Montenegro Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

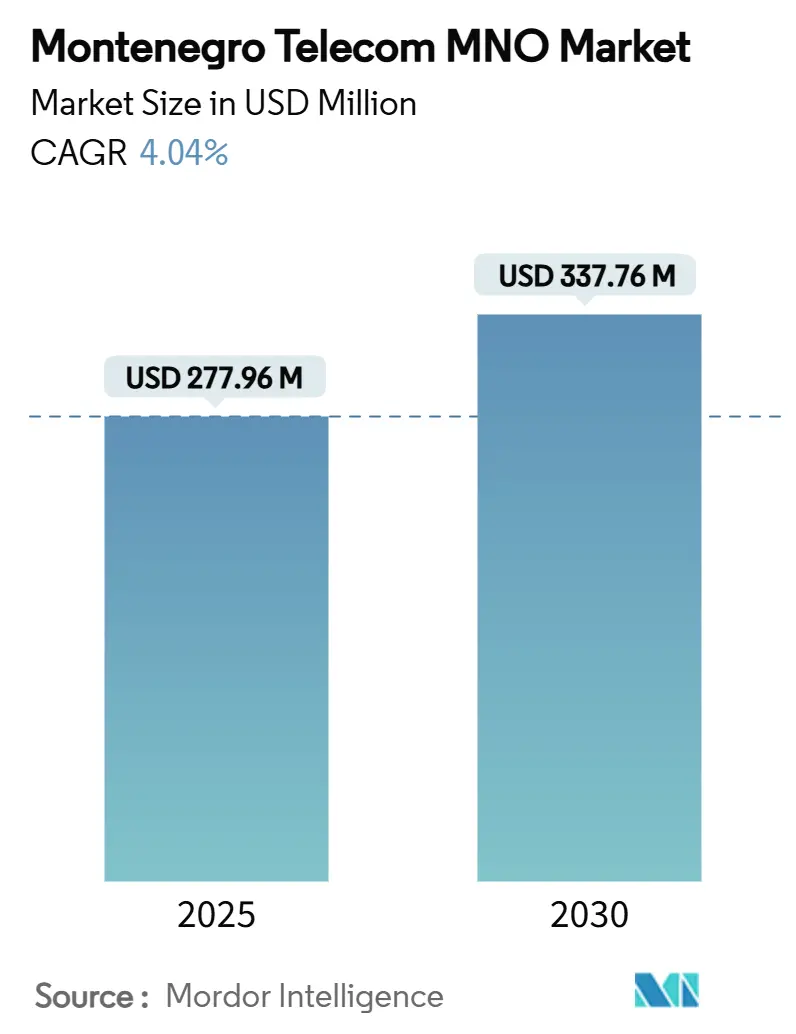

| Market Size (2025) | USD 277.96 Million |

| Market Size (2030) | USD 337.76 Million |

| Growth Rate (2025 - 2030) | 4.04% CAGR |

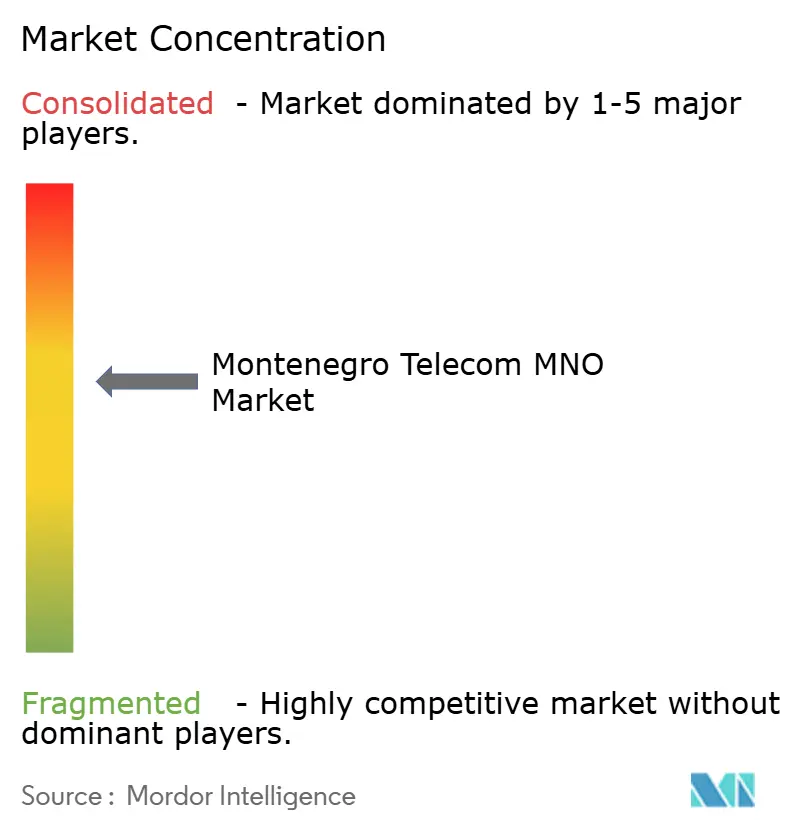

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Montenegro Telecom MNO Market Analysis by Mordor Intelligence

The Montenegro Telecom MNO Market size is estimated at USD 277.96 million in 2025, and is expected to reach USD 337.76 million by 2030, at a CAGR of 4.04% during the forecast period (2025-2030).

Digital-first policy reforms, accelerated 5G spectrum re-farming, and sustained fiber backbone investments anchor this trajectory. Mobile penetration already exceeds 225%, reflecting the country’s tourism-heavy traffic profile and multiple-device ownership habits. Data services dominate revenue formation, while enterprise connectivity outpaces consumer growth as companies modernize operations to satisfy EU accession mandates. Competitive pressure remains high among three nationwide operators, prompting network-sharing dialogues and ongoing regulatory scrutiny that may reshape long-term pricing.

Key Report Takeaways

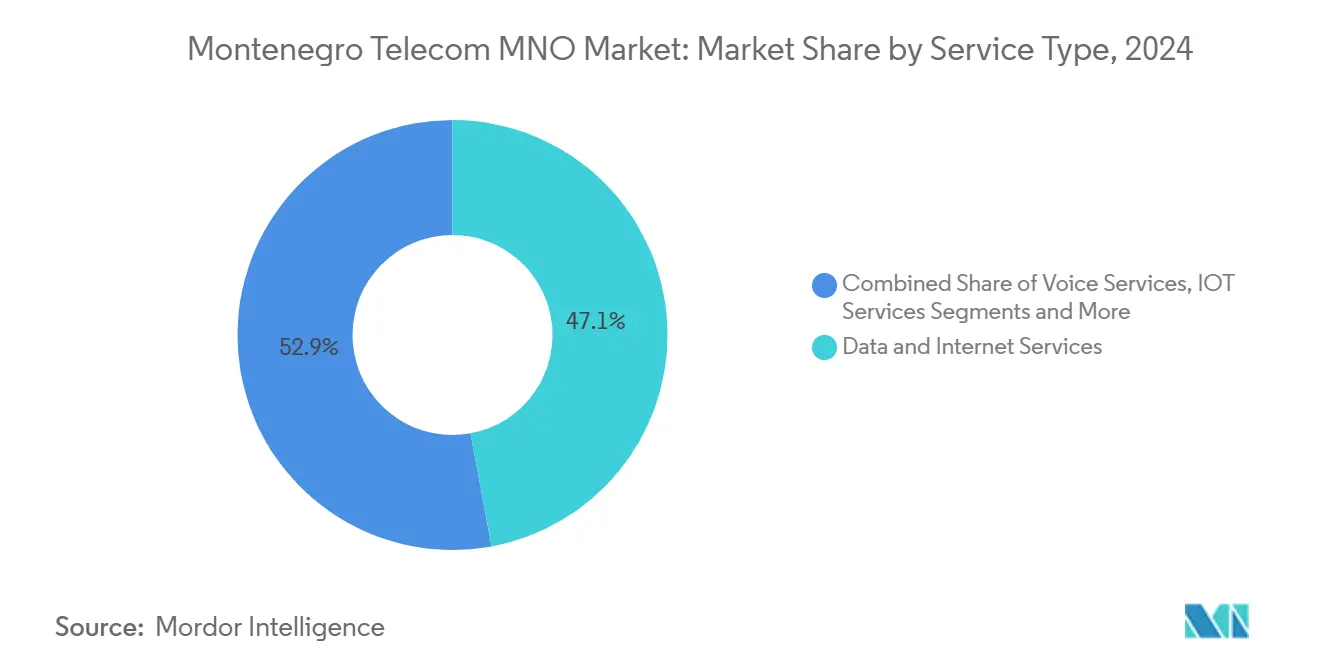

- By service type, data services held 47.10% of the Montenegro telecom market share in 2024 and are expanding at a 4.26% CAGR to 2030.

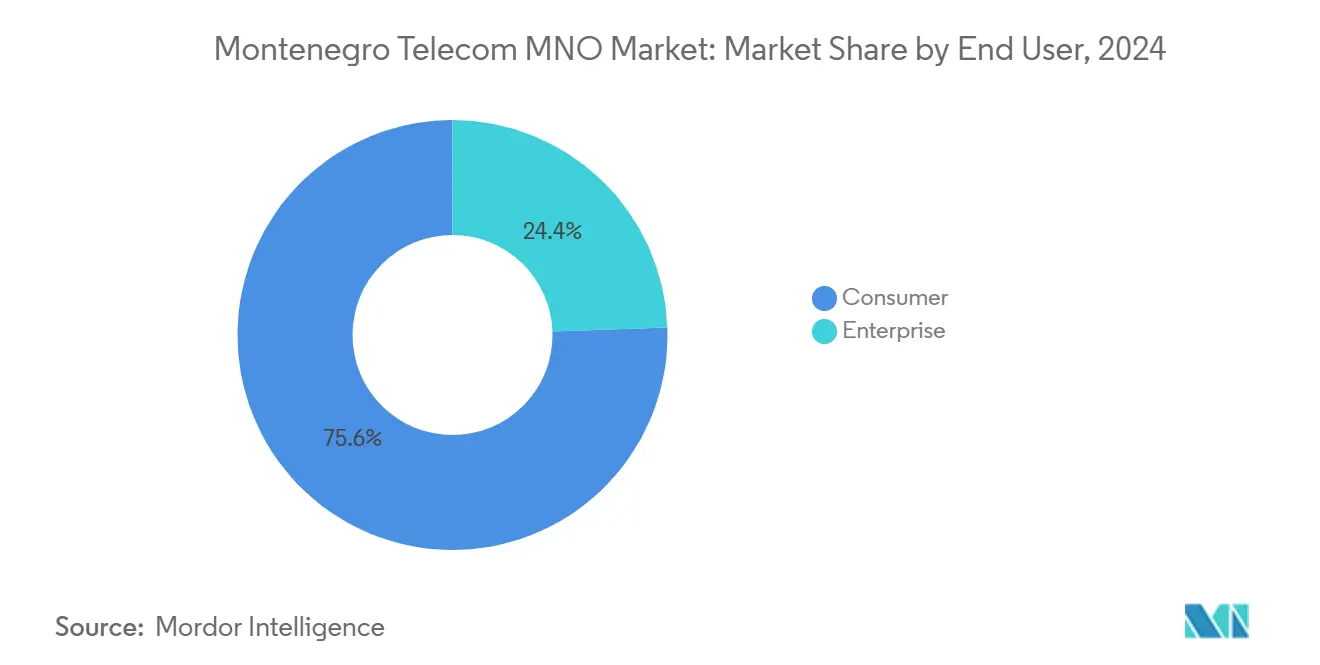

- By end user, enterprise revenues are set to capture 26.9% of the Montenegro telecom market size by 2030, up from 24.44% in 2024.

Montenegro Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing 5G rollout accelerating mobile data consumption | +1.2% | National, early gains in Podgorica, Nikšić, Budva | Medium term (2-4 years) |

| Government national broadband plan driving FTTH uptake | +0.8% | National, rural and underserved areas | Long term (≥ 4 years) |

| Tourism-centric economy boosting seasonal roaming revenues | +0.6% | Coastal and mountain tourism areas | Short term (≤ 2 years) |

| Cross-border fiber links to EU IXPs lowering transit costs | +0.4% | National business corridors | Medium term (2-4 years) |

| Rising enterprise demand for secure SD-WAN & IoT solutions | +0.7% | Urban centers, expanding to industrial zones | Medium term (2-4 years) |

| Pro-investment tax incentives for rural tower sharing | +0.3% | Rural and mountainous regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing 5G rollout accelerating mobile data consumption

One Crna Gora deployed the most 3600 MHz 5G base stations by October 2023, securing first-mover status for enhanced mobile broadband services. Crnogorski Telekom retired its 3G network in January 2024, freeing spectrum for 4G and 5G layers. Average mobile speeds now reach 55.47 Mbps, ranking Montenegro among the top performers in the Western Balkans. EKIP’s technology-neutral licensing lets operators aggregate contiguous blocks to support gigabit-class services. These actions collectively stimulate data-usage intensity and accelerate service monetization.

Government national broadband plan driving FTTH uptake

The National Broadband Plan aligns fiber milestones with EU accession benchmarks, unlocking policy continuity for operators. Crnogorski Telekom lifted retail fiber speeds to 500 Mbps in 2024, signaling excess capacity ready to absorb future demand. United Group’s regional backbone provides wholesale resilience that lowers last-mile costs. Rural subsidies and streamlined civil-works permitting improve build economics, especially in mountainous zones. Together, these interventions underpin long-range FTTH penetration gains and support smart-government platforms rolled out under UNDP’s e-services program.

Tourism-centric economy boosting seasonal roaming revenues

Mobile connections totaled 1.41 million against a resident base of 626,000 in 2024, reflecting heavy tourist SIM uptake. Operators sell visitor bundles offering 500 GB for EUR 10 over 15 days, maximizing short-duration data ARPU. Coastal 4G/LTE coverage exceeds 99%, providing dependable capacity during summer peaks. Predictable high-season cash flows help fund off-season network upgrades. The pattern differentiates the Montenegro telecom market from peers that rely chiefly on domestic usage.

Rising enterprise demand for secure SD-WAN & IoT solutions

Legally mandated electronic data exchange between ministries and businesses is scaling secure connectivity requirements. Real-time environmental IoT pilots monitor water quality in the Bay of Kotor. AgroNET precision-farming deployments optimize fertilizer and irrigation scheduling in the Zeta plain. These use-cases lift enterprise C-level appetite for SD-WAN overlays that outclass legacy MPLS on cost and agility, reinforcing the segment’s 5.05% CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Small population limiting economies of scale | -0.9% | National, rural coverage economics | Long term (≥ 4 years) |

| Persistently low ARPU due to price wars | -0.7% | National, all service categories | Medium term (2-4 years) |

| High spectrum fees relative to GDP discouraging bids | -0.6% | National frequency allocations | Medium term (2-4 years) |

| Brain-drain of telecom engineers to EU markets | -0.4% | National technical workforce | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Small population limiting economies of scale

Serving 626,000 residents caps revenue ceilings while fixed network costs remain inelastic. Rural towers generate thin returns, delaying upgrades and narrowing investment scope. Spectrum auctions priced on pan-European benchmarks tighten capital budgets, compelling cautious 5G staging. GSMA has urged policymakers to recalibrate fee structures for micro-states to sustain network quality. Unless wholesale models or tower-sharing rules mature, operators face persistent under-recovery risks.

Persistently low ARPU due to price wars

Prepaid visitor bundles set an aggressive price anchor that migrates into domestic plans. Regulatory probes in 2024 exposed restrictive agreements, spotlighting the fragility of informal price discipline. While volumetric data revenues rise, per-gigabyte yields shrink, squeezing margins needed for densifying 5G cells. Operators respond with content-bundling and loyalty apps, but uptake has yet to materially lift blended ARPU.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Revenue Growth

Data services generated USD 128.57 million in 2024, equal to 47.10% of the Montenegro telecom market size and are scaling at a 4.26% CAGR to 2030. Voice revenues of USD 97.98 million continue to contract in share even as minutes modestly grow, mirroring EU voice-to-data substitution patterns. The Montenegro telecom market share of IoT stood at 5.02% in 2024 and, paired with a 4.48% CAGR, marks the strongest upside.

OTT and PayTV bundles earned USD 21.33 million last year, supported by United Group’s cross-border content library. Messaging and value-added services delivered USD 11.38 million but face cannibalization from free apps. The segmentation underlines a structural pivot toward data-centric billing, urging operators to monetize network quality, latency, and content partnerships rather than traditional minutes sold.

By End User: Enterprise Segment Accelerates Growth

Enterprises delivered USD 66.72 million in 2024, translating to 24.44% of the Montenegro telecom market size and a 5.05% CAGR outlook. E-governance directives obligate private entities to integrate secure digital interfaces, catalyzing SD-WAN and dedicated fiber orders.

Conversely, consumer revenues of USD 206.24 million expand slower at 3.70% amid price competition. Still, tourism-driven prepaid traffic cushions ARPU compression. Enterprises are also early adopters of IoT telemetry in hospitality and energy, reinforcing network-tier differentiation strategies for operators.

Geography Analysis

Regional revenue clustering reflects Montenegro’s compact but topographically diverse terrain. Coastal municipalities—Budva, Kotor, and Ulcinj—capture the highest seasonal traffic volumes, converting tourist data surges into premium roaming margins. Podgorica, the administrative center, anchors enterprise connectivity demand with dense fiber loops that support government clouds and corporate headquarters.

Northern mountainous districts such as Žabljak face sparse population densities that elevate backhaul costs. Rural subsidy schemes and tower-sharing incentives partially offset the economics, yet network rollouts lag urban benchmarks. Cross-border fiber laterals into Albania, Serbia, and Croatia strengthen international transit resilience, lowering wholesale IP costs for domestic ISPs.

Collectively, these geographic nuances compel operators to adopt region-specific pricing and rollout priorities, balancing ROI between high-density coastal corridors and universal-service mandates in remote hinterlands.

Competitive Landscape

Crnogorski Telekom leverages Deutsche Telekom’s procurement scale to modernize radio layers and deploy a dual-mode 5G core, agreed with Ericsson in November 2024. One Crna Gora, rebranded under 4iG in 2025, leads in 3600 MHz cell deployments and reported EUR 51 million sales on 357,701 subscribers. M:tel Montenegro taps its Serbian parent for roaming alliances and spectrum strategy, while Telemach emphasizes converged bundles integrating PayTV over a DOCSIS 3.1 network.

Regulatory intervention in 2024 challenged alleged restrictive agreements, amplifying scrutiny of tariff structures. Post-probe, operators revived discussions on passive-infrastructure sharing to trim overlapping capex. Competitive differentiation now hinges on quality-of-service metrics, enterprise SLAs, and localized content libraries rather than headline data quotas.

Entry barriers stay high due to limited spectrum and capital-intensive tower grids, preserving a tri-opoly configuration. Niche MVNOs remain absent, though policy papers hint at future wholesale access obligations that could broaden retail choice.

Montenegro Telecom MNO Industry Leaders

M:tel Montenegro

Crnogorski Telekom

One Montenegro

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2024: Crnogorski Telekom completed the nationwide 3G shutdown, reallocating spectrum to fortify 4G and 5G capacity.

- November 2024: Hrvatski Telekom and Crnogorski Telekom selected Ericsson Nikola Tesla to supply a cloud-native dual-mode 5G core.

- December 2024: The Montenegrin Competition Agency imposed remedies following a restrictive-agreement probe involving all three mobile operators.

- October 2024: United Group unveiled 100% renewable-energy sourcing targets by 2027 and expanded IoT offerings in Montenegro.

Montenegro Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise And Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise And Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What was the impact of Montenegro’s 3G shutdown?

Spectrum freed from 3G now boosts 4G and 5G capacity, enhancing average mobile speeds and network efficiency

How does tourism influence telecom revenues?

Seasonal visitors push mobile penetration to 225%, driving prepaid data bundle sales that spike cash inflows during summer months.

Why is enterprise connectivity demand rising?

E-governance mandates and EU-aligned compliance rules compel businesses to upgrade to SD-WAN and secure fiber links.

How many 5G base stations has One Crna Gora deployed?

By October 2023 the operator led the market with the highest count of 3600 MHz 5G sectors.

Page last updated on: