Jordan Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

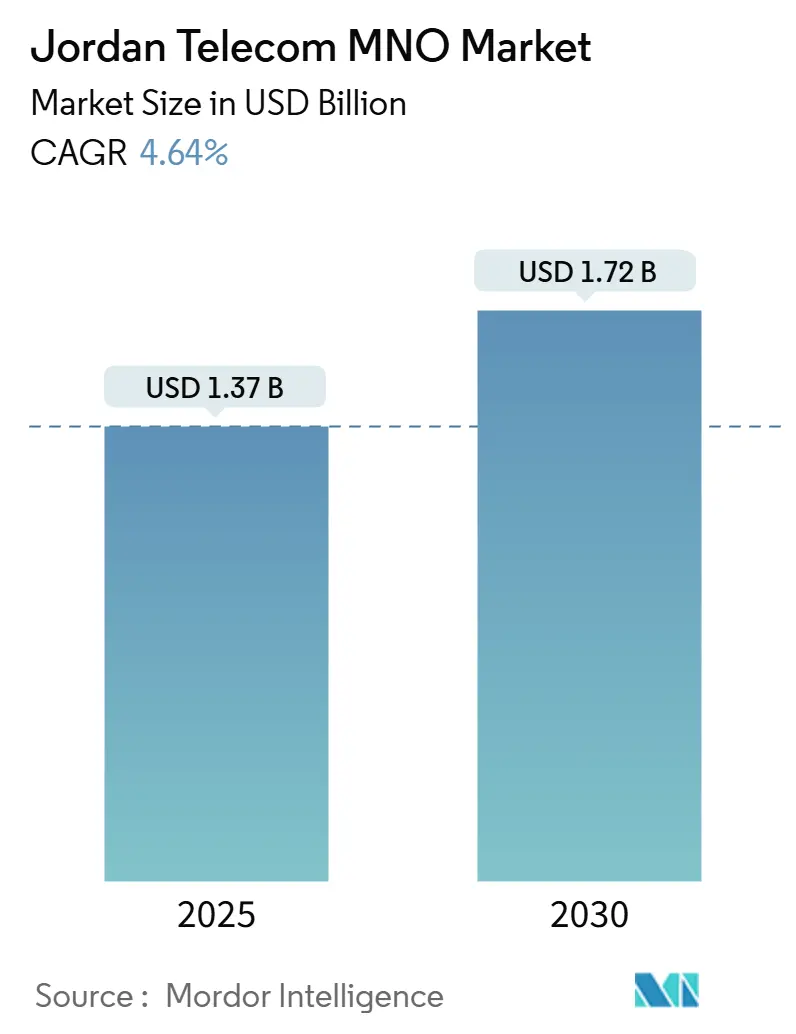

| Market Size (2025) | USD 1.37 Billion |

| Market Size (2030) | USD 1.72 Billion |

| Growth Rate (2025 - 2030) | 4.64% CAGR |

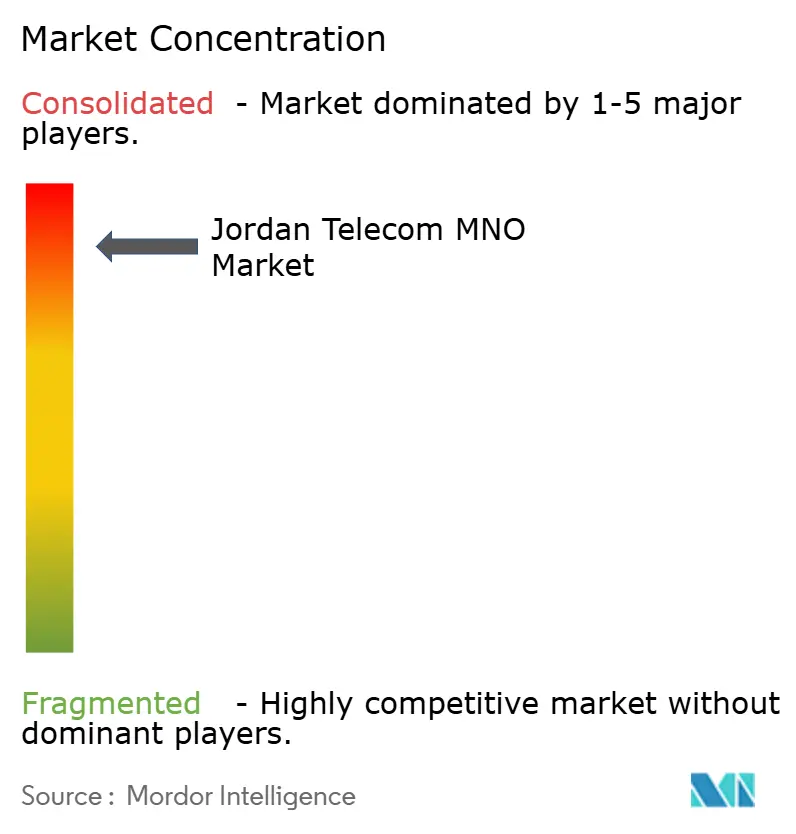

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Jordan Telecom MNO Market Analysis by Mordor Intelligence

The Jordan Telecom MNO Market size is estimated at USD 1.37 billion in 2025, and is expected to reach USD 1.72 billion by 2030, at a CAGR of 4.64% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 9.30 million subscribers in 2025 to 10.80 million subscribers by 2030, at a CAGR of 3.17% during the forecast period (2025-2030).

Momentum stems from nationwide 5G rollouts, expanding fiber backbones, and government targets that assign the digital economy a 3% GDP contribution by 2033. [1]International Trade Administration, “Jordan – Digital Economy,” TRADE.GOV Intensifying demand for cloud-ready bandwidth among enterprises, the rise of mobile-money platforms, and Jordan’s role as a cross-border traffic hub keep capital spending focused on dense urban corridors and key submarine-cable landing sites. Competitive dynamics have shifted from price to performance as Zain, Orange, and Umniah leverage 5G to advertise throughput above 1 Gbps. Operators are also widening service portfolios to include cybersecurity, IoT, and satellite backhaul, creating fresh revenue pools that moderate reliance on voice. A high, sector-specific tax burden and foreign-exchange volatility still weigh on margins, yet disciplined network-sharing agreements and public–private fiber partnerships temper cost pressures.

Key Report Takeaways

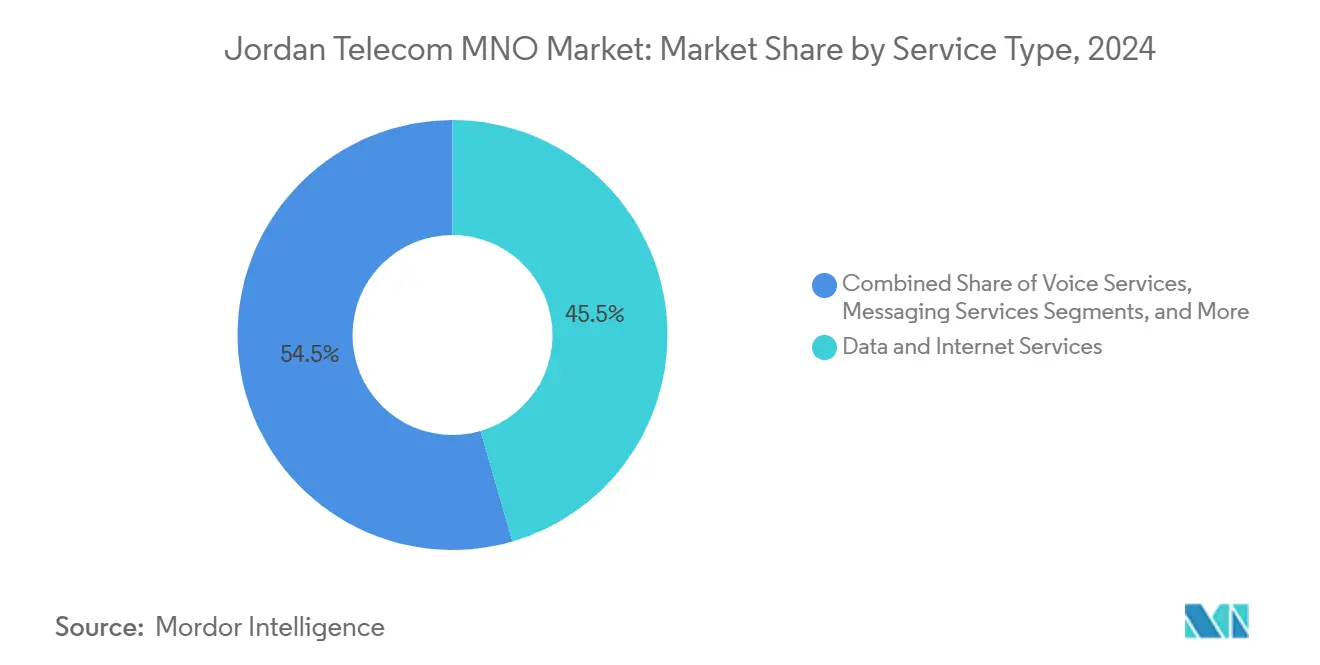

- By service type, data and internet services led with 45.50% of Jordan telecom MNO market share in 2024, and OTT and PayTV services are forecast to expand at a 4.66% CAGR through 2030.

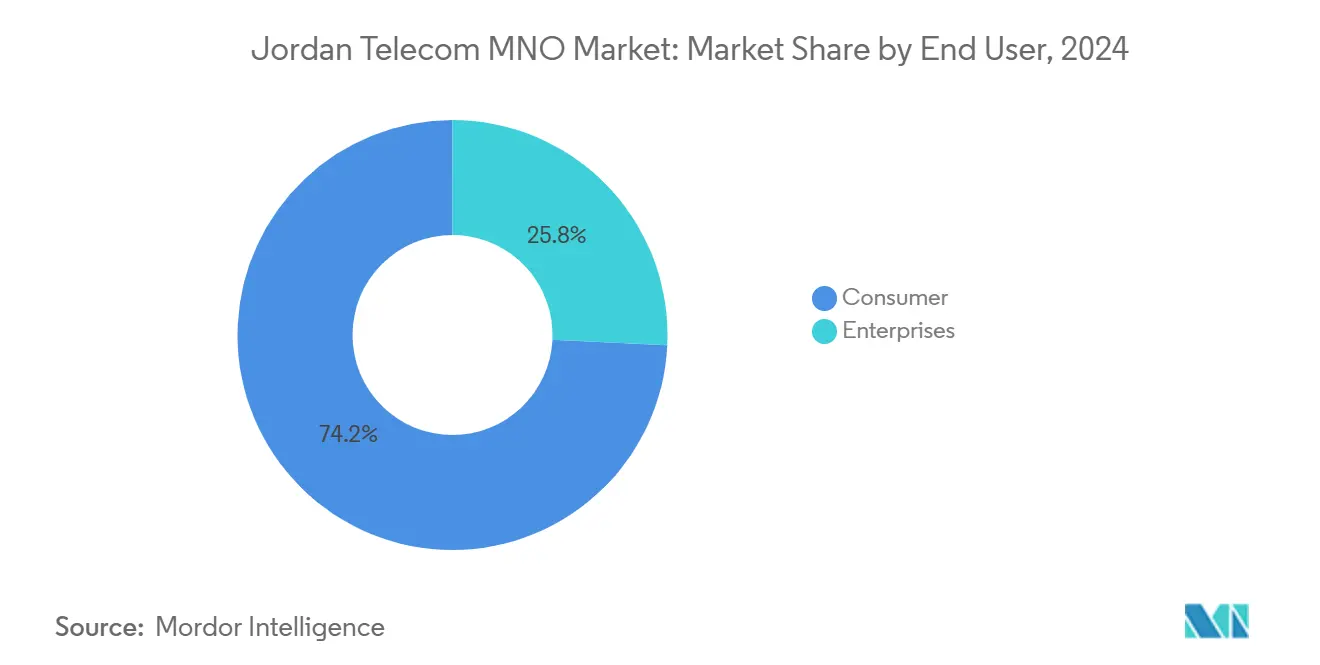

- By end user, the consumer segment accounted for 74.24% of the Jordan telecom MNO market size in 2024, while the enterprise segment is advancing at a 5.04% CAGR through 2030.

Jordan Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in mobile-data traffic post-5G launch | +1.2% | Amman, Irbid, Aqaba | Short term (≤ 2 years) |

| Fixed-fiber rollout backed by public–private funding | +0.8% | Urban centers and industrial zones | Medium term (2-4 years) |

| Enterprise digital-transformation contracts | +0.7% | Amman business district | Medium term (2-4 years) |

| FinTech uptake boosting mobile-money volumes | +0.5% | Rural penetration focus | Long term (≥ 4 years) |

| Cross-border content-delivery hub ambitions | +0.4% | Aqaba Special Economic Zone | Long term (≥ 4 years) |

| Satellite backhaul lowering rural cost | +0.3% | Remote areas nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in mobile-data traffic post-5G launch

Commercial 5G services now deliver peaks above 1 Gbps in Amman and Irbid, prompting a swift shift from legacy bundles to premium data tiers. [2]Zain, “The Number 1 of 5G in Jordan,” JO.ZAIN.COM Coordinated spectrum assignments by the Telecommunications Regulatory Commission keep build-outs synchronized, allowing the three operators to pool passive infrastructure and widen coverage faster. Early usage analytics show video-streaming minutes doubling within months of launch, while corporate clients trial real-time automation in logistics and healthcare. The step-up in traffic feeds higher ARPU and opens incremental revenue streams through IoT connections. Network slicing pilots set to start in 2026 will extend monetization into latency-sensitive industrial segments.

Fixed-fiber rollout backed by public–private funding

Orange Jordan’s Fiber-to-the-Room service and Wi-Fi 6 gateways deliver up to 10 Gbps for households and SMEs. [3]Orange Jordan, “Home Internet Fiber,” ORANGE.JO Operators lease dark fiber from the National Electric Power Company’s 1,500-kilometer grid, freeing capital for last-mile installs. [4]National Electric Power Company, “Fiber Optic Service,” NEPCO.COM.JO Gateway upgrades across 76 sites, executed with Nokia in early 2025, added routing capacity and lowered latency for cloud workloads. The model aligns with the Economic Modernization Vision, which earmarks ongoing funds for industrial-zone connectivity. Rising fiber penetration underpins enterprise cloud adoption and stabilizes backhaul for 5G small-cells.

Enterprise digital-transformation contracts (cloud, cybersecurity)

More than 60% of Jordanian IT firms had integrated AI by 2024, and 20% offered IoT-based products. Operators respond by bundling managed security, SaaS reselling, and edge hosting into multi-year deals that generate ARPU up to five times higher than mass-market plans. Government agendas to automate 960 services drive procurement of secure, low-latency links connecting ministries and data centers. Hackathons and developer programs run by Orange cultivate a solutions ecosystem that accelerates uptake of telco-hosted APIs. As contracts scale, operators diversify away from price-sensitive prepaid traffic toward stickier enterprise cash flows.

FinTech uptake boosting telco mobile-money volumes

The JoMoPay switch lets users move funds instantly between wallets and banks, anchoring a regulatory-grade clearing layer for telecom wallets. Orange Money and Zain Cash overlay this rail with salary-transfer and bill-payment features, broadening reach to unbanked customers. The Central Bank’s sandbox invites new FinTech entrants, fuelling innovation while maintaining prudential oversight. Transaction growth lifts non-connectivity revenue and enhances customer stickiness, especially in rural governorates where physical banking points remain scarce. The long-run payoff lies in credit scoring, insurance micro-products, and merchant acceptance, all of which deepen the digital wallet ecosystem.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Double-digit sector-specific tax burden | -0.9% | Nationwide | Short term (≤ 2 years) |

| Slow wholesale price cuts on international bandwidth | -0.6% | National, data-heavy services | Medium term (2-4 years) |

| Legacy 2G/3G users delaying network-sunset savings | -0.4% | Rural and cost-sensitive areas | Medium term (2-4 years) |

| FX volatility inflating capex for imported gear | -0.3% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Double-digit sector-specific tax burden

Operators face a corporate income tax of 24% plus a 2% national-contribution levy, before sales tax, which climbed to 16% on internet services. The resulting squeeze has forced reprioritization of capex pipelines, with rural base-station plans slowed in favor of urban densification. Management teams weigh tariff hikes against churn risk in a market where prepaid lines dominate. High levies also deter foreign investors evaluating potential greenfield data-center builds tied to the Jordan telecom MNO market. Until fiscal relief surfaces, network monetization strategies lean on cost sharing and spectrum refarming rather than bold coverage extensions.

Legacy 2G/3G users delaying network-sunset savings

Umniah’s target to switch off 2G by the end of 2025 illustrates the balancing act between opex savings and customer migration costs. Maintaining parallel networks keeps energy bills elevated and fragments the spectrum assets needed for 5G carriers. Rural handset subsidy programs lag uptake goals, prolonging low-ARPU traffic on legacy layers. Operators deploy educational campaigns to hasten device churn, yet migration remains slower than in peer markets with stronger disposable income. The extended timeline pushes full-spectrum re-farm benefits beyond 2027, tempering Jordan telecom MNO market efficiency gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data services drive revenue transformation

Data and internet services captured 45.50% of Jordan telecom MNO market share in 2024, buoyed by fiber reaching 64% of broadband lines and 5G stimulating video-first usage. Voice revenue now trends flat as over-the-top calling pivots subscribers to data bundles, while premium enterprise-SMS products steady messaging cash flows. IoT and M2M traffic remains nascent but climbs quickly after General Network received the kingdom’s first dedicated IoT license in 2020. Operators exploit wholesale back-haul from the Aqaba IX to market regional transit, monetizing Jordan’s midpoint geography for MEA-Europe traffic.

OTT and PayTV subscriptions form the fastest-growing slice at a 4.66% CAGR through 2030 as telecom-content tie-ups bundle streaming into data plans. Orange’s satellite-internet launch with Eutelsat diversifies capacity for underserved locales and anchors bundled TV-plus-broadband offers. Roaming, value-added services, and international voice together add incremental margin, though strategic focus stays on upselling higher-bandwidth tiers. Over time, Jordan telecom MNO market size for data-centric services will set the revenue ceiling for operators as legacy lines taper.

By End User: Enterprise adoption accelerates

Consumer connections represented 74.24% of the Jordan telecom MNO market size in 2024, supported by penetration above 150% of the population and aggressive smartphone financing. Urban professionals take up postpaid bundles that fold in roaming and streaming add-ons, while prepaid volumes dominate rural districts. Price competition stays sharp, yet data differentiation via 5G speeds tempers unlimited-plan discounting.

Enterprise subscriptions, although a smaller base, are forecast to deliver a 5.04% CAGR to 2030, driven by public-sector digitization and foreign investors locating shared-service centers in Amman. Managed security, SD-WAN, and private 5G campus networks command premium ARPU multiples. Zain’s live 5G pilots with universities and smart-manufacturing sites showcase these value-added layers. As automated government portals expand, bandwidth-intensive transactional loads will anchor sticky contract revenue, reinforcing the strategic heft of the enterprise slice within the Jordan telecom MNO market.

Geography Analysis

Jordan’s compact geography amplifies the effect of infrastructure nodes on national performance. The Aqaba Internet Exchange registers peak traffic above 100 Gbps, routing Asian and Gulf content toward European eyeballs and trimming latency for local users. Submarine landings that connect to Egypt and Palestine supply redundancy, while the National Electric Power Company’s fiber grid forms a nationwide backbone. Median mobile download rankings improved from 64th to 33rd globally between 2020 and 2024, demonstrating tangible quality-of-service gains.

Rollouts follow an urban-first path. Zain and Orange launched 5G in Amman and Irbid before widening to Zarqa, Mafraq, and Aqaba. Orange’s FTTR initiative packages gigabit home broadband, while Umniah invests in fiber overlays to lift average throughput outside primary metros. Rural connectivity gaps are narrowing after Starlink’s April 2025 entry and Orange’s Eutelsat bundles, which price unlimited 40 Mbps access at JOD 40 per month. Government mapping based on Ookla analytics guides spectrum-site auctions to ensure parity across governorates.

Jordan’s crossroads position sparks data-center interest as hyperscalers scout for politically stable alternatives to Gulf states. Planned upgrades to the DE-CIX Apollon platform in Aqaba will boost available peering capacity and help transform the port city into a regional cache node. Expected spillovers include job creation in colocation services, power-infrastructure investments, and auxiliary cloud-integration contracts for telecom operators. Together these developments reinforce the importance of geography as both a revenue enabler and a competitive differentiator in the Jordan telecom MNO market.

Competitive Landscape

Jordan hosts a classic three-player oligopoly. Zain, Orange, and Umniah each hold nationwide licenses and comparable macro-site footprints, yet differentiation now hinges on latency metrics and enterprise enablement. Zain leads 5G rollouts, advertising channel bandwidth that tops 1 Gbps, while Orange positions on ultra-low latency of 1 ms and residential gigabit fiber. Umniah’s strategy focuses on cost leadership and technology refresh, evidenced by its MoU to broaden 4G coverage and an announced 2G shutdown to free spectrum for 5G carriers.

Vendor partnerships shape network economics. Orange and Nokia’s 2025 gateway upgrade improved capacity and energy efficiency across 76 urban sites. Zain aligns with Huawei for core network virtualization, while Umniah leverages wholesale fiber from NEPCO to cut trenching costs. All three pursue service adjacencies: Zain Cash and Orange Money push deeper into mobile finance; Umniah courts SMEs with bundled security and cloud firewalls.

Emerging entrants remain limited. General Network exploits first-mover status in IoT licensing to supply smart-city sensors and agriculture telemetry. Starlink’s satellite offer is the first external threat to fixed-line revenue, particularly in remote areas. Nonetheless, high spectrum fees, rigorous QoS targets, and entrenched retail footprints keep barriers significant, preserving a concentrated Jordan telecom MNO market through 2030.

Jordan Telecom MNO Industry Leaders

Zain Jordan

Orange Jordan

Umniah

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Starlink launched satellite internet services nationwide following Telecommunications Regulatory Commission approval, extending high-speed access to underserved regions.

- April 2025: Orange Jordan introduced satellite internet packages via Eutelsat with tiered speeds up to 100 Mbps and two-year contracts.

- February 2025: Orange Jordan and Nokia finished broadband gateway upgrades across 76 sites, expanding 5G-ready capacity.

- May 2024: Orange Jordan launched FTTR plus Wi-Fi 6, offering residential gigabit throughput.

- May 2024: Umniah signed an MoU to extend 4G coverage, bridging service gaps ahead of its planned 2G sunset.

- January 2024: Umniah activated Voice over Wi-Fi to improve indoor call quality.

Jordan Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Jordan telecom MNO market in 2025?

The Jordan telecom MNO market size is valued at USD 1.37 billion in 2025 and is on track to reach USD 1.72 billion by 2030.

Which service type contributes most to operator revenue?

Data and internet services lead, accounting for 45.50% of Jordan telecom MNO market share in 2024.

What CAGR is expected for enterprise subscriptions through 2030?

Enterprise lines are forecast to grow at a 5.04% CAGR as businesses adopt cloud and cybersecurity solutions.

How are operators addressing rural connectivity gaps?

Operators combine satellite partnerships with Starlink and Eutelsat plus shared dark-fiber leases to extend high-speed access outside major cities.

Which company leads 5G deployment speeds in Jordan?

Zain reports commercial 5G speeds exceeding 1 Gbps, positioning it as the performance leader.

What tax factors constrain telecom investment?

A combined 26% income tax plus higher sales tax on data services limits capital available for network expansion.

Page last updated on: