Kyrgyzstan Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

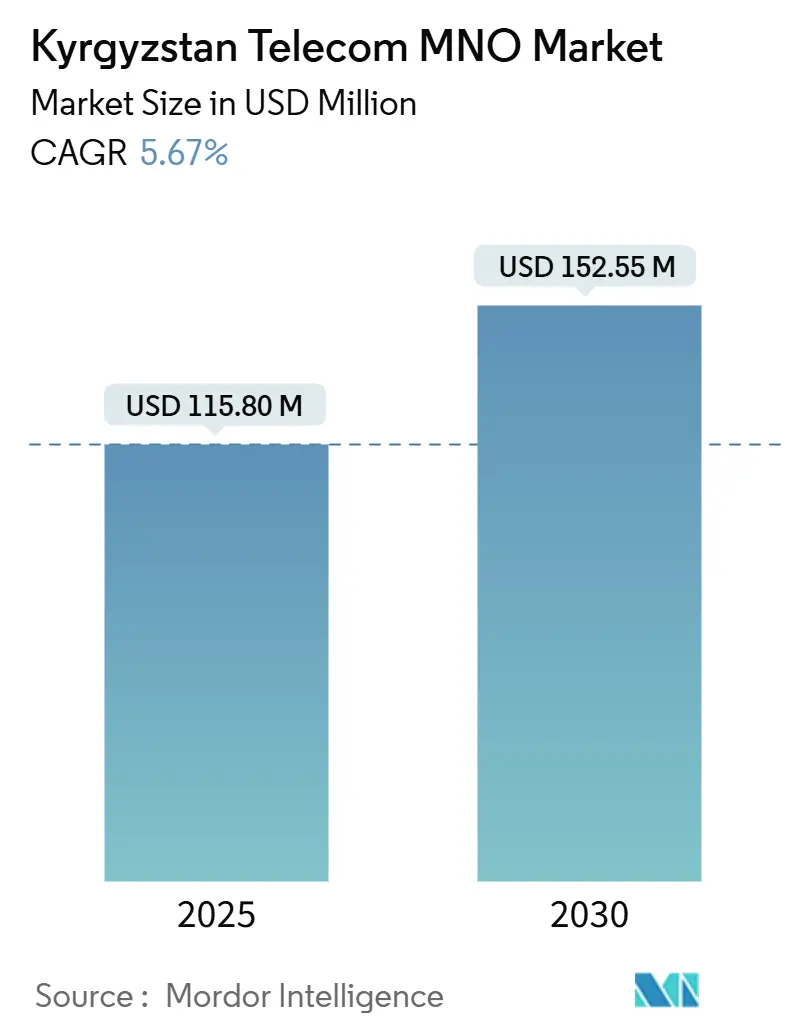

| Market Size (2025) | USD 115.80 Million |

| Market Size (2030) | USD 152.55 Million |

| Growth Rate (2025 - 2030) | 5.67% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kyrgyzstan Telecom MNO Market Analysis by Mordor Intelligence

The Kyrgyzstan Telecom MNO Market size is estimated at USD 115.80 million in 2025, and is expected to reach USD 152.55 million by 2030, at a CAGR of 5.67% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 8.90 million Subscribers in 2025 to 11.90 million Subscribers by 2030, at a CAGR of 5.89% during the forecast period (2025-2030).

Current growth reflects government‐backed digitalization, expanding fibre links, and consumer migration from voice toward data-heavy services. Competitive pressure intensified after VEON’s exit, yet sustained data demand, migrant-funded handset upgrades, and new cross-border transit corridors continue to expand the addressable subscriber base. Enterprise digitalization, spurred by e-government mandates and logistics opportunities linked to the China-Kyrgyzstan-Uzbekistan railway, is reshaping revenue models. Meanwhile, device affordability and near-universal 4G coverage position operators for an orderly 5G transition despite foreign-exchange and topographic cost headwinds.

Key Report Takeaways

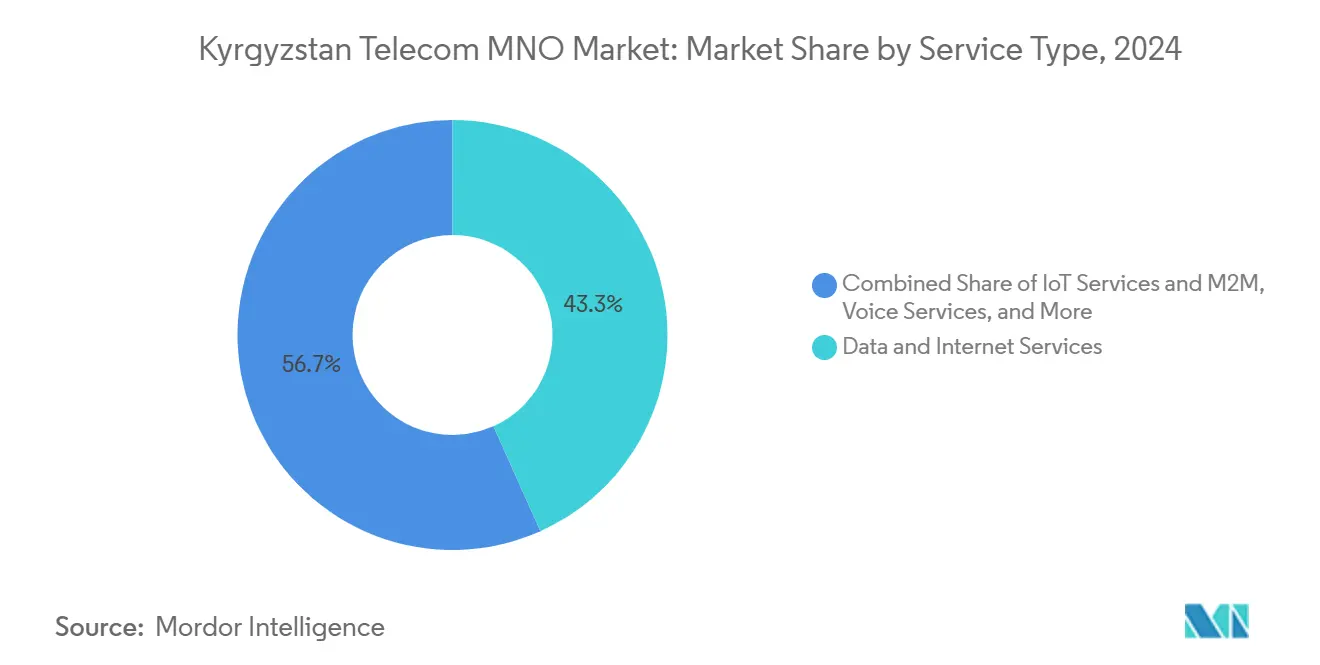

- By service type, data services led with 43.29% Kyrgyzstan telecom MNO market share in 2024 and are projected to post a 5.88% CAGR through 2030.

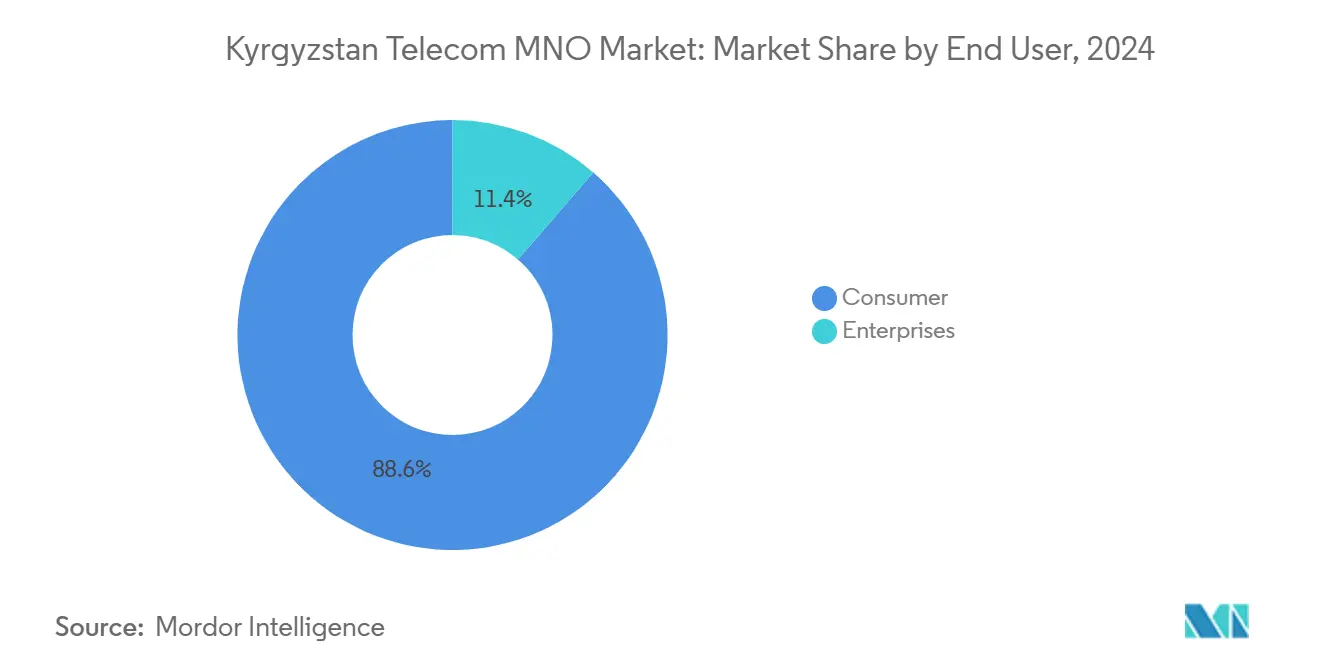

- By end-user, the consumer segment held 88.64% revenue share in 2024, whereas the enterprise segment is expected to expand at 7.08% CAGR to 2030.

Kyrgyzstan Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G spectrum release and affordable smartphone influx | +1.5% | National, with early gains in Bishkek, Osh | Medium term (2-4 years) |

| Surge in video-streaming driven mobile data traffic | +0.8% | National, concentrated in urban centers | Short term (≤ 2 years) |

| National fibre-backbone expansion projects | +1.2% | National, prioritizing rural connectivity | Long term (≥ 4 years) |

| High migrant-remittance cycles accelerating handset upgrades | +0.6% | National, stronger in rural areas | Short term (≤ 2 years) |

| E-government services mandating mobile digital ID linkage | +0.9% | National, government-led adoption | Medium term (2-4 years) |

| Cross-border China–Kyrgyzstan–Uzbekistan fibre corridor revenues | +0.7% | Southern regions, transit corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G Spectrum Release and Affordable Smartphone Influx

Regulators plan to assign new spectrum bands that will enable operators to layer 5G on top of almost nationwide 4G coverage, a transition eased by low-cost Chinese handsets now retailing at sub-USD 100 price points. MegaCom already controls contiguous GSM 900/1800 MHz and LTE B3/B20 holdings, providing an engineering bridge to 5G radio upgrades. [1] MegaCom, “Frequency Holdings and Network Map,” megacom.kgConsumer readiness is high due to elevated multiple-SIM penetration and rising data appetites, but delayed allocation guidelines from the State Communications Agency may moderate the initial pace of sector rollout.

Surge in Video-Streaming Driven Mobile Data Traffic

Social-media and over-the-top video account for the bulk of Kyrgyzstan’s mobile payload. Average plans cost USD 2.70 monthly, a level that keeps price elasticity high and encourages larger data bundles despite thin operator margins. Beeline has introduced tiered packages as large as 100 GB for 700 KGS, showing how players convert screen-time growth into incremental revenue. [2]Beeline Kyrgyzstan, “Tariff Archive,” beeline.kg Urban network cores now carry sustained evening peaks, accelerating investments in content‐delivery nodes and backhaul expansion.

National Fibre-Backbone Expansion Projects

The Digital Kyrgyzstan policy earmarks fibre investments that interlink mountain valleys with urban hubs. International financing packages support kilometres of new ducts, while the concurrent railway build installs optical cables along a 532 km corridor to China and Uzbekistan. Expanded backbones will cut rural latency, lower wholesale IP transit costs, and underpin advanced services such as IoT telemetry for agribusiness.

High Migrant-Remittance Cycles Accelerating Handset Upgrades

Seasonal inflows of overseas earnings lift household spending on smartphones, which in turn pushes data subscription upgrades. Operators execute targeted marketing around peak remittance months to monetise this liquidity bump. Rural users shift from legacy feature phones toward low-range LTE models, raising per-user traffic without dramatic tariff hikes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-war driven ARPU erosion | -1.8% | National, intensified in competitive urban markets | Short term (≤ 2 years) |

| Mountainous terrain inflating rural coverage CAPEX | -0.9% | Rural and remote regions | Long term (≥ 4 years) |

| Forex scarcity constraining network equipment imports | -0.7% | National, affecting all operators | Medium term (2-4 years) |

| Skilled telecom-engineer out-migration | -0.4% | National, concentrated in technical centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price-War Driven ARPU Erosion

VEON’s departure reduced the headline player count yet triggered fiercer pricing battles as remaining operators tried to absorb its base. Kyrgyz plans still average USD 0.17 per GB, far below regional peers, limiting room to fund advanced network elements. The Anti-Monopoly Regulation Service keeps close watch on tariff moves, so operators must extract value from vertical services rather than headline data hikes. [3]Mobile World Live, “VEON to Leave Kyrgyz Market,” mobileworldlive.com

Mountainous Terrain Inflating Rural Coverage CAPEX

Building in high altitudes lifts tower engineering costs by up to threefold compared with flat terrain. Dense 5G cells will require even more sites to navigate ridges and valleys, raising the capital burden. Smaller players therefore tread carefully in rural rollouts, sometimes piggybacking on MegaCom’s passive infrastructure. Without targeted subsidies or sharing frameworks, national coverage targets will stretch operator balance sheets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data and Internet Services Expand Revenue Share

Data consumption generated 43.29% of Kyrgyzstan telecom MNO market revenue in 2024 and will compound at 5.88% annually to 2030. The Kyrgyzstan telecom MNO market size attributable to data services is projected at USD 66.1 million by 2030, reflecting video boom, mobile payments, and e-government needs. Voice minutes are sliding year on year as users pivot to IP messaging, while legacy SMS continues to shrink. IoT connections remain minimal today but will benefit from the railway corridor’s freight‐tracking demand. Operators are bundling over-the-top entertainment into premium tiers to lift retention. The ELQR mobile payment rail, launched in 2022, shows how telecom pipes enable financial transactions and create commission revenue. Roaming and wholesale transit traffic will expand as cross-border fibre goes live.

Value-added services such as device insurance and cloud storage now appear in mid-tier offers. Operators also package cybersecurity for small enterprises that migrate to cloud platforms. Taken together, these additions tilt the service mix firmly toward high-margin digital layers that sit on top of core connectivity. Consequently, data’s Kyrgyzstan telecom MNO market share should exceed 50% before 2030 if current adoption trajectories hold.

By End-User: Enterprise Connections Gain Momentum

In 2024 consumers delivered 88.64% of revenue, yet enterprises post a stronger outlook with 7.08% CAGR to 2030. The Kyrgyzstan telecom MNO market size serving business users is expected to double from USD 13.2 million in 2025 to USD 18.7 million by 2030 as companies digitise operations for trade, payments, and cloud workloads. The High Tech Park’s member companies illustrate export-driven data demand, with 36% of their 2024 earnings tied to US clients. Government mandates for mobile digital ID underpin steady corporate take-up of secure connectivity. SMEs increasingly adopt point-of-sale links and cloud accounting, creating sticky monthly contracts for operators.

Consumer growth will persist but at lower velocity, constrained by tight disposable incomes that cap ARPU gains. Remittance cycles continue to refresh devices, yet incremental traffic monetisation requires creative content partnerships and app bundles. By contrast, enterprises show appetite for dedicated links, campus networks, and IoT telemetry, lifting average revenue per line even as volumes remain modest. Hence, business services will represent the fastest-rising slice of Kyrgyzstan telecom MNO market share through the forecast horizon.

Geography Analysis

Urban strongholds dominate high-bandwidth uptake, yet government policy now channels fibre toward underserved valleys. Mobile connections reached 11.5 million in early 2025, equal to 159% penetration, reflecting heavy multi-SIM habits that inflate headline density. Bishkek and Osh absorb the earliest 5G pilots thanks to existing dense site grids. Rural districts still rely on 3G or low-band LTE due to steep backhaul costs, but state loans target microwave and fibre spurs to ninety remote municipalities.

The China-Kyrgyzstan-Uzbekistan railway, under construction since December 2024, threads a new telecom corridor that will cut latency to mainland Chinese exchange points. Border posts at Irkeshtam, Torugart, and the Bedel Pass opening in January 2025 require secure mobile coverage for customs and facial-ID systems. Operators anticipate wholesale transit revenue once the corridor’s fibres interconnect with domestic rings.

Internet resource distribution mirrors economic clusters: Kyrgyztelecom holds the largest IPv4 pool, while private ISPs serve dense city blocks. The Taza Koom programme funds community Wi-Fi and digital literacy courses, aiming for 60% household internet access by 2026. This geographic rebalancing drives incremental tower deployments as operators chase universal‐service incentives. Consequently, national traffic patterns will flatten, allowing the Kyrgyzstan telecom MNO market to rely less on volatile urban peaks.

Competitive Landscape

MegaCom leads the Kyrgyzstan telecom MNO market following VEON’s withdrawal, leveraging its state shareholder to secure licences and negotiate tower sites on government land. The firm controls spectrum across GSM, UMTS, and LTE, giving it a head start toward 5G refarming. Beeline and O! compete on aggressive bundle pricing and youth-oriented branding, which holds consumer churn near 4% per quarter. Saima Telecom runs niche MVNO plays that piggyback on others’ radio access, focusing on expatriate labourers needing low-cost international minutes.

Technology strategies converge on upgrading core networks to standalone 5G readiness while virtualising legacy functions. Operators pilot mobile edge computing for logistics along the railway, testing container-tracking apps with customs agencies. Mobile money ecosystems expand in partnership with commercial banks, and biometric SIM registration feeds data lakes used for credit-scoring microloans. The telecom association coordinates lobbying on right-of-way fees, while the Anti-Monopoly Regulation Service audits tariff filings to prevent coordinated price rises.

Looking ahead, wholesale fibre transit, managed IoT, and enterprise security services represent the biggest white-space revenue pools. Market entrants from neighbouring Kazakhstan monitor entry options, yet the capital intensity of mountain coverage acts as a natural barrier. Consequently, consolidation around three full-service networks is the likely steady-state structure for the Kyrgyzstan telecom MNO market.

Kyrgyzstan Telecom MNO Industry Leaders

MegaCom

Beeline

O!

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: VEON finalized its Kyrgyzstan exit after arranging a Nasdaq listing for Kyivstar, freeing domestic share for local players.

- January 2025: Bedel Pass border crossing opened, boosting telecom demand for customs and logistics.

- December 2024: Construction began on the China-Kyrgyzstan-Uzbekistan railway with USD 8 billion funding, including parallel telecom ducts for cross-border fibre.

- June 2024: Freedom Holding announced Freedom Telecom plans in Kazakhstan, signaling possible regional ripple effects.

Kyrgyzstan Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the projected value of the Kyrgyzstan telecom MNO market by 2030?

The sector is forecast to reach USD 152.55 million by 2030 under a 5.67% CAGR.

Which service type is expanding fastest in Kyrgyz mobile networks?

Data services are growing at 5.88% annually, driven by video streaming and mobile payment adoption.

How did VEON’s exit affect local operators?

VEON’s withdrawal removed an international competitor, letting domestic providers capture additional subscriber share and spectrum resources.

Why are enterprise connections important for future growth?

Business users are adopting secure links, cloud services, and IoT tools, pushing enterprise revenue to rise at 7.08% CAGR through 2030.

What key infrastructure will boost cross-border data traffic?

The China-Kyrgyzstan-Uzbekistan railway corridor includes fibre ducts that will lower latency and open wholesale transit revenue streams for operators.

What challenge does the mountainous terrain pose?

High-altitude sites cost up to three times more to deploy, increasing capital needs for rural coverage and slow 5G densification.

Page last updated on: