Mali Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

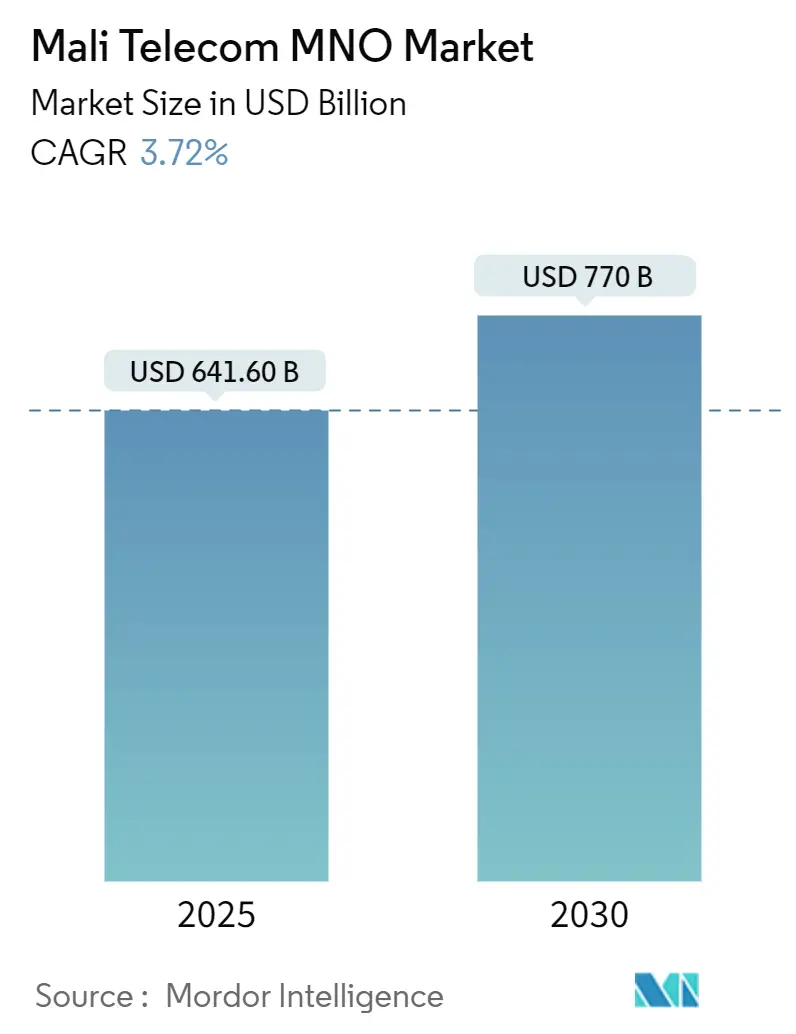

| Market Size (2025) | USD 641.60 Billion |

| Market Size (2030) | USD 770 Billion |

| Growth Rate (2025 - 2030) | 3.72% CAGR |

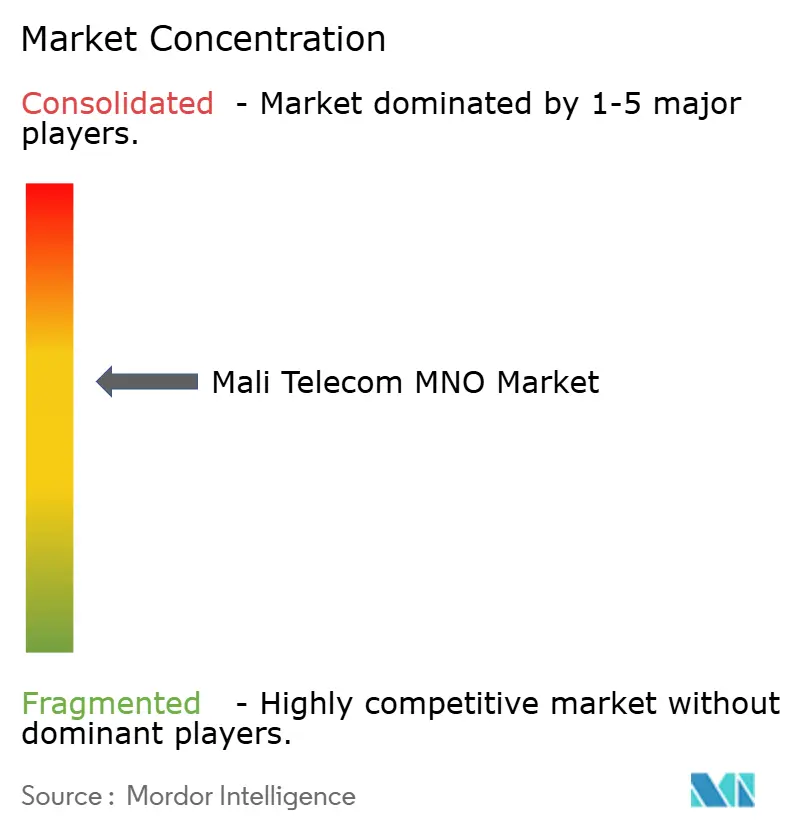

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mali Telecom MNO Market Analysis by Mordor Intelligence

The Mali Telecom MNO Market size is estimated at USD 641.60 billion in 2025, and is expected to reach USD 770 billion by 2030, at a CAGR of 3.72% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 24.86 million subscribers in 2025 to 29.32 million subscribers by 2030, at a CAGR of 3.35% during the forecast period (2025-2030).

The growth path is restrained by political volatility, fiscal pressure and patchy infrastructure, yet it benefits from expanding fiber backbones and accelerating mobile-data uptake. Orange’s 59% command of active SIMs, alongside Malitel’s 41%, creates a tightly held structure that limits tariff‐based rivalry even as regulatory reform inches forward. The recapture of a 56% stake in Sotelma-SA by the government underscores a shift toward state-directed digital sovereignty that echoes across francophone West Africa.

Back-of-the-network improvements are gathering momentum through cross-border fiber projects with Guinea and Senegal that lower IP transit costs and diversify away from a single coastal landing point. Mobile money penetration now reaches 66% of the population, fostering data monetization synergies and spawning new fintech-connectivity bundles. Yet recent telecom-specific taxes save operator margins at a time when chronic grid outages already drive high backup-power spend, pressing carriers to adopt solar-hybrid energy solutions backed by multilateral lenders.

Key Report Takeaways

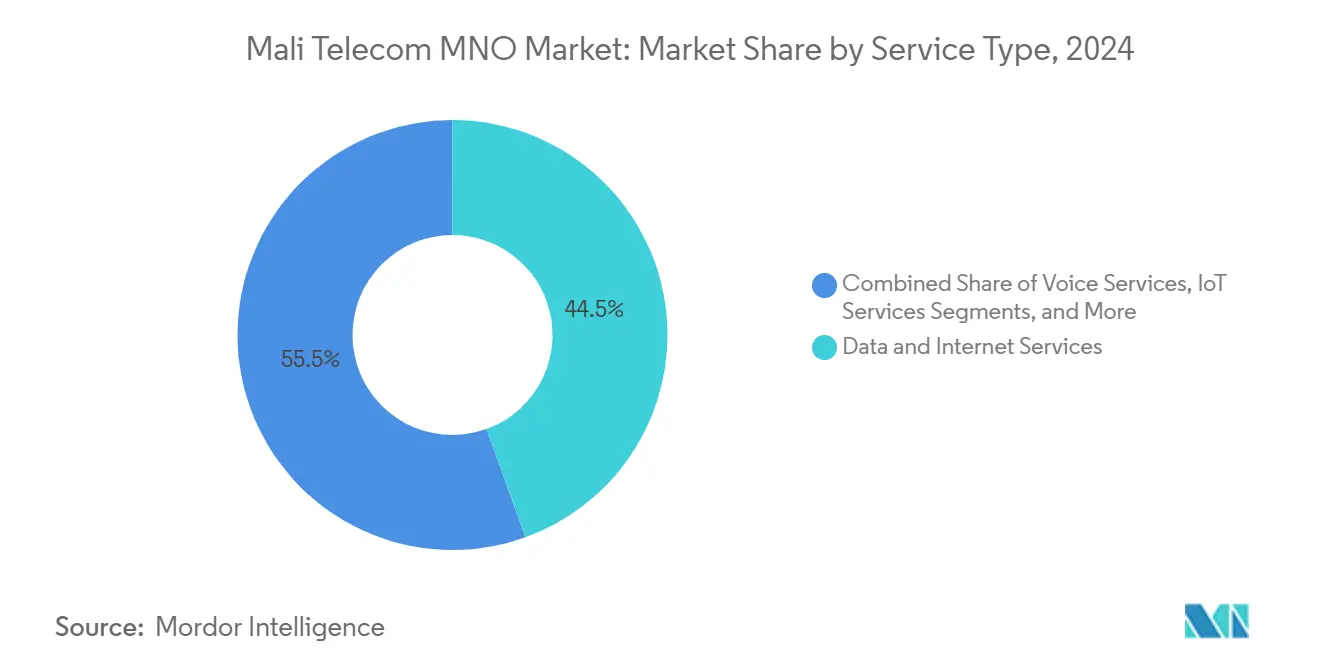

- By service type, data services held 44.49% of 2024 revenue, while IoT services are projected to post the fastest 3.70% CAGR to 2030.

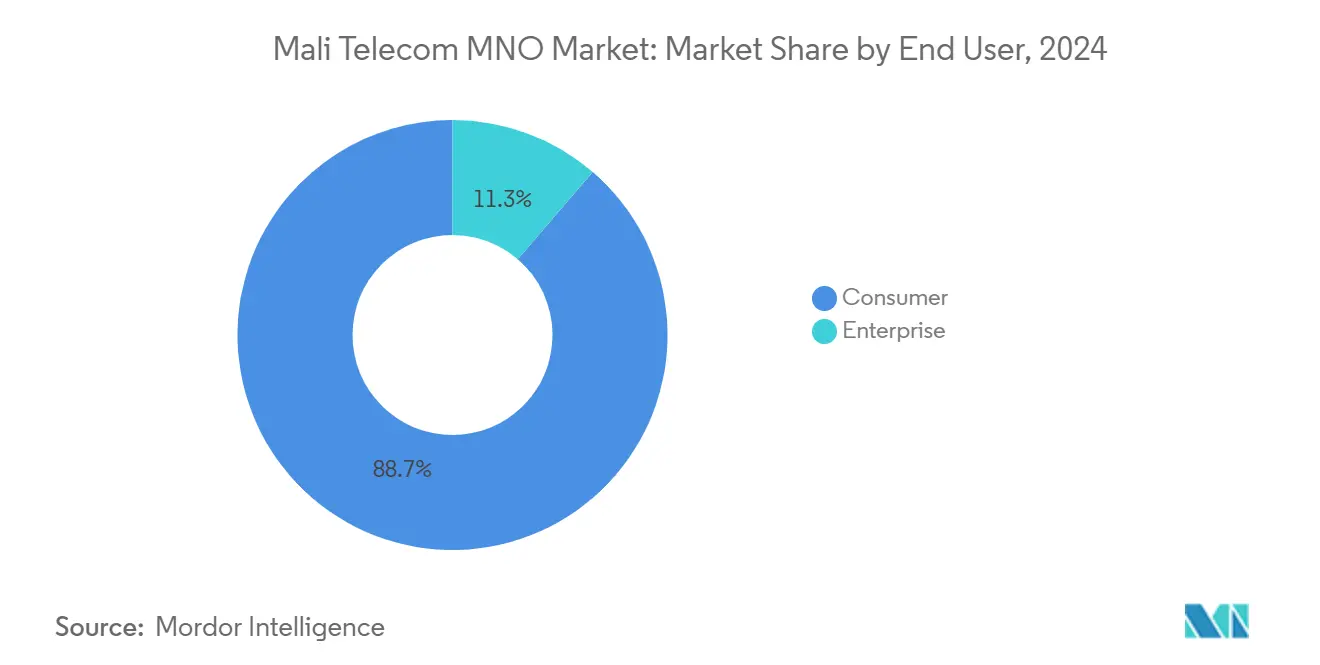

- By end user, consumer services captured 88.69% of 2024 revenue; the enterprise segment is forecast to expand at a 4.60% CAGR through 2030.

Mali Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid smartphone adoption fuelling mobile data demand | +0.8% | National, with concentration in Bamako and regional capitals | Medium term (2-4 years) |

| Nationwide 4G roll-outs and planned 5G pilot licenses | +0.6% | Urban centers expanding to rural areas | Long term (≥ 4 years) |

| Government-led push for mobile money and digital-ID inclusion | +0.4% | National, with focus on unbanked rural populations | Short term (≤ 2 years) |

| Cross-border fibre interconnection deals lowering IP transit costs | +0.3% | Border regions with Guinea, Senegal, and Burkina Faso | Medium term (2-4 years) |

| Operator partnerships on local-language AI enhancing CX and ARPU | +0.2% | National, targeting Bambara and Fulani speakers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Smartphone Adoption Fuelling Mobile Data Demand

Handset affordability is dissolving the urban–rural divide; 23.4 million cellular connections translate into 94.2% population coverage in early 2025. Rising Android penetration substitutes for fixed broadband where fiber is scarce, pushing average monthly data volumes to new highs. Orange’s alliance with Meta and OpenAI to build AI models for Wolof and Pulaar aims to monetize traffic through localized content rather than raw bandwidth. Early 2025 field trials will test whether vernacular chatbots can deepen engagement and raise average revenue per user. As device costs fall and local-language apps multiply, the Mali telecom market is expected to convert latent demand into billable gigabytes.

Nationwide 4G Roll-outs and Planned 5G Pilot Licenses

4G coverage is nearing saturation in Bamako yet remains below 40% in Sahelian districts where terrain and security risks slow tower builds. Malitel’s commercial 4G debut narrowed the capacity gap with Orange, but spectrum scarcity continues to throttle throughput during peak hours. ARCEP has circulated a draft 5G licensing framework that weighs newcomer incentives against incumbent investment pledges, delaying pilot launches into 2026. Harmonized frequency planning within ECOWAS is essential because cross-border spillover can disrupt service quality. Despite regulatory uncertainty, carriers are testing network-slicing and fixed-wireless access scenarios, betting that 5G will underpin enterprise IoT in mining and agribusiness once grid stability improves.

Government-Led Push for Mobile Money and Digital-ID Inclusion

Orange Money’s first-mover advantage has grown into a parallel financial architecture that sidesteps Mali’s thin bank-branch network. Pandemic-era fee waivers by the Central Bank of West African States accelerated wallet openings at 11.4% monthly during 2024. The national digital-ID program now links SIM registration with biometric credentials, creating a trust layer for credit scoring and micro-insurance. Orange’s tie-up with Mastercard introduces virtual and physical debit cards, enabling cross-border commerce for small traders who form the bulk of the informal economy. The linkage of IDs, wallets and merchant tools makes the Mali telecom market central to wider cash-light goals.

Cross-Border Fiber Interconnection Lowering IP Transit Costs

The July 2024 Guinea–Mali fiber pact slashes wholesale IP transit fees by up to 30%, reducing dependence on a single submarine landing point in Senegal. Additional terrestrial links through Burkina Faso diversify routes and provide fail-over capacity during cable cuts. Lower backhaul expenses allow carriers to price entry-level data bundles more aggressively, widening broadband adoption outside Bamako. The upgraded links also speed up content-delivery-network caching, cutting latency for video and gaming services. Over the medium term, these regional pipes are expected to support 5G transport requirements and stimulate carrier-neutral data-center investment inside Mali.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Political Instability and security risks, delaying infrastructure | -0.5% | Northern regions and border areas | Short term (≤ 2 years) |

| Chronic grid unreliability driving high energy OPEX | -0.3% | National, particularly rural areas | Medium term (2-4 years) |

| New Telecom-specific taxes squeezing margins and pricing power | -0.2% | National impact on all operators | Short term (≤ 2 years) |

| Shortage of skilled RF and fiber engineers slowing network roll-outs | -0.1% | National, with acute shortages in technical roles | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Political Instability and Security Risks Delaying Infrastructure

Armed incidents in Gao, Kidal and border corridors force operators to halt tower maintenance and reroute fibers, extending project timelines by up to nine months. Equipment vendors apply war-risk premiums, and lenders demand elevated debt-service coverage ratios, inflating capex costs. Relations with traditional bilateral donors cooled after the 2022 power transition, curbing grant finance for universal-access schemes. Although sanctions eased in late-2024, due-diligence hurdles persist, driving investors toward short tenors and higher coupons. This environment favors incumbents with sunk infrastructure and strains new entrants that must deploy greenfield networks.

Chronic Grid Unreliability Driving High Energy OPEX

National grid availability averages 15 hours daily outside Bamako, compelling carriers to run diesel generators for base-station uptime. Fuel imports expose operators to forex volatility and elevate per-site operating costs by 35%. The government’s 400 MW solar roadmap, backed by the World Bank and a 200 MW Russian-funded plant, promises relief but commercial operation dates fall beyond 2028. In the interim, Orange is piloting lithium-ion battery packs coupled with rooftop PV to save generator runtime by 60%. Malitel trials hybrid micro-grids at rural towers to reduce truck-roll refueling expenses. Energy inefficiencies cap free cash flow, constraining network densification in low-ARPU zones and tempering Mali telecom market growth potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Revenue Transformation

Data services accounted for 36.88% of 2024 revenue within the Mali telecom market, cementing their role as the primary growth engine. Mobile data’s 65.45% slice of the category stems from surging smartphone adoption and video-streaming habits, while fixed data is expanding at a 3.18% CAGR as fiber reaches peri-urban communes. IoT lines, although small, show the quickest 3.11% run rate, buoyed by agricultural soil-sensor roll-outs linked to mobile money gateways. Voice remains relevant-wireless voice still provides 69.81% of the voice segment-but growth has slipped to 1.85% as OTT messaging cannibalizes call minutes.

Operators are reframing data plans as lifestyle bundles. Orange’s local-language AI assistants, for instance, sit atop data packages and push interactive learning modules that generate incremental traffic. OTT TV is migrating to smartphone screens, while value-added services integrate airtime credit scoring for nano-loans. As IoT deployments in irrigation and logistics scale, carriers will pivot from per-megabyte billing to platform fees, widening total addressable revenue beyond traditional connectivity. The Mali telecom market size for data-led services is therefore set to outpace legacy voice by mid-decade.

By End-User: Consumer Dominance Amid Enterprise Digitization

Households represent 71.80% of 2024 turnover, underscoring Mali’s mobile-first consumer culture. Yet enterprise revenue is climbing at 3.88% CAGR as mining, agriculture and public-sector projects automate workflows over private APNs. Gold mines in Kangaba deploy LTE-Advanced networks for fleet management and safety compliance, while cotton cooperatives adopt USSD-based inventory tracking that feeds into cloud ERPs.

The consumer–enterprise boundary is dissolving. Small merchants increasingly receive payments via Orange Money, converting person-to-person wallets into business wallets without changing tariff plans. Government-backed digital ID unlocks e-KYC for micro-retailers, accelerating mobile-payment acceptance. Consequently, the Mali telecom market share of hybrid consumer-merchant segments is forecast to widen, even as pure enterprise accounts remain a minority.

Geography Analysis

Southern provinces cluster over 80% of active data subscriptions, with Bamako alone housing more than one-third. The capital enjoys near-universal 4G, while Sikasso and Kayes trail but still post double-digit data-traffic growth as fiber backhaul eases congestion. In contrast, northern Tombouctou and Kidal provinces represent less than 7% of the Mali telecom market size, hamstrung by security issues that raise tower insurance costs and limit field maintenance.

Cross-border corridors tell a different story. The Kayes–Dakar highway corridor leverages the new Senegal-Mali fiber spur, cutting wholesale bandwidth costs and spurring SME e-commerce adoption. Border towns along Guinea’s Nzérékoré axis benefit from the July 2024 interconnection, registering 28% year-on-year data-traffic spikes. Eastern regions that depend on Burkina Faso’s transit routes still encounter single-point-of-failure risk, which the upcoming Ghana-Mali terrestrial pipe aims to mitigate by 2027.

Urban–rural digital divides persist but are narrowing. Solar-powered small cells under the Universal Service Fund now blanket 250 villages with 3G signals. Although ARPU in these zones sits 40% below national averages, incremental revenue beats diesel-powered alternatives. As new grid-tied solar projects reach commercial date, rural energy costs should decline, improving the profitability equation and enlarging the Mali telecom market.

Competitive Landscape

The market remains a regulated duopoly. Orange leverages its 59% grip to launch bundled 4G-plus-mobile money packages, while Malitel leans on its state affiliation to win public-sector tenders. Telecel’s 2023 license acquisition has yet to translate into mass-market traction, as high capex requirements and limited on-net roaming agreements curb rollout speed.

Strategically, Orange exploits pan-regional scale. Its USD 570 million purchase of Airtel Burkina Faso and Sierra Leone yields procurement savings on radio equipment and provides aggregation hubs that lower international transit costs. Malitel counters with satellite backhaul agreements that prioritise rural coverage, differentiating on territorial reach rather than speed. Both incumbents are testing open-RAN pilots to trim vendor lock-in, though commercial deployment is unlikely before 2027.

Service innovation is the new battleground. Orange’s partnership with Mastercard embeds financial rails into daily connectivity, while Malitel pilots agritech dashboards that marry IoT soil sensors with SMS alerts. Operator strategies thus tilt toward ecosystem orchestration, a shift that could dilute pure connectivity margins yet enlarge overall Mali telecom market size through adjacent revenues.

Mali Telecom MNO Industry Leaders

Orange Mali

Malitel (Sotelma)

Telecel Mali

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Orange Africa and Middle East and Eutelsat introduced satellite broadband up to 100 Mbps for isolated areas using EUTELSAT KONNECT, supporting Orange’s digital-inclusion goals across Mali and the Sahel.

- November 2024: MIGA issued EUR 506 million guarantees for West African Development Bank projects, with half earmarked for climate-finance infrastructure including digital networks in Mali.

- October 2024: Orange Middle East and Africa and Mastercard enabled virtual and physical debit cards for Orange Money users in Mali and six peers, further merging telecom and banking services.

- July 2024: Guinea and Mali signed a fiber-optic interconnection accord that reduces international transit costs and improves network resilience.

Mali Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How does mobile money influence telecom revenues

Mobile money penetration of 66% expands data usage and enables fintech bundles, adding incremental revenue streams for operators.

What major infrastructure projects will impact network quality

Cross-border fiber links with Guinea and Senegal and planned solar-hybrid power solutions are set to improve backhaul capacity and site uptime over the medium term.

How concentrated is market competition

Orange controls 59% of active SIMs and Malitel holds 41%, indicating a duopolistic structure.

What growth rate is expected for IoT services

IoT connections are forecast to expand at a 3.70% CAGR through 2030, propelled by agriculture and mobile-money applications.

Page last updated on: