Sweden Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

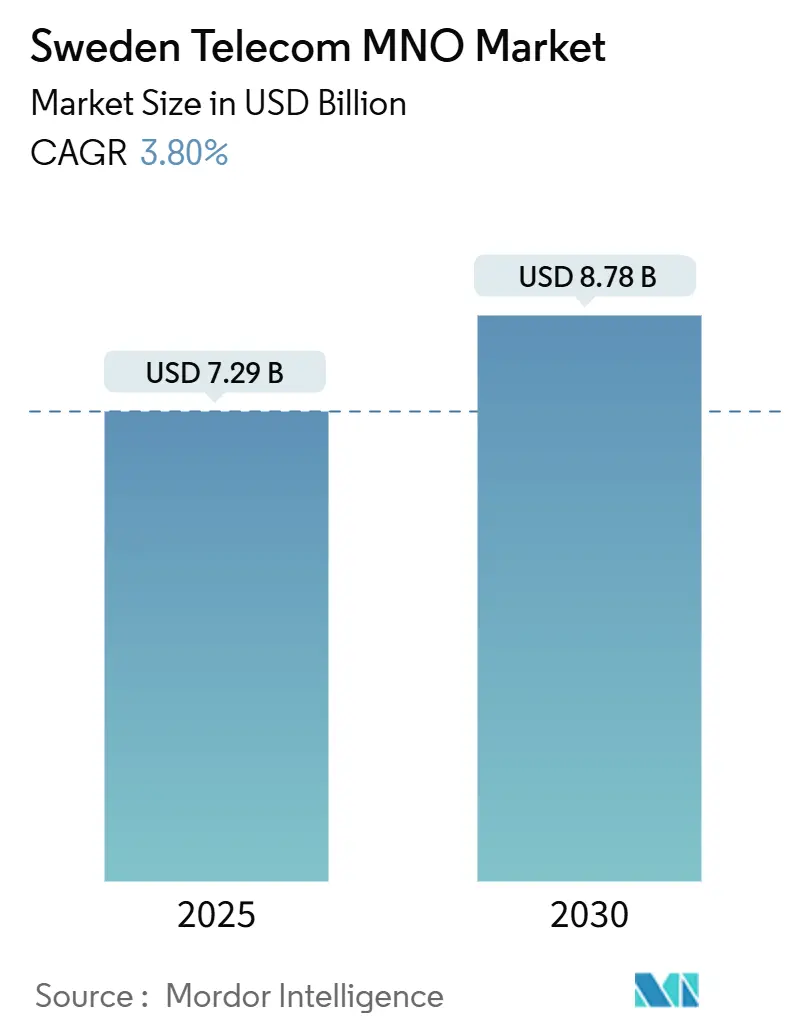

| Market Size (2025) | USD 7.29 Billion |

| Market Size (2030) | USD 8.78 Billion |

| Growth Rate (2025 - 2030) | 3.80% CAGR |

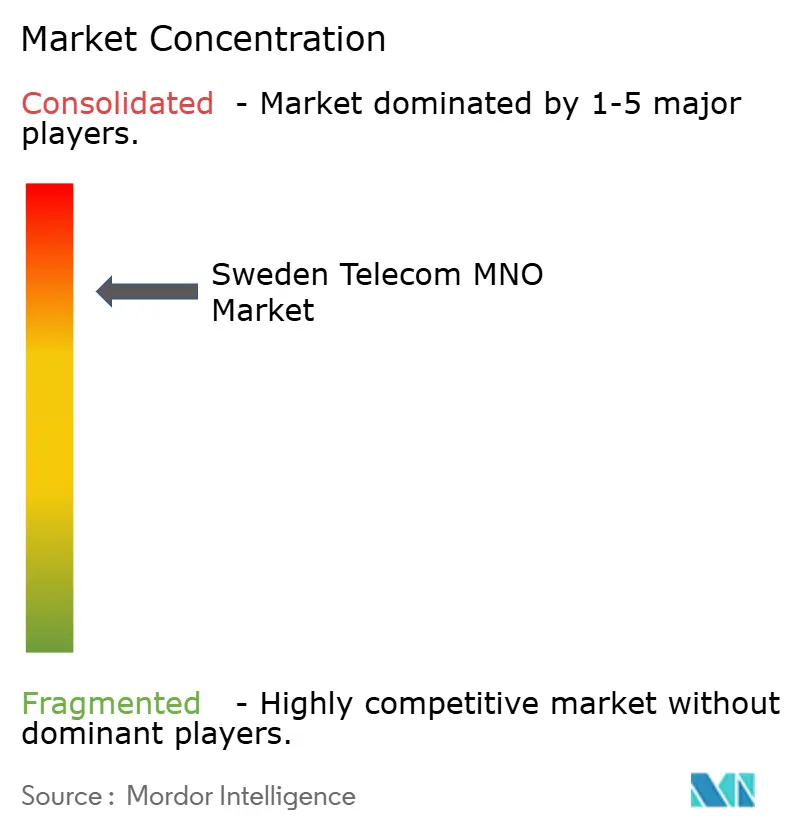

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sweden Telecom MNO Market Analysis by Mordor Intelligence

The Sweden Telecom MNO Market size is estimated at USD 7.29 billion in 2025, and is expected to reach USD 8.78 billion by 2030, at a CAGR of 3.80% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 17.02 million Subscribers in 2025 to 19.73 million Subscribers by 2030, at a CAGR of 3% during the forecast period (2025-2030).

This measured expansion reflects the sector’s pivot from voice-centric offerings toward data-intensive applications such as enhanced mobile broadband and massive machine-type communications. Growing 5G availability of 77.8% in 2025, rising average data usage per subscriber, and government-backed fiber backhaul targets underpin revenue opportunities, while operators balance capital-expenditure efficiency through network-sharing ventures. Competitive intensity remains high even in this concentrated arena, prompting differentiated service bundles around IoT, cloud connectivity, and private 5G for industrial users. Meanwhile, pressure from falling voice ARPU and elevated energy costs incentivizes investments in green-network solutions that trim operating expenditures.

Key Report Takeaways

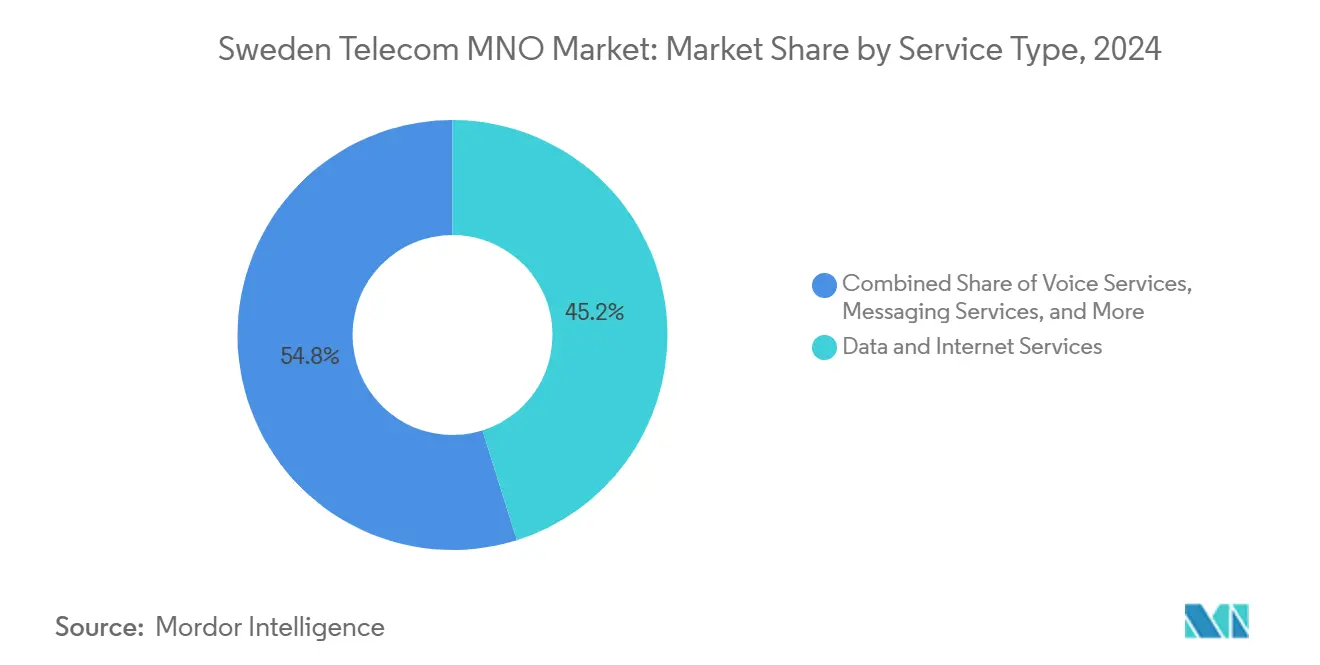

- By service type, Data and Internet services led with 45.16% revenue share in 2024, while IoT and M2M services are projected to expand at a 5.26% CAGR through 2030.

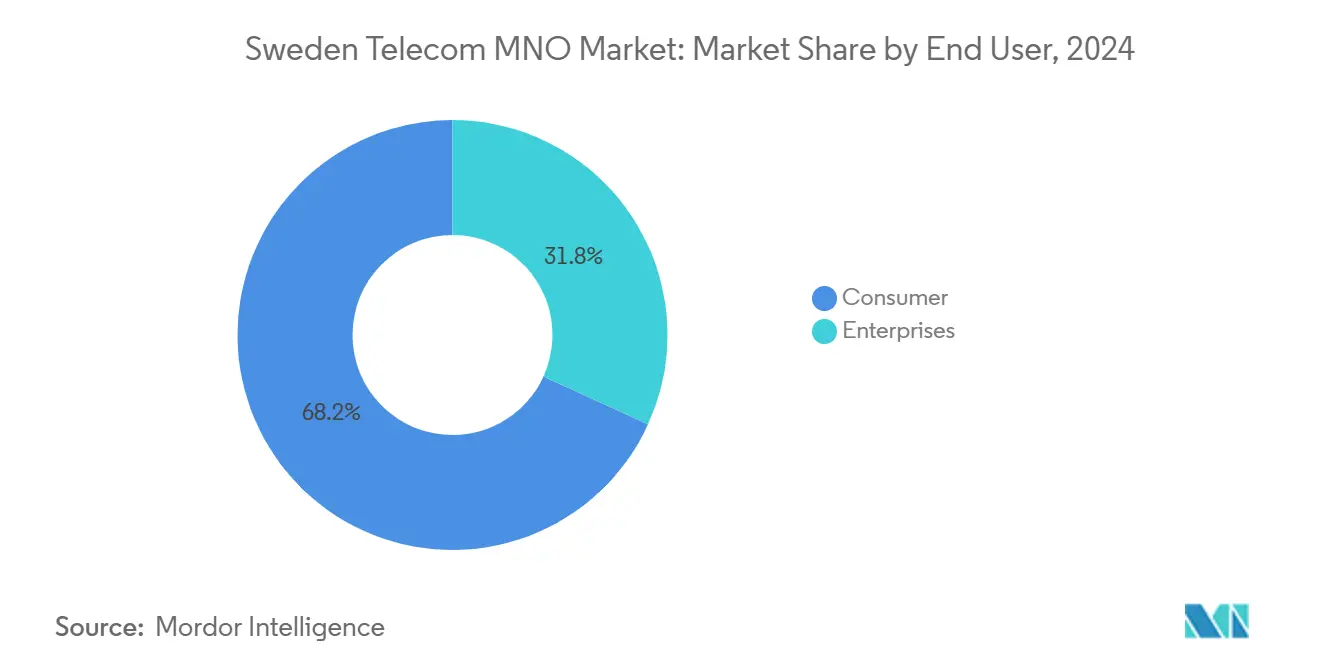

- By end-user, the consumer segment accounted for 68.19% of the Sweden Telecom MNO market share in 2024, whereas enterprise subscriptions are set to rise at a 4.12% CAGR between 2025 and 2030.

Sweden Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nationwide 5G rollout accelerating service upgrades | +1.2% | National, with urban concentration in Stockholm, Gothenburg, Malmö | Medium term (2-4 years) |

| Surging mobile-data consumption per user | +0.8% | National, with higher impact in urban areas | Short term (≤ 2 years) |

| Government-backed fiber-to-the-home (FTTH) expansion targets | +0.6% | National, with rural area focus | Long term (≥ 4 years) |

| Rapid adoption of IoT for smart metering and logistics | +0.7% | National, with industrial concentration in northern Sweden | Medium term (2-4 years) |

| Green-network CAPEX incentives (energy-efficiency mandates) | +0.3% | National | Long term (≥ 4 years) |

| Demand for private 5G networks in mining and manufacturing hubs | +0.4% | Regional, concentrated in Norrbotten and Västerbotten | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Nationwide 5G rollout accelerating service upgrades

Operators reached more than 90% population coverage by late 2024, with Telia alone at 97% and the Tele2-Telenor joint venture Net4Mobility covering 90%. [1]Telia Company, “Telia Annual Report 2024,” Telia.comDeployment across low-band 700 MHz for coverage and 3.5 GHz for capacity enables enhanced mobile broadband and low-latency services for enterprises. Sweden’s proactive spectrum policy, which bundled coverage obligations with licenses, shortened time-to-market, and positioned the Sweden Telecom MNO market as an attractive testbed for advanced use cases. The aggressive build-out also supports revenue diversification as operators launch high-tier 5G packages, benefiting both consumer and enterprise segments. Continuous investment in a standalone 5G architecture is now unlocking private-network propositions for manufacturing and mining clients.

Surging mobile-data consumption per user

Mobile data rose 697% between 2019 and 2023 to 260,176 TBytes, reflecting the ubiquity of video streaming, cloud collaboration, and remote-work tools. [2]Olov Enström, “Svensk Telekommarknad 2023,” Post- och telestyrelsen, Pts.se This surge sustains capacity upgrades and allows tiered pricing strategies that lift ARPU despite price competition. Telia’s five-year record of network-quality leadership reinforces its ability to charge a premium for high-data plans. With 28% of subscriptions already on 5G by end-2023, data-centric tariffs drive incremental revenue while encouraging adoption of value-added content and cloud services. Higher data usage also accelerates traffic offload to Wi-Fi and small-cell solutions, easing macro-network congestion.

Government-backed fiber-to-the-home expansion targets

The Swedish government's broadband strategy, "A Completely Connected Sweden by 2025," outlines goals to meet users' connectivity needs. Adopted in December 2016, it aims for 95% of households and businesses to have digital connectivity of at least 100 Mbps by 2020. By 2025, 98% of households and businesses are expected to access high-speed connectivity with a minimum capacity of 1 Gbps, along with reliable, high-quality mobile services. [3]European Commission, “Broadband in Sweden,” Digital-strategy.ec.europa.eu Fiber deployment improves rural inclusion and supplies cost-efficient backhaul for 5G sites, particularly outside dense urban cores. Operators leverage the expanded fiber footprint to densify 5G deployments without prohibitive leased-line expenses, enhancing network quality for both mobile and fixed-wireless access. Streamlined permitting and co-investment policies further cut rollout timelines, creating positive spillovers for the Sweden Telecom MNO market in terms of lower opex and higher service reliability.

Rapid adoption of IoT for smart metering and logistics

Telia has connected over 2 million smart-meter endpoints via NB-IoT and Cat-M1, illustrating the shift toward low-power wide-area technologies that replace legacy 2G/3G links. [4]Ericsson, “The Power of IoT Connectivity – Mobility Report,” Ericsson.com Utilities benefit from granular consumption data, while operators monetize connectivity plus platform services. Beyond energy, cellular IoT supports temperature-controlled logistics, fleet management, and condition monitoring across Sweden’s export-oriented manufacturing base. Phasing out 2G/3G frees spectrum for 5G, improves carbon efficiency, and widens the addressable enterprise market for operators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Erosion of voice-service ARPU | -0.6% | National | Short term (≤ 2 years) |

| Intensifying price wars among MNOs and MVNOs | -0.8% | National, with urban concentration | Short term (≤ 2 years) |

| Environmental permitting delays for new towers | -0.3% | National, with rural area focus | Medium term (2-4 years) |

| Rising energy costs pressuring OPEX | -0.4% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Erosion of voice-service ARPU

Fixed-line call minutes fell 13% in 2024 as consumers pivoted to OTT voice and messaging apps, compressing legacy-service revenues. Younger demographics rarely pay for traditional telephony, forcing operators to bundle unlimited voice within data plans. While the share of voice in total service revenue continues to contract, the trend accelerates spectrum refarming from 2G/3G toward 4G and 5G. Operators therefore treat voice as a retention tool rather than a profit center, focusing on new value creation on digital services and connectivity.

Intensifying price wars among MNOs and MVNOs

Average mobile subscription prices declined from SEK 282 to SEK 259 per month between 2018 and 2023 despite expanding data allowances. Wholesale-access regulation encourages MVNO entry, and incumbent operators counter with secondary brands that wage aggressive discount campaigns. Although the Sweden Telecom MNO market remains concentrated, headline tariffs in the consumer segment face downward pressure that offsets gains from higher data volumes. Margin defense increasingly relies on cost-efficient shared infrastructure and automation rather than retail price hikes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data-Centric Portfolio Reshapes Revenues

Data and Internet services generated 45.16% of 2024 revenue, underscoring the Sweden Telecom MNO market transition toward bandwidth-heavy applications. The segment captured the largest slice of the Sweden Telecom MNO market share on the back of 5G adoption and consumption of streaming, cloud gaming, and enterprise SaaS traffic. IoT and M2M connectivity, although currently smaller in absolute value, is projected to register a 5.26% CAGR, outpacing other categories and adding high-margin platform services. In contrast, voice and messaging revenue continues its structural slide, reinforcing the need for operators to position 5G and fiber backhaul as enablers of next-generation digital services. OTT and PayTV bundles, such as Telia’s hybrid AVOD/SVOD model, provide cross-selling upside and mitigate churn. Other services, such as roaming, wholesale transit, and value-added enterprise connectivity, supply stable cash flows that complement data-centric growth initiatives.

Second-order effects of this portfolio realignment include traffic patterns that demand agile network slicing, while regulatory incentives to sunset 3G by 2025, and free spectrum for capacity boosters. Operators also experiment with edge-cloud integrations to offer ultra-low-latency applications for gaming and industrial automation. Taken together, the evolving service mix enables the Sweden Telecom MNO market size for high-value digital services to expand faster than traditional connectivity alone, supporting gradual ARPU uplift despite retail price competition.

By End-User: Enterprise Connectivity Outpaces Consumer Growth

The consumer segment commanded 68.19% of 2024 revenue, reflecting saturation in SIM penetration and stable demand for unlimited data bundles. However, enterprise subscriptions are forecast to grow by 4.12% CAGR through 2030, driven by Sweden’s push toward Industry 4.0 and private 5G deployments in mining, manufacturing, and logistics. Early projects at Boliden mines and Saab factories showcase autonomous vehicles, real-time condition monitoring, and AR-assisted maintenance, reinforcing the value proposition of ultra-reliable low-latency communication. As a result, the Sweden Telecom MNO market size linked to enterprise applications is poised to widen its revenue contribution. Operators tailor SLAs, network slices, and managed-service bundles that embed connectivity within long-term digital-transformation contracts, ensuring stickier relationships and higher margins relative to the consumer base.

Consumer-segment growth, while modest, continues to benefit from higher data usage per capita and 5G handset upgrades. Yet price-sensitive sub-segments gravitate toward MVNO offerings, compelling mainline brands to differentiate through superior network quality, converged mobile-fixed bundles, and loyalty programs. In the Sweden Telecom MNO industry, winning strategies, therefore, balance enterprise-focused innovation with consumer-centric simplicity and value.

Geography Analysis

Urban Sweden, principally Stockholm, Gothenburg, and Malmö, accounts for the bulk of 5G traffic and enterprise service adoption, reflecting dense population centers and technology-oriented industry clusters. These cities showcase near-ubiquitous outdoor 5G coverage plus deep indoor enhancements, supporting advanced cloud and edge use cases. The Sweden Telecom MNO market size in metropolitan areas attracts the highest capital intensity; however, network-sharing agreements moderate spending while preserving competitive differentiation on service quality.

Northern regions such as Norrbotten and Västerbotten leverage private 5G networks to modernize mining and forestry operations, anchoring regional demand for ultra-reliable connectivity. Government broadband subsidies also prioritize sparsely populated municipalities, where expanded fiber backhaul makes rural 5G economically viable. As fiber reaches 98% of households with gigabit speeds by 2025, rural inclusion narrows the digital divide and supports remote work, telehealth, and agritech solutions that depend on robust mobile networks.

Sweden’s cold climate provides natural cooling advantages for data centers, drawing hyperscale investments like Microsoft’s USD 3.2 billion cloud build-out. Such projects stimulate additional traffic across operator backbones and justify peering upgrades, thereby enlarging the Sweden Telecom MNO market. Cross-border interconnections with Norway, Finland, and Denmark foster Nordic network resilience, yet Sweden remains the regional leader in 5G availability owing to early spectrum auctions and clear regulatory roadmaps. From now on, geographic strategy will hinge on balancing high-capacity urban densification with cost-effective rural rollouts, leveraging shared infrastructure and green-energy sources to cap opex.

Competitive Landscape

Four operators, Telia, Tele2, Telenor, and 3 Sweden, control a major share of the Sweden Telecom MNO market, creating an oligopoly where technology leadership and customer experience, rather than coverage gaps, define rivalry. Network-sharing ventures, most prominently Net4Mobility between Tele2 and Telenor, covering 90% of the population, allow rapid 5G deployment while curbing capital outlays. Telia maintains an edge through premium network quality and nationwide spectrum holdings, whereas 3 Sweden differentiates with aggressive unlimited-data offers and claims of the fastest average 5G speeds.

Regulatory scrutiny prevents anti-competitive collusion, requiring wholesale access for MVNOs that intensifies price pressure in the consumer segment. Operators thus seek margin recovery by upselling enterprise solutions such as private 5G, edge-cloud services, and IoT platforms. Telia’s exit from Denmark freed balance-sheet capacity to pursue Nordic 5G leadership, while Tele2’s 2025 transformation program targets opex efficiency through IT simplification and automation. Telenor, leveraging its global IoT test lab in Karlskrona, positions itself as a cross-border connectivity partner for multinational enterprises. Overall, sustained investment obligations embedded in spectrum licenses foster continual innovation, preventing complacency despite a concentrated structure.

Sweden Telecom MNO Industry Leaders

Telia Company AB

Tele2

Telenor Sverige

3 Sweden (Hi3G Access)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Tele2 and Telenor expanded 5G coverage beyond 90% population through Net4Mobility, delivering 200-800 Mbit/s speeds on 3.6 GHz spectrum.

- September 2024: 3 Sweden joined a global network-API initiative with Ericsson to monetize advanced network capabilities.

- June 2024: Microsoft committed USD 3.2 billion to Swedish cloud infrastructure, boosting demand for high-capacity connectivity.

- May 2024: Tele2 deployed 5G at the Swedish National Arena in Stockholm to enhance event-venue connectivity.

- April 2024: Telia completed the USD 920 million sale of its Danish unit to Norlys to sharpen its Nordic focus.

Sweden Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the current value of the Sweden Telecom MNO market?

The market stood at USD 7.29 billion in 2025 and is projected to reach USD 8.78 billion by 2030, reflecting a 3.8% CAGR.

Which operator leads Sweden in 5G population coverage?

Telia leads with 97% population coverage, followed closely by the Tele2-Telenor Net4Mobility network at 90%.

Which service category is growing fastest?

IoT and M2M connectivity is forecast to grow at a 5.26% CAGR, driven by smart metering and logistics deployments.

Why are voice revenues declining?

Consumers continue shifting to over-the-top voice and messaging apps, causing traditional voice ARPU to fall and prompting operators to focus on data-centric bundles.

How does network sharing affect competition?

Shared infrastructure, such as Net4Mobility, lowers capital costs and speeds 5G rollout, allowing operators to compete on service innovation rather than basic coverage.

What role do private 5G networks play in Sweden’s industry?

Mining, manufacturing, and logistics companies deploy private 5G for autonomous operations, real-time analytics, and safety monitoring, creating a new enterprise revenue stream for operators.

Page last updated on: