Cyber Ranges And Simulation Platforms Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

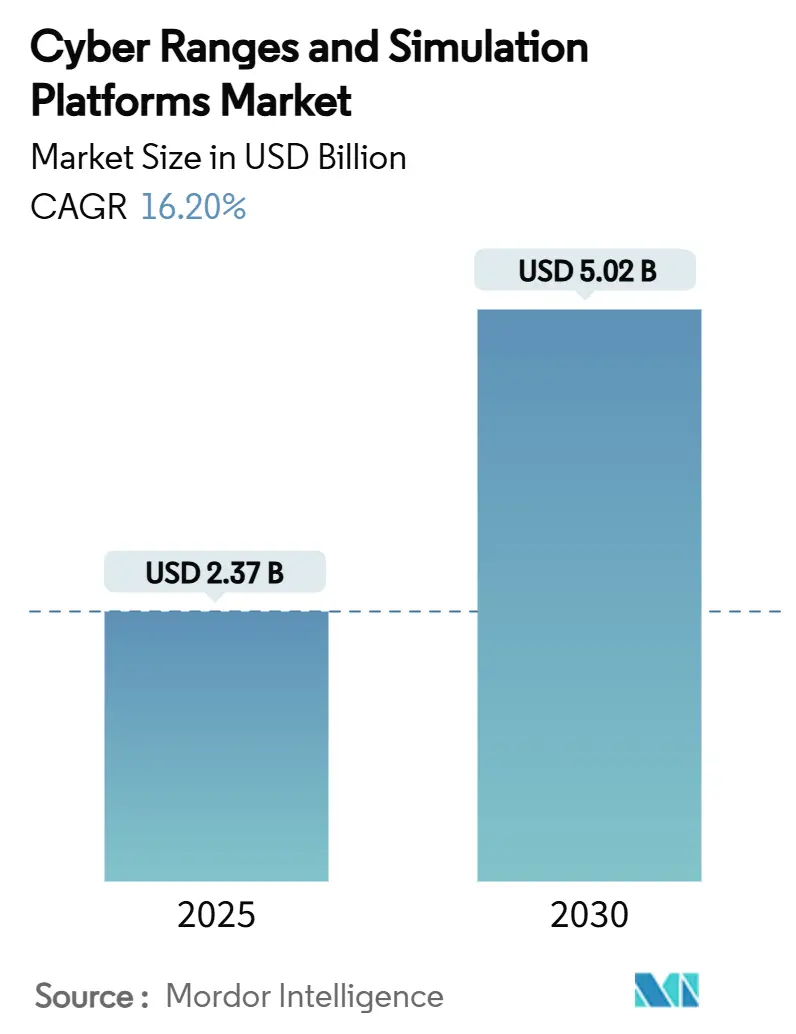

| Market Size (2025) | USD 2.37 Billion |

| Market Size (2030) | USD 5.02 Billion |

| Growth Rate (2025 - 2030) | 16.20% CAGR |

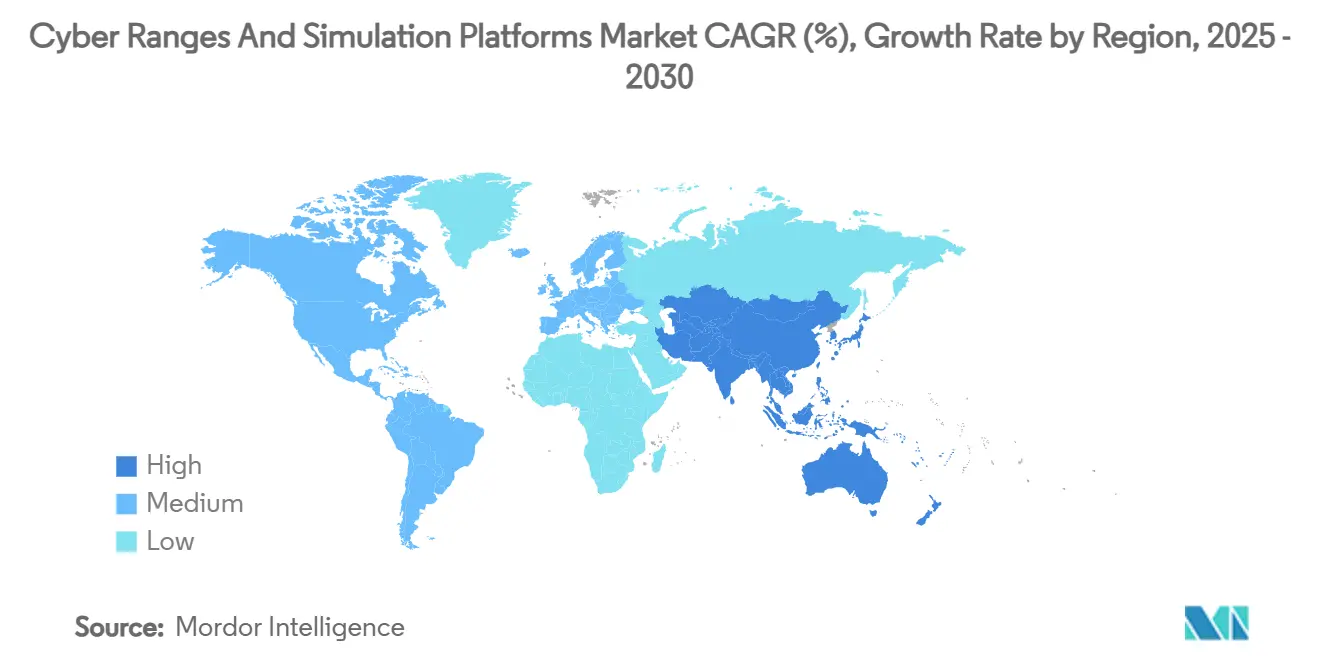

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

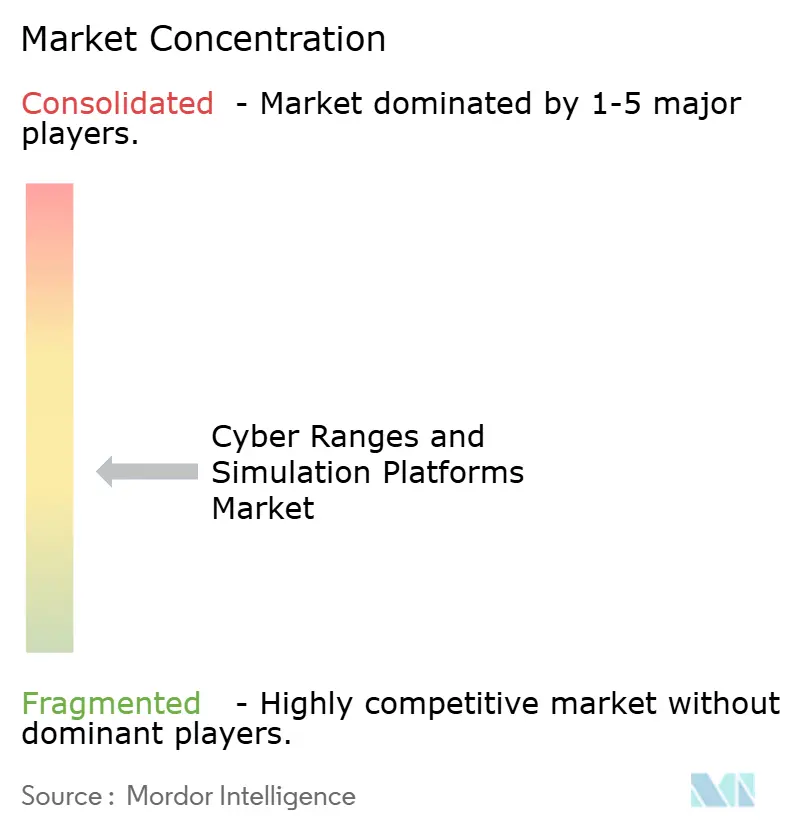

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cyber Ranges And Simulation Platforms Market Analysis by Mordor Intelligence

The cyber ranges and simulation platforms market size reached USD 2.37 billion in 2025 and is forecast to advance to USD 5.02 billion by 2030, posting a sturdy 16.2% CAGR. Rising attack sophistication, tighter regulatory scrutiny, and the shift from classroom theory to hands-on skills development are expanding demand across defense agencies, financial institutions, and critical-infrastructure operators. Mandatory cyber-readiness drills in banking, procurement of digital-twin ranges for mission rehearsal, and adoption of cloud delivery that strips out capital expense collectively accelerate platform uptake. Service-oriented buying behavior shows that many organizations now outsource scenario design and performance analytics instead of owning tooling outright. Meanwhile, small and mid-size enterprises gain low-friction access to enterprise-grade training through consumption-based cloud models, further broadening the total addressable base for the cyber ranges and simulation platforms market.

Key Report Takeaways

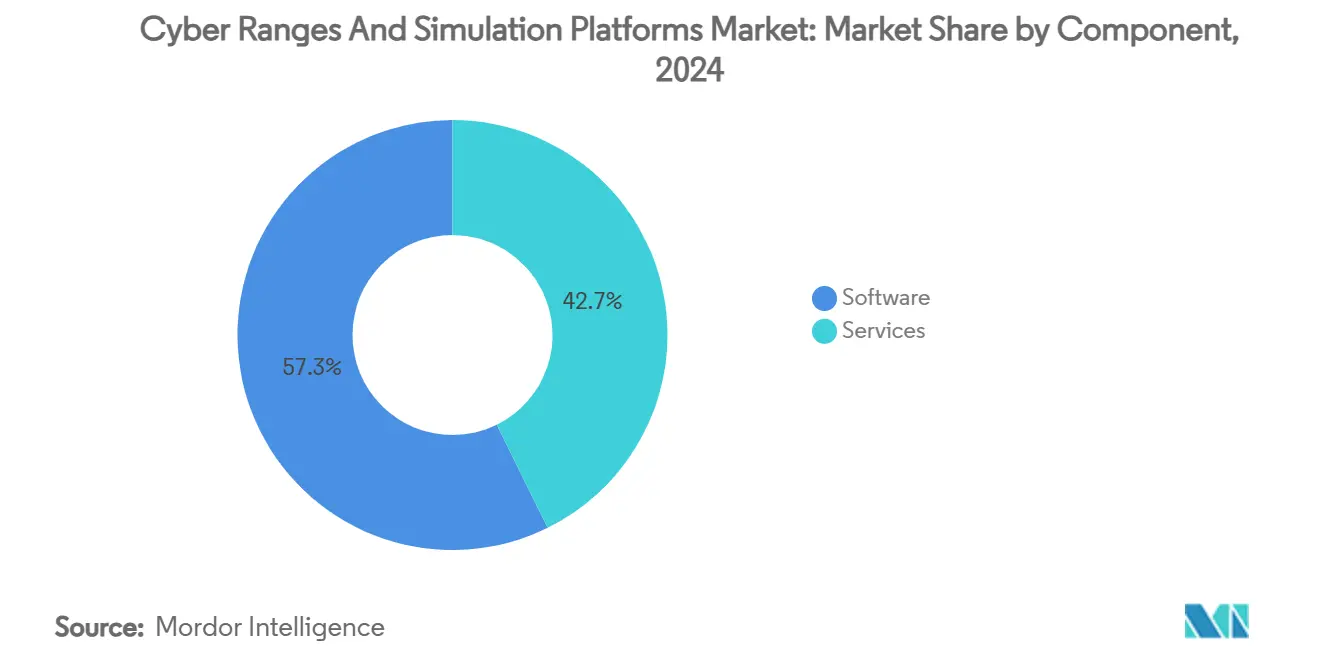

- By component, software led with 57.3% revenue share of the cyber ranges and simulation platforms market in 2024, while services are projected to expand at an 18.1% CAGR through 2030.

- By range type, simulation environments captured 44.3% of 2024 revenue in the cyber ranges and simulation platforms market, whereas hybrid ranges are expected to grow at a 17.3% CAGR to 2030.

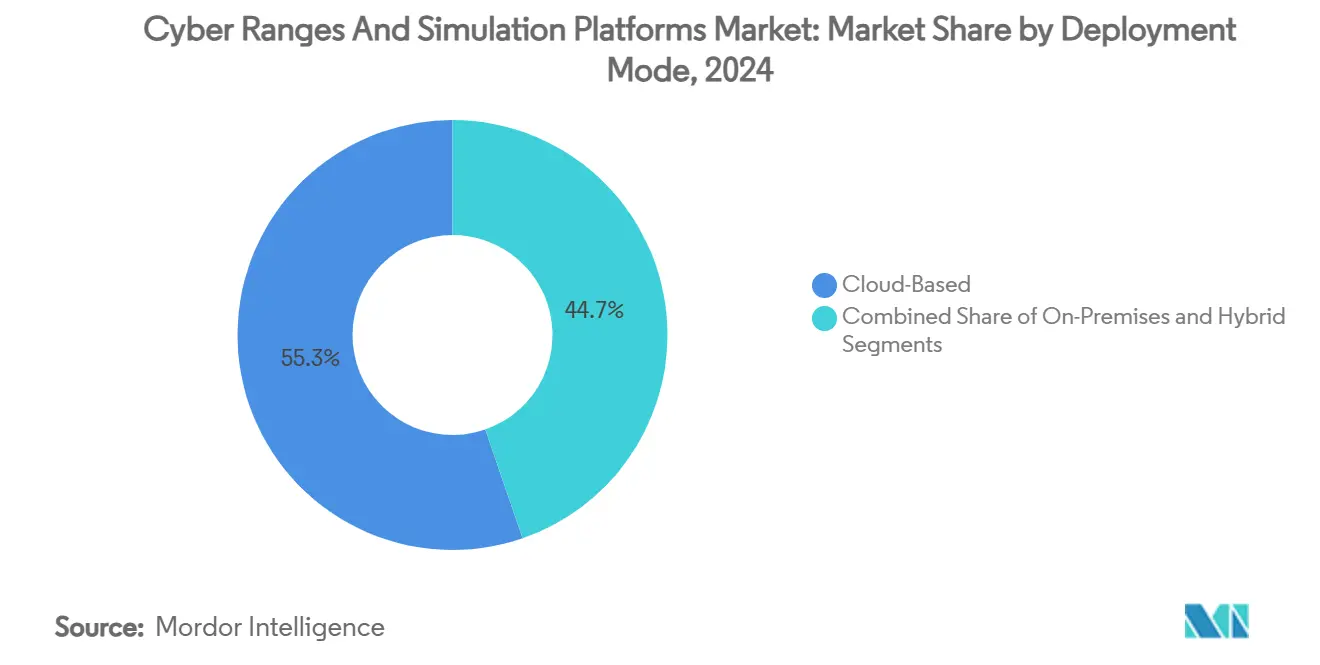

- By deployment mode, cloud-based solutions commanded a 55.3% share of the cyber ranges and simulation platforms market in 2024 and remain the fastest-growing option with a 17.1% CAGR through 2030.

- By end-user, defense and security agencies accounted for a 32.7% share of the cyber ranges and simulation platforms market in 2024, while BFSI demand is advancing at a 17.2% CAGR to 2030.

- By application, training and certification held a 45.8% share of the cyber ranges and simulation platforms market in 2024, whereas threat intelligence and analysis is projected to post the highest 17.4% CAGR through 2030.

- By geography, North America generated 38.3% of 2024 revenue in the cyber ranges and simulation platforms market, while Asia-Pacific is forecast to record the quickest 17.0% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cyber Ranges And Simulation Platforms Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging cyber-attack frequency across critical infrastructure | +3.2% | Global – North America and Europe in focus | Short term (≤ 2 years) |

| Escalating regulatory-mandated cyber-readiness drills | +2.8% | North America and the EU, spreading to APAC | Medium term (2–4 years) |

| Defense digital-twin adoption for mission rehearsal | +2.1% | North America, Europe, select APAC | Long term (≥ 4 years) |

| Cloud-native range delivery lowers TCO for SMEs | +2.5% | Global; early adopters in developed markets | Short term (≤ 2 years) |

| Generative-AI powered threat emulation accelerators | +1.9% | Global; led by North America and Europe | Medium term (2–4 years) |

| Integration with 5G/OT testbeds for converged security | +1.7% | APAC core; spill-over to North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Cyber-Attack Frequency Across Critical Infrastructure

Manufacturing, energy, and transport operators now experience record ransomware volumes, with Singapore’s Cyber Security Agency logging 132 incidents in 2023 that mainly struck industrial environments. [1]Cyber Security Agency of Singapore, “Fall in Phishing, Infected Infrastructure and Website Defacement Incidents Reported to CSA in 2023,” csa.gov.sg This escalation propels demand for operational-technology ranges embedding real controllers and sensor networks. Idaho National Laboratory’s expanded ICS programs illustrate how authentic equipment enriches scenario fidelity. [2]Idaho National Laboratory, “ICS Cybersecurity Training,” inl.gov Exercises such as Liberty Eclipse and GridEx VII underline coordination gaps between cyber teams and grid operators, reinforcing the need for multi-disciplinary simulations. Energy utilities now view cyber training as a safety imperative because failures can trigger physical disruptions. The U.S. Department of Energy’s CyTRICS initiative confirms the trend by stress-testing energy components inside purpose-built ranges.

Escalating Regulatory-Mandated Cyber-Readiness Drills

Financial watchdogs require evidence-based drills rather than policy checklists. New York’s updated 23 NYCRR 500 forces banks to run penetration tests and incident simulations each year. Europe’s DORA imposes harmonised operational-resilience testing across the bloc. FINRA’s 2025 oversight report flags AI-enabled phishing as a top risk and advises member firms to use ranges for response rehearsals. These rules generate continuous demand for platforms that log participant metrics and produce audit-ready evidence, shifting buying criteria from feature lists to outcome documentation.

Defense Digital-Twin Adoption for Mission Rehearsal

Armed forces replicate command networks through digital twins to test cyber and kinetic responses under realistic latency and data-flow conditions. CybExer Technologies integrates twin models into its range so operators can visualise system behaviour while attacks unfold. Booz Allen Hamilton’s carrier-grade 5G labs show how wireless edge and cloud nodes can be fused for air-gapped training. Linking live units with constructive traffic elevates situational awareness and supports coalition exercises where national infrastructures differ. The push toward multi-domain operations ensures that the cyber ranges and simulation platforms market keeps expanding within defense budgets.

Cloud-Native Range Delivery Lowers TCO for SMEs

Moving ranges into public cloud cuts procurement cycles from months to hours. Cyberbit prices one-year SaaS licenses at USD 7,200, far below the six-figure capex once required for on-premises hardware. Automated provisioning using infrastructure-as-code templates allows administrators to spin up hundreds of virtual machines on demand. SMBs, universities, and regional SOCs therefore access the same attack libraries once restricted to national labs. Integration with cloud SIEM and endpoint agents lets trainees validate playbooks that mirror production toolsets, accelerating the cyber ranges and simulation platforms market penetration among resource-constrained buyers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital outlay for immersive physical ranges | -2.1% | Global; most acute for mid-market firms | Short term (≤ 2 years) |

| Shortage of skilled cyber-range content developers | -1.8% | Global; largest gap in APAC and emerging markets | Medium term (2–4 years) |

| Inter-operability gaps between proprietary range stacks | -1.4% | Global; enterprise deployments | Medium term (2–4 years) |

| Data-sovereignty concerns in cross-border range sharing | -1.2% | EU, APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Outlay for Immersive Physical Ranges

Building physical ranges with real switches, PLCs, and SCADA equipment can top USD 1 million. HP’s Wolf Security report shows that 60% of buyers overlook security during device procurement, inflating retrofit budgets. [3]HP Inc., “Wolf Security Lifecycle Report,” hp.com Industrial buyers must also fund power, cooling, and secure facilities, making pure physical builds untenable for many. Virtualised ranges reduce spend, yet certain kinetic scenarios—such as power-grid failovers—still require tangible gear. Organisations therefore delay investment or adopt limited-scope pilots, restraining near-term growth in the cyber ranges and simulation platforms market.

Shortage of Skilled Cyber-Range Content Developers

Only a narrow talent pool can fuse offensive techniques, defensive controls, and instructional design. NIST’s supply-chain guidance states that vendor reliance rises when internal skills lag. Competing salaries within red-team consultancies and threat-intelligence firms worsen attrition. The gap pushes buyers toward managed-service contracts, yet capacity constraints still slow project rollouts. Vendors respond by launching certification programmes and partnering with universities, but medium-term friction is expected.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Managed Services Redefine Value Delivery

Software engines delivered 57.3% of 2024 revenue, underscoring the role of hypervisors, orchestration layers, and analytics dashboards in building realism. Within this domain, AI-assisted threat generation and drag-and-drop network builders reduce scenario lead times. However, enterprises increasingly outsource the heavy lifting. The services segment is tracking an 18.1% CAGR as buyers prefer turnkey curriculum design, live coaching, and post-exercise remediation guidance. Managed providers operate continuous-learning cycles where scenarios update weekly, ensuring relevance without internal headcount strain. This pivot signals that the cyber ranges and simulation platforms market is maturing from a product to an outcome economy.

In practice, providers like Cloud Range embed commercial SIEM, firewall, and EDR stacks inside their ranges so that blue teams rehearse using the same tooling seen in production. Post-event analytics translate performance data into board-level metrics such as mean-time-to-detect. As these insights feed risk dashboards, more CISOs justify subscription renewals, fortifying recurring revenue streams that underpin market stability.

By Range Type: Hybrid Architectures Bridge Realism and Scale

Virtual simulation ranges held 44.3% of the 2024 share thanks to their low entry cost and linear scalability. Universities deploy hundreds of concurrent student pods without physical racks, while enterprises use simulation to certify new hires before granting production access. Yet hybrid designs that marry virtual layers with select physical assets are scaling fastest at 17.3% CAGR. Oil-and-gas majors, for instance, insert actual PLC racks into virtual pipelines to emulate sensor latency and signal noise. The combination supports high-fidelity rehearsals without building entire plants in a lab.

Overlay and emulation ranges cater to niche, protocol-level testing where packet timing or device firmware nuances are mission-critical. Although smaller in absolute dollars, these niches often command premium pricing because of specialised equipment and content.

By Deployment Mode: Cloud Dominance Reconfigures Procurement Cycles

Cloud-based delivery accounted for 55.3% of 2024 revenue and is expanding at a 17.1% CAGR. Buyers cite zero hardware, pay-as-you-grow economics, and instant scenario updates as top advantages. Within this model, regional points of presence meet latency and data-residency needs, widening use cases. The cyber ranges and simulation platforms market size attached to on-premises deployments remains steady among defence and critical-infrastructure operators that need air-gaps for classified work. Hybrid deployment—using elastic cloud capacity for general training and hardened local nodes for sensitive exercises—addresses enterprises with mixed risk profiles.

Cloud acceleration is reinforced by vendor marketplaces where customers spin up ranges via a few API calls. Integration with IAM and ticketing systems embeds cyber drills into daily IT workflows, mainstreaming continuous cyber-readiness over episodic events.

By End-user: Defence Continues to Spend, but BFSI Ramps Fast

Defence and security agencies held 32.7% market share in 2024 as cyber warfare doctrine prioritised live-fire rehearsal. Programmes such as Project Tripoli validate combined arms responses to electronic warfare across 5G networks, reaffirming demand. In contrast, BFSI buyers are clocking a 17.2% CAGR on the back of tightening resilience mandates. Ranges help banks demonstrate controls efficacy under DORA and NY DFS audits, turning drills into regulatory artefacts.

Industrial and healthcare operators follow as ransomware shifts from data theft to operational disruption. Academic institutions leverage vendor-hosted ranges to fill curriculum gaps and certify graduates under national workforce initiatives, seeding future demand for the cyber ranges and simulation platforms market.

By Application: Threat Intelligence Analysis Climbs the Agenda

Training and certification still command 45.8% of 2024 revenue, yet growth is increasingly fueled by threat intelligence analysis, forecast at 17.4% CAGR. Security teams now detonate advanced malware in isolated environments to profile TTPs and fine-tune detection signatures. The capability shortens response times when attacks eventually hit production networks.

Research and development users exploit ranges to test new security products under adversarial conditions, fast-tracking release cycles. Compliance applications convert exercise output into audit trails, proving policy effectiveness to boards and regulators. Together, the portfolio breadth cushions the cyber ranges and simulation platforms industry against spending volatility in any single segment.

Geography Analysis

North America generated 38.3% of 2024 revenue, anchored by generous federal budgets and stringent state-level regulations. The Department of Energy’s OTDefender fellowship funnels graduates into utilities, amplifying local demand for OT-focused ranges. Commercial adoption is further propelled by widespread cloud readiness, enabling rapid SaaS onboarding across mid-market firms. Canada and Mexico participate through cross-border grid-security programmes, though their share is modest relative to the United States.

Asia-Pacific is the fastest-growing theatre at 17.0% CAGR to 2030. Singapore’s Cyber Defence Test and Evaluation Centre offers federated access to academic, military, and private-sector teams. [4]Government of Singapore, “Cybersecurity and Digital Resilience,” gov.sg Japan’s CyberKONGO2025 exercise spans 17 nations and demonstrates regional appetite for coalition interoperability. Meanwhile, India and China channel national-security investments into sovereign ranges that reflect unique telecommunications stacks, underscoring localisation imperatives within the cyber ranges and simulation platforms market.

Europe maintains steady momentum under DORA compliance, joint cyber exercises, and national range build-outs. Germany and France prioritise defence applications, while the UK accelerates financial-sector drills. ECSO’s feature checklist fosters vendor comparison, nudging the market towards interoperability. Elsewhere, Middle East and Africa buyers emphasise energy and telecom protection, leveraging government-funded programmes in the Gulf and South Africa to jump-start local talent pipelines.

Competitive Landscape

The market remains moderately fragmented, with no single vendor exceeding one-fifth of global revenue. SimSpace, Cyberbit, and RangeForce compete on scenario realism, AI-driven threat engines, and SaaS ergonomics. Defence contractors such as Raytheon and Northrop Grumman leverage classified project past performance to secure government contracts that smaller pure-plays cannot access. Value propositions increasingly hinge on content breadth, analytics dashboards, and the ability to integrate with mainstream security platforms.

Platform consolidation is underway. Cymulate acquired CYNC Secure for USD 10 million in January 2025, expanding its exposure-management workflows and signalling a shift toward full-cycle validation suites. SimSpace secured USD 45 million in late-2024 funding to deepen enterprise-stack replication, including ERP, identity, and OT components. Vendors also broaden partner ecosystems: Cyberbit and Kite Distribution joined forces to penetrate European channel networks, bundling range subscriptions with MSSP services.

Artificial intelligence is the next battleground. Providers embed generative models that auto-mutate malware and generate adaptive phishing campaigns. Successful execution demands robust ethical controls to avoid dual-use risks, positioning vendors with mature governance frameworks ahead of pure technology plays. Looking forward, underserved niches—such as quantum-safe cryptography drills and medical-device cyber safety—represent expansion vectors for the cyber ranges and simulation platforms market.

Cyber Ranges And Simulation Platforms Industry Leaders

SimSpace Corporation

Cyberbit Ltd.

RangeForce Inc.

Immersive Labs Ltd.

Circadence Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: IT For teamed with CyberGym Japan to deliver cyber training to financial firms and municipalities.

- February 2025: GMO Cybersecurity by Ierae supported Japan’s CyberKONGO2025 multinational exercise.

- January 2025: Darktrace launched Darktrace/Cloud, applying self-learning AI to cloud threat detection.

- January 2025: Cymulate acquired CYNC Secure for USD 10 million, augmenting its range with asset-led exposure management.

- January 2025: Quorum Cyber entered the U.S. market by purchasing Kivu Consulting to add incident-response services.

Global Cyber Ranges And Simulation Platforms Market Report Scope

| Software |

| Services |

| Simulation Range |

| Emulation Range |

| Hybrid Range |

| Overlay Range |

| On-Premises |

| Cloud-Based |

| Hybrid |

| Defense and Security Agencies |

| BFSI |

| IT and Telecom |

| Healthcare |

| Industrial and Critical Infrastructure |

| Academic and Training Institutes |

| Other End-users |

| Training and Certification |

| Threat Intelligence and Analysis |

| Research and Development / Testing |

| Compliance and Assessment |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Range Type | Simulation Range | ||

| Emulation Range | |||

| Hybrid Range | |||

| Overlay Range | |||

| By Deployment Mode | On-Premises | ||

| Cloud-Based | |||

| Hybrid | |||

| By End-user | Defense and Security Agencies | ||

| BFSI | |||

| IT and Telecom | |||

| Healthcare | |||

| Industrial and Critical Infrastructure | |||

| Academic and Training Institutes | |||

| Other End-users | |||

| By Application | Training and Certification | ||

| Threat Intelligence and Analysis | |||

| Research and Development / Testing | |||

| Compliance and Assessment | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the cyber ranges and simulation platforms market in 2025?

It stands at USD 2.37 billion and is on track to reach USD 5.02 billion by 2030, reflecting a 16.2% CAGR over the forecast period.

Which user group spends the most on cyber ranges?

Defense and security agencies generate the highest revenue, holding 32.7% share in 2024 because mission rehearsal mandates realistic, classified environments.

Why are financial institutions accelerating adoption?

Regulations such as New York’s 23 NYCRR 500 and Europe’s DORA require evidence-based drills, pushing banks toward platforms that document incident-response readiness.

What deployment model is growing fastest?

Cloud-based delivery is expanding at 17.1% CAGR as enterprises favour pay-as-you-use economics and rapid provisioning over hardware ownership.

How do hybrid ranges add value?

They combine virtual networks with select physical devices to replicate latency, protocol quirks, and sensor feedback, allowing high-fidelity training without full-scale physical labs.

Which region is the quickest to grow?

Asia-Pacific is advancing at a 17.0% CAGR through 2030, driven by government-backed initiatives in Singapore, Japan, India, and China.

Page last updated on: