Diabetic Socks Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

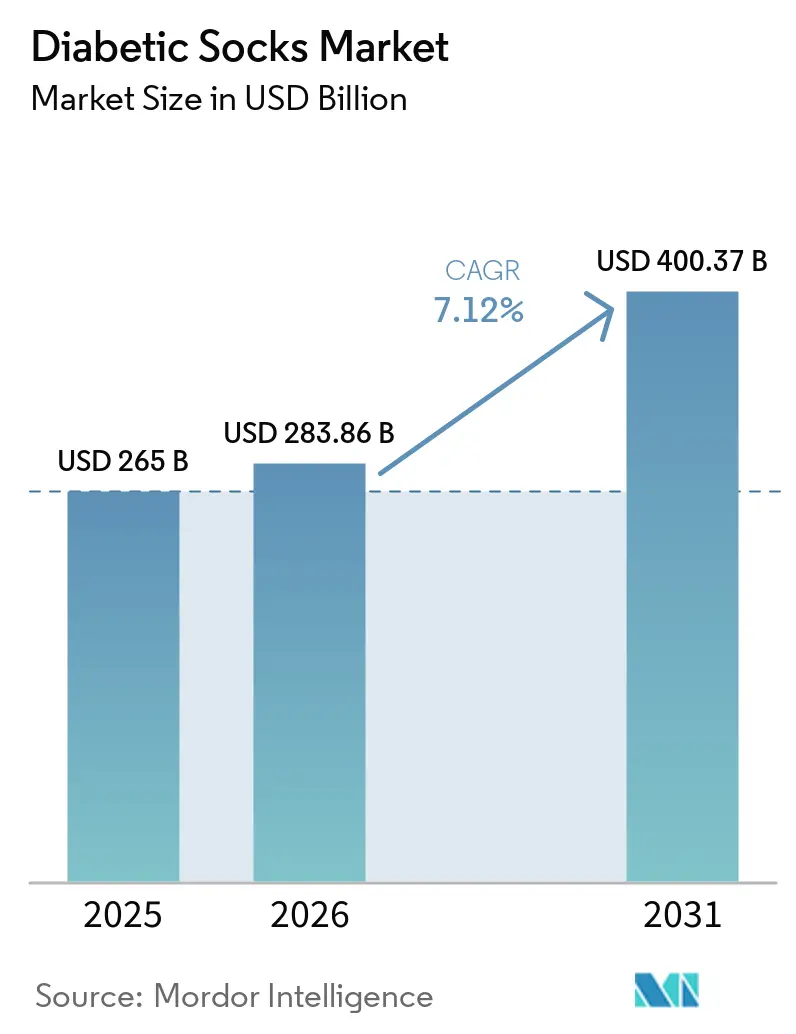

| Market Size (2026) | USD 283.86 Billion |

| Market Size (2031) | USD 400.37 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

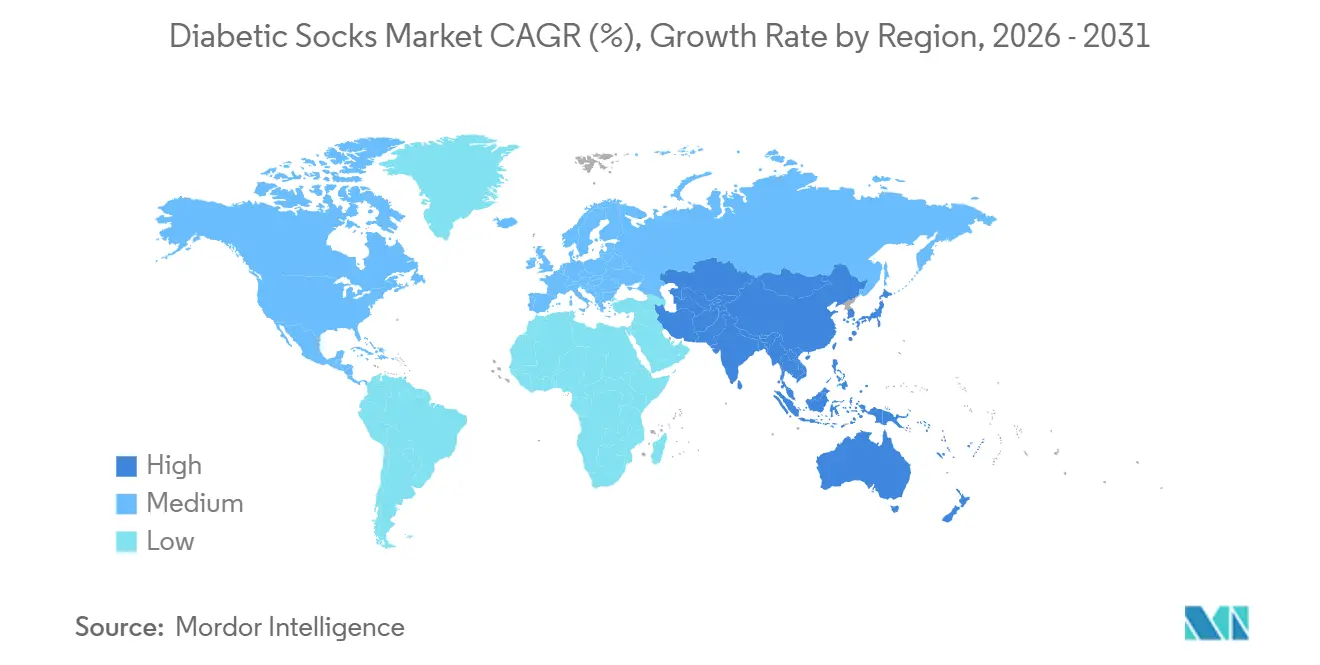

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

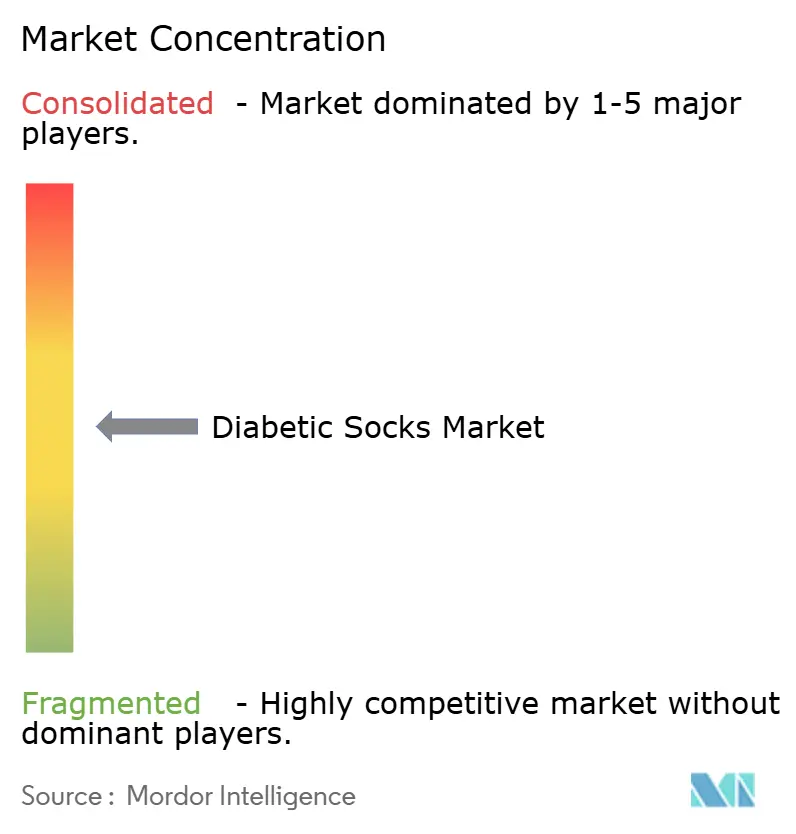

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Diabetic Socks Market Analysis by Mordor Intelligence

The Diabetic Socks Market size was valued at USD 265 billion in 2025 and is estimated to grow from USD 283.86 billion in 2026 to reach USD 400.37 billion by 2031, at a CAGR of 7.12% during the forecast period (2026-2031).

In 2024, the global diabetic population reached 589 million adults, with projections estimating growth to 853 million by 2050, driving consistent demand for preventive foot care.[1]International Diabetes Federation, “Diabetes Facts & Figures,” IDF Diabetes Atlas 11th Edition, idf.org Peripheral neuropathy, which reduces the ability to sense pressure and minor injuries, highlights the necessity of protective hosiery in routine care. North America leads the market due to high healthcare expenditure, structured diabetic foot care pathways, and strong reimbursement frameworks, ensuring these products are embedded in clinical use.

Key Report Takeaways

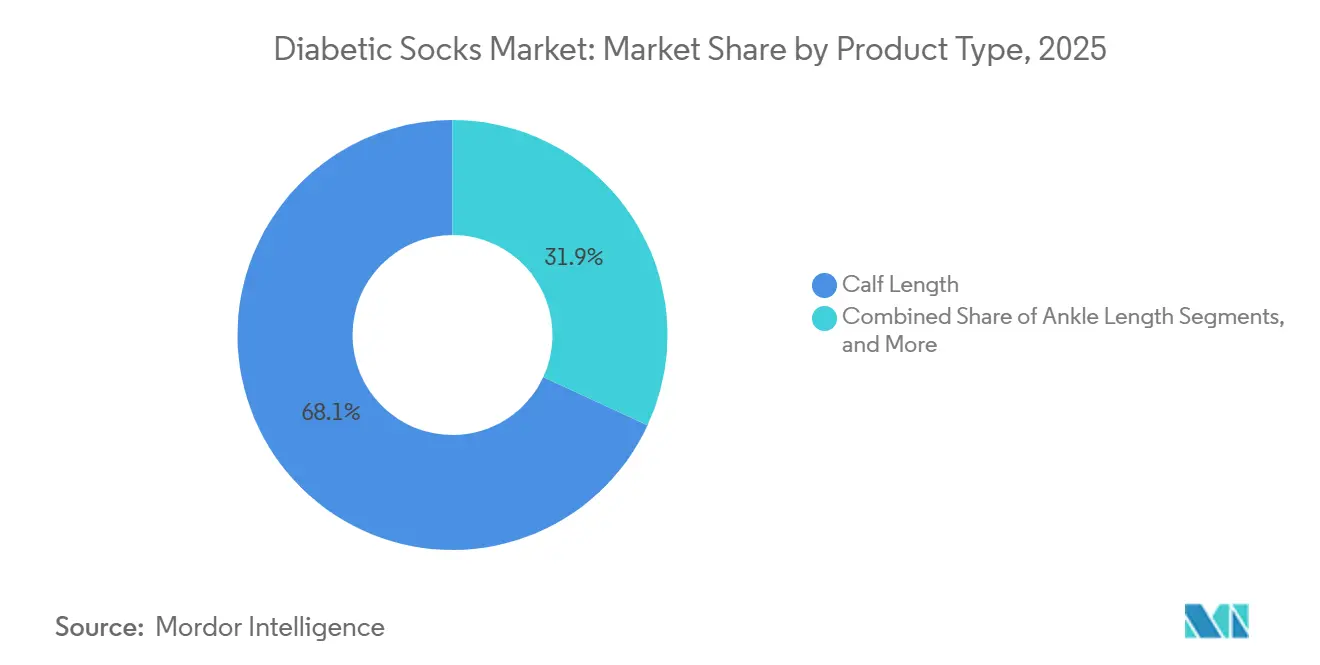

- By product type, calf length socks held 68.10% share in 2025, while ankle length socks are expected to expand at a 7.45% CAGR through 2031.

- By material, cotton accounted for 44.40% share in 2025, while bamboo-based materials are projected to grow at a 7.70% CAGR through 2031.

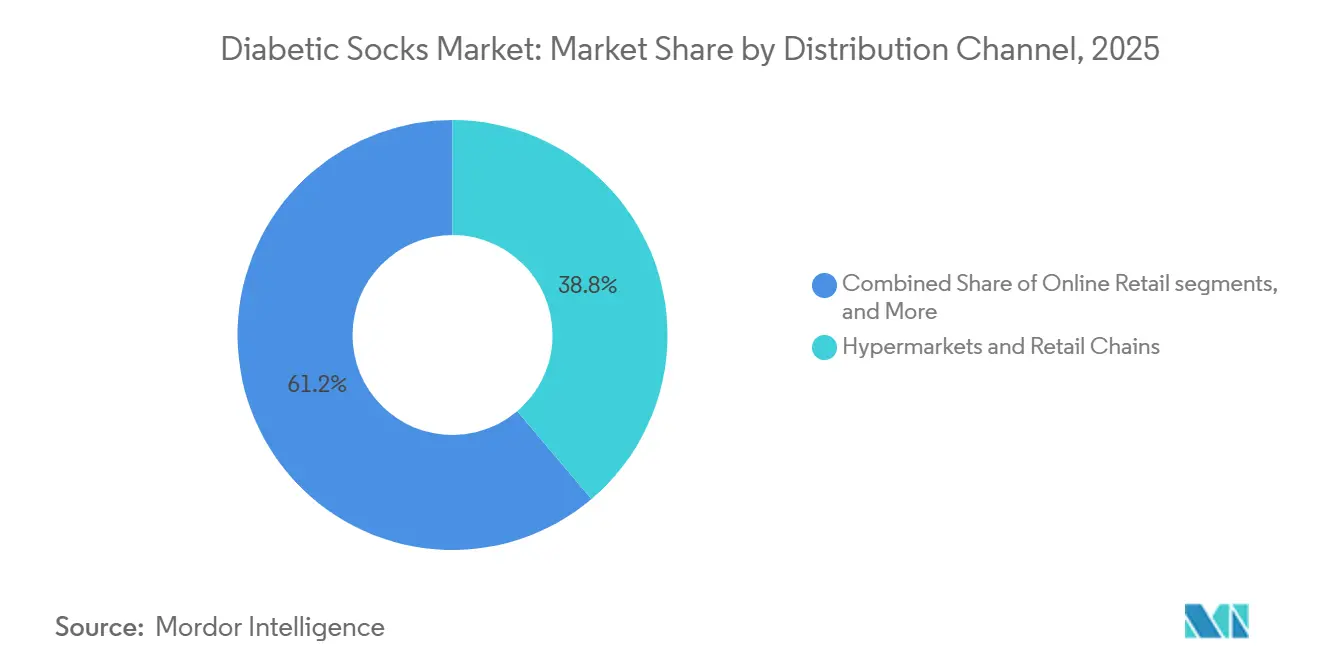

- By distribution channel, hypermarkets and retail chains held 38.77% share in 2025, while online retail is expected to grow at an 8.85% CAGR through 2031.

- By end user, unisex diabetic socks held 42.50% share in 2025 and also recorded the highest projected CAGR at 7.25% through 2031.

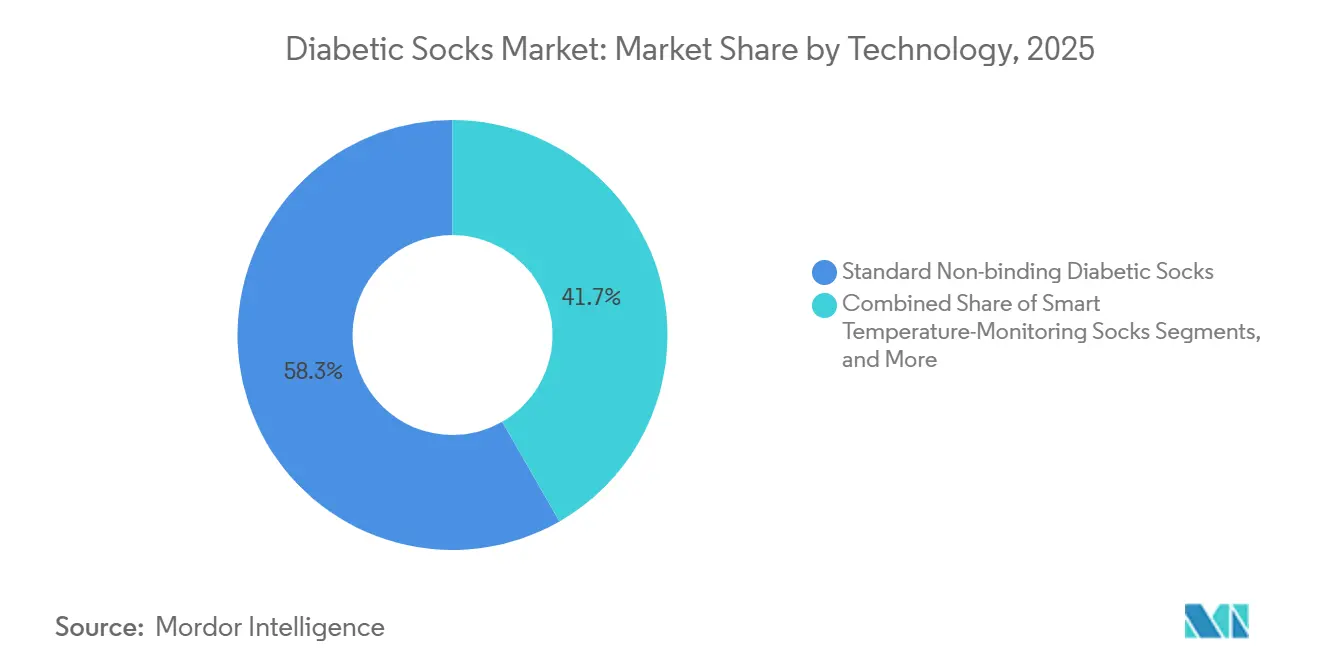

- By technology, standard non-binding socks held 58.34% share in 2025, while smart temperature-monitoring socks are projected to grow at a 9.02% CAGR through 2031.

- By geography, North America held 40.12% of the diabetic socks market share in 2025, while Asia-Pacific is projected to expand at a 9.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Diabetic Socks Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising diabetes prevalence and peripheral neuropathy | +2.1% | Global | Long term (≥ 4 years) |

| Greater clinical emphasis on ulcer prevention | +1.5% | North America & EU | Medium term (2-4 years) |

| Wider retail and e-commerce availability of diabetic socks | +1.2% | Global, APAC core, spill-over to MEA | Short term (≤ 2 years) |

| Reimbursed remote temperature-monitoring socks | +0.9% | North America | Medium term (2-4 years) |

| Fiber-engineered moisture and friction control | +0.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes Prevalence and Peripheral Neuropathy

The diabetic socks market is expanding due to the increasing global prevalence of diabetes. In 2024, 589 million adults were living with diabetes, a figure projected to reach 853 million by 2050, creating a growing demand for foot protection. Additionally, up to 50% of diabetes patients develop peripheral neuropathy, making friction-reducing and protective products essential for preventive care. Urban areas, with a 12.26% diabetes prevalence in 2024 compared to 9.23% in rural regions, enhance market accessibility through pharmacies, hospitals, and online platforms.[2]International Diabetes Federation, “Diabetes Facts & Figures,” IDF Diabetes Atlas 11th Edition, idf.org Painful diabetic neuropathy, affecting 46.7% of patients with diabetic peripheral neuropathy, further drives demand for protective socks.

Greater Clinical Emphasis on Ulcer Prevention

The market is benefiting from a stronger clinical focus on ulcer prevention rather than post-complication treatment. Temperature-sensing diabetic socks have demonstrated significant reductions in foot ulcers, amputations, and outpatient visits, elevating their role in structured podiatric and endocrinology workflows. Clinicians are increasingly incorporating these socks into early-intervention protocols, supported by evidence that strengthens reimbursement prospects. Brands like THORLO differentiate themselves with clinical studies showcasing reduced foot pain, blisters, and moisture, setting them apart from general retail alternatives.

Wider Retail and E-Commerce Availability of Diabetic Socks

Diabetic socks are now more accessible through expanded distribution channels, including online platforms and physical retail outlets. Online retail supports replenishment needs for these consumables, allowing patients to compare features conveniently. In regions with limited specialty medical retail, e-commerce serves as a primary access point. Physical retail, including hypermarkets and pharmacies, is also increasing visibility, encouraging routine purchases and driving consistent consumption in both developed and emerging markets.

Fiber-Engineered Moisture and Friction Control

Advancements in material design are driving the market, with a focus on moisture control, temperature regulation, and friction reduction. Bamboo viscose blends are gaining traction for their antimicrobial, thermal, and sustainable properties. Dual-layer olefin-based designs effectively manage sweat, creating a protective environment for patients at risk of skin issues. Copper-oxide embedded yarn ensures long-lasting antimicrobial performance, while Merino wool remains a preferred choice in colder climates due to its insulation and pressure-buffering properties.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Premium pricing versus ordinary socks | -1.2% | APAC, MEA, South America | Long term (≥ 4 years) |

| Limited awareness and physician recommendations | -0.7% | APAC core, MEA, with early gains in urban clusters | Medium term (2-4 years) |

| Guideline caution on compression or knee-high variants | -0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium Pricing Versus Ordinary Socks

The diabetic socks market faces affordability challenges in many regions, particularly where diabetes prevalence outpaces disposable income growth. Clinically designed socks are priced significantly higher than standard cotton alternatives, with premium brands ranging from USD 17 to USD 140, compared to basic options under USD 3. This disparity is critical as 81% of the global diabetic population resides in low- and middle-income countries with limited healthcare budgets. The cost gap is even wider for smart socks due to advanced features like temperature monitoring and connectivity. Without insurance or payer support, expanding premium and smart products to a broader audience remains challenging.

Limited Awareness and Physician Recommendations

The diabetic socks market grows slowly in regions with weak clinical recommendation pathways. The IDF Diabetes Atlas 2025 highlights that 43% of adults with diabetes, or 252 million people, remain undiagnosed, excluding a significant user base from healthcare systems.[3]International Diabetes Federation, “Diabetes Facts & Figures,” IDF Diabetes Atlas 11th Edition, idf.org Even diagnosed patients often lack consistent guidance on foot care and preventive footwear, especially in lower-income areas. Physician endorsements, a key driver for first-time purchases, are often absent. To address this, the market requires greater healthcare professional education in emerging regions. As foot-care standards become more formalized, specialist sock recommendations are expected to increase, though progress remains uneven across markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Calf Length Leads, Ankle Styles Drive Volume Expansion

In 2025, calf length socks dominated the diabetic socks market, accounting for 68.10% of the product type segment. Their mid-leg coverage offers protection without knee restriction, making them versatile for casual, medical, and orthopedic footwear. These socks address areas prone to rubbing and pressure, aligning with preventive foot-care needs, and remain the market's volume anchor due to their balance of protection, comfort, and daily wear compatibility.

Ankle length socks are the fastest-growing product type, projected to grow at a 7.45% CAGR from 2026 to 2031. Their appeal lies in catering to active users preferring athletic footwear and lighter coverage in warm weather. Over-the-calf and knee-high variants, while offering advanced features, face cautious adoption due to clinical concerns. Circufiber’s over-the-calf range addresses this by focusing on circulation support rather than compression, maintaining relevance in the market.

By Material: Cotton Dominates by Volume, Bamboo Leads on Functional Innovation

Cotton held 44.40% of the material segment in 2025, driven by its affordability, availability, and consumer familiarity. However, its clinical limitations, such as friction risks when wet, highlight the need for patient education on fiber choices as a health decision rather than a comfort preference.

Bamboo-based materials, with a forecasted 7.70% CAGR through 2031, are gaining traction for their antimicrobial, temperature-regulating, and sustainable properties, particularly in North America and Europe. Wool remains relevant in colder climates for insulation and pressure buffering, while acrylic and synthetic blends balance affordability and performance, ensuring their continued role in the market.

By Distribution Channel: Hypermarkets Lead, Online Retail Reshapes the Access Model

Hypermarkets and retail chains led the distribution channel mix in 2025 with a 38.77% share, benefiting from high visibility, foot traffic, and strategic placement near diabetes-care products. This format supports convenience and compliance by integrating purchases into routine care shopping.

Online retail, growing at an 8.85% CAGR through 2031, is reshaping access by offering repeat purchase options, detailed product insights, and broader availability. In regions with limited specialty medical retail, e-commerce serves as a primary access point, while pharmacies and specialty stores remain relevant for products requiring clinical guidance or fitting support.

By End User: Unisex Designs Anchor Both Volume and Growth

Unisex diabetic socks held 42.50% of the end-user segment in 2025 and are projected to grow at a 7.25% CAGR through 2031. Their practicality simplifies manufacturing, retail planning, and institutional procurement, making them the default choice across supply channels.

Male-specific socks remain significant due to higher diabetes prevalence among men and delayed podiatric care, while female-specific ranges cater to design and fit preferences, especially in urban markets. Brands continue to balance unisex efficiency with tailored options for gender-specific needs.

By Technology: Standard Non-binding Anchors Volume, Smart Monitoring Drives Strategy

Standard non-binding diabetic socks led the technology segment in 2025 with a 58.34% share, driven by their alignment with core diabetic foot care needs. However, competition is intensifying, shifting differentiation toward materials and clinical credibility.

Smart temperature-monitoring socks, projected to grow at a 9.02% CAGR through 2031, represent a key growth area, offering advanced risk identification features. Compression socks remain relevant in prescription-led segments, while antimicrobial and copper-infused products differentiate on hygiene and skin protection.

Geography Analysis

In 2025, North America led the diabetic socks market with a 40.12% share, driven by high diabetes prevalence, strong healthcare spending, and structured clinical pathways for diabetic foot care. CMS coverage for diabetic therapeutic shoes and related supplies under specific eligibility criteria has facilitated the transition of diabetic socks from retail interest to medically supported use. Additionally, the region's early adoption of connected products, such as smart socks, aligns with its care delivery and payer systems, reinforcing its market leadership.

Europe, led by Germany, the United Kingdom, France, Italy, and Spain, is another key player in the diabetic socks market. National health systems and referral pathways streamline the integration of diabetic foot products into routine care. Germany's strong adoption of compression hosiery supports established players like Jacob Rohner AG and Thuasne LLC through pharmacy and hospital channels. Sustainability is also becoming a differentiator, with companies like SIGVARIS GROUP France introducing waterless-dyed compression stockings and reducing water consumption in product lines, blending clinical and environmental priorities.

Asia-Pacific is the fastest-growing region in the diabetic socks market, projected to grow at a 9.35% CAGR through 2031. China and India, with a combined diabetic adult population exceeding 200 million in 2024, provide a strong volume base. However, uneven reimbursement and physician recommendations across countries highlight the need for diverse growth strategies. Online channels are bridging gaps in specialty retail infrastructure, while Japan stands out for its early adoption of advanced healthcare products and structured retail distribution. Orthofeet’s distributor in Japan expanded to over 80 retail outlets by fall 2025, reflecting international brands' growing presence in the region.

Competitive Landscape

The diabetic socks market is moderately fragmented, with competition structured into three tiers. Established compression-textile specialists like SIGVARIS GROUP, Jacob Rohner AG, and Thuasne LLC focus on clinical reputation, regulatory compliance, and established access to pharmacy and hospital channels. Technology-driven firms are advancing the market toward monitored care by integrating connected temperature sensing, transforming hosiery into preventive tools.

Recent strategic developments highlight that partnerships and product differentiation are driving the diabetic socks market. In January 2025, Mölnlycke Health Care invested USD 8 million in Siren, combining temperature-sensing textile technology with its clinical network and distribution. In April 2025, SIGVARIS GROUP France introduced a waterless-dyed compression stocking, reducing water usage by 90%, showcasing sustainability as a competitive strategy. THORLO continues to differentiate through peer-reviewed clinical evidence for its diabetic range, emphasizing capability building over broader product listings.

White-space opportunities in the diabetic socks market indicate areas for future competition. These include affordable smart monitoring products for price-sensitive Asia-Pacific markets with high clinical needs but limited reimbursement, and bamboo-based antimicrobial premium products in developed markets where sustainability supports premium pricing. Gender-specific clinical lines for women in emerging urban markets also remain untapped, as fit, comfort, and appearance influence compliance. Entry barriers in the smart-sock segment are rising due to stringent regulatory and clinical evidence requirements, favoring firms capable of managing extended development cycles. This dynamic fosters innovation while protecting established players with strong distribution, credibility, and regulatory readiness.

Diabetic Socks Industry Leaders

SIGVARIS GROUP

Dr. Comfort, LLC

THORLO, Inc.

Simcan Enterprises Inc.

Essity Aktiebolag

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Professors Neil Reeves, Moi Hoon Yap, and Katie Chatwin co-developed "FootSnap-AI," an app paired with a smart sock featuring sensors to measure friction and provide AI-powered foot screenings.

- November 2025: MYNERVA, an ETH Zurich spin-off, launched "Leia," a smart sock with electrodes that restore foot sensation, reduce chronic pain, and block pain signals via nerve stimulation.

- April 2025: SIGVARIS GROUP France introduced its first waterless-dyed compression stocking under the Dynaven Fin medical compression range, reducing water usage by 90%.

- January 2025: Mölnlycke Health Care invested USD 8 million in Siren to advance temperature-sensing textile technology for early detection of diabetic foot ulcer risks.

Global Diabetic Socks Market Report Scope

As per the scope of the report, a diabetic sock is a specially engineered non-restrictive garment designed to protect sensitive feet and reduce the risk of foot injuries, infections, and ulcers. People with diabetes face a higher risk of peripheral neuropathy (nerve damage causing numbness) and vascular disease (poor blood circulation).

The diabetic socks market is segmented by product type, material, distribution channel, end-user, technology, and geography. By product type, the market includes ankle length, calf length, and over-the-calf/knee-high socks. By material, the market is segmented into cotton, bamboo, wool, acrylic, and synthetic blends. By distribution channel, the market is categorized into hypermarkets and retail chains, pharmacy and drug stores, online retail, and specialty medical stores. By end-user, the market is segmented into male, female, and unisex. By technology, the market includes standard non-binding diabetic socks, compression diabetic socks, antimicrobial/copper-infused diabetic socks, smart temperature-monitoring socks, and infrared/circulation-enhancing socks. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Ankle Length |

| Calf Length |

| Over-the-calf / Knee-high |

| Cotton |

| Bamboo |

| Wool |

| Acrylic |

| Synthetic Blends |

| Hypermarkets and Retail Chains |

| Pharmacy and Drug Stores |

| Online Retail |

| Specialty Medical Stores |

| Male |

| Female |

| Unisex |

| Standard Non-binding Diabetic Socks |

| Compression Diabetic Socks |

| Antimicrobial / Copper-Infused Diabetic Socks |

| Smart Temperature-Monitoring Socks |

| Infrared / Circulation-Enhancing Socks |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | Saudi Arabia | |

| By Product Type | Ankle Length | ||

| Calf Length | |||

| Over-the-calf / Knee-high | |||

| By Material | Cotton | ||

| Bamboo | |||

| Wool | |||

| Acrylic | |||

| Synthetic Blends | |||

| By Distribution Channel | Hypermarkets and Retail Chains | ||

| Pharmacy and Drug Stores | |||

| Online Retail | |||

| Specialty Medical Stores | |||

| By End User | Male | ||

| Female | |||

| Unisex | |||

| By Technology | Standard Non-binding Diabetic Socks | ||

| Compression Diabetic Socks | |||

| Antimicrobial / Copper-Infused Diabetic Socks | |||

| Smart Temperature-Monitoring Socks | |||

| Infrared / Circulation-Enhancing Socks | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | Saudi Arabia | ||

Key Questions Answered in the Report

What is the current size of the diabetic socks market?

The diabetic socks market stands at USD 283.86 billion in 2026 and is forecast to reach USD 400.37 billion by 2031 at a CAGR of 7.12%.

Which region leads diabetic socks demand?

North America leads with 40.12% share in 2025, supported by stronger reimbursement, higher healthcare spending, and established diabetic foot-care pathways.

Which region is growing the fastest through 2031?

Asia-Pacific is the fastest-growing region with a 9.35% CAGR, supported by very large diabetic populations in China and India and wider access through digital channels.

Which product category is the largest?

Calf length socks lead product demand with 68.10% share in 2025 because they balance coverage, comfort, and clinical suitability for routine use.

What is driving adoption of smart diabetic socks?

Smart temperature-monitoring socks are growing at a 9.02% CAGR because they support early intervention and have shown strong outcomes in reducing ulcers and amputations in high-risk patients.

What is the biggest challenge for broader adoption?

Premium pricing remains a major barrier, especially in low- and middle-income countries where most adults with diabetes live and reimbursement for advanced products is limited.

Page last updated on: