Ukraine Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

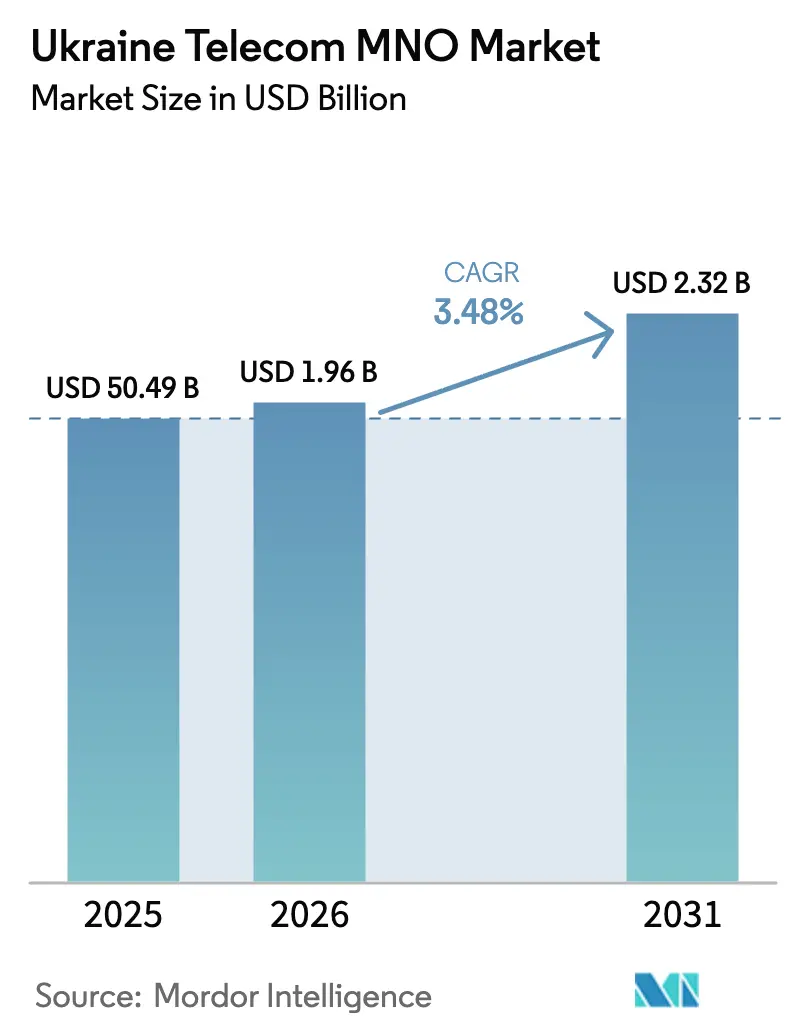

| Base Year Market Size (2025) | USD 50.49 Billion |

| Market Size (2026) | USD 1.96 Billion |

| Market Size (2031) | USD 2.32 Billion |

| Growth Rate (2026 - 2031) | 3.48% CAGR |

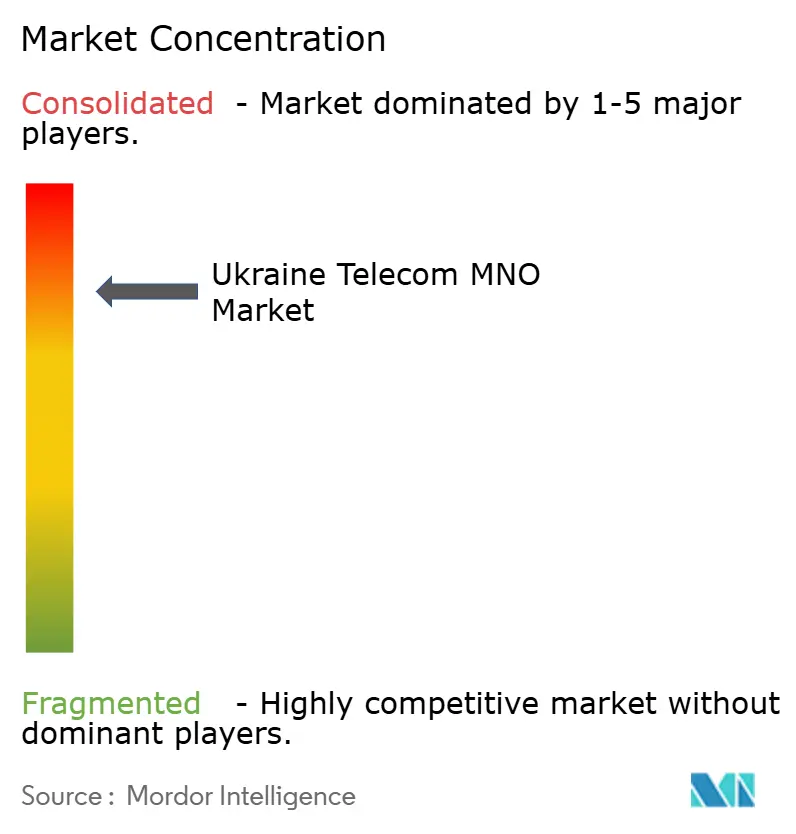

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ukraine Telecom MNO Market Analysis by Mordor Intelligence

The Ukraine Telecom MNO Market size was valued at USD 1.89 billion in 2025 and estimated to grow from USD 1.96 billion in 2026 to reach USD 2.32 billion by 2031, at a CAGR of 3.48% during the forecast period (2026-2031). In terms of subscriber volume, the market is expected to grow from 50.49 million subscribers in 2025 to 60.96 million subscribers by 2030, at a CAGR of 3.84% during the forecast period (2025-2030). Continued network reconstruction, large-scale foreign investment, and fast-rising demand for resilient broadband collectively underpin this upward trajectory. The Ukraine telecom MNO market benefits from VEON’s USD 1 billion multi-year upgrade plan, joint EBRD-IFC funding of USD 435 million, and government schemes that target 95% high-speed internet coverage in underserved districts. [1]European Bank for Reconstruction and Development, “EBRD and IFC Investment in Ukrainian Telecom,” ebrd.com Mobile data traffic growth, widespread 4G restoration in liberated territories, and early preparations for 5G also reinforce momentum. Competitive strategies now emphasize infrastructure sharing, Open RAN deployment, and satellite-cellular integration, all of which compress costs and accelerate rural roll-outs. Simultaneously, the Ukrainian telecom MNO market is capturing new opportunities in agritech IoT, critical infrastructure backhaul, and digital platforms that extend beyond connectivity.

Key Report Takeaways

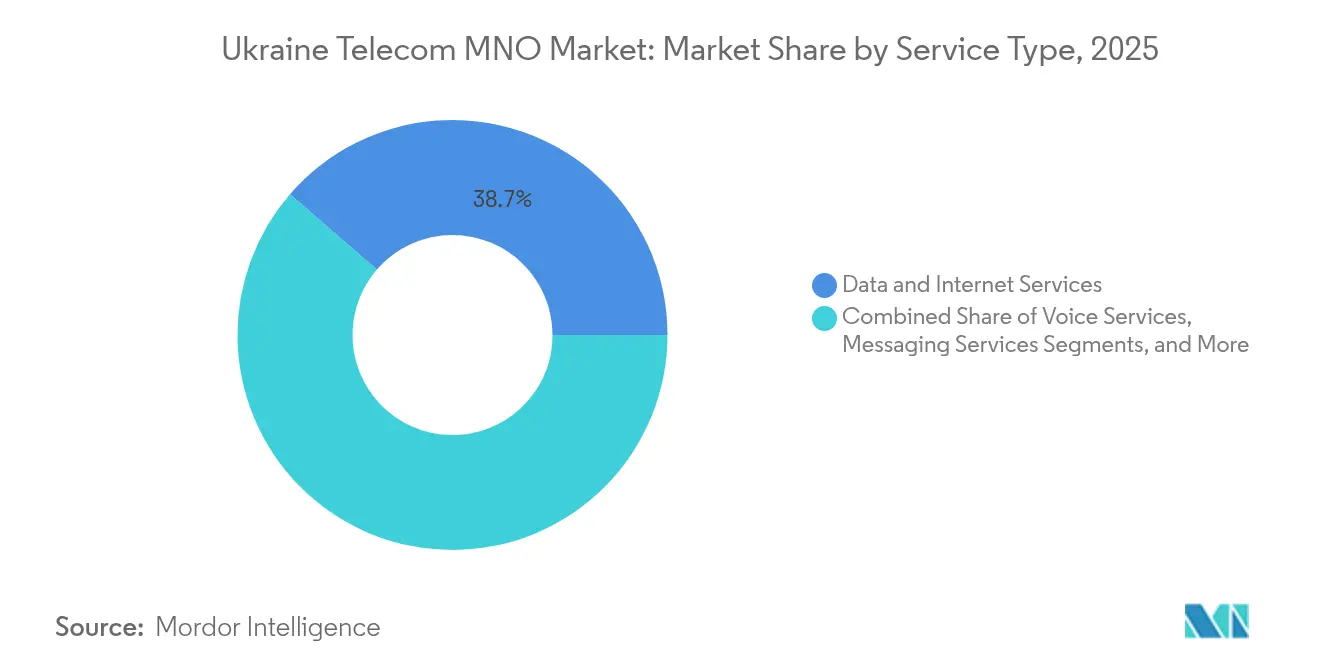

- By service type, Data and Internet Services captured 38.65% of Ukraine telecom MNO market share in 2025; IoT and M2M Services are projected to expand at a 4.29% CAGR to 2031.

- By end-user, the Consumer segment held 70.62% of the Ukraine telecom MNO market size in 2025, whereas the Enterprise segment is projected to rise at a 3.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Ukraine Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 4G/4G+ Network Expansion Post-War Reconstruction | +1.8% | National, priority in liberated territories | Medium term (2-4 years) |

| Government-Backed 5G Spectrum Roadmap and Relief on License Fees | +1.2% | National, early deployment in major cities | Long term (≥ 4 years) |

| Surge in Demand for Low-Latency Broadband for Critical Infrastructure (Defense, Energy) | +1.0% | National, concentrated in defense and energy sectors | Short term (≤ 2 years) |

| Rising Enterprise Digitization and Cloud Adoption Among SMBs | +0.8% | National, elevated in western regions | Medium term (2-4 years) |

| EU Roam-Like-at-Home Agreements Boosting Outbound Usage | +0.6% | National, benefiting 4 million refugees in EU | Short term (≤ 2 years) |

| Private LTE/5G Networks for Agritech and Mining Corridors | +0.4% | Rural agricultural regions and mining zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

4G/4G+ Network Expansion Post-War Reconstruction

Restoring connectivity has become a nation-building task. Kyivstar rebuilt 95% of damaged radio sites and added 828 base stations in Q1 2025 alone, lifting mobile broadband coverage to 95.9% even where up to 30% of hardware lay in ruins. [2]Kyiv Post, “Operators Restore Connectivity in Liberated Regions,” kyivpost.com All three operators now pool towers and civil works to stretch scarce capital, and their joint Open RAN pilot with Rakuten Symphony swaps vendor-locked boxes for cloud-native software that can be installed in days rather than weeks. [3]Symphony Rakuten, “Open RAN Collaboration with Kyivstar,” symphony.rakuten.com The Ministry of Digital Transformation backs the effort with a USD 6 billion seven-year fund earmarked for base-station rebuilds, high-capacity microwave links, and public Wi-Fi at schools and hospitals. Together, these actions enable the Ukrainian telecom market to reconnect frontline communities faster than power grids or roadways, turning mobile service into an early indicator of recovery. Operators also seize the opportunity to upgrade legacy 2G gear to LTE-Advanced radios, thereby increasing spectral efficiency and stabilizing energy consumption across the network.

Government-Backed 5G Spectrum Roadmap and Relief on License Fees

Regulators have circulated a draft spectrum release that pairs 700 MHz and 3.5 GHz blocks with discounted fees for carriers promising 90% population coverage within five years. That carrot matters in a capital-strained Ukrainian telecom market, where operators have spent over UAH 50 billion on 3G and 4G since 2015 and now face nearly double energy bills. Kyivstar has already repurposed 2100 MHz 3G airwaves to boost 4G capacity, trialing DSS software that allows radios to shift automatically between LTE and 5G once new licenses are issued. The roadmap also invites industrial players, ports, mines, and railways to bid for local 100 MHz slices under a private-network model that keeps critical data on-site. By easing license installments and aligning band plans with EU norms, Kyiv expects cross-border roaming and device procurement to improve, while investors gain a clearer view of medium-term cash needs in the Ukrainian telecom market.

Surge in Demand for Low-Latency Broadband for Critical Infrastructure

Missile-alert systems, drone command links, and real-time power-grid controls all need sub-10 ms round-trip latency, forcing a redesign of network topologies. Operators now install micro-data centers beside major substations and fuel depots, keeping traffic local rather than backhauling across the Dnipro. Kyivstar’s acquisition of Helsi, a national e-health platform, underscores how life-critical apps rely on those same links; surgeons in Lviv use 4K video consultations that tolerate no more than a five-millisecond lag. To hedge against fiber cuts, carriers lease Ku-band ground stations and chain Starlink nodes onto mobile base stations, a design that maintained 93% call-completion rates during January 2025 blackouts. Government tenders for hardened shelters specify dual terrestrial-satellite backhaul and mandate 48-hour battery autonomy, locking low-latency resilience into every new build. Those blueprints raise the technology bar for the entire Ukrainian telecom MNO market and create fresh revenue when defense agencies pay premium SLAs.

Rising Enterprise Digitization and Cloud Adoption Among SMBs

Fiber backbones are being extended from oblast capitals to industrial parks, allowing even 20-seat exporters to run ERP in Azure or AWS European zones without latency spikes. Cybersecurity sits at the top of procurement lists, with 71% of chief digital officers funneling budget into managed firewalls, DDoS shields, and SASE gateways. Operators answer by bundling secure cloud, Microsoft 365, and adaptive bandwidth into one invoice, lifting enterprise ARPU by almost 11% year on year. Ternopil and Lviv oblasts now outspend Kyiv on a per-company basis, demonstrating how reconstruction hubs attract remote staff and e-commerce storefronts. That wave of small-business modernization feeds sustained traffic growth across the Ukrainian telecom MNO market and partially offsets the low-margin prepaid consumer base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Power and Backhaul Disruptions in Conflict Zones | –1.5% | Eastern and southern frontline regions | Short term (≤ 2 years) |

| Currency Instability Pressuring CAPEX and OPEX Budgets | –0.8% | National, higher impact on import-dependent operations | Medium term (2-4 years) |

| High Cost of Imported Active Equipment under Sanctions and Logistics Bottlenecks | –0.5% | National | Medium term (2-4 years) |

| Limited Domestic Fiber Manufacturing Capacity | –0.3% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Power and Backhaul Disruptions in Conflict Zones

The International Energy Agency projects a 6 GW generation deficit during winter 2024/2025, a gap that already triggers evening brownouts from Odesa to Kharkiv. [4]International Energy Agency, “Ukraine Winter Power Outlook 2025,” iea.org Operators burned through UAH 1.4 billion on diesel gensets and lithium-phosphate packs to keep base stations live, yet still lost 11% of call minutes during the coldest week of January. Freedom House reports 60,000 km of lines severed since February 2022, forcing carriers to lay aerial cables or run microwave hops that halve their potential capacity. Even when crews rebuild, live mines delay trenching, and power crews must finish grid repairs first. The Ukrainian telecom MNO market, therefore, pivots toward mesh architectures that can reroute traffic in 200 milliseconds and fall back to satellite whenever two terrestrial legs fail.

Currency Instability Pressuring CAPEX and OPEX Budgets

Rising borrowing costs squeeze smaller internet service providers that rely on short-term overdrafts to pay customs and VAT ahead of subscriber revenue. Vodafone Ukraine trimmed its 2025 radio roadmap by 14% and postponed rural fiber in Kherson until currency swaps stabilized. The government’s FX “corridor” policy offers some predictability, but every 5% swing still shaves millions off free cash flow and delays 5G MIMO imports that the Ukrainian telecom MNO market needs for capacity relief.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data-Centric Usage Transforms the Market

Data and Internet Services generated 38.65% of 2025 revenue, giving the category the highest weighting within the Ukraine telecom MNO market share. Explosive mobile traffic, enterprise cloud migration, and bundled OTT video keep data services central to operator strategy. IoT and M2M services, advancing at a 4.29% CAGR, expand addressable opportunities in agriculture and smart municipalities.

Schools and councils in western oblasts are consistently upgrading their bandwidth, driven by the increasing demands of government portals, public-sector ERP systems, and digital document workflows. Continued fiber roll-out, Open RAN adoption, and government grants aimed at public service facilities solidify the data-centric evolution. In parallel, voice usage shifts into data channels via VoLTE and communications apps, tightening integration across service types and lifting average throughput per user in the Ukrainian telecom MNO market.

By End User: Enterprise Growth Edges Ahead

Consumers still account for 70.62% of 2025 revenue, but enterprise accounts are expanding more quickly at a 3.92% CAGR due to digital-first reconstruction and hybrid work models. SMB appetite for managed services, cybersecurity, and cloud connectivity deepens operator engagement, helping diversify income streams in the Ukrainian telecom MNO market.

Kyivstar's USD 155.2 million acquisition of ride-hailing firm Uklon integrates mobility services into its super-app, slightly increasing daily ARPU through ride micro-payments. Enterprise buyers now prefer three-year deals that bundle connectivity, Azure credits, and 24/7 SOC monitoring. Despite currency risks, multinational insurers and agribusinesses find these bundles more cost-effective than self-hosting or regional data export. These trends indicate that the enterprise segment will continue to narrow the gap, reducing the consumer share of Ukraine's telecom MNO market during the projected period.

Geography Analysis

Kyiv has traditionally served as the epicenter of Ukraine's telecom MNO market, but wartime migration has shifted the digital focus westward. Between early 2022 and mid-2025, Lviv's population increased by 16%. In response, telecom operators deployed 411 new LTE sites and established a 400 Gbps optical ring around the city. Ivano-Frankivsk and Ternopil received similar infrastructure upgrades, enabling local software exporters to deliver projects to European clients without latency issues. Despite these developments, Kyiv remains the leader in fiber penetration, with 92% of households connected. The city also hosts the country's two Tier-III data centers and accounts for one-third of Ukraine's mobile traffic, reinforcing its position as the nation's ICT hub.

In contrast, eastern regions such as Donetsk and Luhansk face significant network instability. Over 4,000 mobile sites and large sections of backbone fiber have been destroyed or remain inaccessible, resulting in inconsistent 2G coverage supported by satellite backhaul. Operators have been deploying generators and microwave dishes to newly reclaimed towns within 48 hours of clearance. However, as of May 2025, drive tests, approximately 4% of the population still experiences coverage gaps. Odesa and Mykolaiv encounter similar disruptions, particularly during naval attacks that impact power infrastructure. Cross-border usage introduces additional complexity. 22 European telecom operators have aligned their tariffs with domestic Ukrainian rates, reducing roaming costs for 4 million Ukrainian refugees residing in Poland, Germany, and Spain. By January 2026, Ukraine is expected to fully integrate into the EU's "roam-like-at-home" initiative, eliminating roaming fees. This policy encourages longer stays abroad without requiring SIM card changes, while compelling Ukrainian operators to maximize outbound wholesale revenues. At the same time, they anticipate that returning users will demand higher-quality services, intensifying competition within the domestic market.

Competitive Landscape

The Ukrainian telecom MNO market is indicating a consolidated competitive structure with three powerhouses. Kyivstar leads with a significant number of mobile users, base stations, and its own fiber network. Its deep rural reach allows it to price-differentiate, offering Kyivites gigabit fiber while maintaining lower-cost, lower-speed bundles in Chernihiv villages, thereby protecting both ends of its margin mix.

Vodafone Ukraine sits close behind, having invested USD 600 million since 2023 to densify 4G layers and turn on VoLTE/VoWiFi across all oblasts. The carrier relies on a German-style network-sharing ethos, co-installing radios with Lifecell on 2,427 towers, resulting in a 35% reduction in rental fees. To stand out, Vodafone promotes IoT kits for smart meters and cold-chain monitoring, capitalizing on logistics corridors that supply the EU market. It also pilots Open RAN slicing, allowing an agritech startup to rent a dedicated 10 MHz chunk in Kropyvnytskyi during harvest season, an early taste of demand-based wholesale that could become a material revenue stream.

Lifecell entered new hands after Xavier Niel’s consortium closed the USD 524 million Datagroup-Volia acquisition in September 2024. The merged entity pairs 10 million mobile lines with 4 million fixed-line and PayTV customers, creating Ukraine’s first truly converged challenger. Bundled quad-play at UAH 299 (USD 7.20) lures cost-conscious families, while fiber synergies let Lifecell backhaul 5G-ready cells without leasing from rivals. That integration pressures incumbents to revisit triple-play pricing and accelerates the shift toward platform revenue, which collectively redraws service boundaries within the Ukrainian telecom MNO market.

Ukraine Telecom MNO Industry Leaders

Vodafone Ukraine

Lifecell, LLC

Kyivstar PJSC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Kyivstar obtained clearance to pilot Starlink direct-to-cell SMS, with national launch planned for Q4 2025.

- May 2025: Vodafone Ukraine activated VoLTE and VoWiFi nationwide, promising higher-definition voice without extra charges.

- March 2025: Kyivstar bought ride-hailing app Uklon for USD 155.2 million, expanding its platform play.

- October 2024: EBRD and IFC jointly lent USD 435 million to modernize infrastructure, anchoring the new Datagroup-Volia-Lifecell entity.

- September 2024: Xavier Niel’s consortium closed the USD 524 million Datagroup-Volia-Lifecell takeover.

- February 2024: Kyivstar and Rakuten Symphony signed an Open RAN letter of intent, backed by VEON’s USD 1 billion investment envelope.

Ukraine Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the current value of the Ukraine telecom MNO market?

The Ukraine telecom MNO market size is USD 1.96 billion in 2026 and is projected to reach USD 2.32 billion by 2031.

Which service type leads in revenue?

Data and Internet Services generate the highest revenue, accounting for 38.65% of 2025 turnover.

How fast is IoT and M2M services growing in Ukraine’s telecom sector?

IoT and M2M Services are the fastest-growing category, expanding at a 4.29% CAGR through 2031.

When will Ukraine join the EU roam-like-at-home zone?

Full inclusion is scheduled for January 2026, eliminating extra roaming charges across 27 EU countries.

Who are the main telecom operators in Ukraine?

Kyivstar PJSC, Vodafone Ukraine, and Lifecell, LLC dominate, collectively serving more than 50 million mobile subscribers.

What technological shift is most critical after the war?

Rapid 4G reconstruction combined with early 5G spectrum planning and satellite-cellular integration are the key technological shifts.

Page last updated on: