Digital Forensics And Incident Response (DFIR) Solutions Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 10.46 Billion |

| Market Size (2030) | USD 26.43 Billion |

| Growth Rate (2025 - 2030) | 20.37% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Forensics And Incident Response (DFIR) Solutions Market Analysis by Mordor Intelligence

The digital forensics and incident response solutions market size stood at USD 10.46 billion in 2025 and is forecast to reach USD 26.43 billion by 2030, advancing at a 20.37% CAGR. Growth is propelled by aggressive ransomware innovation, stricter breach-notification rules that compress investigation windows, and the migration of business-critical workloads to cloud and edge platforms that legacy tools cannot parse effectively. Vendors that marry automated evidence capture with human expertise are winning share as buyers shift from reactive log collection to proactive threat-hunting programs. Consolidation among platform providers, coupled with venture funding for niche specialists, signals an environment where differentiated analytics and cloud-native visibility trump standalone point products. Organizations now treat robust DFIR capabilities as board-level risk-mitigation assets rather than discretionary compliance outlays, further accelerating adoption across regulated and unregulated sectors alike.[1]CrowdStrike Holdings Inc., “CrowdStrike Reports Fourth Quarter and Fiscal Year 2025 Financial Results,” ir.crowdstrike.com

Key Report Takeaways

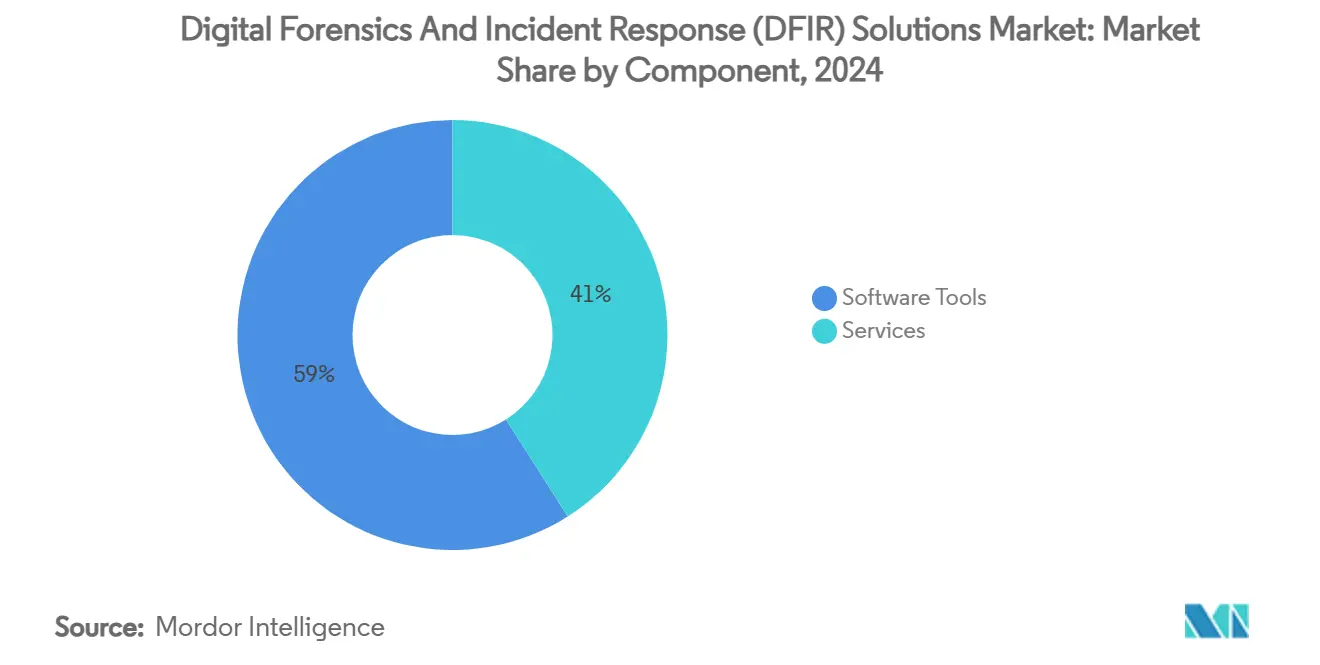

- By component, software tools led with 59% of the digital forensics and incident response solutions market share in 2024, while services are on track to expand at a 24.40% CAGR to 2030.

- By deployment mode, on-premises maintained 52% share of the digital forensics and incident response solutions market size in 2024, yet cloud-based offerings are projected to surge at 26.80% CAGR through 2030.

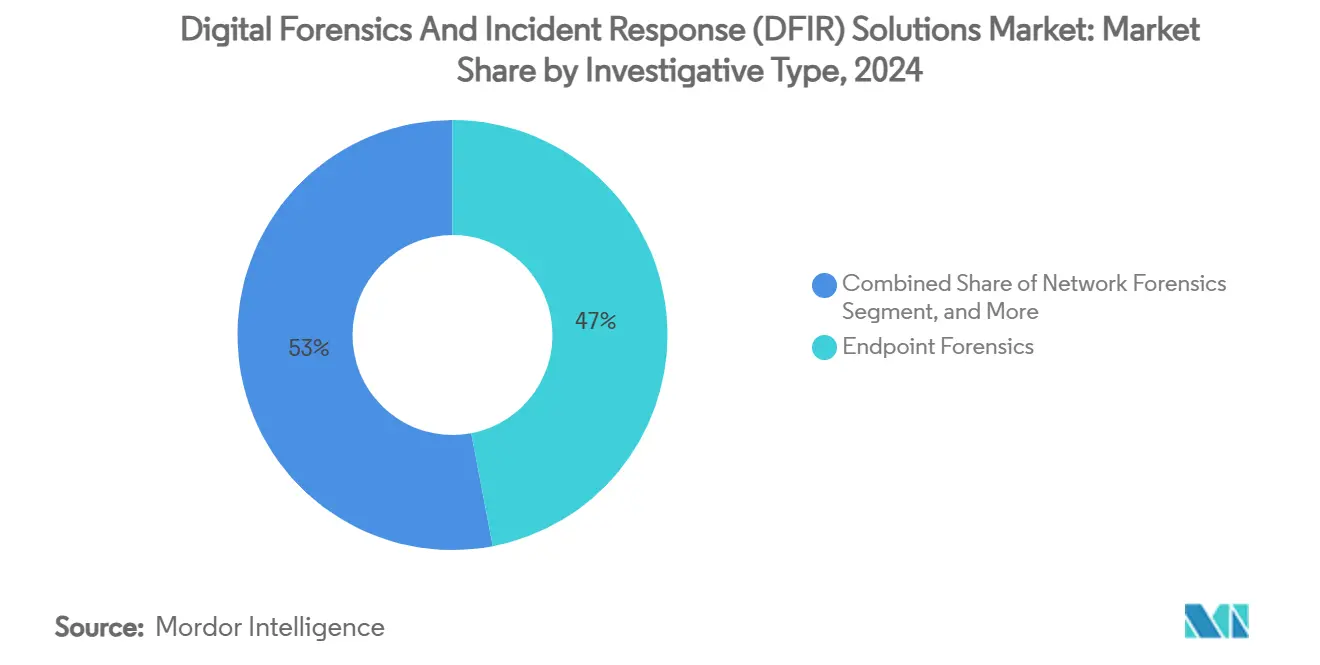

- By investigative type, endpoint forensics captured 47% of 2024 revenue whereas cloud forensics is forecast to climb at a 28.20% CAGR to 2030.

- By end-user vertical, government and defense held 26% of 2024 revenue; healthcare is advancing at a 25.60% CAGR over the same period.

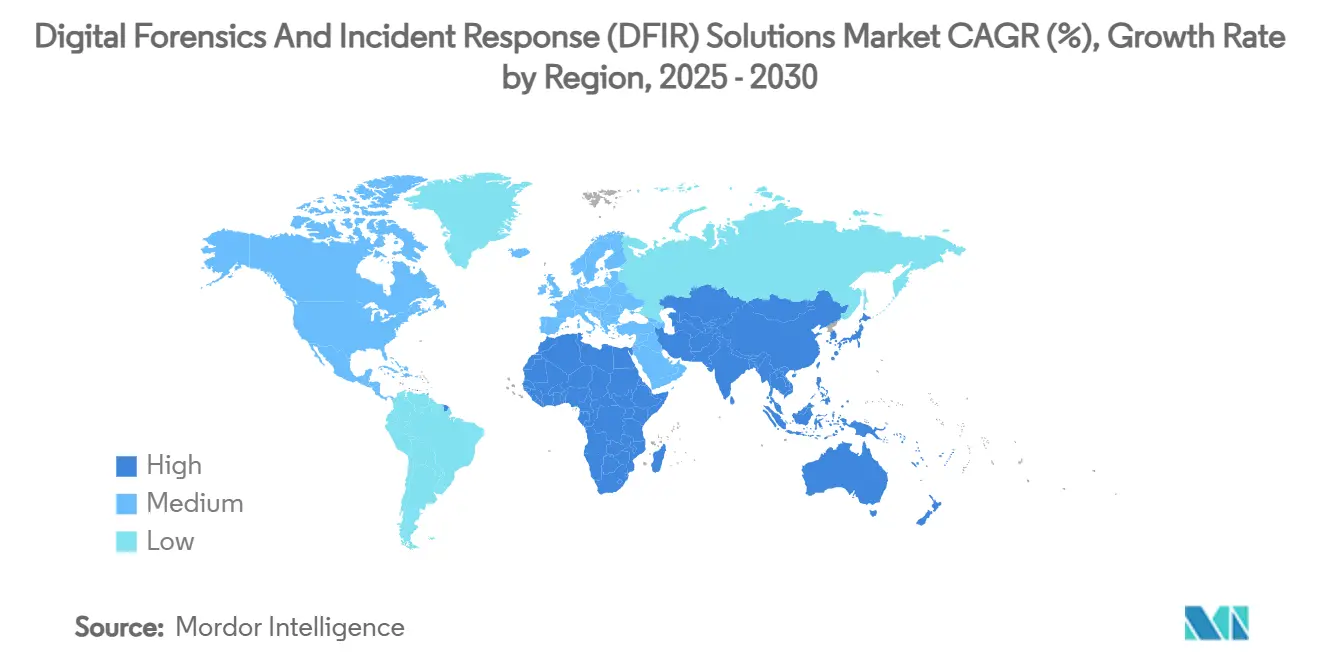

- By geography, North America accounted for 38% of 2024 revenue, while Asia-Pacific is poised for a 23.90% CAGR to 2030.

Global Digital Forensics And Incident Response (DFIR) Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating ransomware sophistication | +4.20% | Global, with acute impact in North America and Europe | Short term (≤ 2 years) |

| Rapid regulatory tightening on breach notification | +3.80% | North America and EU leading, APAC following | Medium term (2-4 years) |

| Cloud-native workload visibility gaps | +3.50% | Global, concentrated in cloud-first economies | Medium term (2-4 years) |

| Endpoint telemetry explosion (EDR/XDR overlap) | +2.90% | North America and APAC core markets | Short term (≤ 2 years) |

| AI-driven triage reducing analyst fatigue | +2.10% | Advanced economies with skilled workforce shortages | Long term (≥ 4 years) |

| Convergence of OT and IT investigations in critical infra | +1.80% | Industrial economies, particularly North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating ransomware sophistication

Ransomware collectives have pivoted from blunt encryption tactics to multi-stage playbooks that weaponize zero-days and automate reconnaissance with AI. Recent campaigns by the FunkSec syndicate showcase affiliate distribution at industrial scale, forcing enterprises to implement forensic tooling that reconstructs cross-domain kill chains within minutes rather than days.[2]Bitdefender Enterprise, “FunkSec: An AI-Centric and Affiliate-Powered Ransomware Group,” bitdefender.com Encryption-less extortion, where data exfiltration precedes any file locking, demands real-time evidence snapshots and behaviour-based analytics. Average breach costs reached USD 4.88 million for victims in 2025, converting DFIR outlays from discretionary spend to insured risk-transfer prerequisites.

Rapid regulatory tightening on breach notification

Statutes such as the U.S. Cyber Incident Reporting for Critical Infrastructure Act (CIRCIA) mandate 72-hour disclosures, while federal banking agencies require notices inside 36 hours. Similar compression is visible under GDPR and newly proposed APAC cyber-resilience bills.[3]Cybersecurity and Infrastructure Security Agency, “Cyber Incident Reporting for Critical Infrastructure,” cisa.gov These timeframes eliminate extended manual data gathering, obliging firms to automate chain-of-custody, evidence hashing, and preliminary root-cause analysis. DFIR suites now embed compliance templates that generate regulator-ready timelines at the click of a button, reframing incident response as a legal deliverable rather than an exclusively technical task.

Cloud-native workload visibility gaps

Ephemeral containers, serverless functions, and autoscaling clusters erase forensic artifacts the moment an instance terminates. The shared-responsibility model further obscures ownership of logs and memory snapshots across multiload estates. Platforms such as Cado Security capture volatile data continuously and stitch evidence across AWS, Azure, and Google Cloud, cutting average investigation time to 26.1 days. Demand for immutable, vendor-agnostic evidence vaults is rising as insurers and courts question the admissibility of cloud logs without verifiable custody trails.

Endpoint telemetry explosion (EDR/XDR overlap)

Proliferation of endpoint detection and response agents has flooded SOCs with alerts. CrowdStrike’s Charlotte AI processed more than 14 trillion telemetry events in 2025, triaging cases and shortening mean-time-to-respond by 48% for Falcon Complete customers. The intersection of EDR, XDR, and DFIR compels vendors to consolidate tooling so investigators can pivot from prevention data to deep-dive forensics without exporting artifacts into separate silos.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of qualified DFIR analysts | -3.10% | Global, acute in developed markets | Medium term (2-4 years) |

| Encryption and zero-trust architectures hindering evidence collection | -2.40% | Advanced economies with mature security postures | Long term (≥ 4 years) |

| Budget diversion to preventive controls | -1.90% | Cost-conscious markets, particularly SME segments | Short term (≤ 2 years) |

| Cloud service-provider "shared-responsibility grey zones" | -1.60% | Cloud-first economies and multi-cloud deployments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of qualified DFIR analysts

Demand outstrips supply as universities struggle to keep curricula current with threat evolution. Entry-level responders rarely possess kernel-level, packet-level, and cloud architecture knowledge simultaneously. Rising salaries push smaller firms toward managed DFIR services, but providers confront the same hiring bottlenecks, constraining overall capacity. AI assists by standardizing evidence tagging, yet expert testimony and tool-validation requirements maintain a floor of human involvement.

Encryption and zero-trust architectures hindering evidence collection

Widespread TLS 1.3 adoption, disk encryption, and micro-segmented networks safeguard data in transit and at rest yet block legitimate investigators from acquiring memory dumps or decrypted traffic flows. Organizations must implement escrowed key-management or real-time packet capture prior to encryption, adding cost and architectural complexity. These hurdles slow DFIR engagements and heighten the risk of incomplete timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Acceleration Outpaces Software Growth

Services captured 41% of 2024 revenue, yet they are projected to climb 24.40% CAGR to 2030, closing the gap with software that presently controls 59%. The digital forensics and incident response solutions market size for services is expected to reach USD 14.1 billion by 2030 as enterprises outsource 24/7 evidence capture, reverse engineering, and litigation support. Managed offerings amortize scarce investigator talent across dozens of clients, delivering economies individual firms cannot match. CrowdStrike’s Falcon Complete, underpinned by Charlotte AI, exemplifies this fusion of agentic automation with human escalation pathways.

Software growth remains solid but slower, constrained by complex deployment and skills requirements. Pure-play vendors mitigate friction by embedding guided workflows, low-code playbooks, and SaaS delivery. Exterro’s FTK 8.1 introduces entity-centric views that condense terabytes into actionable pivots for junior analysts. Over the forecast period, convergence into platform-as-a-service models will blur the line between license and retainer, enabling usage-based billing that mirrors cloud compute.

By Deployment Mode: Cloud Migration Accelerates Despite Sovereignty Concerns

On-premises installations still held 52% of 2024 spend as heavily regulated sectors guard evidence in local vaults. However, cloud-hosted suites are expanding at 26.80% CAGR, reflecting operational efficiencies and elastic compute for large-scale memory and packet analysis. The digital forensics and incident response solutions market size for cloud deployments is forecast to exceed USD 11 billion by 2030. Google Cloud’s Security Command Center Enterprise integrates Mandiant telemetry, providing single-pane investigations across multiload and on-prem assets.

Sovereign-cloud regions and customer-managed encryption keys address chain-of-custody anxieties. Hybrid topologies, where evidence is cached on-prem then offloaded to cloud analytics engines, are gaining favour among European financial institutions bound by residency laws. Vendors that offer tamper-proof hashing at ingestion and support e-discovery export formats will differentiate as courts scrutinize the integrity of cloud-stored exhibits.

By Investigative Type: Cloud Forensics Leads Growth Curve

Endpoint forensics generated 47% of 2024 billings, anchored by entrenched EDR footprints. Yet cloud forensics is the fastest-growing segment at 28.20% CAGR, propelled by container-orchestrated environments where evidence disappears in seconds. The digital forensics and incident response solutions market share for cloud forensics is projected to hit 31% by 2030. Darktrace’s planned purchase of Cado Security underscores the rush to absorb expertise in memory-for-serverless acquisition and cross-cloud timeline stitching.

Network and mobile forensics maintain vital roles for lateral-movement detection and bring-your-own-device policies. Emerging operational-technology forensics adds a fresh layer as utilities and manufacturers demand artifact extraction from programmable logic controllers. Patent filings for distributed computational graphs and selective log access illustrate ongoing R and D to scale analysis while preserving privacy.

By End-user Vertical: Healthcare Growth Surges Past Government Spending

Government and defense remain the top spenders at 26% revenue share, justified by national-security imperatives and classified network requirements. Nonetheless, healthcare is surging 25.60% CAGR, driven by ransomware impacts on patient safety and regulatory penalties. Annual HIPAA settlements exceeded USD 120 million in 2024, elevating forensic readiness to board priorities. The digital forensics and incident response solutions market size for healthcare is projected to triple to USD 5.2 billion by 2030.

BFSI continues steady adoption as regulators demand immutable audit trails for fraud-related incidents, while manufacturing invests to secure converged OT-IT production lines. Vendor specialization-such as Cellebrite’s medical device artifact parsers-demonstrates that sector-specific plugins can unlock premium pricing. Cross-sector collaboration on evidence-retention standards is expected as insurers harmonize breach-cost modelling across industries.

Geography Analysis

North America retained 38% of 2024 revenue, supported by CIRCIA, SEC cyber-reporting rules, and federal cybersecurity allocations surpassing USD 10 billion. High breach volumes and litigation exposure foster demand for enterprise-grade DFIR platforms with courtroom-defensible evidence chains. Venture funding concentrates in the region, further entrenching technological leadership. Talent shortages, however, cap organic expansion, pushing buyers toward automated toolsets and managed retainers.

Europe delivers mid-teens growth under GDPR’s 72-hour mandate and impending NIS-2 directives that extend reporting to a broader swath of critical entities. Data-sovereignty strictures channel demand toward on-prem or sovereign-cloud deployments that can notarize evidence without violating privacy statutes. The region’s AI sovereignty push is steering procurement toward platforms that offer transparent model cards and algorithmic audit features.

Asia-Pacific records the fastest trajectory at 23.90% CAGR. Massive digitization, surging cyber-insurance penetration, and government incentives such as Indonesia’s BerdAIa for Security program-expected to avert IDR 29 trillion in losses-amplify adoption. Diverse regulatory maturity demands modular tooling that can toggle between prescriptive regimes in Singapore and nascent guidelines in emerging ASEAN markets. Local SOC buildouts and data-residency mandates spur regional cloud nodes and bilingual investigation consoles, positioning APAC as a major battleground for vendor expansion through 2030.

Competitive Landscape

The digital forensics and incident response solutions market is moderately fragmented. The top five vendors captured roughly 48% of 2024 revenue, leaving room for specialist disruptors. Platform leaders-CrowdStrike, IBM, Google Cloud-Mandiant, and Microsoft-compete on telemetry breadth, AI acceleration, and ecosystem lock-in. Charlotte AI’s 22% ARR lift exemplifies the revenue impact of embedding generative models inside investigation flows.[4]Exterro Inc., “Exterro Completes Significant Strategic Recapitalization in Excess of USD 1 Billion,” exterro.com

Consolidation is accelerating: Exterro’s USD 1 billion recapitalization absorbed AccessData, expanding from e-discovery into full-spectrum forensics. Darktrace’s proposed Cado Security acquisition adds cloud-native memory capture, while Trustwave’s merger with Cybereason blends MDR scale with endpoint telemetry depth. Buyers value integrated stacks that collapse SIEM, SOAR, and DFIR into unified workspaces, reducing swivel-chair fatigue for analysts.

Niche players keep margins by addressing gaps such as mobile extraction (Cellebrite), large-scale data-carving (Nuix), or OT protocol parsing (Dragos). Patent filings around selective log-access and distributed graph analysis suggest continued innovation momentum outside the mega platform orbit. Over the forecast horizon, the market is likely to bifurcate full-stack suites for Fortune 1000 buyers and specialized SaaS micro-services for mid-market incident responders.

Digital Forensics And Incident Response (DFIR) Solutions Industry Leaders

International Business Machines Corporation

Cisco Systems, Inc.

OpenText Corporation

Cellebrite DI Ltd.

Magnet Forensics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Google Cloud launched Indonesia BerdAIa for Security program with a Jakarta security-operations region, aiming to prevent IDR 29 trillion (USD 1.8 billion) in cyber losses over five years.

- June 2025: CrowdStrike posted 22% ARR growth for Q1 FY26 and introduced Falcon Privileged Access, extending AI-driven protection across identity layers.

- May 2025: Securonix unveiled GenAI Agents to automate Level 1-3 SOC workflows, promising analyst-time savings of up to 60%.

- April 2025: CrowdStrike released Charlotte AI with agentic investigation capabilities that halve meantime-to-resolve metrics for early adopters.

Global Digital Forensics And Incident Response (DFIR) Solutions Market Report Scope

| Platform-level Zero Trust Network Access (ZTNA) |

| Data-centric Security Platforms |

| Identity and Access Management (IAM) Suites |

| Security Service Edge (SSE) Solutions |

| Cloud-based |

| Hybrid |

| On-premises |

| Large Enterprises (Less than 1,000 employees) |

| Small and Mid-sized Enterprises (SME) |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Government and Public Sector |

| IT and Telecom |

| Manufacturing and Critical Infrastructure |

| Retail and e-Commerce |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Platform-level Zero Trust Network Access (ZTNA) | |

| Data-centric Security Platforms | ||

| Identity and Access Management (IAM) Suites | ||

| Security Service Edge (SSE) Solutions | ||

| By Deployment Mode | Cloud-based | |

| Hybrid | ||

| On-premises | ||

| By Organization Size | Large Enterprises (Less than 1,000 employees) | |

| Small and Mid-sized Enterprises (SME) | ||

| By Industry Vertical | Banking, Financial Services and Insurance (BFSI) | |

| Healthcare and Life Sciences | ||

| Government and Public Sector | ||

| IT and Telecom | ||

| Manufacturing and Critical Infrastructure | ||

| Retail and e-Commerce | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current liquid crystal display market size and its growth outlook?

The liquid crystal display market generated USD 2.14 billion in 2025 and is projected to reach USD 3.29 billion by 2030, reflecting an 8.98% CAGR.

Which region holds the largest share of the liquid crystal display market?

Asia-Pacific leads with 47.1% revenue share, supported by China's dominant manufacturing capacity.

How fast is the automotive segment within the liquid crystal display market growing?

Automotive applications are forecast to expand at a 12.7% CAGR from 2025-2030, the fastest among major application categories.

Why are Mini-LED backlit LCDs important for the liquid crystal display market?

Mini-LED backlighting boosts contrast and energy efficiency, enabling LCDs to compete with OLED in premium devices while extending LCD relevance in high-end segments.

Who are the top manufacturers in the liquid crystal display market?

BOE and TCL Huaxing together control just over 50% of global LCD panel capacity, followed by Samsung Display and several niche specialists.

What is the primary competitive threat to the liquid crystal display market?

Continued OLED price erosion is narrowing the cost gap, potentially diverting premium demand away from LCDs over the medium term.

Page last updated on: