Dairy Testing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

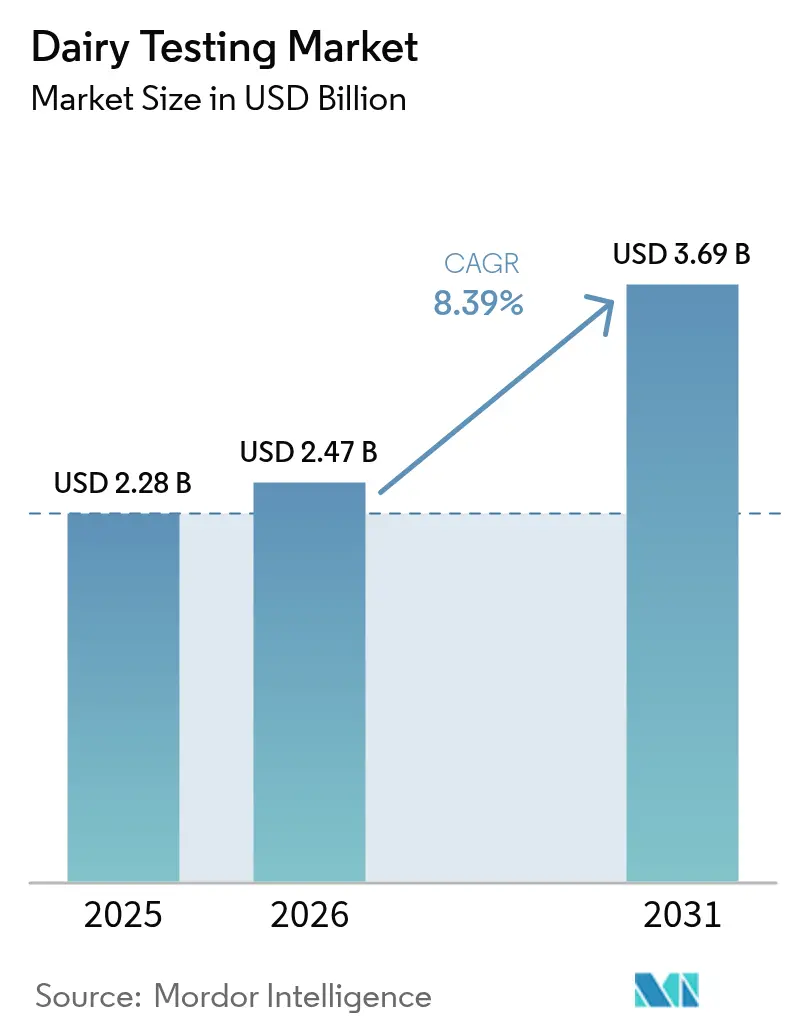

| Market Size (2026) | USD 2.47 Billion |

| Market Size (2031) | USD 3.69 Billion |

| Growth Rate (2026 - 2031) | 8.39% CAGR |

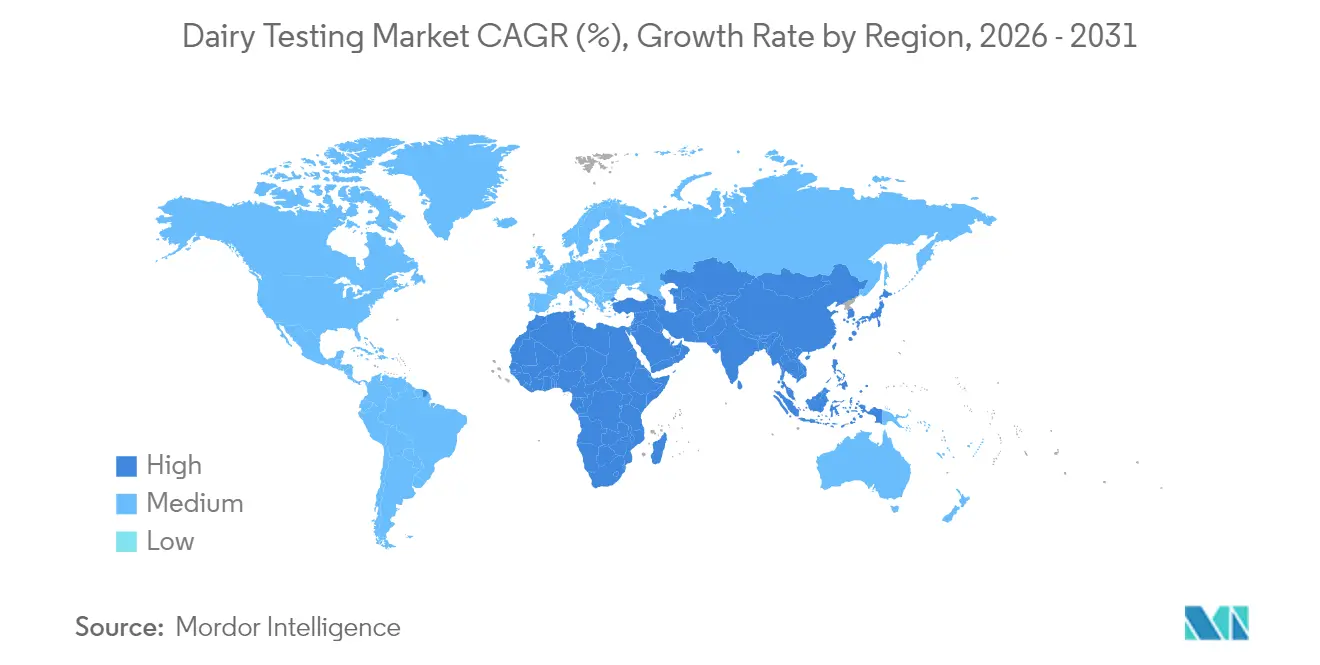

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

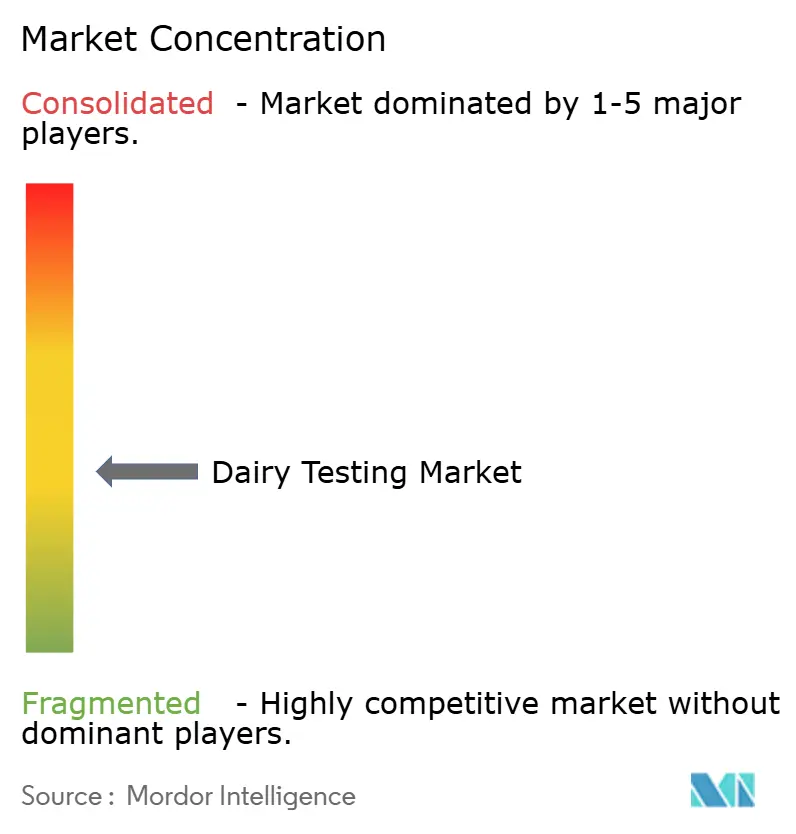

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dairy Testing Market Analysis by Mordor Intelligence

Dairy testing market size in 2026 is estimated at USD 2.47 billion, growing from 2025 value of USD 2.28 billion with 2031 projections showing USD 3.69 billion, growing at 8.39% CAGR over 2026-2031. This growth is driven by heightened global food safety concerns following major contamination incidents and the implementation of stricter regulatory standards, particularly in Europe, North America, and the Asia-Pacific region. The suspension of the United States' milk quality monitoring program in April 2025 prompted dairy processors to seek accredited third-party laboratories, thereby increasing demand for private sector testing. Ongoing listeria and salmonella incidents maintain pathogen detection as the primary testing service, while increased aflatoxin risks due to climate change drive growth in mycotoxin testing. The integration of automation, biosensors, and real-time data analytics reduces testing time and enables predictive quality management, driving adoption among medium and large dairy facilities [1]University of Wisconsin-Madison, “Suspension of FDA’s Grade “A” Milk Proficiency Testing Program,” farms.extension.wisc.edu.

Key Report Takeaways

- By testing type, pathogen screening led with a 38.02% share of the dairy testing market in 2025 and mycotoxin testing is projected to grow at a 9.55% CAGR.

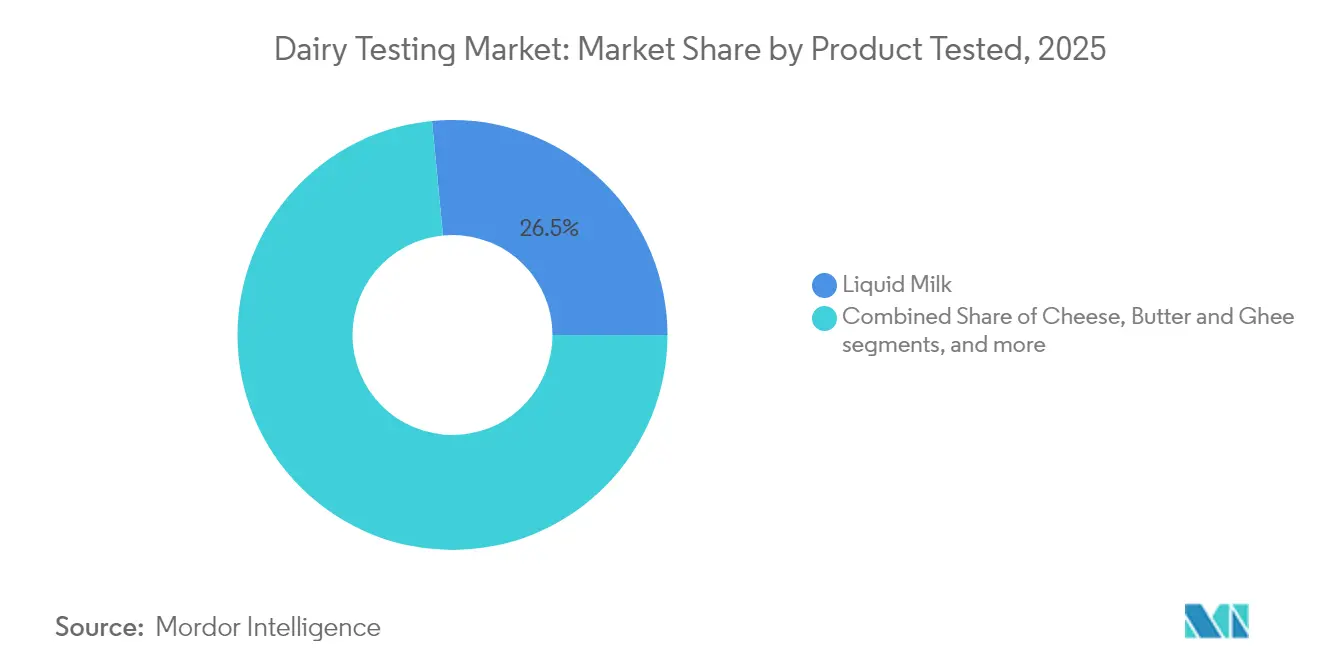

- By product tested, liquid milk held 26.52% share of the dairy testing market in 2025, while the ice-cream and frozen dessert category is poised for a 9.61% CAGR to 2031.

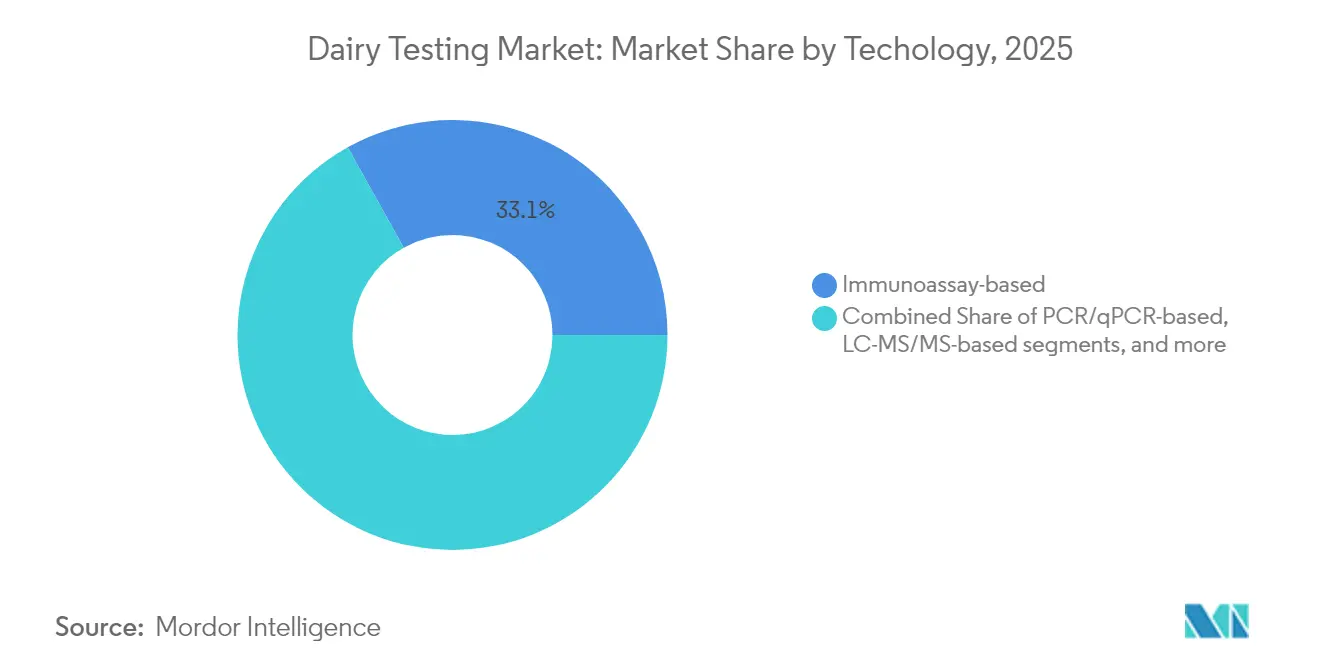

- By technology, immunoassays commanded a 33.10% revenue share in 2025 and will post steady mid-single-digit expansion, whereas biosensor and lab-on-chip platforms are forecast to log a 10.33% CAGR.

- By geography, Europe retained leadership with a 32.55% share in 2025; Asia-Pacific represents the fastest-growing region at 10.21% CAGR for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dairy Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing incidences of milk adulteration and contamination | +2.1% | Global, with acute impact in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Stringent food safety regulations | +1.8% | North America & EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Rising demand for quality and authentic dairy products | +1.4% | Global, led by developed markets | Long term (≥ 4 years) |

| Technological advancements in testing equipment | +1.2% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Rising demand for processed and packaged dairy products | +0.9% | Global, accelerating in emerging markets | Long term (≥ 4 years) |

| Rise in cross-contamination checks for plant-based dairy products | +0.7% | North America & EU, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Incidences of Milk Adulteration and Contamination

The escalating frequency of dairy contamination incidents has fundamentally altered risk management priorities across the global supply chain, with regulatory responses creating mandatory testing requirements that directly expand market demand. The USDA's launch of a national milk testing strategy for bird flu in December 2024, following the detection of H5N1 virus traces in pasteurized milk, demonstrates how emerging pathogen threats rapidly translate into systematic testing protocols [2]United States Department of Agriculture,"USDA Launches National Milk Testing Strategy".usda.gov . China's enforcement of a ban on milk powder in shelf-stable milk products reflects growing consumer awareness of adulteration practices, forcing manufacturers to implement more rigorous authenticity testing to verify compliance with new standards. The FDA's initiation of aged raw milk cheese sampling for bird flu in January 2025 signals regulatory expansion beyond liquid milk into specialty dairy categories, broadening the testing market scope.

Stringent Food Safety Regulations

Regulatory harmonization across major markets is creating standardized testing requirements that eliminate competitive advantages based on lax oversight, forcing universal adoption of advanced testing protocols. The European Commission's implementation of Regulation (EU) 2023/915 establishes maximum contaminant levels that require sophisticated analytical methods, particularly for emerging contaminants not previously regulated. Japan's Consumer Affairs Agency introduced mandatory application processes for dairy products with non-milk ingredients in April 2025, requiring detailed safety documentation and genetic identification for probiotic components, significantly expanding testing requirements for functional dairy products [3]European Commission, “Regulation (EU) 2023/915,” ec.europa.eu. The FDA's Laboratory Accreditation for Analyses of Foods (LAAF) program determination of sufficient laboratory capacity for mycotoxin testing in June 2024, establishes mandatory accreditation requirements for import-related food testing, creating barriers to entry that favor established testing providers [4]The Office of the Federal Register (OFR), "A Rule by the Food and Drug Administration on 06/03/2024", www.federalregister.gov. The Grade 'A' Pasteurized Milk Ordinance's 2023 revision reinforces standardized milk sanitation practices across states, ensuring uniform testing protocols that support interstate commerce while maintaining safety standards. These regulatory developments create predictable, long-term demand for testing services while raising industry standards globally.

Rising Demand for Quality and Authentic Dairy Products

Consumer sophistication regarding dairy product authenticity has reached a tipping point where premium pricing justifies comprehensive testing protocols, particularly for specialty products claiming specific origin or composition characteristics. The development of proteomic technologies combined with artificial neural networks for milk origin identification addresses growing consumer demand for traceability, with MALDI-TOF mass spectrometry achieving high accuracy in distinguishing bovine, ovine, and caprine milk samples. A2 milk authentication has become a critical testing requirement, with ELISA and Lateral Flow Immunoassay methods achieving 100% sensitivity and specificity for detecting β-casein A1 contamination at levels above 10% in fermented milk products. The quality assessment of combined dairy products using cow's and mare's milk with vegetable additives demonstrates expanding testing requirements for innovative dairy formulations that cater to health-conscious consumers. Investment in dairy processing infrastructure exceeding USD 8 billion as of 2025 reflects industry commitment to premium product development, with new facilities requiring sophisticated testing capabilities to justify premium positioning. This trend toward premiumization creates sustained demand for advanced testing services that can verify product claims and support brand differentiation.

Technological Advancements in Testing Equipment

The convergence of miniaturization, automation, and artificial intelligence in testing equipment is enabling real-time quality monitoring that transforms dairy processing from reactive to predictive quality management. Ultrasensitive aptasensor technology for kanamycin residue detection achieves detection limits of 16.56 aM with 60-second analysis times, representing a quantum leap in speed and sensitivity for antibiotic residue screening. Hyperspectral imaging technology for aflatoxin B1 detection in maize silage addresses feed safety concerns that directly impact milk quality, with Chinese regulatory guidelines requiring AFB1 testing every two weeks in spring and weekly during summer and autumn. The ProSpect In-Line Dairy Analyzer provides real-time analysis of fat, protein, moisture, and total solids with laboratory-grade accuracy, enabling continuous process optimization and reducing waste through immediate quality feedback. Development of immunoassays using streptavidin-polymerized horseradish peroxidase (SA-PolyHRP) for pathogen detection achieves limits of detection of 1.4 × 10^4 CFU/mL for E. coli O157:H7, significantly improving sensitivity compared to traditional methods.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced testing equipment | -1.6% | Global, acute impact in emerging markets | Short term (≤ 2 years) |

| Skilled labor shortage in food diagnostics | -1.3% | North America & EU, expanding globally | Medium term (2-4 years) |

| Cold-chain logistics challenges in emerging markets | -0.8% | Asia-Pacific, Africa, Latin America | Long term (≥ 4 years) |

| Complexity of multicomponent testing | -0.6% | Global, particularly affecting smaller laboratories | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Testing Equipment

The high cost of triple-quadrupole LC-MS/MS platforms for multi-toxin confirmation testing leads many smaller laboratories to outsource their testing. This outsourcing reduces local testing capabilities and increases the time needed to obtain results. The requirement for method life-cycle management in regulatory guidelines increases expenses further, as equipment upgrades necessitate new validation studies. Government laboratories face similar constraints - budget reductions led the FDA to suspend its milk-quality program in April 2025, creating a gap that private laboratories now address. Market growth remains constrained, especially in emerging regions, due to these high capital requirements and instrument costs.

Skilled Labor Shortage in Food Diagnostics

The shortage of skilled labor in food diagnostics poses a significant challenge to the dairy testing market. Dairy testing relies on expertise in microbiology and chemistry. A lack of trained professionals leads to slower testing processes, higher error rates, and reduced capacity. This directly impacts product safety, quality, and operational costs, while also limiting the scalability of testing services. Compliance with strict regulatory standards becomes more difficult, increasing the risk of penalties or market restrictions. The labor shortage further delays the adoption of advanced diagnostic technologies, which require skilled oversight, and slows innovation in testing methods and tools due to insufficient R&D talent. This gap in skilled labor undermines the efficiency, reliability, and growth potential of the global dairy testing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Tested: Liquid Milk Leads While Frozen Desserts Accelerate

In 2025, liquid milk accounted for a notable 26.52% of the revenue share, underscoring the global regulatory emphasis on maintaining the integrity of raw milk. Across major jurisdictions, mandatory screenings for antibiotic residues, alkaline-phosphatase activity, and total plate counts uphold a high density of testing. The ice-cream and frozen dessert segment is poised for a robust expansion, projected at a 9.61% CAGR. This growth is largely attributed to premium brands introducing innovative complex inclusions, necessitating heightened allergen and compositional checks.

Cheese testing is witnessing a surge, driven by European Regulation (EC) 2073/2005, which mandates specific microbiological criteria tailored to aging profiles. Testing for powdered milk and infant formulas remains stringent, emphasizing the detection of Cronobacter and the analysis of heavy metals. Furthermore, the testing of butter, ghee, and cultured products is increasingly incorporating fatty-acid profiling. This not only verifies label claims but also helps in identifying potential adulteration with vegetable oils, leading to a surge in the adoption of chromatographic testing methods.

By Testing Type: Pathogen Detection Drives Market Leadership

The pathogen detection segment accounted for 38.02% share of the dairy testing market revenue in 2025. Increased regulatory requirements for surveillance, driven by recurring listeria outbreaks, require consistent testing volumes throughout the year. The implementation of stringent safety protocols and the need for continuous monitoring have reinforced pathogen detection's central role in dairy safety assurance.

Mycotoxin testing, though a smaller segment, is projected to grow at a 9.55% CAGR as expanding aflatoxin risk zones in temperate regions due to wetter climates lead dairy facilities to implement comprehensive mycotoxin testing for feed materials. Pesticide residue and allergen testing contribute to stable baseline demand, while hormone testing demand increases due to growing concerns about veterinary drug residues. The rising awareness of food safety among consumers and regulatory bodies has further emphasized the importance of these testing segments.

By Technology: Immunoassays Dominate While Biosensors Emerge

Immunoassays captured 33.10% of 2025 revenue due to ease of use, reasonable cost and broad regulatory acceptance, but their relative share will taper as real-time biosensor formats mature. The 10.33% CAGR predicted for biosensor and lab-on-chip platforms reflects processor appetite for on-line, high-frequency measurement capable of triggering immediate line adjustments. LC-MS/MS and HPLC remain critical for confirmation and compositional work, anchoring the dairy testing market size for capital-intensive reference labs.

Aptamer-based electrodes now detect antibiotic residues at femtomolar concentrations within one minute, facilitating shift-based release testing. Simultaneously, portable hyperspectral imagers can screen feed silage for aflatoxin at truck-dump points, preventing contamination from entering closed milk loops. Time-resolved fluorescence strips for brucellosis antibody detection, sensitive to 1:12,800 dilutions, illustrate rapid progress in field diagnostics, charting a path for even broader dairy-plant implementation.

Geography Analysis

Europe dominated the dairy testing market with a 32.55% share in 2025, supported by consistent implementation of Regulation (EU) 2023/915 and comprehensive laboratory accreditation. Regional processors integrate rapid microbiology platforms with enterprise resource-planning systems to enhance compliance reporting for cross-border shipments. National reference laboratories collaborate through inter-laboratory proficiency programs to ensure result harmonization and safeguard the region's export interests.

Asia-Pacific demonstrates the highest growth rate at 10.21% CAGR through 2031. China's implementation of 50 new National Food Safety Standards introduces additional pesticide, heavy-metal, and mycotoxin testing requirements, driving investment in mass-spectrometry equipment. Japan's ingredient-notification system includes verification for functional fermented milks, expanding the dairy testing market for molecular-identification assays. India and Southeast Asian nations focus on cold-chain integrity programs, increasing demand for stabilizer, preservative, and shelf-life testing.

North America maintains a strong market position. While the Grade 'A' Pasteurized Milk Ordinance establishes core microbial standards, the April 2025 federal testing pause shifted verification activities to commercial laboratories, increasing dairy testing market share for specialized service providers. Canada's Safe Food for Canadians Regulations require pathogen and antibiotic screening for all dairy imports, increasing testing volume at border inspection facilities. Latin America and the Middle East & Africa exhibit moderate growth, limited by capital constraints and workforce shortages, but present opportunities for mobile laboratories and multinational processor-sponsored capacity-building initiatives.

Competitive Landscape

The dairy testing market shows moderate fragmentation, with Eurofins Scientific, Intertek, SGS, and Bureau Veritas as the primary market leaders. These companies maintain extensive global networks and hold ISO/IEC 17025 accreditations. Eurofins generated food testing revenue of EUR 5,142 million in the first nine months of 2024, providing the company with financial capacity for strategic acquisitions.

Strategic realignment is underway: Bureau Veritas exited routine food testing in October 2024 through a EUR 360 million divestiture to Mérieux NutriSciences, illustrating a pivot toward specialized providers. Neogen Corporation integrated 3M’s Food Safety Division, broadening pathogen, mycotoxin, and allergen platforms into a single catalog that resonates with large dairy conglomerates seeking one-stop solutions. Technology differentiation remains key; labs deploying AI-driven reporting tools can deliver validated results up to 30% faster, a decisive advantage for fast-moving short-shelf-life categories.

Regional entrants leverage localized knowledge and cost advantages but face accreditation hurdles such as the U.S. LAAF rule set, which now governs import-related mycotoxin tests. Consequently, several mid-sized Asian labs partner with equipment suppliers to attain method-validation support, while Latin American players pursue joint ventures with global majors to share reference-standard libraries. Looking forward, acquisition pipelines are likely to focus on geographies where laboratory density remains low relative to dairy output, permitting multinational chains to expand both capacity and the overall dairy testing market footprint.

Dairy Testing Industry Leaders

-

SGS GROUP

-

Bureau Veritas S. A.

-

Intertek Group plc

-

Neogen Corp.

-

Merieux NutriSciences

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: SGS formed a partnership with The PLEDGE on Food Waste, a third-party audited certification program that helps food service providers reduce food waste and improve sustainability in their operations.

- October 2024: Mérieux NutriSciences acquired the food testing business from Bureau Veritas at an enterprise value of EUR 360 million, with net proceeds from disposals amounting to EUR 290 million.

- April 2023: Symbio inaugurated its fifth diagnostic research laboratory in suburban Melbourne, marking a significant milestone. Spanning an impressive 8,600 square meters, this establishment stands as the largest of its kind in the entire Southern Hemisphere.

Global Dairy Testing Market Report Scope

The global dairy testing market is segmented by test type into, pathogen testing, pesticide, and residue testing, mycotoxin testing and other contaminants testing. By technology the global dairy testing market is segmented into, HPLC-based, LC-MS/MS-based, immunoassay-based and other technologies and by geography.

| Pathogen Testing |

| Pesticide and Residue Testing |

| Mycotoxin Testing |

| Allergen Testing |

| Hormone and Antibiotic Screening |

| Nutritional and Composition Analysis |

| Others |

| Liquid Milk |

| Cheese |

| Milk Powder and Infant Formula |

| Butter and Ghee |

| Ice-cream and Frozen Desserts |

| Yogurt and Fermented Dairy |

| Others |

| Immunoassay-based |

| PCR/qPCR-based |

| LC-MS/MS-based |

| HPLC-based |

| Biosensor and Lab-on-Chip |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Testing Type | Pathogen Testing | |

| Pesticide and Residue Testing | ||

| Mycotoxin Testing | ||

| Allergen Testing | ||

| Hormone and Antibiotic Screening | ||

| Nutritional and Composition Analysis | ||

| Others | ||

| By Product Tested | Liquid Milk | |

| Cheese | ||

| Milk Powder and Infant Formula | ||

| Butter and Ghee | ||

| Ice-cream and Frozen Desserts | ||

| Yogurt and Fermented Dairy | ||

| Others | ||

| By Technology | Immunoassay-based | |

| PCR/qPCR-based | ||

| LC-MS/MS-based | ||

| HPLC-based | ||

| Biosensor and Lab-on-Chip | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the dairy testing market?

The market is valued at USD 2.47 billion in 2026 and is projected to reach USD 3.69 billion by 2031.

Which testing type dominates revenue?

Pathogen detection led with a 38.02% share in 2025 due to strict global microbiological safety requirements.

Which region is growing the fastest?

Asia-Pacific is forecast to record a 10.21% CAGR through 2031, driven by new Chinese and Japanese food-safety standards.

What technologies are gaining popularity?

Biosensor and lab-on-chip platforms are expanding at a 10.33% CAGR, offering rapid on-site testing capabilities.

How fragmented is the competitive landscape?

The market shows moderate fragmentation with a concentration score of 4, indicating significant room for mergers and acquisitions.

Page last updated on: