Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 12.03 Billion |

| Market Size (2026) | USD 12.48 Billion |

| Market Size (2031) | USD 15.02 Billion |

| Growth Rate (2026 - 2031) | 3.77% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey Telecom MNO Market Analysis by Mordor Intelligence

The Turkey Telecom MNO Market size was valued at USD 12.03 billion in 2025 and estimated to grow from USD 12.48 billion in 2026 to reach USD 15.02 billion by 2031, at a CAGR of 3.77% during the forecast period (2026-2031).

The expansion is propelled by resilient mobile‐data demand, sustained pricing power that has lifted blended ARPU by more than 50% year on year, and the ability of operators to defend margins despite persistent hyperinflation. Robust 4.5G coverage, rapid smartphone adoption, and preparations for the August 2025 5G spectrum auction collectively underwrite long-term revenue visibility for every tier-one carrier. Consolidation around three national players enables disciplined capital deployment, while emergent enterprise-IoT opportunities create fresh addressable revenue pools. The Turkey telecom MNO market continues to benefit from the country’s geographic role as a Eurasian data transit hub, giving operators wholesale upside from new terrestrial and subsea routes.

Key Report Takeaways

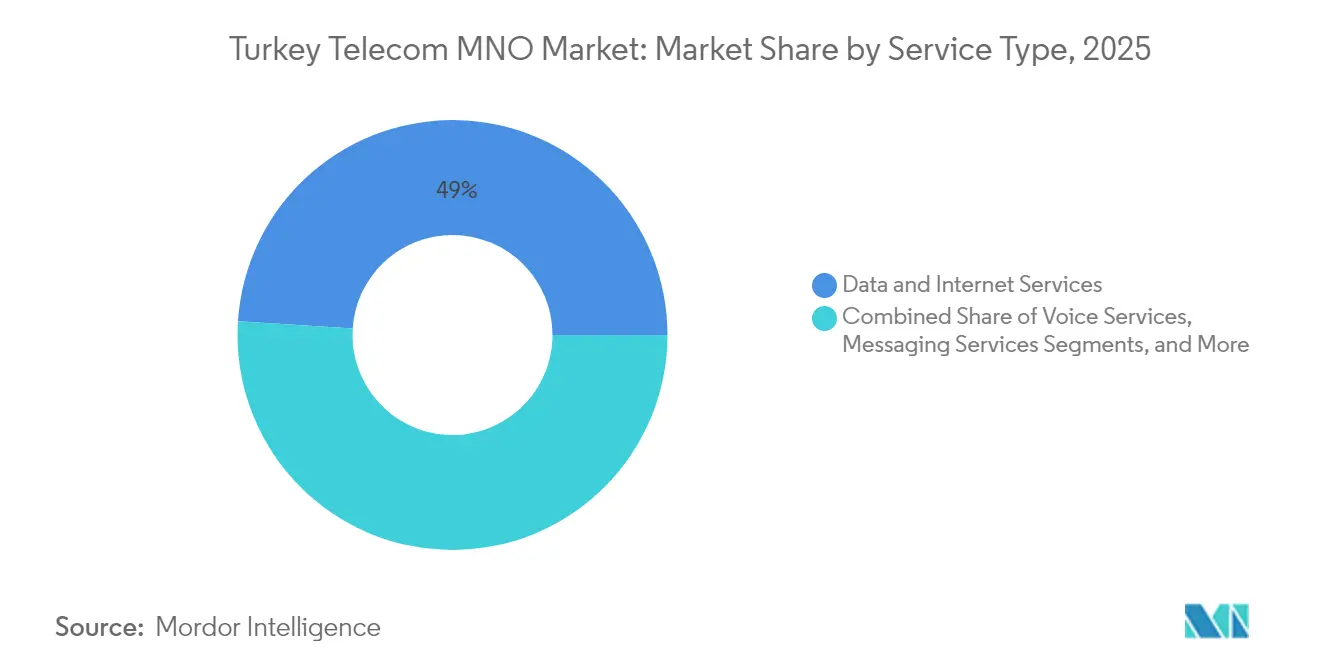

- By service type, data and internet services captured 48.98% of the Turkey telecom MNO market share in 2025, whereas IoT and M2M services are advancing at a 3.84% CAGR through 2031.

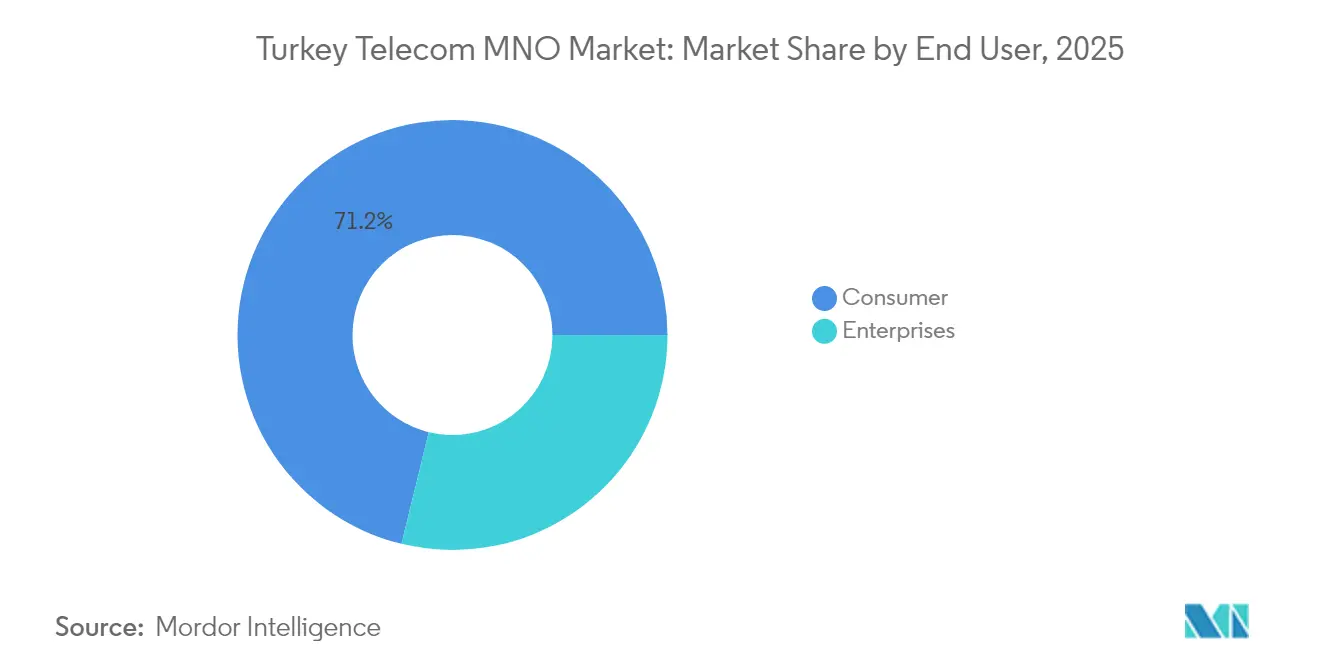

- By end-user, consumer subscriptions accounted for 71.19% of the Turkey telecom MNO market size in 2025; enterprise connections are projected to expand at a 4.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Turkey Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mobile data-traffic boom and nationwide 4.5G coverage | +1.2% | National; strongest in Istanbul, Ankara, Izmir | Medium term (2-4 years) |

| Government-led 5G roadmap and 2025 spectrum auction | +0.8% | National; early rollouts in major urban centers | Short term (≤ 2 years) |

| Enterprise digital-transformation demand for IoT connectivity | +0.6% | Nationwide; industrial zones and smart-city pilots | Long term (≥ 4 years) |

| High smartphone penetration lifting data ARPU | +0.5% | National; rural areas catching up fast | Medium term (2-4 years) |

| New Turkey–Europe submarine cables boosting backhaul capacity | +0.4% | National; vital for international traffic | Long term (≥ 4 years) |

| AI-driven network automation cutting OPEX and enabling new B2B services | +0.3% | National; enterprise-service hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mobile Data-Traffic Boom and Nationwide 4.5G Coverage

Explosive data usage is reshaping revenue composition as carriers pivot from voice toward bandwidth-centric monetization models. Turkcell alone processed more than 6 billion GB over five years, underscoring network stress but also underpinning steady ARPU accretion [1]Bazaartimes Staff, “Over 6 billion GB … with Turkcell’s 4.5G,” Bazaar Times, bazaartimes.com. Comprehensive 4.5G footprints deliver uniform quality-of-service that supports real-time video, mobile gaming, and IoT telemetry, letting operators craft tiered speed plans. Traffic density accelerates the business case for edge-compute nodes that lower latency for augmented-reality and industrial-automation workloads. Continuous capacity upgrades, however, inflate capex, driving a parallel push for sophisticated pricing algorithms and spectrum refarming. The surging traffic also intensifies vendor partnerships focused on massive-MIMO and carrier aggregation to squeeze efficiency from limited spectrum holdings.

Government-Led 5G Roadmap and 2025 Spectrum Auction

The Ministry’s August 2025 auction compresses a decade of spectrum planning into a single milestone that will dictate strategic bandwidth portfolios for all bidders. Pre-qualification criteria encourage domestic R&D links, exemplified by Türk Telekom’s 6G collaboration with Ericsson, to safeguard technological sovereignty. Winning blocks carry rollout obligations across urban and rural zones, adding clarity to business-case modeling and catalyzing capital-market interest. Aligned policy signals also deter fragmentation by choreographing simultaneous nationwide launches, helping operators monetize scale faster than peers in markets with staggered licensing. The auction’s timing amid hyperinflation forces carriers to juggle high spectrum fees with macro-driven funding costs, sharpening focus on network-sharing and neutral-host models to dilute capex shocks.

Enterprise Digital-Transformation Demand for IoT Connectivity

Manufacturers, utilities, and logistics firms are upgrading legacy systems with sensor networks and analytics platforms that depend on carrier-grade connectivity. Dedicated network slices and guaranteed-latency SLAs command premium pricing, lifting enterprise ARPU well above consumer averages. Operators respond by bundling connectivity with device management, cybersecurity, and API integration, thereby moving up the value stack. Smart-city pilots in Izmir and Bursa illustrate the pull-through effect: once connectivity is in place, carriers upsell video analytics and cloud storage. Long-term contracts mitigate churn risk and smooth cash flows, providing a hedge against consumer-segment volatility. BTK’s eSIM compliance rules add clear standards, accelerating adoption and letting carriers lock in recurring license revenue while protecting numbering resources.

High Smartphone Penetration Lifting Data ARPU

Turkey now exhibits smartphone penetration exceeding 90%, transforming traffic profiles toward high-definition video and cloud gaming. Rich device capabilities allow carriers to introduce service-tier differentiation, such as unlimited social-media bundles, that monetize specific usage clusters [2]Digital TV News Editorial, “Inflation driving telecommunication services revenue growth,” Digital TV News, digitaltvnews.net . Improved antenna technologies embedded in flagship handsets boost spectral efficiency, reducing the marginal cost of each additional gigabyte and sustaining gross margins. Saturation shifts the competitive lens to experience quality and loyalty programs rather than net-add races. Consequently, investment emphasis pivots to customer analytics engines that detect churn signals and enable personalized upsell offers. The mature device base also furnishes anonymized sensor data that carriers leverage for network optimization, lowering OPEX and reinforcing the value proposition of premium data tiers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyper-inflation squeezing consumer spending on telecom | −0.9% | Nationwide; heavier in rural, low-income districts | Short term (≤ 2 years) |

| Regulatory delays and uncertainty around 5G licensing fees | −0.4% | Nationwide; impacts all carriers’ rollout calendars | Medium term (2-4 years) |

| Rising tower-lease costs from seismic retrofitting mandates | −0.3% | Nationwide; acute in earthquake zones | Long term (≥ 4 years) |

| Emerging LEO-satellite broadband substituting rural mobile data | −0.2% | Sparsely populated eastern provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hyper-Inflation Squeezing Consumer Spending on Telecom

With headline inflation oscillating above 40%, disposable incomes lag tariff adjustments, pushing prepaid users toward smaller data bundles or opportunistic SIM swapping. Operators have countered with frequent micro-top-up promotions and loyalty perks, yet churn risk remains elevated in low-income cohorts [3]Digital TV News Editorial, “Inflation driving telecommunication services revenue growth,” Digital TV News, digitaltvnews.net . Inflation also inflates energy and site-maintenance costs, eroding EBITDA despite nominal revenue growth. Despite the squeeze, mobile connectivity is deemed essential, enabling carriers to introduce quarterly price revisions without inciting mass disconnections. Successful navigation hinges on advanced segmentation analytics that calibrate price elasticity by region and socioeconomic bracket, allowing revenue yields to outpace CPI while keeping churn within historical norms.

Regulatory Delays and Uncertainty Around 5G Licensing Fees

Elapsed time between policy announcements and final license terms has lengthened business-case paybacks and muddied debt-capital planning. Spectrum cost opacity complicates vendor negotiations, forcing provisional equipment contracts with escalation clauses that add financial risk. Delays defer commercial 5G launches, letting neighboring EU markets steal an innovation march, which can divert multinational enterprise demand toward cross-border roaming or private-network imports. Financing uncertainty dampens appetite among foreign investors for tower-sale-and-leaseback deals that normally release cash for spectrum fees. Operators mitigate by trialing non-stand-alone 5G in existing bands, keeping consumer excitement alive while hedging regulatory timing risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Revenue Transformation

Data and Internet services accounted for 48.98% of the Turkey telecom MNO market size in 2025, reflecting an accelerated pivot from voice to bandwidth monetization. The segment keeps expanding on the back of streaming video, cloud productivity tools, and gaming traffic, and it remains the anchor for upselling unlimited and speed-tiered plans. Voice revenues continue to decline in absolute terms but serve as customer-retention glue inside converged bundles that include messaging, video, and storage add-ons. Messaging sits in structural decline as OTT platforms cannibalize legacy SMS, yet operators have stabilized volumes by promoting RCS for enterprise-to-customer alerts. IoT and M2M services, while still single-digit contributors, outpace every other line with a 3.84% CAGR. The opportunity centers on industrial automation, fleet tracking, and smart-city deployments, each supported by network-slice capabilities under test in Ankara and Izmir. OTT and PayTV solutions round out the portfolio, letting carriers leverage content partnerships to grow average revenue per household and diversify away from pure mobile-only accounts. Other services, such as roaming, cloud storage, and cybersecurity consulting, add high-margin ancillary streams that cushion inflation-driven OPEX spikes.

Sustained data-traffic elasticity means even modest tariff increases translate into outsized revenue gains, underscoring why every operator directs over 60% of annual capex to capacity upgrades and fiber backhaul. Differential quality of service packages give incumbents room to upsell, especially now that traffic management tools embedded in 5G-ready RAN software can guarantee latency for premium mobile-gaming tiers. The impending auction will widen frequency holdings, enabling contiguous spectrum blocks that support 5G Stand-Alone and unlock network-slice monetization for IoT. As ARPU skews higher toward data-heavy postpaid accounts, the Turkey telecom MNO market builds a buffer against future regulatory price caps and recession-induced volume dips. That trajectory anchors investor confidence in sustained free-cash-flow expansion even in an inflationary macro context.

By End-User: Enterprise Growth Accelerates Digital Transformation

Consumer subscriptions still deliver scale, representing 71.19% of the Turkey telecom MNO market share in 2025. Growth, however, is maturing as penetration nears 100% of the addressable population, prompting a shift from acquisition to wallet-share capture. Operators, therefore, bundle mobile with fixed broadband, PayTV, and cloud storage to raise ARPU and lower churn. Loyalty programs and family data pools further reinforce stickiness. Yet competition intensifies on experiential factors such as video streaming quality and gaming latency, areas where network densification and edge caching play decisive roles. Hyperinflation adds complexity, compelling carriers to tailor bite-sized daily data options that cater to compressed consumer budgets while preserving headline ARPU growth.

Enterprises, by contrast, are the fastest-growing cohort, expanding at a 4.05% CAGR owing to Industry 4.0 projects and government smart-city grants. Dedicated connectivity for manufacturing execution systems, real-time asset monitoring, and connected-vehicle platforms attracts premium pricing, raising enterprise ARPU to more than 3× consumer levels. Contract tenures averaging three years reduce revenue volatility and support stable cash-flow projections. Edge-compute nodes sited at industrial parks shorten latency for automated-guided vehicles and robotics, turning operators into strategic partners rather than commodity bandwidth suppliers. These dynamics prompt specialized sales units within each carrier, focusing on verticals such as logistics, energy, and public safety, complete with tailored SLAs and integrated analytics dashboards. As 5G Stand-Alone arrives, private network slices will further entrench operator relevance in enterprise digital roadmaps, consolidating a high-margin pillar within the Turkey telecom MNO market.

Geography Analysis

Istanbul, accounting for more than one-third of the Turkey telecom MNO market size, remains the epicenter of high-value traffic and technology pilots. The city’s dense business districts and affluent consumer base support early adoption of premium 5G handsets and high-throughput enterprise solutions, justifying aggressive small-cell densification and edge-cloud deployments. Ankara and Izmir follow as secondary nodes, driven by a concentration of government agencies, defense contractors, and export-oriented manufacturers that demand resilient, low-latency networks. Seasonal tourism corridors from Antalya to Bodrum boost summer traffic, prompting dynamic capacity reallocation tools that protect user experience while maximizing yield pricing.

Rural Anatolian provinces reveal a contrasting picture where terrestrial build-outs remain economically challenging. Türk Telekom’s fiber push, laying 100 kilometers per day, prioritizes underserved localities, aiming to leverage universal-service funding and minimize BTK penalty exposure for coverage gaps . Where towers are sparse, operators experiment with satellite backhaul and shared-infrastructure consortia to contain costs. Meanwhile, global LEO constellations start to nibble at uncapped rural data demand, nudging carriers toward hybrid-access bundles that combine terrestrial voice with satellite broadband to defend market share.

International connectivity confers strategic leverage. New subsea systems, including the Sparkle–Turkcell link and the BlueMed project, position Turkey as a Mediterranean data crossroads, funneling European and Middle Eastern traffic through carrier landing stations. Terrestrial corridors, such as the 1,850-kilometer SOCAR Fiber route, diversify transit paths, improving resiliency and catering to hyperscale cloud providers seeking multi-region presence. Wholesale revenues from these projects underpin capex for domestic last-mile upgrades, creating a virtuous investment cycle that reinforces Turkey’s role as a digital bridge.

Competitive Landscape

Turkey’s mobile market is an oligopoly: Turkcell, Vodafone, and Türk Telekom collectively command over 95% of subscriptions, driving disciplined competition anchored in technology differentiation rather than price wars. Turkcell leverages aggressive virtualization targets, 40% of network functions by 2025, to lower OPEX and launch cloud-native services rapidly, positioning itself as a digital-services platform. Vodafone Turkey focuses on customer-experience metrics, integrating AI bots for care interactions and rolling out loyalty partnerships such as the Hepsiburada rewards scheme to lock in high-value postpaid users. Türk Telekom leverages nationwide fiber assets to bundle fixed and mobile propositions, exploiting cross-selling opportunities in enterprise ICT contracts and public-sector digitalization projects.

Collaborative R&D is surfacing as the next battleground. The Ericsson-Türk Telekom 6G pact and the Turkcell-Huawei 5G-Advanced MoU exemplify vendor-operator co-innovation aimed at lowering time-to-market for latency-sensitive services such as holographic conferencing. Edge computing footprints, often colocated within carrier central offices, are being opened to third-party developers, signaling a platform approach where revenue is shared across connectivity and application layers. Infrastructure sharing, historically limited, is gaining traction under inflationary pressure; passive tower joint ventures are under evaluation, promising capex savings of up to 30% over standalone builds.

Regulation acts as both a moat and a motivator. BTK’s 0.2% revenue penalty for coverage laps incentivizes incumbents to maintain nationwide service quality, raising a barrier for any would-be entrant lacking large-scale capital reserves. Simultaneously, the looming cybersecurity law mandates data localization and pushes carriers toward domestic cloud partnerships, influencing vendor selection and network-architectural choices. In net terms, sustained high barriers and sticky subscriber bases suggest the Turkey telecom MNO market will remain a three-horse race for the medium term.

Turkey Telecom MNO Industry Leaders

Turkcell Communication Services Inc.

Türk Telekom

Vodafone Turkey

Netgsm

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Turkcell and Huawei signed a comprehensive MoU covering 5G-Advanced and quantum-key-distribution research at MWC 2025.

- March 2025: Ericsson and Türk Telekom entered a 6G collaboration agreement during MWC 25, positioning Turkey for early-stage 6G trials.

- March 2025: Sparkle and Turkcell signed an MoU to develop new subsea cable projects linking Turkey with southern Europe, boosting international capacity.

- January 2025: Turkcell hosted the ITU’s inaugural AI-Native Networks working meeting in Istanbul, underscoring the operator’s leadership in automation research.

Turkey Telecom MNO Market Report Scope

The Turkish telecom MNO market study tracks the revenues generated through the sale of various telecom services (data, voice, messaging, roaming, etc.) provided by major telecom companies to end users (consumers and enterprises) in Turkey.

The Turkish telecom MNO market is segmented by telecom services (voice services (wired, wireless), data and messaging services, OTT and payTV services). The report offers market forecasts and size in value (USD) for all the above segments.

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

End-user

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the current value of the Turkey telecom MNO market?

The market is worth USD 12.48 billion in 2026 and is projected to hit USD 15.02 billion by 2031.

How fast is the market expected to grow?

It is forecast to advance at a 3.77% CAGR between 2026 and 2031.

Which service type generates the most revenue?

Data and Internet services lead with 48.98% share of total revenue in 2025.

Who are the key players?

Turkcell, Vodafone Turkey, and Türk Telekom jointly hold more than 95% of subscriptions.

When will Turkey hold its 5G spectrum auction?

The national 5G auction is scheduled for August 2025.

Which end-user segment is growing the fastest?

Enterprise connections are expanding at a 4.05% CAGR due to IoT and digital-transformation projects.

Page last updated on: