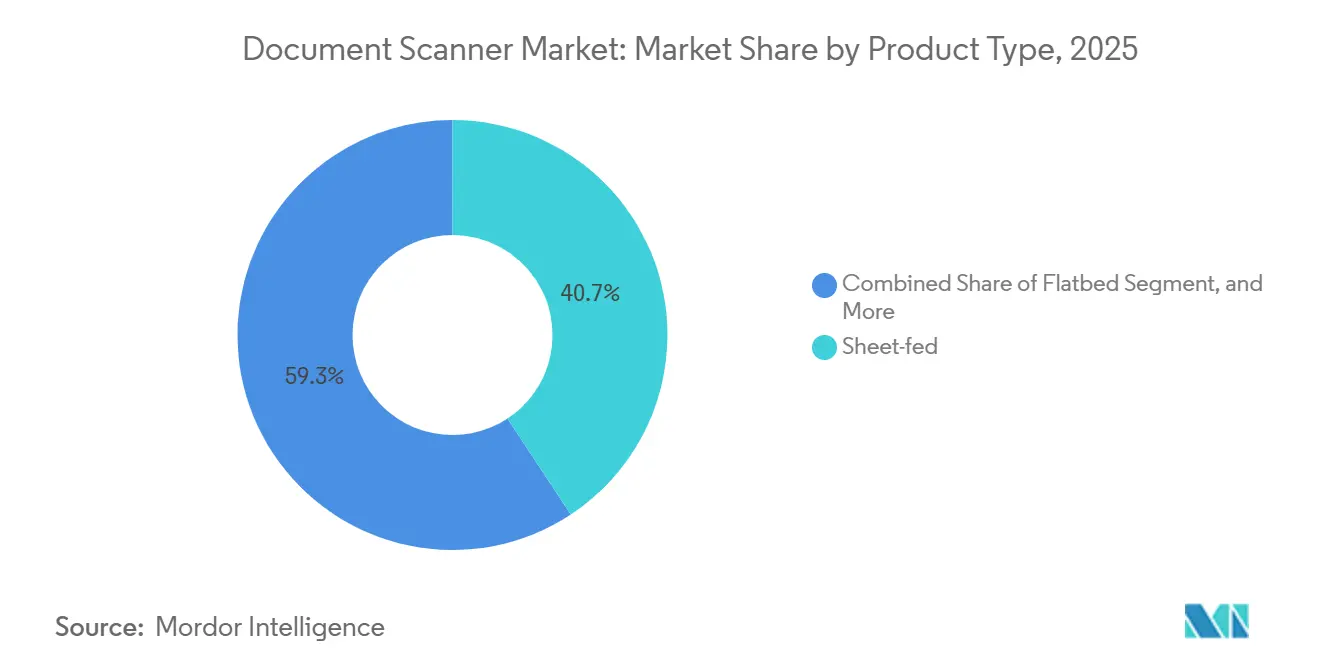

- By product type, sheet-fed models led with 40.73% revenue share in 2025, whereas portable and handheld units are forecast to expand at a 4.92% CAGR through 2031.

- By end-user industry, government entities accounted for 28.81% of 2025 demand, while healthcare is projected to post the fastest growth at 5.03% over 2026-2031.

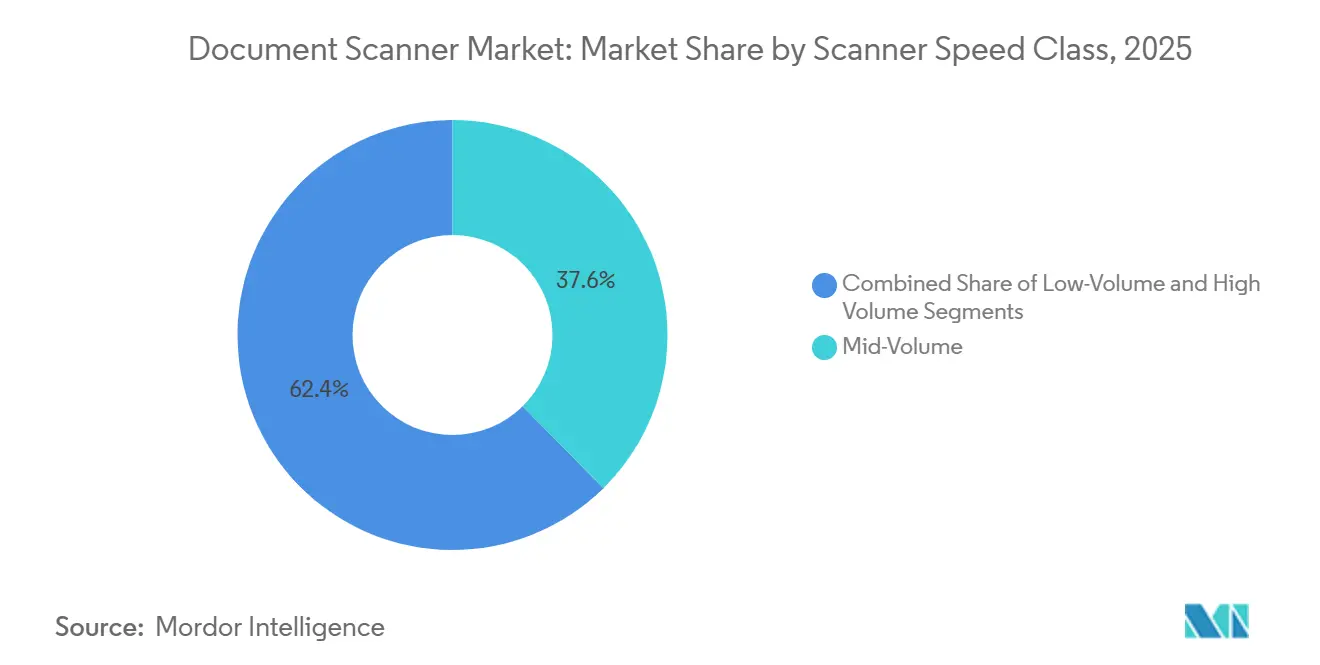

- By scanner speed class, mid-volume devices (30-60 ppm) held 37.62% share of the document scanner market size in 2025, but high-volume systems (>60 ppm) are advancing at a 4.88% CAGR through 2031.

- By connectivity, wireless and cloud-enabled scanners represented 36.82% of 2025 shipments and are progressing at a 5.09% growth rate to 2031.

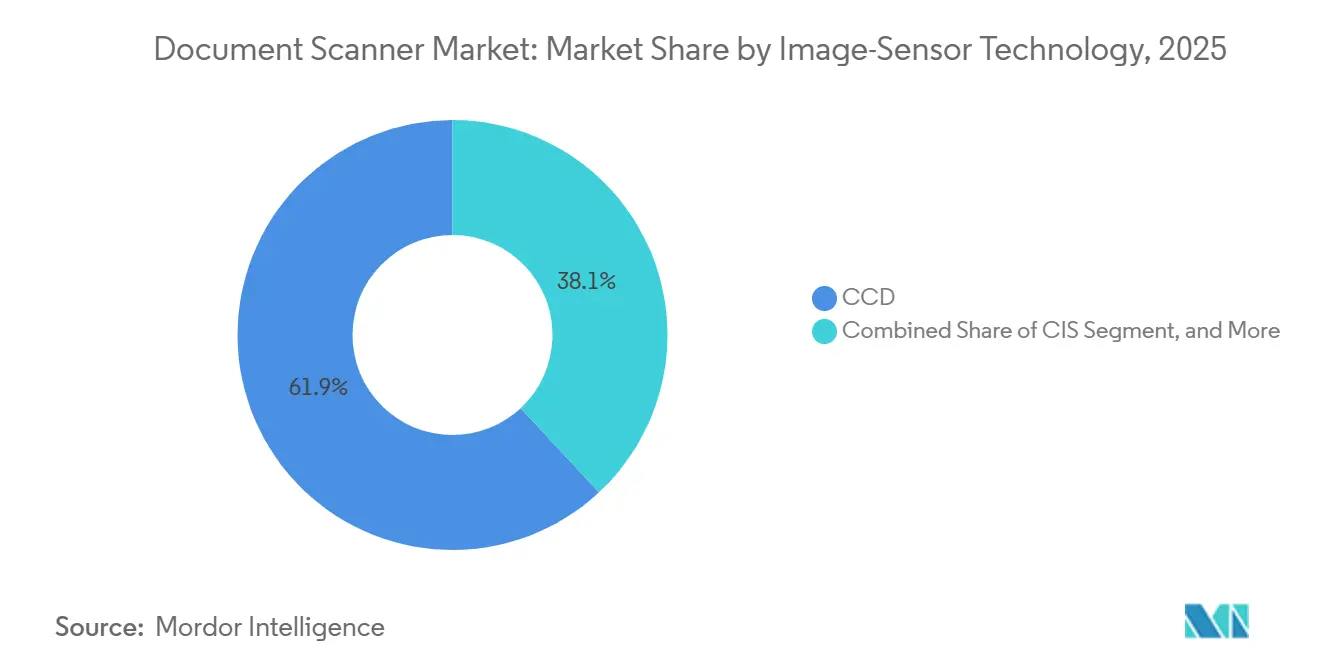

- By image-sensor technology, Contact Image Sensor devices retained 61.94% share in 2025, whereas Charge-Coupled Device units are expected to record the highest 5.05% CAGR across the forecast window.

- By distribution channel, direct sales captured 62.72% of 2025 revenue, but value-added resellers and e-commerce routes will expand at 5.11%, reflecting small-business preference for online procurement.

- By geography, Asia-Pacific commanded 41.77% of 2025 revenue and is on track for the quickest 5.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Document Scanner Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid hybrid-work adoption drives distributed scanning | +0.9% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Sharp price/performance leaps in sheet-fed models | +0.7% | Global, early adoption in Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Government e-records mandates accelerate archive projects | +1.2% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| BFSI KYC automation requires high-fidelity images | +0.6% | Global, concentrated in financial centers across all regions | Long term (≥ 4 years) |

| Cloud scanner-as-a-service subscriptions slash capex | +0.8% | North America and Europe, spill-over to Asia-Pacific | Medium term (2-4 years) |

| AI-based quality control raises OCR accuracy benchmarks | +0.5% | Global, led by North America and Europe technology adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Hybrid-Work Adoption Drives Distributed Scanning

Hybrid work splits document capture among home offices, co-working spaces, and branch locations, increasing demand for compact Wi-Fi-enabled scanners that route files directly to cloud repositories. HP’s Scan AI Enhanced, released in 2024, crops and deskews on-device, sidestepping bandwidth limits for remote users. Konica Minolta’s 2024 integration with M-Files adds automated metadata tagging, eliminating manual filing. Enterprises upgrading from legacy USB models now prioritize zero-touch configuration and remote fleet monitoring, accelerating refresh cycles. As a result, portable scanners that workers can install without IT support are gaining traction, reinforcing a distributed-first deployment mindset.

Government E-Records Mandates Accelerate Archive Projects

The U.S. Code of Federal Regulations 36 CFR 1236 prescribes 300-dpi bitonal capture for textual records and 24-bit color at 400 dpi for photographs, compelling agencies to procure production-grade devices that maintain image fidelity. The White House’s M-23-07 memo sets a December 31 2024 deadline for fully electronic federal workflows, compressing scanner procurement timelines. Similar mandates in the United Kingdom’s National Health Service and India’s Ayushman Bharat Digital Mission reinforce global momentum. Service bureaus such as Iron Mountain reported rising state-agency contracts as governments outsource large-scale back-file conversion. High-throughput duplex units that meet archival color standards now anchor multi-year digitization budgets.

Cloud Scanner-as-a-Service Subscriptions Slash Capex

Vendors bundle hardware, workflow software, and cloud storage into monthly operating-expense plans, lowering entry costs for small firms. HP’s Managed Print Services includes scanners, predictive maintenance, and per-page billing aligned with actual use.[1]HP Inc., “Scan AI Enhanced,” HP.COM Konica Minolta’s Workplace Hub lets customers scale capacity without upfront outlays, an attractive option when cash preservation outranks capital investment. Subscription models also embed automatic firmware updates and analytics dashboards, supporting a lifecycle revenue stream that offsets hardware price erosion. This shift favors brands with robust service footprints and disadvantages low-cost importers lacking field technicians.

AI-Based Quality Control Raises OCR Accuracy Benchmarks

Machine-learning algorithms embedded in firmware now detect shadows, skew, and bleed-through, correcting images before they reach downstream OCR engines. Google Cloud’s Enterprise OCR achieves 99.8% accuracy on structured forms, yet depends on high-quality input scans.[2]Google Cloud, “Enterprise OCR for Document AI,” CLOUD.GOOGLE Fujitsu’s fi-8000 series pairs convolutional-network classification with automatic document routing, cutting post-scan labor.[3]Fujitsu, “fi-8000 Series Scanners,” FUJITSU.COM Vendors differentiate through on-device AI accelerators that compress, enhance, and index content in real time, justifying premium pricing and locking customers into proprietary ecosystems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mobile-camera capture cannibalizes entry-level scanners | -0.6% | Global, most pronounced in North America and Europe | Short term (≤ 2 years) |

| Shrinking workplace paper volumes (~5% YoY) | -0.5% | Global, concentrated in developed markets | Medium term (2-4 years) |

| CIS image-sensor supply-chain volatility | -0.3% | Global, with acute impact in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Data-sovereignty barriers to cloud capture | -0.2% | Europe, Middle East, and select Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mobile-Camera Capture Cannibalizes Entry-Level Scanners

Smartphone apps such as Adobe Scan and Microsoft Lens create high-quality PDFs at zero marginal cost, eroding demand for sub-USD 200 flatbeds. Brother’s ADS-4900W targets small offices by offering direct cloud upload and multi-sheet feeds that mobile cameras cannot match. Vendors respond by emphasizing ultrasonic mis-feed detection, infrared fraud checks, and integration APIs absent from camera software. Nonetheless, low-volume personal scanning tasks increasingly default to phones, squeezing the bottom tier of the document scanner market.

Shrinking Workplace Paper Volumes

Digital signatures, electronic invoicing, and cloud collaboration tools reduce the number of pages entering office workflows. Vendors pivot toward software-centric value, exemplified by Konica Minolta’s metadata automation partnership with M-Files. While hybrid workers sometimes print at home, overall office paper output continues a mid-single-digit annual decline, tightening replacement cycles for low-speed department scanners. The resulting mix shift favors high-volume archive projects and subscription bundles over one-off hardware sales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Portable Units Propel Field Workflows

Portable and handheld scanners are forecast to grow at a 4.92% CAGR, surpassing the document scanner market average as auditors, adjusters, and visiting nurses digitize paperwork at client locations. Sheet-fed devices, which held a 40.73% document scanner market share in 2025, remain the default for government mailrooms that batch-process mixed media. Canon’s 1.2 kg imageFORMULA R50 shows how mobility now pairs with 50 ipm throughput.

The segment’s upside comes from smartphone-attachable models such as Socket Mobile’s XG640 and battery-powered Avision AD370F, blurring boundaries between capture hardware and mobile computing. Flatbeds stay relevant for fragile or oversized originals, whereas production-class units anchor service bureaus converting legacy archives to meet e-records deadlines. Vendors differentiate through ultrasonic mis-feed detection and self-healing firmware updates, sustaining premium pricing even as average selling prices slide on entry-level units.

By End-User Industry: Healthcare Surges Under Interoperability Mandates

Government agencies generated 28.81% of 2025 revenue owing to statutory compliance timetables, yet healthcare is set to expand at a 5.03% CAGR as hospitals digitize patient intake and insurance verification. Hyland found that near-universal EHR adoption still leaves consent forms and legacy files on paper, sustaining capture demand.

Banking, financial services, and insurance firms automate know-your-customer workflows that require high-fidelity scans with infrared fraud detection. Education, IT, and telecom outlets digitize contracts and student records, while service bureaus monetize outsource conversions. The document scanner market size for healthcare is projected to widen as telehealth growth pushes providers to cloud-based workflows that rely on embedded scanner APIs for real-time file ingestion.

By Scanner Speed Class: High-Volume Devices Serve Archive Consolidation

High-volume systems (>60 ppm) are slated to progress at a 4.88% CAGR through 2031 as service bureaus tackle multi-year back-file conversion. Mid-volume units balanced cost and capacity to secure a 37.62% document scanner market size share in 2025. Ricoh’s fi-8170, scanning 70 ppm with ultrasonic multi-feed detection, exemplifies throughput-plus-reliability positioning.

Regulations specifying 300 dpi bitonal capture drive demand for on-board image processing that avoids throughput bottlenecks. Low-volume devices under 30 ppm confront substitution by smartphone cameras and MFPs, steering vendors to bundle workflow software that raises switching costs. The speed-class hierarchy thus reflects customer emphasis on project scale and regulatory image-quality thresholds.

By Connectivity: Wireless and Cloud Integration Re-Shape Deployment

Wireless and cloud-enabled scanners accounted for 36.82% of 2025 revenue and are growing at 5.09%, reflecting hybrid-work dispersion. USB-only models linger in cost-sensitive roles, whereas Ethernet-networked units persist in centralized mailrooms. HP embeds machine-learning enhancement locally to limit bandwidth needs.

Konica Minolta couples its bizhub line with intelligent information management to eliminate manual filing, turning connectivity into workflow value. Canon’s Wi-Fi Direct allows smartphone pairing on job sites lacking corporate networks. As zero-trust security shifts authentication from perimeter to device, scanners become managed cloud endpoints, positioning the document scanner market for subscription-driven recurring revenue.

By Image-Sensor Technology: CIS Dominates but CCD Finds Archival Niches

Contact Image Sensor devices held 61.94% of 2025 revenue due to compact size and low power draw, yet Charge-Coupled Device units are projected for a 5.05% CAGR because of deeper focus depth and richer color capture, prized in legal discovery and cultural-heritage projects. Image Access demonstrated 600 dpi CIS resolution at sub-10 watt power, bringing fanless acoustics to desktop models.

Advances in back-side-illuminated CIS arrays shrink the quality gap, but FADGI guidelines still endorse CCD for master files requiring century-long preservation. Supply-chain clustering among Asian CIS foundries poses volatility risk, nudging some buyers toward dual-source strategies that include CCD-based alternatives.

By Distribution Channel: VARs and E-Commerce Win Small-Business Wallets

Direct sales captured 62.72% of 2025 revenue through entrenched relationships with large agencies, yet value-added resellers and online retailers are forecast for 5.11% growth as small enterprises prefer self-service purchasing. Amazon Business and CDW enable overnight delivery and transparent pricing, eroding field-sales advantages.

VARs differentiate by bundling capture devices with document-management software, training, and integration services, shifting profit from hardware markup to recurring support. HP’s per-page subscription bundles and Brother’s cloud-ready ADS-4900W, sold primarily online, illustrate the model’s appeal to budget-constrained buyers seeking predictable costs and rapid deployment.

Geography Analysis

Asia-Pacific generated the largest contribution with a 41.77% document scanner market share in 2025 and is expected to deliver a 5.23% CAGR through 2031. China’s 14th Five-Year Plan mandates full provincial e-government by 2027, Japan’s Digital Agency champions fax elimination, and India’s Ayushman Bharat Digital Mission compels hospitals to maintain electronic records. South Korea’s 2025 deadline for local-government digital archives further fuels regional momentum.

North America remains the second-largest territory, propelled by National Archives and Records Administration rules and the White House M-23-07 transition mandate. Canada’s pending Library and Archives Act amendments widen the addressable pool, while Mexican municipal digitization initiatives begin to unlock latent demand. Portable scanners with Wi-Fi connectivity resonate with dispersed government field offices and hybrid-work staff.

Europe shows steady but moderate expansion. The United Kingdom’s National Health Service targets full patient-record digitization by 2026. Germany’s BSI issued 2024 archival guidelines that specify minimum scanner resolution. France now requires electronic storage of public contracts over EUR 25,000. Elsewhere, Middle East and Africa plus South America register nascent growth constrained by budget limits, often outsourcing archive projects to service bureaus rather than purchasing fleets outright.

Competitive Landscape

Top Companies in Document Scanner Market

The document scanner market contains a mid-tier concentration where the top five brands—Ricoh, Canon, Epson, Fujitsu, and HP—exploit installed MFP footprints to cross-sell dedicated scanners. Each follows one of three plays: premium AI-centric differentiation, low-cost CIS-driven designs, or vertical workflow specialization. Specialty niches such as large-format technical-drawing capture and ruggedized portable units remain fragmented, giving entrants like Hexagon and Socket Mobile room to innovate.

Ricoh’s ultrasonic multi-feed patent illustrates a pivot toward machine-learning feature locks that sustain pricing power while reducing human error. Canon’s 1.2 kg R50 targets field professionals needing mobility and speed. Epson’s compact ES-580W addresses home-office clusters where wireless setup outranks raw throughput. Fujitsu’s fi-8000 embeds document classification, reinforcing a platform strategy built around capture software subscriptions.

Smaller brands—including Plustek, Visioneer, and Avision—compete on entry-price points but lack nationwide service footprints. Their ability to win public-sector contracts improved after Plustek’s ISO 9001:2015 certification, yet large enterprises still favor full-service vendors offering on-site maintenance and scanner-as-a-service financing. White-space opportunities lie in hybrid devices combining 2D document capture with 3D object imaging for e-commerce and in battery-powered scanners hardened for field engineers in extreme environments.

Document Scanner Industry Leaders

Canon Inc.

Seiko Epson Corporation

HP Inc.

Xerox Holdings Corporation

Brother Industries, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Ricoh completed acquisition of the remaining shares of Fujitsu’s scanner business, strengthening its global position and broadening its product lineup.

- January 2025: ScanTech AI Systems completed its merger with Mars Acquisition Corp. and began trading on Nasdaq under ticker STAI, expanding AI imaging applications into security screening.

- January 2025: FUJIFILM Business Innovation and Konica Minolta established Global Procurement Partners Corp. to centralize imaging equipment component sourcing, aiming for cost efficiency and supply-chain resilience.

- December 2024: Xerox announced its intention to acquire Lexmark International from Ninestar for USD 1.5 billion, enhancing manufacturing breadth and geographic reach.

Global Document Scanner Market Report Scope

The document scanner converts the physical document into digital format. It enables the user or an organization to store and retrieve the documents online, which lessens storage costs and delivers greater work efficiency. Furthermore, digital records allow greater collaboration within business processes, reducing cycle times and costs.

The Document Scanner Market Report is Segmented by Product Type (Flatbed, Sheet-fed, Production/High-Speed, Portable/Handheld), End-User Industry (BFSI, Government, Healthcare, IT and Telecom, Education, Service Bureaus and BPO), Scanner Speed Class (Low-Volume, Mid-Volume, High-Volume), Connectivity (USB-Only, Networked, Wireless/Cloud-Enabled, Stand-alone Touchscreen), Image-Sensor Technology (CCD, CIS), Distribution Channel (Direct, VAR/e-Commerce), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). Market Forecasts are Provided in Terms of Value (USD).

| Flatbed |

| Sheet-fed |

| Production / High-Speed |

| Portable / Handheld |

| Banking, Financial Services and Insurance (BFSI) |

| Government |

| Healthcare |

| Information Technology and Telecom |

| Education |

| Service Bureaus and BPO |

| Low-Volume (< 30 ppm) |

| Mid-Volume (30 – 60 ppm) |

| High-Volume (> 60 ppm) |

| USB-Only |

| Networked (Ethernet) |

| Wireless / Cloud-Enabled |

| Stand-alone Touchscreen |

| CCD |

| CIS |

| Direct (OEM) |

| Value-Added Resellers / e-Commerce |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Flatbed | |

| Sheet-fed | ||

| Production / High-Speed | ||

| Portable / Handheld | ||

| By End-user Industry | Banking, Financial Services and Insurance (BFSI) | |

| Government | ||

| Healthcare | ||

| Information Technology and Telecom | ||

| Education | ||

| Service Bureaus and BPO | ||

| By Scanner Speed Class | Low-Volume (< 30 ppm) | |

| Mid-Volume (30 – 60 ppm) | ||

| High-Volume (> 60 ppm) | ||

| By Connectivity | USB-Only | |

| Networked (Ethernet) | ||

| Wireless / Cloud-Enabled | ||

| Stand-alone Touchscreen | ||

| By Image-Sensor Technology | CCD | |

| CIS | ||

| By Distribution Channel | Direct (OEM) | |

| Value-Added Resellers / e-Commerce | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the document scanner market be by 2031?

It is projected to reach USD 8.95 billion by 2031, marking a 4.86% CAGR from 2026.

Which product type is growing fastest?

Portable and handheld units are forecast to expand at a 4.92% CAGR as field workers digitize documents on site.

Why is healthcare scanning demand accelerating?

Interoperability mandates require digital intake and legacy record conversion, pushing healthcare to a 5.03% growth rate.

What role does cloud connectivity play in scanner adoption?

Wireless and cloud-enabled models simplify hybrid-workflows and are advancing at a 5.09% CAGR through subscription bundles.

How are vendors differentiating against smartphone capture?

They embed AI quality control, ultrasonic mis-feed detection, and secure cloud APIs that mobile cameras cannot match.

Which region offers the highest growth opportunity?

Asia-Pacific leads with a 5.23% CAGR, propelled by government digitization plans in China, Japan, India, and South Korea.

Page last updated on: