Sugar-Free Food And Beverage Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 72.98 Billion |

| Market Size (2031) | USD 107.94 Billion |

| Growth Rate (2026 - 2031) | 8.15% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sugar-Free Food And Beverage Market Analysis by Mordor Intelligence

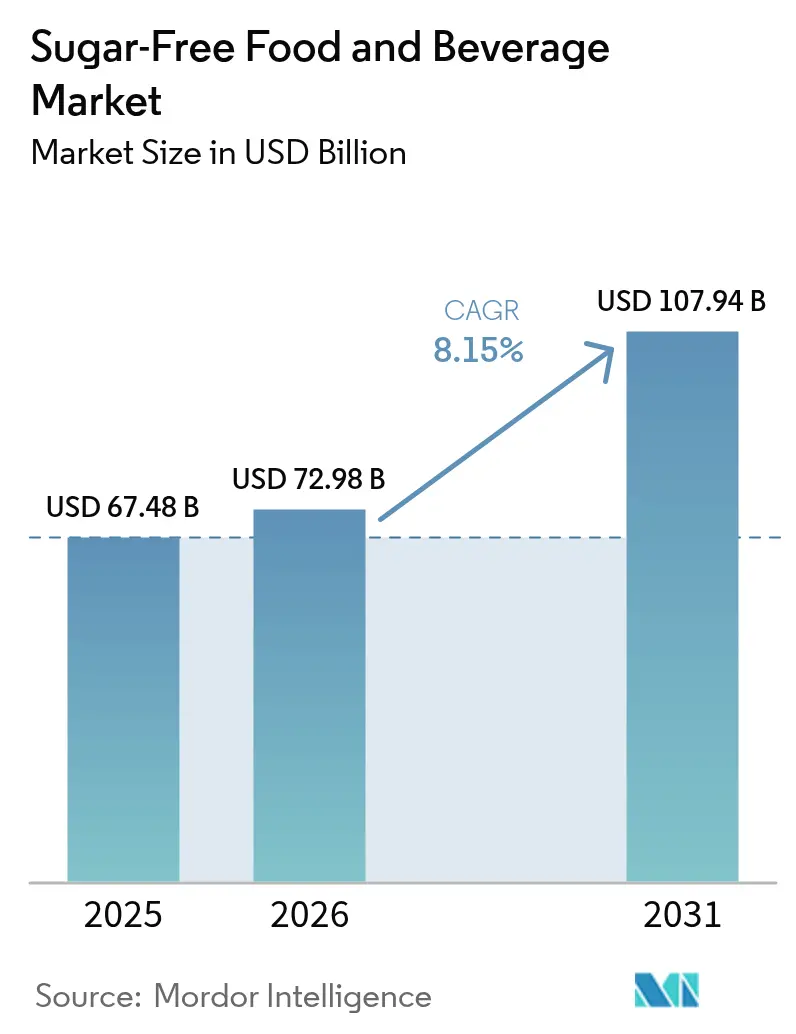

The sugar-free food and beverages market size is expected to grow from USD 67.48 billion in 2025 to USD 72.98 billion in 2026 and is forecast to reach USD 107.94 billion by 2031 at 8.15% CAGR over 2026-2031. Ongoing diabetes escalation, wider adoption of fiscal sugar controls, and continuous ingredient innovation drive this upward trajectory. Beverage reformulations remain vigorous as 54 nations deploy sugar taxes that favor zero-calorie recipes and spur portfolio diversification. Personal nutrition technology[1]World Obesity Federation. "Sugar-Sweetened Beverage Tax: case studies." March 9, 2024. https://www.worldobesity.org/resources/policy-dossiers/pd-1/case-studies., especially continuous glucose monitors linked to diet apps, brings new product personalization pathways. Governments also accelerate approvals for natural high-intensity sweeteners, lowering development risks and attracting fresh capital. Meanwhile, retailers enlarge private-label ranges, leveraging trust and aggressive shelf pricing to expand value creation across every demographic pocket.

Key Report Takeaways

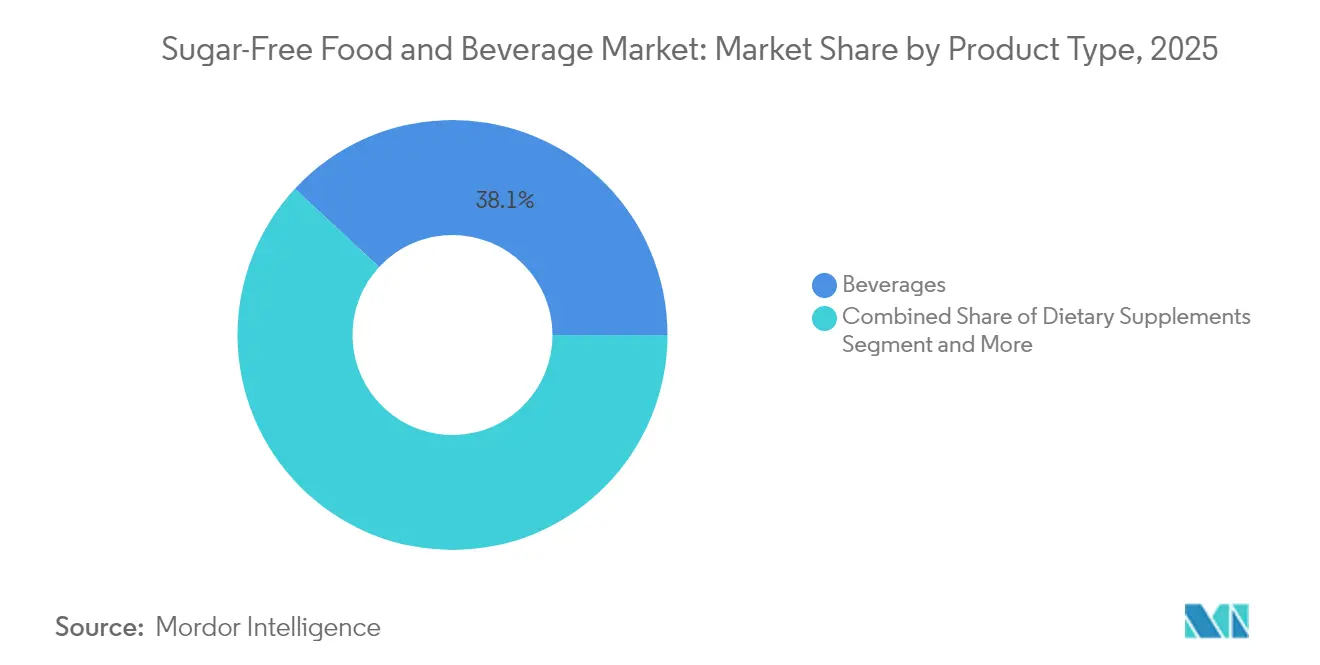

- By product category, beverages held 38.10% of the sugar-free food and beverages market share in 2025; dietary supplements recorded the fastest expansion at a 7.08% CAGR to 2031.

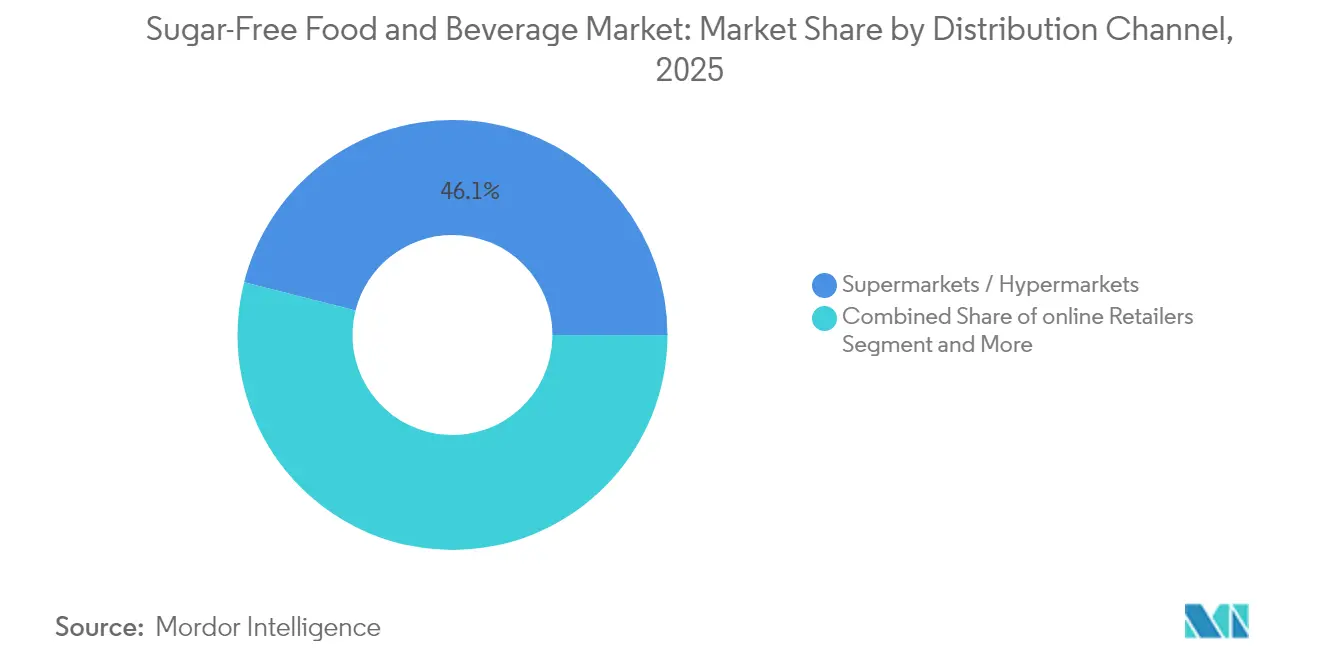

- By distribution channel, supermarkets and hypermarkets captured 46.05% of the sugar-free food and beverages market size in 2025, while online retail advances at an 11.12% CAGR through 2031.

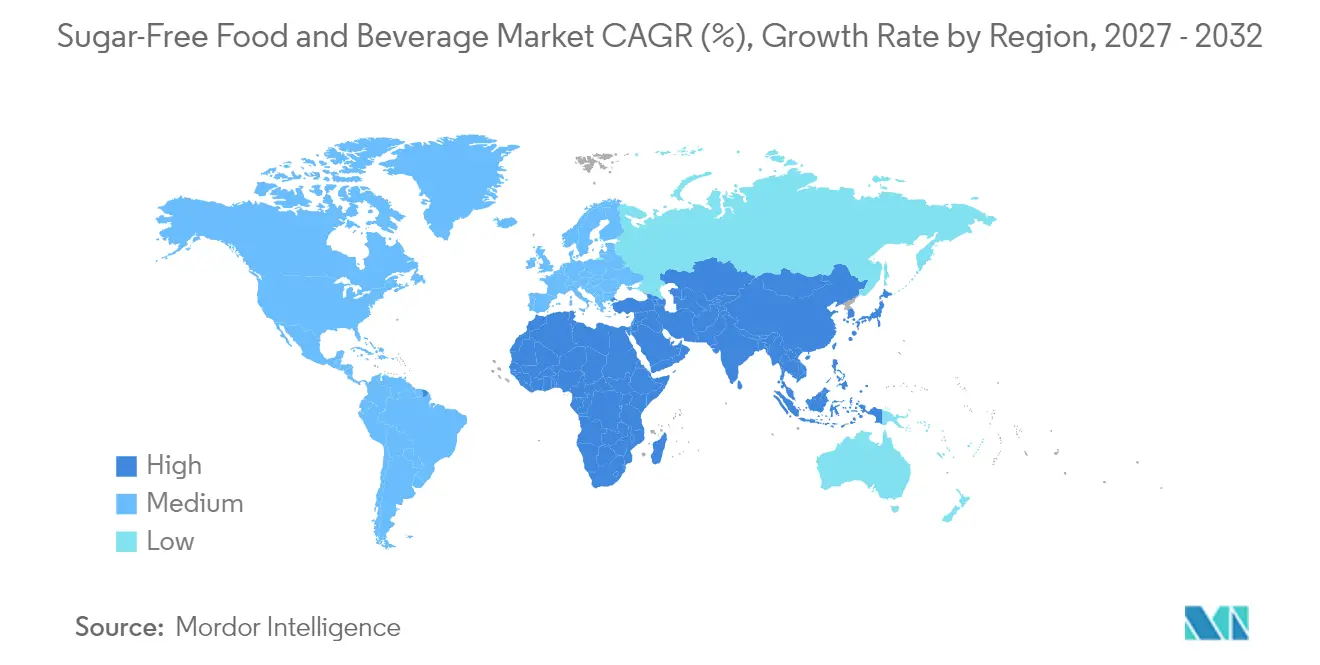

- By geography, North America led with a 32.05% share of the sugar-free food and beverages market size in 2025; Asia-Pacific is advancing at an 8.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sugar-Free Food And Beverage Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Diabetes & obesity prevalence fuels demand | +2.1% | Global, with highest impact in APAC and North America | Long term (≥ 4 years) |

| Global sugar-tax legislation accelerates reformulations | +1.8% | Global, with 54 countries implementing policies | Medium term (2-4 years) |

| Continuous product innovation in natural high-intensity sweeteners | +1.3% | North America & EU leading, expanding to APAC | Medium term (2-4 years) |

| Retailer private-label expansion in sugar-free SKUs | +0.9% | North America & Europe primarily | Short term (≤ 2 years) |

| Wearable CGM-driven dietary personalization | +0.7% | North America and developed APAC markets | Long term (≥ 4 years) |

| AI-driven e-commerce merchandising for low-sugar products | +0.5% | Global, concentrated in digitally mature markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Diabetes & Obesity Prevalence Fuels Demand

World diabetes cases have quadrupled since 1990 and now exceed 800 million adults, firmly embedding sugar reduction within public health priorities. Population-wide dietary interventions rank high in national action plans as the economic burden of metabolic disorders climbs. In the Asia-Pacific region, forward projections indicate 1.31 billion diabetes cases by 2050, keeping demand for sugar-free alternatives resilient even during economic cycles. Employers and insurers increasingly subsidize low-sugar meals in cafeterias and wellness programs to mitigate productivity losses. Low- and middle-income economies will host nearly 79% of global obesity by 2035, expanding the target consumer base for accessible formulations[2]Arabic Association for the Study of Diabetes and Metabolism. "Dietary recommendations for people with diabetes in special situations: a position statement report by Arabic Association for the Study of Diabetes and metabolism (AASD)." Journal of Health, Population and Nutrition 43 (2024): 139. https://doi.org/10.1186/s41043-024-00619-y.. This demographic momentum, combined with a structural shift toward preventive care, guarantees enduring demand across all income brackets.

Global Sugar-Tax Legislation Accelerates Reformulations

Sugar-sweetened beverage levies install a clear financial incentive for manufacturers to reformulate existing recipes rather than pay higher tax rates. The U.K. Soft Drinks Industry Levy triggered a 43.7% reduction in average sugar per liter across taxed beverages, while South Africa’s Health Promotion Levy drove a 29% fall in fizzy drink purchases. Mexico’s decade-old excise tax continues to deliver a 37% volume decline, demonstrating durable public health gains. Yet only seven of 19 MENA economies have adopted similar laws, highlighting untapped legislative white space. As more nations refine levy structures to penalize sugar grams rather than volume alone, reformulation races quicken and multinational firms streamline global ingredient standards to avoid multi-jurisdictional complexity.

Continuous Product Innovation in Natural High-Intensity Sweeteners

Regulatory green lights for novel sweeteners widen formulation toolkits and help brands answer clean-label expectations. Australia and New Zealand approved D-allulose in August 2024, cementing an Oceania staging ground for broader Asia rollouts. The European Food Safety Authority is evaluating monk fruit extract and has already endorsed several new stevia fractions, signaling growing openness to plant-derived sweetness[3]European Food Safety Authority. "Safety of D‐allulose as a novel food pursuant to Regulation (EU) 2015/2283." June 1, 2025. https://efsa.onlinelibrary.wiley.com/doi/10.2903/j.efsa.2025.9468.. Enzymatic bioconversion lowers production costs for rebaudioside D and M, improving flavor profiles close to sucrose without bitterness. Lower input expense, combined with scale efficiencies, narrows the historic price premium that limited adoption in mainstream categories.

Retailer Private-Label Expansion in Sugar-Free SKUs

Major supermarket chains deploy dedicated “better-for-you” aisles that spotlight store-brand sugar-free snacks, beverages, and bakery mixes. Private-label margins often eclipse branded lines by 300–400 basis points, encouraging retailers to fund in-house R&D teams and rapid sensory testing pipelines. Consumer trust rises as retailers back quality claims with loyalty-card discounts and digital nutrition scorecards. Quick procurement cycles mean private-label ranges react faster to ingredient breakthroughs, compelling national brands to intensify innovation cadence to preserve shelf presence. This dynamic fosters an iterative race that widens assortment choice, especially among shoppers who seek value without sacrificing perceived health benefits.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing versus sugared counterparts | -1.4% | Global, with highest impact in price-sensitive emerging markets | Medium term (2-4 years) |

| Clean-label backlash against some artificial sweeteners | -0.8% | North America & Europe primarily | Short term (≤ 2 years) |

| Supply volatility of rare plant-based sweeteners | -0.6% | Global, concentrated in natural sweetener segments | Medium term (2-4 years) |

| Sensory "flavor fatigue" limiting repeat purchases | -0.4% | Global, varies by product category | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Pricing Versus Sugared Counterparts

Sugar-free recipes still command 15–30% shelf premiums because alternative sweeteners need specialized processing lines, smaller batch runs, and stringent compliance protocols. Macroeconomic headwinds, especially currency swings in emerging markets, amplify sticker shocks relative to subsidized conventional products. Price-elastic demographic cohorts hesitate to trial sugar-free options when household budgets tighten, stalling penetration in lower middle-income segments. Manufacturers must either scale volumes or co-invest with retail partners in value packs to soften cost barriers.

Clean-Label Backlash Against Some Artificial Sweeteners

Consumer sentiment pivots quickly when viral posts question the safety of specific artificial sweeteners, even when scientific consensus affirms their use. Brands reliant on sucralose or aspartame face periodic sales dips until narrative control is regained through transparent sourcing and third-party validations. The upcoming Dietary Guidelines for Americans 2025 edition will target zero added sugars, which could intensify scrutiny of all non-nutritive sweeteners and pressure reformulation roadmaps. Companies diversify ingredient stacks to hedge against sudden sentiment shifts, raising development costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Beverages Retain Leadership While Supplements Scale Quickly

Beverages accounted for 38.10% of the sugar-free food and beverages market share in 2025, buoyed by aggressive reformulations triggered by national sugar levies that penalize excess grams rather than total volume. Flagship cola brands extend zero-sugar variants into seasonal flavor drops, sustaining double-digit volume gains that illustrate sustained mass acceptance. Ready-to-drink teas and enhanced waters add incremental shelf presence, leveraging clean-label botanicals and nootropic claims that complement sugar elimination goals. The segment’s robust cold-chain infrastructure and established promotional calendars ease nationwide rollouts, tightening incumbent moats. In 2025, beverages added USD 2.6 billion to overall category value, validating a strategic focus on flavor innovations over entirely new sub-categories.

Dietary supplements recorded the highest 7.08% CAGR through 2031, fueled by clinician endorsements that position sugar-free formulations as adjunct tools for glycemic modulation. Functional powders fortified with chromium, zinc, and plant polyphenols accelerate mainstream uptake among gym-goers aiming for metabolic flexibility. Partnerships with CGM manufacturers enable digital bundle offers that align supplement dosage reminders with glucose alerts. Although volumes remain smaller, average unit prices are triple those of beverages, lifting segment profitability. Rapid soft-gel format adaptations further expand addressable demographics, including elderly consumers seeking easy ingestion solutions. Manufacturers collaborate with medical associations to secure endorsement seals, amplifying credibility and shelf pull.

By Distribution Channel: Supermarkets Dominate While Online Retail Surges

Supermarkets and hypermarkets controlled 46.05% of the sugar-free food and beverages market size in 2025, capitalizing on expansive end-cap displays and in-store tastings that educate shoppers on flavor parity with sugared counterparts. Dual placement—main aisles and dedicated health sections—maximizes visibility, while loyalty-card analytics feed real-time coupon personalization for sugar-free SKUs. Promotional tie-ins with community health screenings reinforce retailer authority in wellness merchandising. As inflation moderates, shoppers flock back to physical stores for bulk buys, sustaining foot traffic that benefits impulse trial of innovative low-sugar snacks. Yet shelf competition intensifies as private-label ranges proliferate, squeezing secondary brands unless they secure themed gondola deals.

Online retail, advancing at an 11.12% CAGR, thrives on algorithmic cross-selling that aligns sugar-free purchases with self-reported health objectives inside app profiles. Filter tools that isolate “no added sugar” tags compress search friction and boost basket share. Subscription models offering regular shipment of staple items like tabletop sweeteners and meal-replacement shakes elevate lifetime customer value. Seamless mobile payments and same-day delivery in urban zones remove historic barriers for frozen and chilled sugar-free goods, encouraging experimentation beyond ambient categories. Online marketplaces also democratize entry for micro-brands that rely on influencer marketing and limited direct-to-consumer runs, diversifying the overall product landscape.

Geography Analysis

In 2025, North America led the sugar-free food and beverages market with a 32.05% share, driven by mature regulatory frameworks, widespread product familiarity, and insurance-supported nutrition counseling that promotes sugar avoidance. Retailers distinctly segment artificial and natural sweetener products, enabling targeted promotions for specific consumer groups. Sustainable packaging initiatives by regional suppliers align with eco-conscious consumer values, justifying premium pricing. Additionally, the U.S.-Mexico-Canada Agreement has simplified labeling for zero-sugar claims, streamlining tri-national logistics. Meanwhile, Asia-Pacific recorded the fastest growth with an 8.62% CAGR projected through 2031. Rising urbanization and middle-class incomes are fueling demand for premium sugar-free products, including confectionery and dairy alternatives. Programs like Singapore’s Nutri-Grade, which links sugar thresholds to colored labels, are encouraging manufacturers to reformulate products for favorable ratings. China’s "Healthy China" plan signals stricter sugar regulations, while localized flavor innovations, such as monk fruit beverages in China and stevia-sweetened yuzu tonics in Japan, enhance cultural relevance and address taste concerns.

Europe maintains steady mid-single-digit growth, supported by EFSA’s stringent approval protocols that build consumer trust in sweetener claims. The region’s push for front-of-pack traffic-light labeling is steering consumers toward healthier, low-sugar options. In South America, sugar taxation is gaining momentum, with Brazil considering a tiered levy inspired by Mexico’s model, which could accelerate reformulations. In the Middle East and Africa, increasing awareness of non-communicable diseases, combined with low taxation coverage, presents an opportunity for policy changes that could boost market value. These regional dynamics collectively highlight the evolving landscape of the global sugar-free food and beverages market.

Competitive Landscape

The sector, with a concentration index of 4 out of 10, reflects moderate fragmentation, balancing competition between global leaders and agile challengers. Coca-Cola capitalizes on its distribution network to promote Zero Sugar extensions across sparkling, sports, and mixer lines, supported by a 65% shift to digital advertising targeting health-conscious micro-segments. PepsiCo expands its zero-sugar offerings in key franchises like Mountain Dew and Gatorade, focusing on flavor parity to address trial hesitations. Mars's USD 35.9 billion acquisition of Kellanova highlights a strategic pivot toward healthier snacking, integrating bar and cereal brands with its chocolate portfolio to enhance R&D synergies. Emerging brands, such as Zevia, leverage natural sweeteners and eco-friendly sourcing to attract Millennials and Gen Z, with Zevia surpassing 1.9 billion cans sold using stevia and monk fruit. Private-label brands add pricing pressure but maintain category momentum through high rotation rates and frequent flavor updates. Additionally, Abbott's partnership linking its FreeStyle Libre CGM with Medtronic’s insulin pumps strengthens brand loyalty by connecting medical devices with dietary products.

Rising ingredient regulations are increasing barriers to entry, as novel sweeteners require extensive safety dossiers and multi-year investments, favoring established players with regulatory expertise. However, multinationals are fostering innovation by hosting contests that allow start-ups to pitch functional sweetening technologies, offering opportunities for niche disruptors to scale globally through licensing. These dynamics, combined with the sector's focus on health-driven innovation and technological integration, are shaping the competitive landscape and driving growth across key markets.

Sugar-Free Food And Beverage Industry Leaders

-

The Coca-Cola Company

-

PepsiCo Inc.

-

Nestlé S.A.

-

Mondelēz International Inc.

-

Mars Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Starbucks has officially launched its new “Sugar-free Flavours” syrups in China, allowing customers to enjoy popular drinks like hazelnut lattes and mixed berry Americanos with all the flavor but no added sugar.

- February 2025: The Coca‑Cola Company launched Simply Pop, its first-ever prebiotic soda. Made with real fruit juice concentrate, no added sugar, and sweetened naturally with monk fruit extract, Simply Pop supports gut health with 6 grams of prebiotic fiber and boosts immunity with Vitamin C and Zinc.

- March 2024: Volvic launched its newest creation, Touch of Fruit Sparkling Sugar Free, made with British spring water. In addition to this fresh product release, Volvic also revamped its Touch of Fruit till range to further entice consumers to explore the flavored water selection.

Global Sugar-Free Food And Beverage Market Report Scope

Sugar-free food and beverages are food products that contain no added sugars. According to the FDA, sugar-free foods are foods that have less than half a gram of added or naturally occurring sugar. The sugar-free food and beverage market is segmented into product type, distribution channel, and geography. The market is segmented by product type into beverages, dairy and dairy alternatives, confectionery, bakery products, dietary supplements, and other product types. Based on the distribution channel, the market can be segmented into supermarkets/hypermarkets, convenience stores, pharmacies/drug stores, online retail stores, and other distribution channels. Furthermore, the market is segmented based on geography worldwide, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizes and forecasts are offered on the basis of value (USD).

| Beverages | Carbonated Soft Drinks |

| Functional Drinks | |

| Juices & RTD Tea / Coffee | |

| Dairy & Dairy Alternatives | Milk Drinks |

| Yogurt | |

| Ice Cream | |

| Confectionery | Chocolate |

| Gum & Mints | |

| Bakery Products | |

| Dietary Supplements | |

| Savory Snacks | |

| Others |

| Supermarkets / Hypermarkets |

| Convenience & Grocery Stores |

| Specialty Health and Wellness Stores |

| Online Retail |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East & Africa | Saudi Arabia |

| South Africa | |

| UAE | |

| Rest of MEA |

| By Product Type | Beverages | Carbonated Soft Drinks |

| Functional Drinks | ||

| Juices & RTD Tea / Coffee | ||

| Dairy & Dairy Alternatives | Milk Drinks | |

| Yogurt | ||

| Ice Cream | ||

| Confectionery | Chocolate | |

| Gum & Mints | ||

| Bakery Products | ||

| Dietary Supplements | ||

| Savory Snacks | ||

| Others | ||

| By Distribution Channel | Supermarkets / Hypermarkets | |

| Convenience & Grocery Stores | ||

| Specialty Health and Wellness Stores | ||

| Online Retail | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East & Africa | Saudi Arabia | |

| South Africa | ||

| UAE | ||

| Rest of MEA | ||

Key Questions Answered in the Report

How large is the sugar-free food and beverages market in 2026?

The category is valued at USD 72.98 billion in 2026 with an 8.15% CAGR outlook to 2031.

Which product segment leads sales?

Beverages hold the top position with 38.10% share of 2025 revenue.

Which region is expanding fastest?

Asia-Pacific posts the highest growth at 8.62% CAGR through 2031 as health policies and incomes rise.

What drives consumer demand for sugar-free products?

Rising diabetes prevalence, sugar taxes, and advances in natural sweeteners sustain demand momentum.

How are retailers supporting market growth?

Supermarkets expand private-label ranges and deploy data-driven promotions, while online platforms personalize recommendations and subscription models.

Page last updated on: