Dairy Processing Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

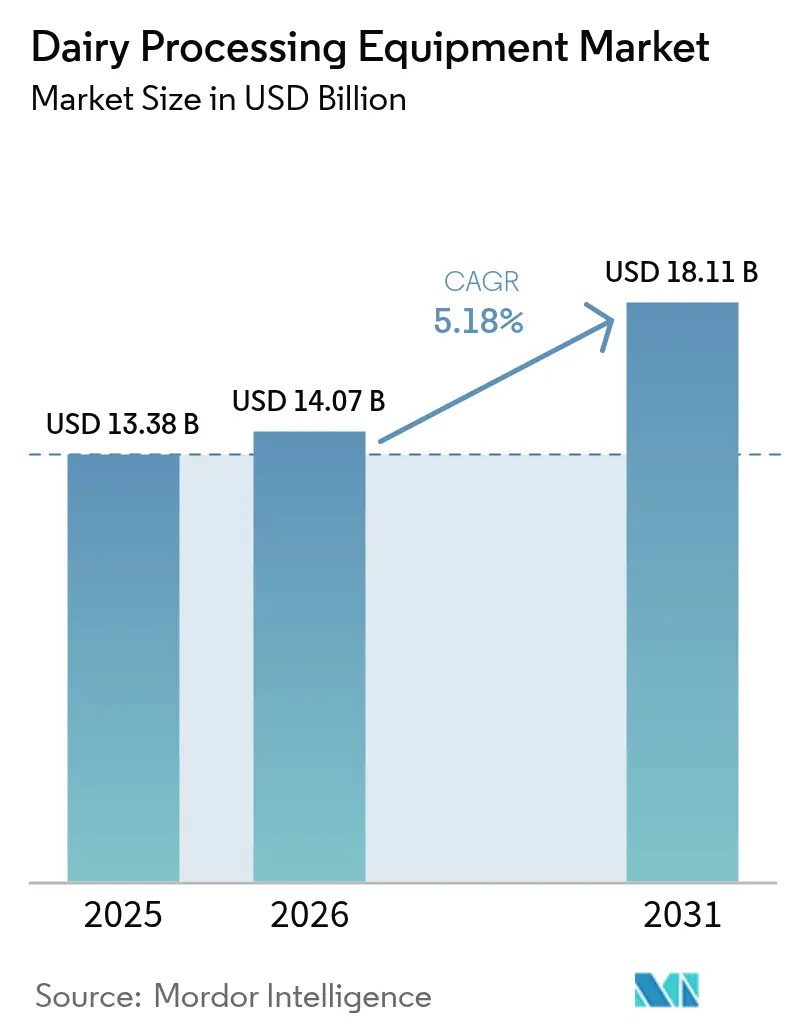

| Market Size (2026) | USD 14.07 Billion |

| Market Size (2031) | USD 18.11 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dairy Processing Equipment Market Analysis by Mordor Intelligence

The dairy processing equipment market size was valued at USD 13.38 billion in 2025 and estimated to grow from USD 14.07 billion in 2026 to reach USD 18.11 billion by 2031, at a CAGR of 5.18% during the forecast period (2026-2031). This growth is driven by a consistent consumer demand for packaged milk, cheese, and functional ingredients. Additionally, there's a push for stricter food-safety measures and a rise in automation across processing lines. Modernization efforts, like the USDA's Dairy Business Innovation Initiatives, are accelerating plant upgrades. Simultaneously, the FDA's 2023 Pasteurized Milk Ordinance (PMO) is prompting systematic equipment overhauls. Agencies such as Natural Resources Canada are emphasizing energy efficiency, directing funds towards technologies like membrane filtration, heat pumps, and cogeneration. These not only reduce emissions but also cut utility costs. To stay competitive, players are focusing on integrated solutions that prioritize compliance, sanitary design, and digital monitoring, all while aiming for reduced operational costs. This strategy aligns with the regulatory and sustainability trends that are set to shape the dairy processing equipment market until 2030.

Key Report Takeaways

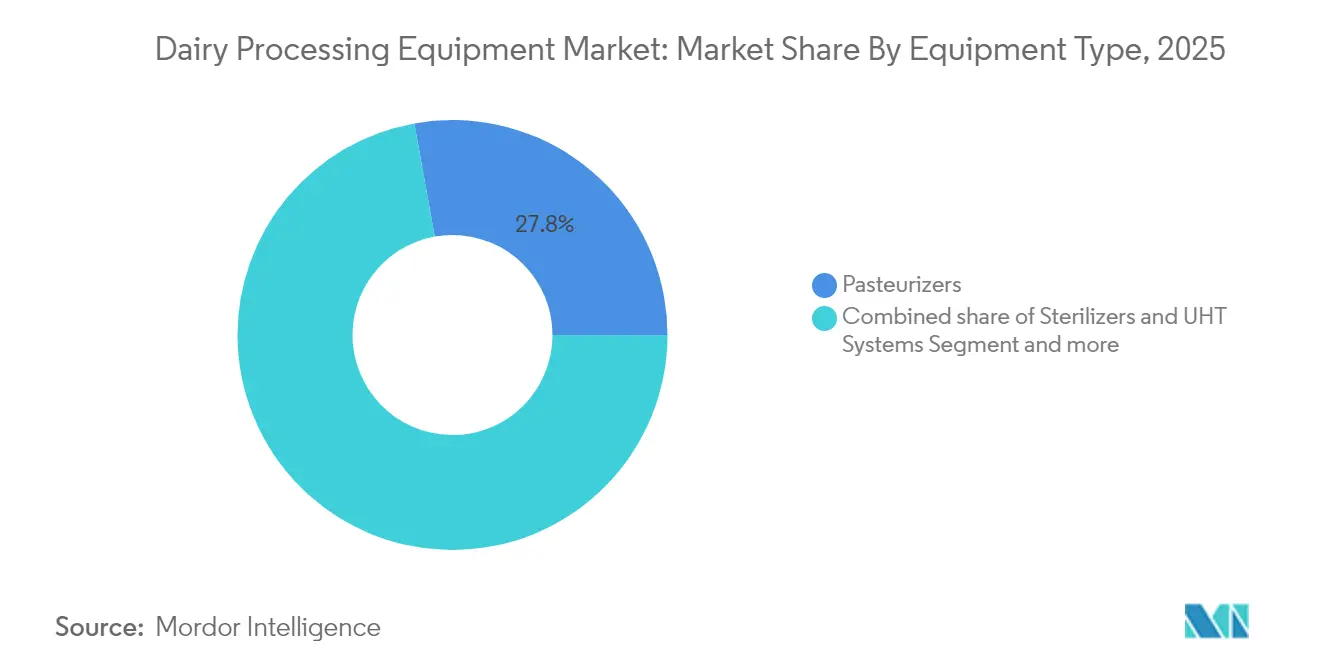

- By equipment type, pasteurizers led with 27.84% of dairy processing equipment market share in 2025, while membrane filtration systems post the fastest 6.68% CAGR for 2026-2031.

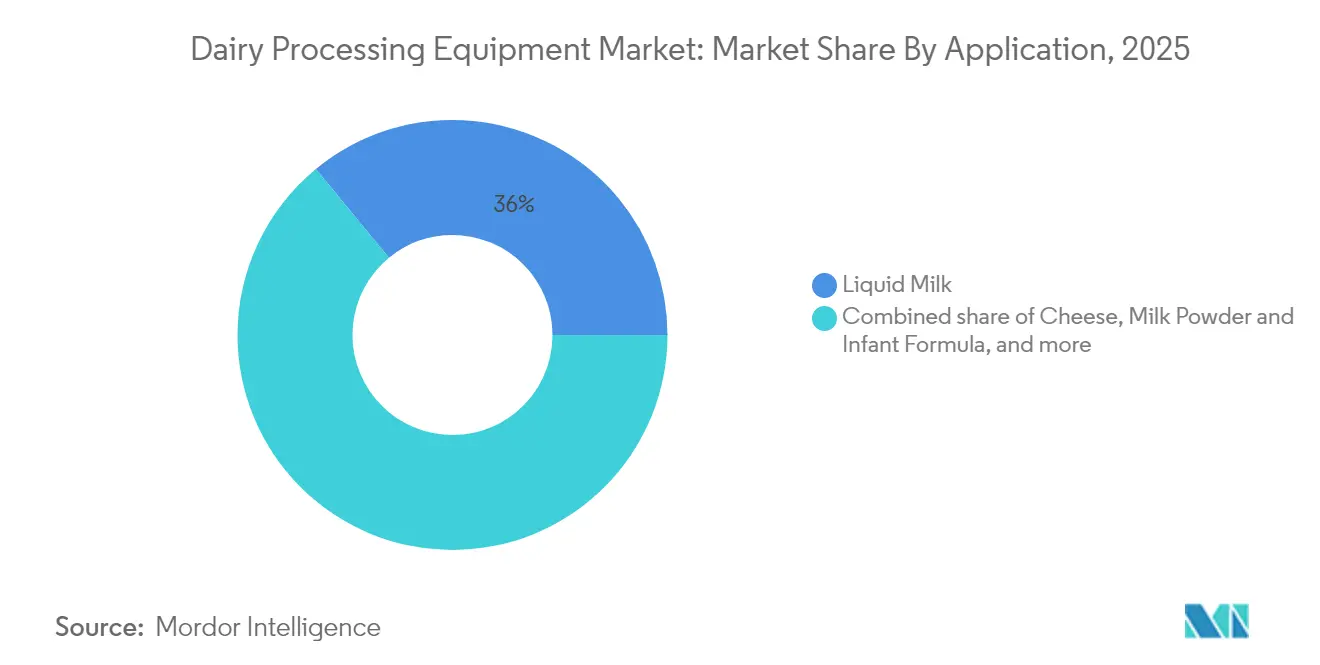

- By application, liquid milk processing accounted for a 35.96% share of the dairy processing equipment market size in 2025; milk powder and infant formula is projected to expand at a 6.82% CAGR to 2031.

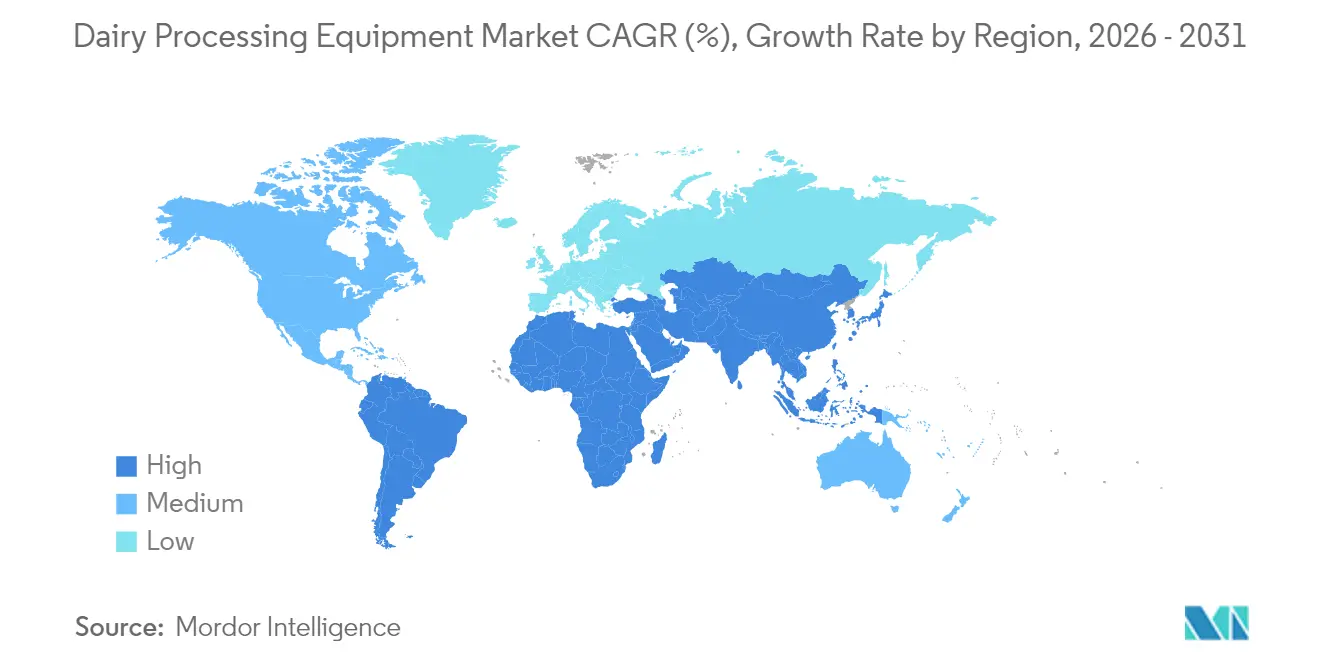

- By geography, Asia-Pacific commanded 39.21% of the dairy processing equipment market in 2025; South America records the highest 7.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dairy Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumption of processed and value-added dairy products | +1.2% | Global, with strongest impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Growing demand for shelf-stable and long-life dairy formats | +0.9% | Global, particularly emerging markets in APAC and South America | Long term (≥ 4 years) |

| Government incentives for dairy processing modernization | +0.8% | North America, Europe, India, and select South American countries | Short term (≤ 2 years) |

| Stringent food safety regulations | +0.7% | Global, with highest impact in North America and Europe | Medium term (2-4 years) |

| Adoption of automation and industry 4.0 technologies | +1.1% | North America, Europe, and developed APAC markets | Medium term (2-4 years) |

| Innovation in energy-efficient and low-emission processing systems | +0.6% | Global, with early adoption in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumption of processed and value-added dairy products

As consumers increasingly favor convenience-oriented dairy products, there's a growing demand for advanced processing equipment within the global dairy processing equipment market. This equipment is tailored to produce products with extended shelf lives and specialty formulations, subsequently boosting the consumption of value-added dairy products. The USDA's Agricultural Marketing Service highlights a growing demand for specialized dairy ingredients, with whey protein and milk albumin experiencing robust growth in export markets. To meet this demand, processing facilities are prioritizing investments in flexible equipment configurations that can support multiple product lines[1]U.S Department of Agriculture, "South American Dairy Market Overview", www.usda.gov. These investments align with the FDA's Grade 'A' Pasteurized Milk Ordinance, which outlines stringent requirements for equipment used in manufacturing value-added dairy products. Additionally, the Pennsylvania Department of Agriculture underscores the critical role of specialized equipment tailored to specific dairy products, such as yogurt and cheese, which require distinct processing protocols and equipment specifications. These niche offerings not only cater to evolving consumer preferences but also command premium pricing, justifying the adoption of advanced equipment to enhance production capabilities and competitiveness in the market.

Growing demand for shelf-stable and long-life dairy formats

The growing demand for shelf-stable dairy products is driving significant investments in ultra-high temperature (UHT) processing systems and aseptic packaging technologies across the dairy processing equipment market. These advancements are critical for meeting regulatory standards and expanding market opportunities. The FDA mandates specific pasteurization requirements for shelf-stable products, with 21 CFR 1240.61 stipulating that all milk products in their final packaged form must be pasteurized using approved methods[2]The Electronic Code of Federal Regulations (eCFR), "§ 1240.61 Mandatory pasteurization for all milk and milk products in final package form intended for direct human consumption.", www.ecfr.gov. UHT processing equipment must adhere to strict temperature and time controls, and the FDA requires the use of accurate recording devices to document compliance with sterilization parameters. Beyond developed markets, UHT technology is gaining traction in regions with limited cold-chain infrastructure. The USDA reports increasing opportunities for exporting shelf-stable dairy products to these areas, highlighting the technology's role in addressing logistical challenges. Additionally, government agencies emphasize the importance of UHT processing for ensuring food security. This technology is particularly vital in emergency preparedness scenarios where refrigerated storage is unavailable, underscoring its relevance in both domestic and international markets.

Government incentives for dairy processing modernization

Government incentives are playing a crucial role in driving the modernization of dairy processing across major global markets, strengthening the outlook of the dairy processing equipment market. In the United States, as of December 2024, the USDA's Dairy Business Innovation Initiatives, supported by a USD 53 million fund allocated through 2027, aim to enhance the production of value-added dairy products, improve supply chain resilience, and optimize processing efficiency for small and mid-sized dairy businesses[3]Northeast Dairy Business Innovation Center, "NE-DBIC Impacts", www.nedairyinnovation.com . Similarly, in India, the Production Linked Incentive (PLI) Scheme for the Food Processing Industry is significantly transforming the dairy manufacturing landscape. These government-backed programs not only reduce the financial burden associated with acquiring capital-intensive equipment but also align with the natural lifecycle of machinery replacement, creating a conducive environment for processors to modernize their operations. Moreover, these initiatives are contributing to rural employment generation, enhancing export competitiveness, and ensuring compliance with stringent food safety standards. These factors collectively play a critical role in sustaining the growth of the global dairy processing equipment market, positioning it for long-term development and innovation.

Stringent food safety regulations

Regulatory compliance is driving significant advancements across the dairy processing equipment industry. The FDA's Grade 'A' Pasteurized Milk Ordinance (PMO) establishes stringent standards for dairy processing facilities to ensure food safety and quality. The 2023 revision of the PMO incorporates updated provisions for Hazard Analysis and Critical Control Points (HACCP) systems and preventive controls, outlining precise equipment specifications for pasteurization and packaging processes[4]National Conference on Interstate Milk Shipments (NCIMS), "Grade ” A” Pasteurized Milk Ordinance (PMO", www.ncims.org. Additionally, the FDA's Dairy Grade A Voluntary HACCP program provides an alternative compliance pathway, focusing on science-based food safety measures and requiring processors to conduct systematic hazard analyses across their operations. Equipment manufacturers are required to design systems that comply with FDA standards for sanitary design and cleanability. The PMO mandates that all processing equipment must be easily cleaned and maintained in a sanitary condition to prevent contamination risks. Furthermore, the regulatory framework extends beyond federal requirements. State agencies, such as the Minnesota Department of Agriculture, play a critical role by offering detailed guidance on equipment standards, particularly for small-scale dairy processing plants, ensuring compliance at all operational levels.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial investment and maintenance costs for dairy processing equipment | -0.8% | Global, with highest impact in emerging markets and small-scale operations | Short term (≤ 2 years) |

| Limited technical expertise | -0.6% | Emerging markets in APAC, Africa, and parts of South America | Medium term (2-4 years) |

| Complex integration of new equipment into legacy plants | -0.5% | Developed markets with established infrastructure | Medium term (2-4 years) |

| Price sensitivity in emerging markets | -0.7% | APAC emerging markets, South America, and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High initial investment and maintenance costs for dairy processing equipment

Small-scale processors face significant challenges in adopting new equipment, primarily due to the high costs tied to regulatory compliance which continues to impact on the dairy processing equipment market. The Minnesota Department of Agriculture emphasizes the substantial investments required by small dairy processing plants to procure essential equipment, such as pasteurizers, homogenizers, and fermentation vats, to meet regulatory standards. Similarly, the University of Tennessee highlights that the financial burden extends beyond the initial purchase, encompassing ongoing maintenance, calibration, and replacements mandated by regulatory authorities. These high initial investments, coupled with recurring maintenance costs, create a significant barrier for small and medium-sized enterprises (SMEs) in adopting modern dairy processing equipment. Additionally, operational costs, including regular maintenance, energy consumption, and skilled labor, further escalate the total cost of ownership. As a result, many processors are compelled to either continue using outdated systems or rely on basic equipment, which significantly hampers production efficiency and limits product innovation. This situation poses a critical challenge to the global dairy industry, as it restricts the ability of small-scale and medium-sized processors to compete effectively in a market increasingly driven by technological advancements and consumer demand for high-quality dairy products.

Limited technical expertise

The shortage of skilled technicians proficient in operating and maintaining advanced dairy processing equipment continues to hinder dairy processing equipment market growth, particularly in regions with inadequate technical education infrastructure. The Food and Agriculture Organization identifies limited access to training programs and modern equipment as critical barriers for small-scale processors in developing countries. State regulatory agencies, such as the Pennsylvania Department of Agriculture, emphasize the critical role of comprehensive training for dairy processing personnel to ensure compliance with evolving food safety regulations. Additionally, the FDA's HACCP guidelines mandate that dairy processing facilities employ qualified personnel capable of implementing and maintaining robust food safety systems, further intensifying the demand for specialized training. In response, government agencies are introducing technical assistance programs aimed at addressing these gaps. However, the increasing complexity of modern dairy processing systems, which now integrate advanced automation and IoT technologies, necessitates expertise that extends beyond traditional mechanical skills. This growing need for specialized knowledge underscores the importance of developing targeted training initiatives to equip technicians with the competencies required to operate and maintain these sophisticated systems effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Pasteurizers Ensure Regulatory Compliance

In 2025, pasteurizers dominate the dairy processing equipment market with a 27.84% share, highlighting their indispensable role in ensuring food safety compliance across dairy processing operations. This dominance is driven by stringent regulatory requirements that mandate precise temperature and time controls during pasteurization. The FDA requires pasteurization equipment to maintain specified temperatures for designated durations and to include accurate recording devices to ensure compliance. State regulatory bodies, such as the Minnesota Department of Agriculture, further emphasize the importance of pasteurization equipment, identifying it as a critical investment for dairy processing facilities seeking regulatory approval. Additionally, the University of Tennessee's guidelines for dairy processing plants underscore the necessity of pasteurizers in meeting both federal PMO standards and state-specific regulations, ensuring product safety and facilitating market access.

Membrane filtration systems are poised to be the fastest-growing equipment segment within the dairy processing equipment market, with a projected CAGR of 6.68% from 2026 to 2031. Their growth is fueled by their versatility in applications such as protein concentration, lactose removal, and water recovery. Natural Resources Canada highlights membrane filtration as a key energy-efficient technology capable of significantly reducing energy consumption while concentrating cheese whey and standardizing milk composition. Regulatory bodies, including the FDA, recognize membrane filtration as an approved method for achieving specific product characteristics without compromising food safety. Furthermore, government agencies advocate for the technology's environmental benefits, such as water recovery and waste reduction, aligning with sustainability mandates that are increasingly shaping the dairy processing industry. The segment's rapid expansion reflects the growing need for flexible processing technologies that enable manufacturers to produce a variety of specialized dairy products from a single processing line, meeting both regulatory requirements and evolving market demands.

By Application: Liquid Milk Processing Maintains Market Leadership

In 2025, liquid milk processing accounts for 35.96% of the dairy processing equipment market share, solidifying its position as the most widely consumed dairy format globally and the backbone of dairy processing operations. According to the USDA's Agricultural Marketing Service, fluid milk represents the largest volume segment in dairy processing, driven by steady demand patterns that influence equipment investment strategies. Regulatory frameworks further strengthen this segment's dominance, with the FDA's Grade 'A' Pasteurized Milk Ordinance outlining stringent standards tailored specifically for fluid milk processing facilities. Additionally, the Minnesota Department of Agriculture highlights the necessity of specialized equipment configurations to ensure product quality and compliance with regulatory requirements for interstate distribution. These factors collectively reinforce the critical role of liquid milk processing in the dairy industry.

Between 2026 and 2031, the milk powder and infant formula segment is expected to grow significantly, further expanding the dairy processing equipment market at a CAGR of 6.82%, fueled by increasing export opportunities and the need for extended shelf life, aligning with global food security priorities. The USDA's Foreign Agricultural Service identifies significant potential for U.S. dairy ingredient exports, particularly whey and milk albumin, which are essential components in health foods and infant formula production. Infant formula, recognized as a vital application, demands the highest processing standards. To address this, the FDA enforces stringent regulations requiring manufacturers to adopt advanced equipment capabilities. The segment's growth is further supported by expanding international trade, with the USDA reporting rising demand for specialized dairy ingredients in emerging markets where domestic production capacity remains insufficient. This trend underscores the strategic importance of milk powder and infant formula applications in meeting global nutritional needs.

Geography Analysis

In 2025, Asia-Pacific commands a 39.21% share of the global dairy market, underscoring its position as both the leading milk producer and the fastest-growing consumer market. This growth is bolstered by proactive government policies, notably in India, where the Ministry of Food Processing Industries has earmarked INR 4,600 crore under the PM Kisan Sampada Yojana, emphasizing dairy processing. Meanwhile, China's evolving regulatory landscape sees the National Food Safety Standards proposing bans on reconstituted milk in sterilized products, a move that could redefine equipment needs for local processors. The USDA highlights a paradox in China's dairy market: domestic production inches up even as cow inventories dwindle, signaling a ripe opportunity for efficient dairy processing equipment. Japan, facing labor challenges, is turning to advanced automation, backed by government initiatives to ensure production efficiency amidst demographic shifts.

South America is set to be the fastest-growing region in the dairy processing equipment market, projected at a 7.05% CAGR from 2026 to 2031. This growth is underpinned by favorable production conditions and government policies that champion export-oriented dairy processing. The USDA's Agricultural Marketing Service notes a rise in South American milk production, thanks to favorable weather and a robust demand for dairy exports. Brazil's food processing landscape is notably dominated by dairy, as evidenced by government data highlighting its significant share in the country's food manufacturing. With advantages like a conducive climate and lower production costs, South American nations are carving out a competitive edge in the global dairy arena. Regional government agencies are not just recognizing this potential but are actively promoting dairy processing as a strategic industry, bolstering infrastructure and technology to enhance global competitiveness. North America, with its comprehensive regulatory frameworks and proactive government programs, continues to hold a dominant market position. A notable highlight is the Northeast Dairy Business Innovation Center, a testament to significant federal investment aimed at modernizing processing technologies.

Competitive Landscape

In the global dairy processing equipment market, numerous regional and national players vie for market share, leading to a moderately fragmented landscape. While a handful of major companies lead in scale and technological prowess, smaller firms adeptly address niche needs and local demands. This dynamic fosters a competitive atmosphere, spurring innovation and tailored product offerings across the dairy processing equipment market. Companies frequently set themselves apart through advancements in energy-efficient technologies, automation, and robust after-sales services.

Strategic trends highlight a push towards automation, enhanced energy efficiency, and modular designs that offer adaptable production setups. The competitive landscape is shaped by a tug-of-war between established players with vast installed bases and upstart tech providers rolling out groundbreaking innovations, particularly in membrane filtration and IoT monitoring.

Recent consolidations such as Heat & Control's acquisition of Tek-Dry Systems Ltd. and Hunt Heat Exchangers in April 2025 underscore a strategic tilt towards bolstering technological prowess and expanding market reach. Emerging markets, buoyed by infrastructure growth, present white-space opportunities, especially for cost-effective processing solutions. Specialized sectors, like plant-based dairy alternatives, also beckon, demanding tailored processing technologies. Companies that offer comprehensive solutions, blending equipment supply with continuous technical support, are finding favor in this competitive arena, especially where technical expertise is scarce.

Dairy Processing Equipment Industry Leaders

-

GEA Group Aktiengesellschaft

-

Krones AG

-

Tetra Laval Group (Tetra Pack)

-

SPX FLOW, Inc

-

Alfa Laval

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Agathangelou has launched a fully automatic halloumi and grilled cheese production line, marking a major shift from manual to advanced automation and setting new industry standards in efficiency and product quality. According to the company, the new system reduces labor costs by 70%, increases yield by 2–3%, and ensures uniform taste, texture, and consistency, while preserving the authenticity of traditional Cypriot halloumi.

- January 2025: DeLaval launched the Milking Automation MA Series, featuring three models (MA100, MA200, MA500) with automated milking process monitoring and modular design for future upgrades. The system integrates real-time data insights and scalable functionality for conventional parlour systems, representing a significant advancement in automated milking technology.

- March 2024: GEA has launched the GEA ecoclear i, a bacteria removal separator designed as a compact, plug-and-play skid solution for small to medium-sized dairies, enabling efficient reduction of bacteria and spores in milk. According to the brand, the system features fully automated operation, energy-efficient drives, and low water consumption, making it both cost-effective and sustainable. This innovation helps dairies improve product safety, extend shelf life, and meet stringent quality standards with minimal installation effort.

- January 2024: SPX FLOW, Inc. has unveiled the Seamless Infusion Vessel under its APV brand, designed to enhance the efficiency and hygiene of ingredient infusion processes in the food, beverage, and dairy industries. According to the company, this innovative vessel features a seamless, crevice-free design that minimizes contamination risks and simplifies cleaning, supporting strict sanitary standards.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our analysis defines the dairy processing equipment market as all purpose-built machinery installed in industrial facilities to heat-treat, separate, homogenize, concentrate, ferment, or otherwise convert raw milk into fluid, condensed, dried, or cultured dairy products. The boundary begins at milk reception tanks and ends before primary retail packaging lines, and values are expressed in USD at manufacturer selling prices.

Scope Exclusion: The study omits on-farm robotic milking units and standalone filling or labeling machines.

Segmentation Overview

-

By Equipment Type

- Pasteurizers

- Sterilizers and UHT Systems

- Homogenizers

- Centrifuges and Separators

- Evaporators and Dryers

- Membrane Filtration Systems

- Mixing and Blending

- CIP and Automation Modules

-

By Application

- Liquid Milk

- Cheese

- Milk Powder and Infant Formula

- Yogurt and Fermented Products

- Butter and Spreads

- Other

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- United Kingdom

- Germany

- Spain

- France

- Italy

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with plant engineers, dairy technologists, regional food-safety inspectors, and procurement managers across Asia-Pacific, Europe, the Americas, and the Middle East helped validate throughput assumptions, average selling prices, and replacement cycles. Follow-up surveys captured the adoption of automation modules and membrane retrofits that desk research could not quantify.

Desk Research

Mordor analysts reviewed open data from sources such as the Food and Agriculture Organization, United States Department of Agriculture, Eurostat, and India's NDDB to map milk output, trade flows, and plant capacity. Technical codes from UN Comtrade and national customs were mined to benchmark import prices for pasteurizers, separators, and membrane systems. We also drew context from peer-reviewed journals on thermal kinetics and sanitary design, along with corporate 10-K filings and investor decks that disclose equipment order backlogs. Where relevant, paid repositories like D&B Hoovers and Dow Jones Factiva supplied company-level revenue splits. This list is illustrative; many additional publications underpinned figure checks and narrative framing.

Market-Sizing & Forecasting

A top-down reconstruction starts with national milk production, shares it into processed pools using pasteurization penetration and export ratios, and then converts volumes into equipment demand with throughput standards per hour. Results are cross-checked through selective bottom-up roll-ups of major supplier shipments and sampled ASP × unit data. Key model drivers include global raw-milk output, heat-treatment compliance rates, investment incentives (for example, India's PLI scheme), average plant utilization, and membrane filtration adoption. Forecasts rely on multivariate regression blended with scenario analysis, capturing links between disposable income, dairy retail prices, and capex intentions voiced by interviewed processors. Data gaps in supplier counts are bridged by calibrated ratios from comparable plants.

Data Validation & Update Cycle

Each draft passes variance screens, anomaly flags, and a second-analyst review. Before publication, we re-contact select experts if new regulations or material mergers emerge. Updates occur annually, with interim refreshes triggered by events that move the market by more than three percent.

Why Mordor's Dairy Processing Equipment Baseline Earns Decision-Makers' Trust

Published numbers often diverge because firms choose different equipment lists, geographic mixes, and refresh rhythms.

Key gap drivers include whether membrane retrofits are counted, how often ASPs are refreshed, and if currency conversions are frozen or rolling.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.38 B (2025) | Mordor Intelligence | - |

| USD 13.49 B (2024) | Global Consultancy A | Includes ancillary CIP chemicals and relies on four-year update cadence |

| USD 10.70 B (2023) | Industry Association B | Excludes membrane systems and uses single top-down ratio without primary validation |

| USD 12.22 B (2025) | Regional Consultancy C | Focuses on Western plants only and keeps ASP static across regions |

The comparison shows that our carefully aligned scope, annual refresh, and dual-path validation give stakeholders a balanced, transparent baseline they can retrace and replicate with confidence.

Key Questions Answered in the Report

What is the current value of the dairy processing equipment market?

The dairy processing equipment market size is USD 14.07 billion in 2026 and is projected to reach USD 18.11 billion by 2031.

Which region leads global demand?

Asia-Pacific accounts for 39.21% of global demand, supported by high milk output in India and rapid processing investments across China and Southeast Asia.

Which equipment segment is growing fastest?

Membrane filtration systems post the highest 6.68% CAGR because they enhance protein concentration, water recovery and energy efficiency.

Why are pasteurizers still the largest segment?

Mandatory FDA and PMO regulations require every fluid milk plant to pasteurize, making pasteurizers foundational and giving them 27.84% of market share.

Page last updated on: