Cyprus Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

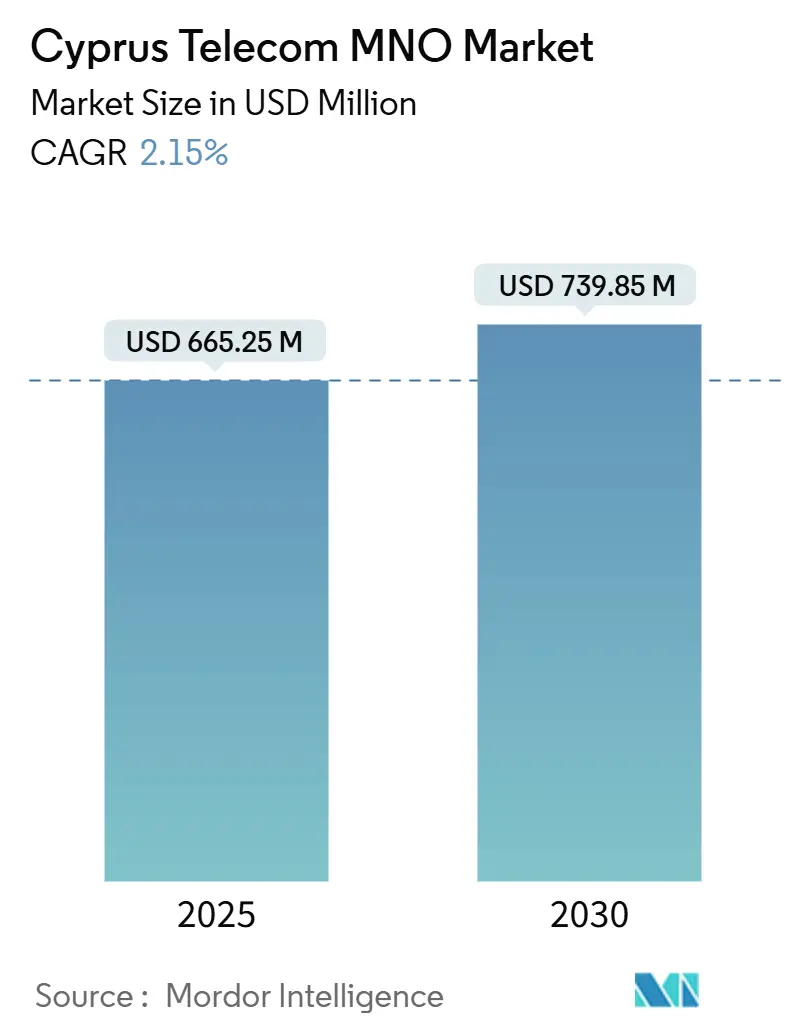

| Market Size (2025) | USD 665.25 Million |

| Market Size (2030) | USD 739.85 Million |

| Growth Rate (2025 - 2030) | 2.15% CAGR |

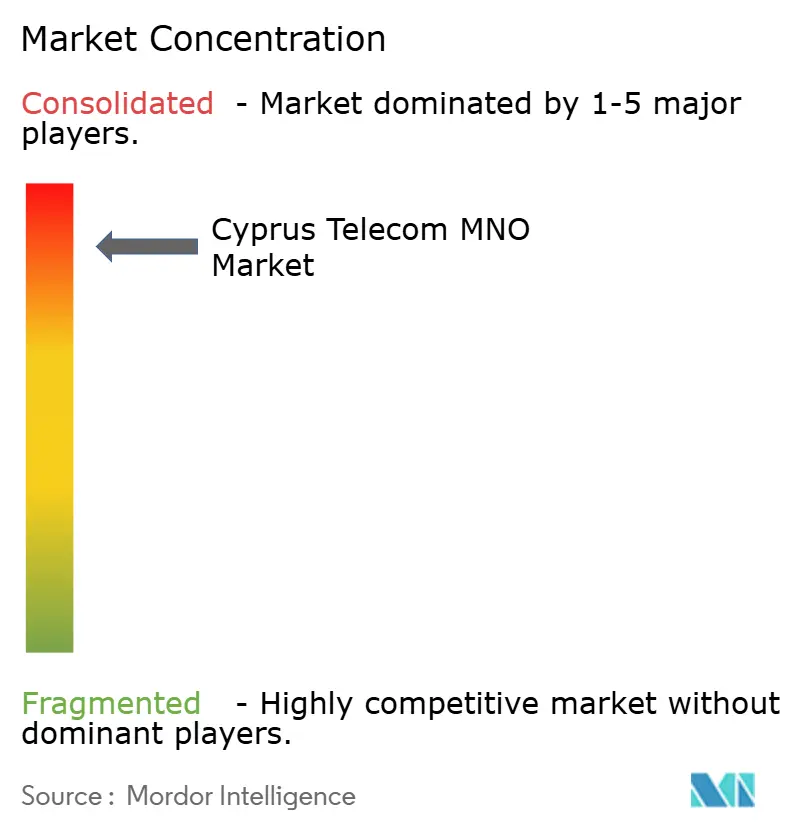

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cyprus Telecom MNO Market Analysis by Mordor Intelligence

The Cyprus Telecom MNO Market size is estimated at USD 665.25 million in 2025, and is expected to reach USD 739.85 million by 2030, at a CAGR of 2.15% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 1.46 million Subscribers in 2025 to 1.62 million Subscribers by 2030, at a CAGR of 2.07% during the forecast period (2025-2030).

This growth arises from sustained 5G monetization, steady fiber uptake and expanding international connectivity services that leverage the island’s subsea-cable network. Operators concentrate capital on network optimization, premium service tiers and enterprise cloud networking instead of fresh subscriber acquisition. Data-centric offerings already outpace legacy voice lines, and seasonal tourism surges plus a growing financial-services sector reinforce bandwidth demand. Government voucher programs, EU recovery funding and private subsea cable consortia supply additional momentum, although OTT substitution and spectrum-cost burdens temper margins.

Key Report Takeaways

- By service type, data services held 44.45% of the Cyprus telecom market share in 2024 while IoT services are projected to advance at a 2.13% CAGR through 2030.

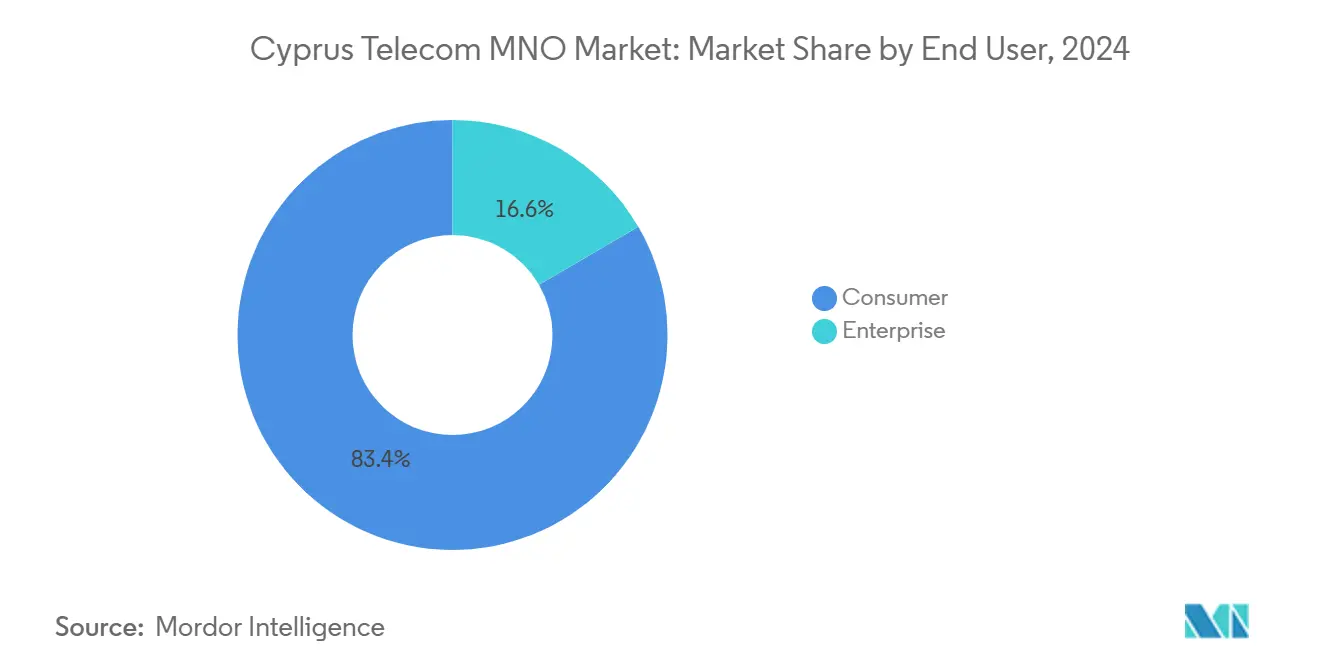

- By end user, the enterprise segment accounted for 83.39% of revenue in 2024 and is expected to grow fastest at a 2.75% CAGR through 2030.

Cyprus Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G coverage completion | +0.8% | Nicosia, Limassol, Larnaca | Medium term (2-4 years) |

| Gigabit FTTH voucher rollout | +0.6% | Rural and underserved zones | Short term (≤2 years) |

| Data-hungry tourism traffic | +0.4% | Coastal resorts Paphos, Ayia Napa, Protaras | Short term (≤2 years) |

| Enterprise cloud and SD-WAN adoption | +0.5% | Business districts in Nicosia and Limassol | Medium term (2-4 years) |

| Subsea-cable landing-station positioning | +0.3% | Southeastern coastal stations | Long term (≥4 years) |

| Growth of shipping IoT corridors | +0.2% | Limassol and Larnaca ports | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

5G coverage completion

Nationwide 5G availability since mid-2023 frees operators from heavy radio-access rollouts and lets them channel funds into capacity layering, network slicing and Vo5G services. The fully assigned 700 MHz and 3.6 GHz licenses enable blanket rural reach and dense urban throughput, making premium plans more marketable and elevating Cyprus above regional peers[1]5G Observatory, “Quarterly Report 2025,” 5gobservatory.eu. Cyta capitalizes on its speed-lead ranking to pitch differentiated B2B packages, while Epic accelerates deployment with European Investment Bank backing. Complete coverage simultaneously supports edge-cloud applications for shipping logistics, autonomous port operations and augmented-reality tourist guides.

Gigabit FTTH voucher rollout

A government-funded EUR 10 million voucher program subsidizes up-to-2 Gbps fiber upgrades for roughly 82,000 households. The incentive compresses payback periods in low-density villages, spurring Cyta and Epic to speed builds outside the four major cities. Uptake bolsters average revenue per fixed-line user, mitigates OTT erosion of voice, and provides a future platform for 10 Gbps services. Voucher eligibility criteria that require sub-100 Mbps baseline speeds ensure the measure specifically targets underserved homes.

Data-hungry tourism traffic

Peak visitor months often double active mobile-data sessions, compelling operators to deploy temporary small-cells at beaches and archaeological sites. Roaming bundles designed for tourists already command price premiums of 15-20% over domestic plans. Forward bookings for summer 2025 suggest another record influx, reinforcing near-term traffic growth. Tourism-related data bursts also drive content-delivery partnerships with streaming platforms that cache video closer to end users.

Enterprise cloud and SD-WAN adoption

Financial-services and professional-services clusters increasingly demand managed SD-WAN links to multi-cloud environments hosted by emerging hyperscalers zones in Limassol. The government’s EUR 177.25 million innovation fund accelerates pilot migrations of tax-administration systems to cloud infrastructure [2]Kyriaki Michael, “Government Unveils EUR 177 million Innovation Fund,” Cyprus Mail, cyprus-mail.com. Operators respond by bundling security gateways, analytics dashboards and zero-touch provisioning, deepening enterprise stickiness and lifting ARPU.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OTT substitution of voice and SMS | -0.9% | Nationwide, higher in cities | Short term (≤2 years) |

| High spectrum fees versus small population | -0.4% | National licensing regime | Medium term (2-4 years) |

| Cross-border roaming price erosion | -0.2% | Buffer-zone tourist areas | Medium term (2-4 years) |

| Limited skilled fiber-deployment labor pool | -0.3% | Rural buildouts | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

OTT substitution of voice and SMS

Smartphone penetration above 95% and the prevalence of unlimited bundles intensify the shift toward WhatsApp and Viber, eroding operator voice receipts that already dropped 45% worldwide by 2024. Cyprus’s tech-savvy user base accelerates this trend. Operators attempt mitigation through Vo5G high-definition calling and bundling of advanced call-management features for enterprises.

High spectrum fees versus small population

One million residents shoulder license outlays comparable with those of larger EU countries. This elevates spectrum costs to more than the global 7%-of-revenue benchmark, squeezing EBITDA margins and slowing incremental network upgrades.[3]GSMA, “Spectrum Pricing in Small Markets,” gsma.com Smaller players such as Epic must stretch capital budgets over longer horizons, raising the risk of under-investment and widening performance gaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Revenue Transformation

Data services accounted for 32.56% of the Cyprus telecom market size in 2024, underscoring their ascendance over traditional voice. Traffic volumes will keep expanding as 4K streaming, cloud gaming and real-time translation apps permeate daily life. IoT remains the headline growth pocket, projected at 3.48% CAGR through 2030, buoyed by smart-container tracking across the island’s ports and real-time fuel-management systems on cruise ships. Operators align pricing with tiered data allowances, edge caching and differentiated latency guarantees that command enterprise premiums. Voice, messaging and other legacy lines will continue to shrink yet retain niches in emergency communications, fax-dependent public administration and specific call-center use cases.

Service diversification also reflects a strategic swing toward platform revenue models. Cyta’s launch of an integrated OTT-plus-broadband bundle illustrates how incumbents leverage network ownership to position exclusive content libraries. Meanwhile, Epic’s partnership with global cybersecurity vendors delivers managed threat-protection overlays on cloud links, unlocking higher margin segments. The mix of broadband, mobile data and managed digital services forms a revenue core less exposed to pure connectivity commoditization.

By End User: Enterprise Growth Outpaces Consumer Maturation

Enterprises generated 31.88% of 2024 revenue but are forecast to expand at a 4.01% CAGR to 2030, outstripping the consumer base where penetration is saturated. Financial-services conglomerates, maritime operators and an emergent tech-startup scene require international MPLS, SD-WAN and secure multi-cloud connectivity that local operators are best placed to deliver. The consumer segment nevertheless remains dominant at 68.12% of the Cyprus telecom market size, supported by bundled streaming, smart-home security and gaming add-ons.

Enterprise contracts now favor outcome-based service-level agreements stressing latency, data residency and threat-detection guarantees. Cyta’s full-stack BSS/OSS overhaul with Netcracker equips product teams to tailor complex deals swiftly, shrinking quote-to-cash cycles. Epic counters with a fiber-backed unified-communications-as-a-service offering that converges desktop, mobile and video collaboration into one license. These dynamics raise overall revenue quality even as consumer pricing remains competitive.

Geography Analysis

Cyprus’s compact size coupled with its Eastern Mediterranean perch gives operators a unique blend of complete domestic reach and lucrative transit potential. The main subsea cable landings at Yeroskipou, Pentaskhinos and Ayia Napa integrate systems such as ALEXANDROS, CADMOS and UGARIT, routing Europe-to-Middle East traffic that fortifies wholesale income. These gateways also underpin cloud-region feasibility studies by hyperscalers seeking low-latency bridges between continents.

Urban areas receive first-wave technology upgrades. Nicosia’s government quarter and Limassol’s finance district enjoy symmetrical multi-gigabit options, supporting high-frequency trading and blockchain-as-a-service incubators. Larnaca International Airport hosts multi-operator 5G indoor systems to cope with dense seasonal footfall. Conversely, mountainous Troodos villages depend on a combination of state vouchers and fixed-wireless links for broadband, a disparity that remains a policy concern despite recent progress.

Cross-border dynamics inject complexity. EU roaming rules cease at the United Nations buffer zone, so subscribers face higher tariffs in the Turkish-administered north, prompting operators to issue split pricing advisories. To alleviate consumer confusion during day trips, Cyta pilots seamless multi-IMSI SIMs that switch tariffs automatically when detection algorithms flag location changes. Meanwhile, marine coverage is strengthened through cooperative agreements with satellite operators that equip merchant fleets with hybrid 5G-satcom terminals, positioning Cyprus as a testbed for maritime broadband corridors.

Competitive Landscape

The Cyprus telecom market exhibits a high level of concentration: Cyta held 54.22% of mobile connections in 2024, Epic followed with 34.79% and Cablenet covered the remainder across cable and mobile virtual network offerings. PrimeTel’s 2023 exit tightened the field and accelerated spectrum reallocation negotiations. Cyta leverages its vertically integrated assets, from subsea gateways to national fiber backbones, to cross-sell wholesale capacity and retail quad-play bundles.

Strategic moves hinge on digital modernization and international reach. Cyta’s EUR 19 million Netcracker deployment streamlines product catalog management and real-time charging, preparing the operator for network slicing commerce at scale. Epic secured EUR 19 million from the European Investment Bank to add 1,600 km of fiber, challenging Cyta’s fixed-access dominance. Cablenet, which piggybacks on Cyta’s mobile network for 5G, focuses on quality-of-experience differentiation using Infovista assurance analytics.

Market entry threats come from infrastructure players rather than traditional telcos. Grid Telecom and Tamares Telecom aim to build an open-access landing station that could lure new wholesale competitors and global content networks. The incumbents respond with discriminatory service innovation: Cyta bundles edge-cloud capacity with wholesale circuits, while Epic offers integrated SD-WAN overlays for enterprises seeking multi-path resilience. Overall, healthy capex levels and targeted product innovation maintain competitive pressure despite structural consolidation.

Cyprus Telecom MNO Industry Leaders

Cyta

Epic

PrimeTel

Cablenet

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Government launched a EUR 120 subsidy for ≥200 Mbps internet, targeting 82,000 homes across rural districts.

- January 2025: The national ICT sector reached EUR 2.33 billion, equal to 13% of GDP, underpinned by a EUR 177.25 million innovation program.

- November 2024: Epic began mandatory SIM registration for prepaid lines, with cut-off set for 10 Nov 2024.

- September 2024: Cyta selected Netcracker for end-to-end BSS/OSS transformation to accelerate 5G monetization.

Cyprus Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How extensive is 5G coverage in Cyprus?

As of mid-2023, 5G household coverage reached 100%, allowing operators to focus on capacity upgrades and service innovation rather than fresh rollouts.

What government incentives support broadband upgrades?

A EUR 10 million gigabit voucher scheme offers EUR 200 for households upgrading sub-100 Mbps connections to fiber speeds of up to 2 Gbps.

Who leads the Cyprus telecom market?

State-owned Cyta holds 54.22% of mobile subscribers and controls most fiber and subsea infrastructure, followed by Epic at 34.79%.

Which segment is growing fastest in Cyprus telecom services?

IoT services exhibit the highest projected growth at a 2.13% CAGR through 2030, driven by maritime logistics and smart-asset tracking.

Page last updated on: