Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 13.74 Billion |

| Market Size (2026) | USD 14.42 Billion |

| Market Size (2031) | USD 18.37 Billion |

| Growth Rate (2026 - 2031) | 4.95% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Telecom MNO Market Analysis by Mordor Intelligence

The Indonesia Telecom MNO Market size was valued at USD 13.74 billion in 2025 and estimated to grow from USD 14.42 billion in 2026 to reach USD 18.37 billion by 2031, at a CAGR of 4.95% during the forecast period (2026-2031).

Spending growth follows rapid mobile data uptake, persistent network upgrades, and state-backed digital inclusion programs that cut across the archipelago’s 17,500 islands. Operators funnel capital toward 4G densification and 5G rollouts to keep pace with video-heavy traffic, while enterprise clients seek secure cloud connectivity that boosts average revenue per user. Ongoing spectrum reforms and infrastructure-sharing models lower deployment risk, yet sustained price competition keeps headline ARPU growth muted. The XL Axiata–Smartfren merger exemplifies the strategic push for scale that helps monetize next-generation networks and counters over-the-top substitution.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive mobile data consumption fueled by video and gaming apps | +1.8% | Java, Sumatra, and core urban centers | Short term (≤ 2 years) |

| Nationwide 4G and 5G rollout reaching outer islands | +1.2% | Eastern Indonesia, Maluku, Papua | Medium term (2-4 years) |

| Fixed–mobile convergence bundles lifting household ARPU | +0.9% | Greater Jakarta, Surabaya, Tier-2 cities | Medium term (2-4 years) |

| Government-led Palapa Ring and Nusantara fiber backbone projects | +0.7% | Remote districts across 514 regencies | Long term (≥ 4 years) |

| Hyperscale data-center interconnect demand under data-sovereignty law | +0.3% | Jakarta, Surabaya, Batam | Short term (≤ 2 years) |

| LEO-satellite backhaul enabling remote-area enterprise IoT | +0.2% | Mining and agriculture clusters on outer islands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive mobile data consumption fueled by video and gaming apps

Telkom Indonesia recorded 127.1 million mobile broadband users in 2023 with data traffic of 17.9 million TB, confirming that video-centric habits now anchor revenue decisions.[1]Telkomsel, “4G LTE and VoLTE,” telkomsel.com Disney+ Hotstar captured 70% of paid streaming subscriptions, while Netflix held 46%, pushing average smartphone users to consume high-definition content on 4G and emerging 5G networks. XL Axiata logged 19% traffic spikes during peak holidays, with East Lombok surging 34% and Malioboro tourism zones up 115%. Operators now prioritize capacity upgrades to avoid congestion and to support gaming applications that demand latency below 40 ms. The Indonesia telecom MNO market sees sustained data monetization as premium bundles pair generous quotas with low-latency assurance, creating upsell potential even in a price-sensitive prepaid base.

Nationwide 4G and 5G rollout reaching outer islands

Telkomsel already covers 97% of the population through 247,472 base stations, and its 5G speeds reach 64.3 Mbps—almost four times faster than 4G. The government mandates commercial 5G presence in 29 cities by 2025, supported by the Palapa Ring fiber backbone that reduces backhaul bottlenecks. Expanded mid-band spectrum will enable operators to deliver enterprise-grade service for smart ports, mining automation, and logistics corridors in Sulawesi and Kalimantan. With private LTE and 5G networks forecast to reach USD 7.4 billion globally by 2027, Indonesian carriers target dedicated slices for factories and oil rigs where wired links remain impractical. Improved network quality translates into stronger customer experience scores, reinforcing willingness to pay for elevated tiers.

Fixed–mobile convergence bundles lifting household ARPU

IndiHome leads fixed broadband with 10.1 million subscribers and 66.7% share, yet average household ARPU stands at USD 17, showing headroom for value expansion once converged offers gain traction. Triple-Play packages that combine fiber, pay-TV, and unlimited mobile data defend against cord-cutting while attracting new households that need bundled pricing to manage budgets. Fixed revenue is projected to grow from USD 3.2 billion in 2024 to USD 4 billion in 2029, aided by deeper fiber coverage and rising demand for remote work solutions. Operators deploy self-install kits and flexible payment plans to open new addressable markets among the 26% of homes still lacking fixed broadband. As convergence adoption rises, churn drops, underpinning lifetime value improvement.

Government-led Palapa Ring and Nusantara fiber backbone projects

The USD 1.5 billion Palapa Ring fiber extends 35,000 km across every regency, furnishing carriers with scalable backhaul and reducing individual capital outlays through open-access leasing.[2]GSMA, “Accelerating 5G in Indonesia: A Spectrum Roadmap for Success,” gsma.comTelkom Indonesia’s own 176,663 km fiber footprint complements this backbone, enabling rapid service extensions to mining and tourism sites in outer islands that historically relied on microwave links. Fiber continuity supports Nusantara, the future national capital, where IDR 280 billion in new telco fiber spend is slated through 2026. Each 10% rise in broadband penetration correlates with a 1-1.5% GDP per capita uplift, validating the state focus on digital infrastructure. Lower backhaul tariffs improve project economics for smaller players and community ISPs, widening the Indonesia telecom MNO market base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent price competition suppressing ARPU | -1.4% | Nationwide prepaid segments | Short term (≤ 2 years) |

| Fragmented spectrum and high reserve prices | -0.8% | All national 5G license areas | Medium term (2-4 years) |

| Right-of-way permit delays slowing fiber rollout | -0.6% | Dense urban corridors | Medium term (2-4 years) |

| Shortage of 5G radio-frequency planning talent | -0.3% | Eastern islands outside Java | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent price competition suppressing ARPU

Indonesian prepaid users still focus on affordability, keeping blended ARPU well below the Asia-Pacific average of USD 10.5 despite heavier data usage. Tariff wars in 2023 shaved effective yields even as traffic grew, compelling Smartfren to hike data prices by 10% to restore margins, a move only partly matched by rivals. The pending XL Axiata–Smartfren merger should raise market discipline, promising USD 300-400 million in annual cost savings that offset revenue pressure. Nevertheless, over-the-top players such as WhatsApp, which cut business messaging fees by up to 97%, continue to erode legacy voice and SMS income. Sustained promotional intensity will keep the Indonesia telecom MNO market chasing volume over price increases in the near term.

Fragmented spectrum and high reserve prices

The 5G auction delay to 2025 freezes operator roadmaps, while limited mid-band holdings curb rollout efficiency. GSMA recommends each carrier secure 100 MHz in the 3.5 GHz layer to deliver target speeds, yet reserve prices remain at a premium to regional benchmarks. Smaller carriers face leverage risk once bidding opens, potentially slowing investment in rural coverage where returns are already thin. The situation favors incumbents with deeper balance sheets and existing spectrum depth. Regulatory clarity on staggered fees and coverage obligations would ease capital strain and accelerate 5G availability across the Indonesia MNO telecom market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Segment 1

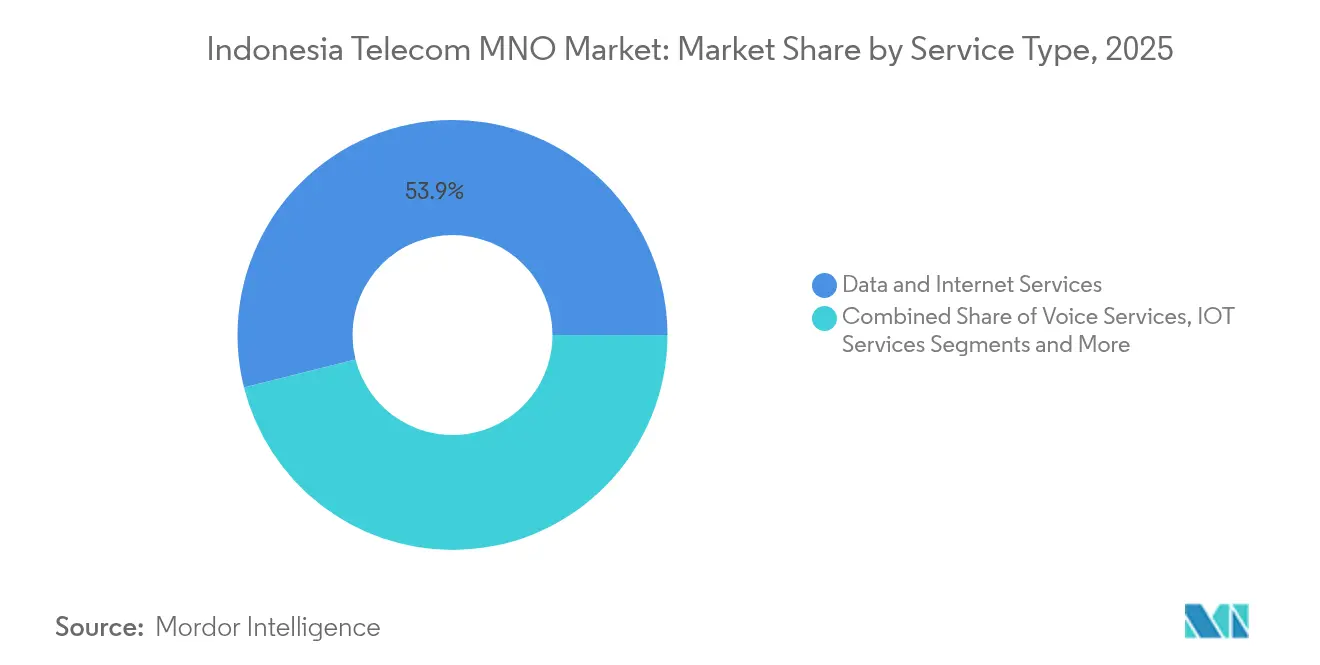

Data and Internet Services accounted for 53.92% of Indonesia telecom MNO market revenue in 2025, underscoring a structural pivot from legacy voice lines. Voice still holds 20.62% with a 4.79% CAGR through VoLTE adoption, proving carrier-grade call quality has residual appeal even under OTT pressure. IoT and M2M claim 5.75% share, and operators expect triple-digit device growth by 2028 as automotive, banking, and utilities fleets connect to XL Axiata’s IoT Connectivity+ platform. OTT and PayTV services sit at 5.43%, with Disney+ Hotstar’s 70% slice highlighting direct streaming traction. The remainder 14.28% comes from wholesale, roaming, and varied digital services that ride a cloud market expanding at 25% CAGR to USD 0.8 billion in 2023.

Investment priorities favor packet-core upgrades and edge computing nodes that keep latency below 20 ms for mobile gaming and industrial automation. Private LTE pilots in ports and mining sites help validate returns ahead of broad 5G monetization. Revenue diversification flows from cybersecurity bundles and data-center colocation designed for enterprises complying with Indonesia’s data-sovereignty law. With fixed-mobile convergence gaining momentum, operators bundle fiber with unlimited mobile data and streaming content, reinforcing household stickiness and reducing churn within the Indonesia telecom MNO market.

By End-User: Enterprise momentum outpaces mass market

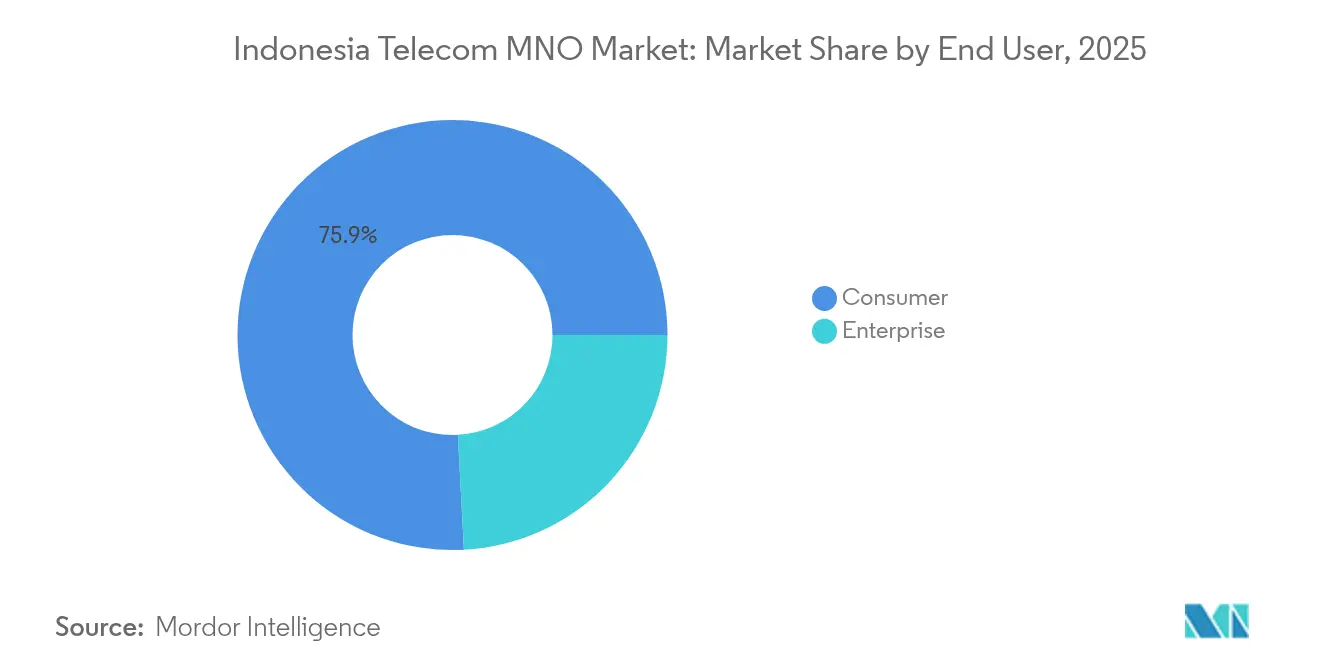

Enterprises generated 24.15% of revenue in 2025 and are projected to reach 29.15% by 2028, driven by 5.29% CAGR as firms digitize operations and shift workloads to the cloud. Telkom Indonesia serves 618,854 SMEs plus 714 public institutions via integrated ICT offers that blend connectivity with cybersecurity and analytics. Digital payment usage among SMEs rises, expanding the addressable base for secure connectivity and managed services. Consumer lines still provide 75.85% and post a 4.74% CAGR, yet growth leans on higher-value data tiers rather than subscriber additions because penetration already exceeds 120%.

Rising smartphone shipments—up 20% year-on-year in Q2 2024 led by Xiaomi at 18.1%—sustain throughput growth in the consumer segment. Growing appetite for mobile-only entertainment pushes carriers to negotiate favorable content licensing, seeking differentiated bundles that ease OTT substitution risk. Enterprise demand meanwhile tilts toward private networks, managed SD-WAN, and data-center interconnect, enlarging the strategic weight of enterprise revenue in the Indonesia telecom MNO market size calculus.

Geography Analysis

Java and Sumatra together generate more than 74.65% of revenue thanks to dense populations, mature 4G footprints, and early 5G launches. Data traffic density in Jakarta regularly tops 10 GB per user each month, persuading carriers to densify sites with massive-MIMO arrays that quadruple spectral efficiency. Suburban spillover boosts take-up of fixed–mobile convergence packages as fiber passes an additional 3 million homes per year. The Indonesia telecom MNO market size tied to Java reaches well above USD 8.35 billion, guiding network planning and marketing budgets.

Kalimantan and Sulawesi grow off a smaller base but outpace the national average on a percentage basis as resource extraction zones demand resilient links for IoT and remote surveillance. Edge data centers in Balikpapan and Makassar reduce backhaul needs and support local processing for oil rigs and plantations. Government incentives around the Nusantara capital relocation further accelerate fiber trenching and tower builds, extending 5G pilots to new economic clusters by 2026.

The eastern island group of Papua, Maluku, and Nusa Tenggara remains under-served, yet Palapa Ring fiber and LEO-satellite backhaul open new service corridors. Operators deploy solar-powered micro-cells and fixed-wireless access to cover low-density villages. Commercial viability improves once shared-infrastructure leasing cuts the cost of tower deployment by up to 30%. Progress here upholds national digital equity targets and adds incremental subscribers to the Indonesia telecom MNO market, though revenue contribution stays modest through 2030.

Competitive Landscape

Telkomsel leads with 45% subscriber share and top-ranked 5G speeds in all Opensignal categories [3]Opensignal, “Indonesia Mobile Network Experience Report 2024,” opensignal.com . Indosat Ooredoo Hutchison maintains 28% share, leveraging international parentage for capital access and network upgrade support. The combined XL Axiata–Smartfren entity will hold 27%, banking on synergy savings and contiguous spectrum assets to enhance coverage and quality.

Competitive differentiation centers on network-experience leadership, fixed–mobile bundles, and enterprise vertical solutions. Telkomsel bundles cloud security with connectivity for SMEs, leveraging its Telkom Group data-center assets. Indosat pushes digital lifestyle offers through its IM3 brand, pairing music streaming and gaming passes to raise ARPU. XL Axiata’s partnership with Cisco underpins an IoT platform that automates device onboarding, critical for scaling connected-car deals. Regulatory scrutiny ensures service-quality benchmarks and national roaming directives that guard against monopolistic abuse, while upcoming spectrum auctions will shape cost dynamics for the next investment cycle.

Carrier strategies extend to non-connectivity plays such as fintech integration and advertising technology. Telkomsel explores embedded finance with GoTo ecosystem partners, whereas Indosat invests in programmatic ad exchanges. Despite revenue diversification efforts, network reliability remains the primary brand differentiator that drives churn. Sustained capex of about 22% of sales underlines the capital intensity that characterizes the Indonesia telecom MNO market.

Indonesia Telecom MNO Industry Leaders

PT XL Axiata Tbk

PT Telekomunikasi Selular (Telkomsel)

PT Indosat Tbk(IndosatOoredoo Hutchison)

PT SmartfrenTelecom Tbk (SinarmasBusiness Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: XL Axiata completed its USD 6.5 billion merger with Smartfren, forming XLSmart with 94.5 million subscribers and IDR 45.4 trillion revenue

- February 2025: Axiata Group and Sinar Mas signed memoranda covering 5G solutions and fintech innovation ahead of the merger closing

- October 2024: Ericsson has unveiled the ‘Ericsson Hackathon 2024’ to drive digital transformation in Indonesia, leveraging Generative Artificial Intelligence (Gen AI) and 5G technology. This initiative is a joint venture with the Ministry of Industry, PIDI 4.0, Ministry of Communication and Digital, Innovation & Learning Centers, Swiss German University, and KORIKA. The hackathon will stimulate innovation and collaboration, further propelling the telecom market in Indonesia.

- January 2024: Aviat Networks, Inc., a player in wireless transport and access solutions, has entered into a strategic collaboration with PT Smartfren Telecom Tbk. This partnership aims to provide high-speed, ultra-reliable wireless connectivity, both indoor and outdoor private wireless networks, and services for digitalization and automation to private network customers throughout Indonesia. The collaboration seeks to capitalize on market opportunities, bolster competitive positioning, and enhance service to Indonesian clients. This will be achieved through pre-sales and solution engineering, joint sales efforts, market opportunity development, and unified customer service and support. Following its acquisition of NEC's Wireless Transport Business, Aviat has emerged as the wireless transport provider in Indonesia, boasting a wide-ranging portfolio of solutions and a robust local presence.

Indonesia Telecom MNO Market Report Scope

Telecommunications, or telecom, refers to the transmission of information over long distances using electromagnetic signals. The study on the Indonesian telecom MNO market includes a detailed analysis of connectivity trends, focusing on fixed networks, mobile networks, and telecom towers.

Telecom services is segmented into (voice services, data and messaging services, over-the-top (OTT) services, and Pay TV services).

The study also examines the impact of macroeconomic trends on the market and impacted segments. The study also discusses the drivers and restraints likely to influence the market's evolution in the near future. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming And International Services, Enterprise And Wholesale Services, etc.) |

End-user

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming And International Services, Enterprise And Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How fast is revenue expected to grow in the Indonesia telecom MNO market through 2031?

Revenue is projected to rise from USD 14.42 billion in 2026 to USD 18.37 billion by 2031, reflecting a 4.95% CAGR.

What share of revenue came from data and internet services in 2025?

Data and Internet Services contributed 53.92% of total revenue, illustrating the dominance of mobile data consumption.

Which operator holds leadership in subscriber share?

Telkomsel leads with 45% of subscribers, supported by the widest 4G coverage and top-ranked 5G speeds.

Why is the enterprise segment important for future growth?

Enterprises show a 5.29% CAGR thanks to cloud adoption, private networks, and rising demand for secure connectivity solutions.

Page last updated on: