Greece Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

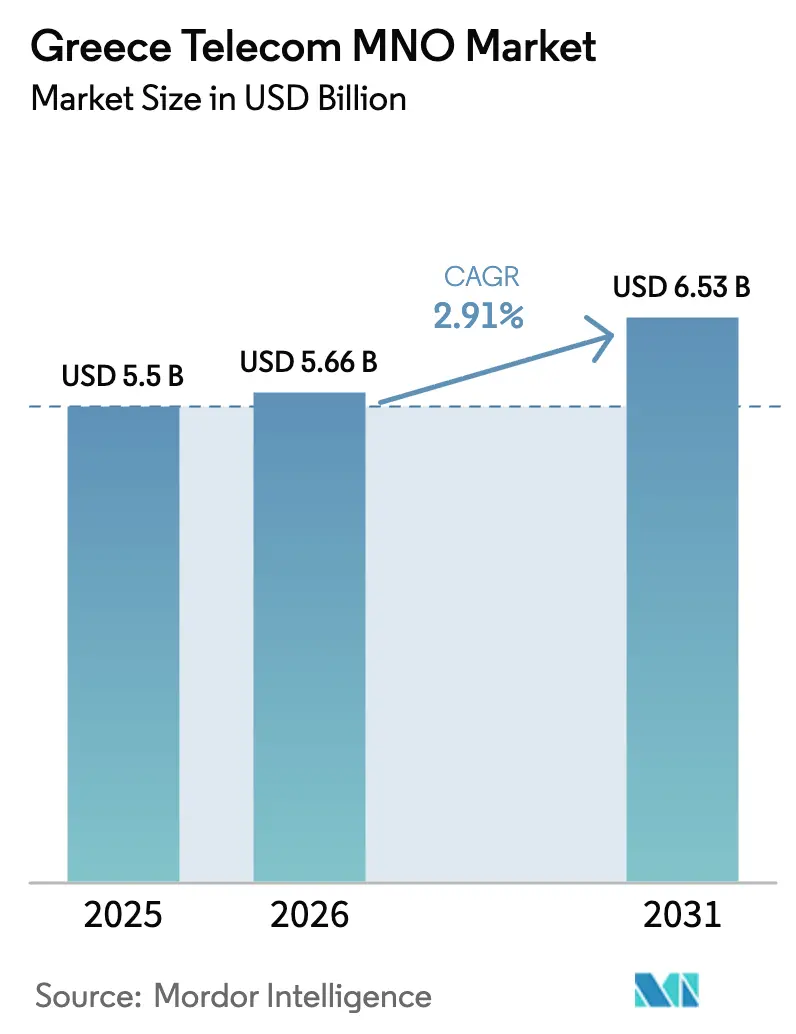

| Base Year Market Size (2025) | USD 5.5 Billion |

| Market Size (2026) | USD 5.66 Billion |

| Market Size (2031) | USD 6.53 Billion |

| Growth Rate (2026 - 2031) | 2.91% CAGR |

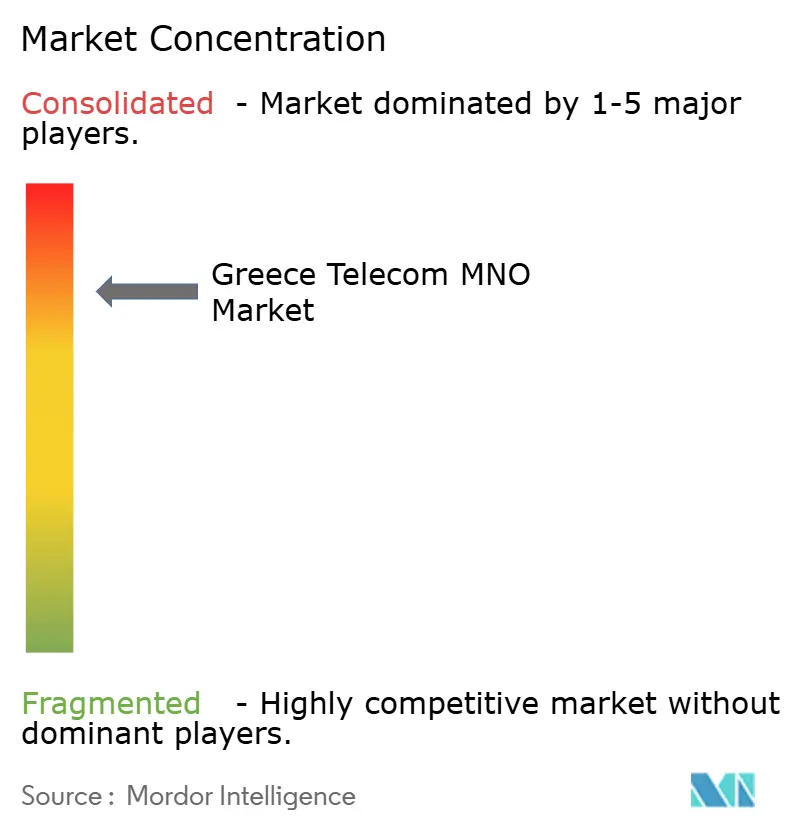

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Greece Telecom MNO Market Analysis by Mordor Intelligence

The Greece Telecom MNO Market size in 2026 is estimated at USD 5.66 billion, growing from 2025 value of USD 5.5 billion with 2031 projections showing USD 6.53 billion, growing at 2.91% CAGR over 2026-2031.

Although growth is modest, the Greece telecom MNO market benefits from high-value service pivots, particularly in enterprise connectivity, converged bundles, and 5G monetization. Government backing through the EUR 6.4 billion digital transformation plan and EU Recovery and Resilience Fund allocations lowers infrastructure risk and stimulates demand, setting the Greece telecom MNO market apart from regional peers. Technical leadership is evident: Greece topped Europe’s 5G standalone speed league at 547.52 Mbps in 2024, allowing operators to charge premium prices and raise ARPU. Accelerated fiber roll-outs, IoT demand, and data-center-driven wholesale backhaul collectively reinforce the long-term resilience of the Greece telecom MNO market despite energy-cost inflation and wholesale-rate cuts.

Key Report Takeaways

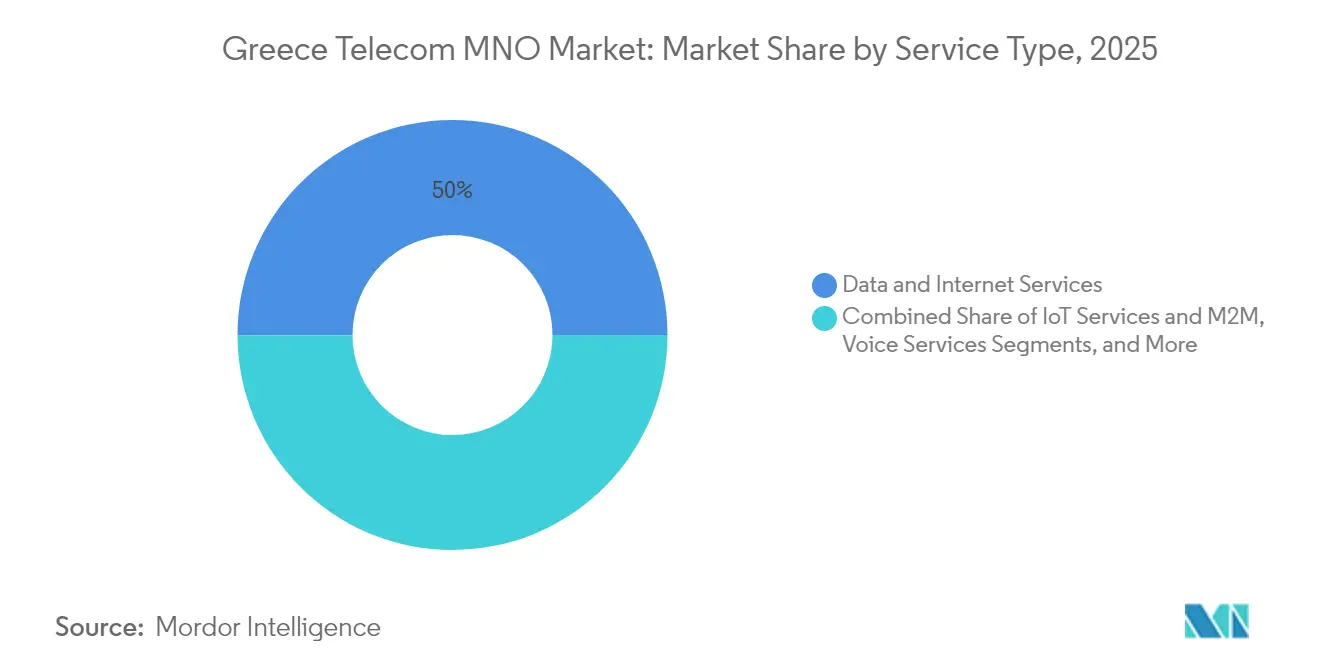

- By service type, data and internet commanded 50.04% of the Greece telecom MNO market share in 2025.

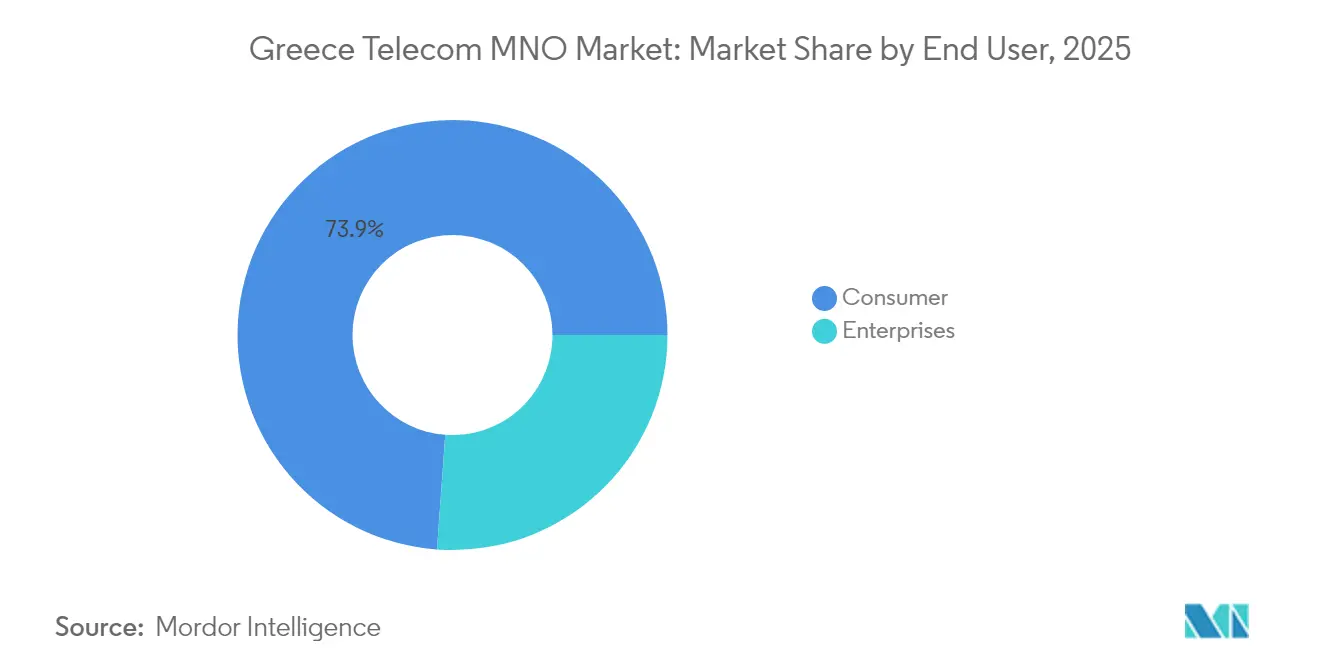

- By end-user, enterprises are advancing at a 3.28% CAGR through 2031, while consumers retained a 73.85% revenue share of the Greece telecom MNO market size in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Greece Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G rollout and spectrum monetization | +1.2% | National; strongest in Athens and Thessaloniki | Medium term (2-4 years) |

| Government-funded Ultrafast Broadband push | +0.8% | Nationwide; rural priority | Long term (≥ 4 years) |

| Enterprise appetite for managed IoT | +0.6% | Athens; national spill-over | Medium term (2-4 years) |

| Converged bundles lift ARPU | +0.4% | Urban centers | Short term (≤ 2 years) |

| Athens data-center boom | +0.3% | Athens metro; Thessaloniki | Medium term (2-4 years) |

| EU RRF island fiber and microwave subsidies | +0.2% | Aegean and Ionian islands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid 5G rollout and spectrum monetization

The Greece telecom MNO market enjoys 98.1% 5G population coverage, the highest in the EU, enabling operators to upsell faster data tiers and edge-enabled applications. Additional spectrum across 700 MHz, 3.6 GHz, and 26 GHz creates capacity for enhanced mobile broadband, massive IoT, and ultra-reliable low-latency use cases.[1]European 5G Observatory, “Greece 5G Deployment Update,” 5gobservatory.eu, 5GOBSERVATORY.EU A EUR 1 –1.5 billion 5G capex pipeline through 2030 signals unwavering investment commitment. These factors allow premium pricing, reduce churn, and consolidate the competitive moat of the Greece telecom MNO market.

Government-funded Ultrafast Broadband push

Public funding shifts infrastructure risk away from operators. Of the EUR 6.4 billion digital plan, EUR 700 million is earmarked for broadband networks, while a EUR 200 voucher per household stimulates adoption. OTE’s plan to pass 2.1 million homes with fiber by 2025, underpinned by an EUR 150 million EBRD loan, illustrates how subsidies accelerate roll-outs. [2]European Bank for Reconstruction and Development, “EBRD Backs OTE FTTH,” ebrd.com, EBRD.COM The resulting take-up fuels data-premium growth and fortifies the Greece telecom MNO market.

Enterprise appetite for managed IoT connectivity

Global IoT links rose to 3.8 billion in 2024 and head toward 6.4 billion by 2029, a trajectory mirrored in Greece as enterprises demand secure, managed services. Deutsche Telekom’s global tariff suite, available via OTE, permits pooled data, multi-network fallback, and energy-efficient LTE-M, upping stickiness among shipping and tourism clients. Athens’ data-center boom adds low-latency edge nodes, cementing IoT as a strategic revenue pillar for the Greece telecom MNO market.

Converged bundles lift ARPU

Nova’s fiber-plus-EON TV plans and Vodafone’s fixed-mobile-Pay-TV line-ups prove that triple-play packs lengthen contract terms and reduce churn. With prepaid price wars eroding standalone margins, converged offers are key to defending profitability in the Greece telecom MNO market. OTE’s 2025 rebrand to “Cosmote Telekom” aligns with Deutsche Telekom’s integrated platform, paving the way for content-rich bundles that lift household spend.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flat population growth and aging user base | -0.7% | National; acute in rural areas | Long term (≥ 4 years) |

| Price wars and wholesale-rate cuts | -0.5% | Nationwide; urban concentration | Short term (≤ 2 years) |

| Slow municipal permitting of small cells | -0.3% | Athens and Thessaloniki | Medium term (2-4 years) |

| Rising energy costs for 5G densification | -0.2% | National; high-density zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Flat population growth and aging user base

Low birth rates and youth emigration shrink the addressable subscriber pool and tilt usage toward basic connectivity. This demographic squeeze pushes operators to extract more value per user through higher-tier data plans and family bundles. The aging cohort’s lower data appetite dampens ARPU growth, compelling the Greece telecom MNO market to diversify into enterprise and IoT niches where volumes outpace population trends.

Price wars and wholesale-rate cuts

BEREC’s wholesale cost-model revisions and the European Commission’s push for lower voice-termination fees compress margins. New low-cost entrants spark prepaid price skirmishes, forcing incumbents to sacrifice headline tariffs to defend share. [3]Body of European Regulators for Electronic Communications, “Wholesale Termination Rates 2025,” berec.europa.eu, BEREC.EUROPA.EU While consumers win, the Greece telecom MNO market must offset lost revenue via premium 5G tiers, enterprise contracts, and digital upsells.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Leadership Shapes Revenue Mix

Data and internet lines captured 50.04% of the Greece telecom MNO market in 2025, underscoring the move away from voice and SMS. With IoT and M2M set to grow at 2.98% CAGR until 2031, data-centric monetization remains non-negotiable. The Greece telecom MNO market size for data-driven segments is expected to expand further as operators introduce low-latency 5G-edge offerings. Voice retains a loyal base but faces OTT cannibalization, while messaging revenues erode amid WhatsApp dominance. OTT video and Pay-TV, bundled inside converged packs, now anchor ARPU uplift strategies. Operators leverage 26 GHz millimeter-wave for fixed-wireless access, advancing household penetration in rural zones. Other value-added services such as roaming, wholesale backhaul, and cloud security add margin headroom, reinforcing the Greece telecom MNO market’s multi-service earnings profile.

Even at modest growth, the segment’s scale acts as a cash generator, underwriting 5G capex. The Greece telecom MNO market share held by data services is poised to climb as FTTH adoption and voucher subsidies translate into higher traffic per user. Success hinges on differentiated content agreements, network slicing for enterprise SLAs, and flexible tiered data plans that align usage with willingness to pay.

By End-User: Enterprise Upswing Balances Consumer Saturation

Consumers still contributed 73.85% of 2025 revenue, yet enterprise lines outpace them at a 3.28% CAGR, highlighting a structural pivot inside the Greece telecom MNO industry. Enterprise demand is buoyed by cloud migration, shipping telematics, and tourism analytics requiring secure, low-latency circuits. The Greece telecom MNO market size for enterprise services is forecast to reach USD 1.75 billion by 2031, reflecting tailwinds from Recovery Fund e-procurement projects. Contract lengths average three years versus 12 months in consumer plans, improving visibility. Bundled solutions—SD-WAN, managed Wi-Fi, and cybersecurity—allow operators to upsell beyond connectivity.

On the consumer side, demographic headwinds and intense prepaid competition weigh on unit revenues, but family bundles and device-financing schemes soften churn. Operators segment the silver-age demographic with simplified UI handsets and health-monitoring add-ons, an approach that shields the Greece telecom MNO market from ARPU erosion. Nonetheless, the enterprise growth engine remains the most dependable lever to sustain top-line momentum through 2031.

Geography Analysis

Athens anchors traffic and revenue, benefiting from hyperscale data-center builds by Microsoft and Digital Realty that elevate wholesale backhaul demand. The Greece telecom MNO market thrives on the capital’s dense fiber grid, permitting rapid 5G SA roll-outs and flag-ship edge-computing showcases for shipping and fintech clients. Thessaloniki mirrors this trajectory with university-driven tech clusters that spur IoT pilot uptake and require robust mobile-access redundancy.

Rural mainland and island regions have historically lagged because of challenging topography and thin populations; however, Recovery and Resilience Facility grants earmarked for island fiber and microwave links are closing the digital divide. The Greece telecom MNO market size attributable to rural zones is forecast to inch upward as voucher-subsidized households migrate to 100 Mbps tiers. Operators employ 700 MHz spectrum for wide-area ruralesque coverage while targeting tourist hot-spots with 3.6 GHz capacity to accommodate seasonal spikes.

Crete and Cyprus cables, spearheaded by Grid Telecom partnerships, reinforce Greece’s role as a Eurasian traffic gateway. New landing stations reduce latency to Middle-East IXPs, enhancing the Greece telecom MNO market’s wholesale proposition and attracting OTT players seeking diversity from traditional north-south European routes. Collectively, balanced urban innovation and rural inclusion underpin a geographically diversified revenue outlook through 2030.

Competitive Landscape

The Greece telecom MNO market hosts three principal operators—OTE S.A, Vodafone Greece, and Nova. Combined, the trio controls roughly 95% of mobile revenue, reflecting high concentration yet vigorous rivalry. OTE defends leadership with EUR 3 billion FTTH capex and an evaluated tower spin-off that will re-route capital to 5G densification. Vodafone commits EUR 1 billion to network upgrades through 2029, targeting enterprise fixed and IoT verticals. Nova, backed by United Group refinancing rounds, leverages EON TV content to push converged bundles but struggles with customer-experience gaps.

Infrastructure sharing via VICTUS Networks lowers site-duplication opex for Vodafone and Nova, allowing spectrum parity with OTE while preserving balance-sheet headroom. Technology trajectories focus on standalone 5G, AI-driven automation, and network slicing. Deutsche Telekom’s AI alliance positions OTE for predictive maintenance and hyper-personalized plans, sharpening its edge in the Greece telecom MNO market. Energy-cost inflation and stricter environmental norms press all players to adopt solar-powered cell-sites and liquid-cooling data rooms, ensuring compliance and opex savings.

Strategically, operators diversify into managed cloud, cybersecurity, and paid-TV aggregations to hedge pure-play mobile exposure. Wholesale backhaul to hyperscalers, enterprise SLAs for shipping routes, and rural FWA packages form new revenue pillars. Despite regulatory wholesale-rate cuts, differentiated QoS and service packaging preserve margin resilience in the Greece telecom MNO market.

Greece Telecom MNO Industry Leaders

OTE S.A

Vodafone Greece

Nova Greece

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Vodafone Greece unveiled a EUR 1 billion plan to expand fiber and 5G through 2029, underlining long-term network leadership ambitions.

- April 2025: OTE Group adopted “Cosmote Telekom” branding, aligning with Deutsche Telekom’s integrated service strategy.

- October 2024: United Group refinanced EUR 600 million notes with a new EUR 750 million issue to fund Nova’s Greek expansion.

- August 2024: Grid Telecom and Tamares Telecom announced open-access cable landing in Cyprus to deepen regional connectivity.

Greece Telecom MNO Market Report Scope

Telecom or telecommunication is the long-range transmission of information by electromagnetic means. The Greece telecom MNO market includes in-depth trend analysis based on connectivity, such as fixed networks, mobile networks, and telecom towers. Telecom services are divided into voice services (wired and wireless), data and messaging services, and OTT and pay-TV services. Several factors, including an increasing demand for 5G, are likely to drive the adoption of telecom services.

The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Greece telecom MNO market in 2026?

It generated USD 5.66 billion in revenue during 2026 and is slated to reach USD 6.53 billion by 2031.

What is the projected CAGR for Greek mobile network operators?

The Greece telecom MNO market is expected to grow at a 2.91% CAGR between 2026 and 2031.

Which service category leads operator revenue?

Data and internet services hold 50.04% of total revenue, eclipsing voice and messaging lines.

Where is the strongest geographic growth in Greece?

Athens leads due to data-center investments, while Thessaloniki follows as a regional tech hub.

How are operators addressing rural connectivity gaps?

They combine 700 MHz 5G coverage with Recovery Fund-backed fiber and voucher incentives to serve remote areas.

What drives future enterprise revenue for Greek MNOs?

Managed IoT connectivity, SD-WAN, and cloud-integrated services underpin enterprise ARPU expansion through 2030.

Page last updated on: