Immersive Simulator Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

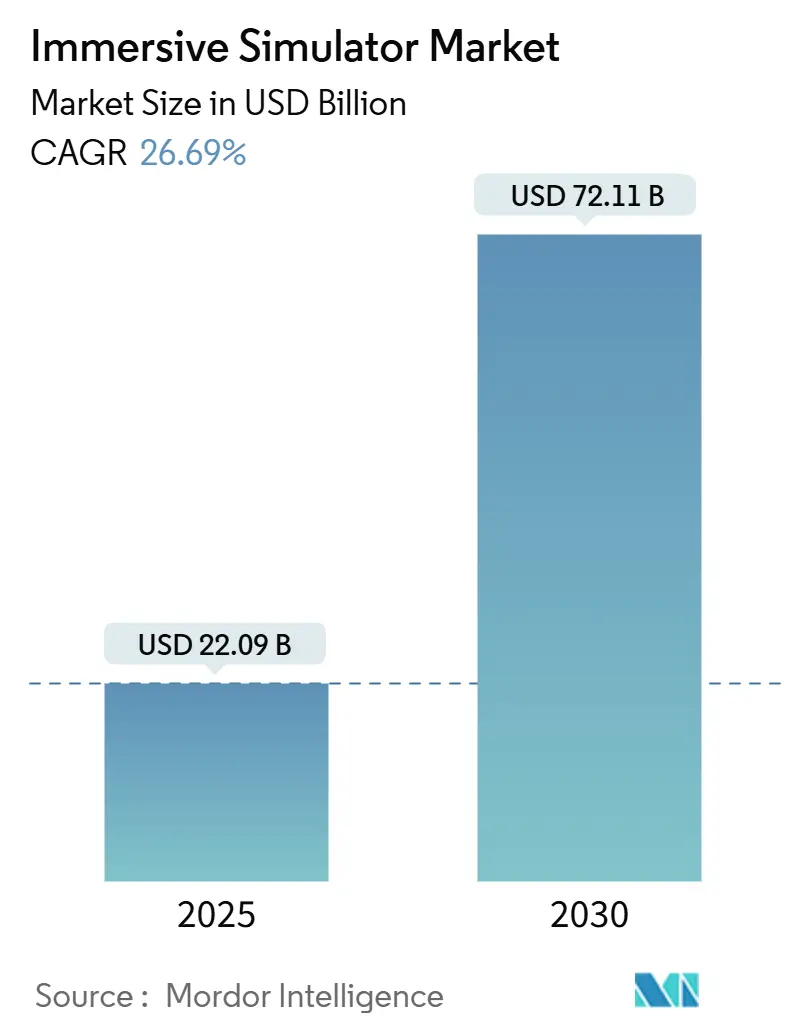

| Market Size (2025) | USD 22.09 Billion |

| Market Size (2030) | USD 72.11 Billion |

| Growth Rate (2025 - 2030) | 26.69% CAGR |

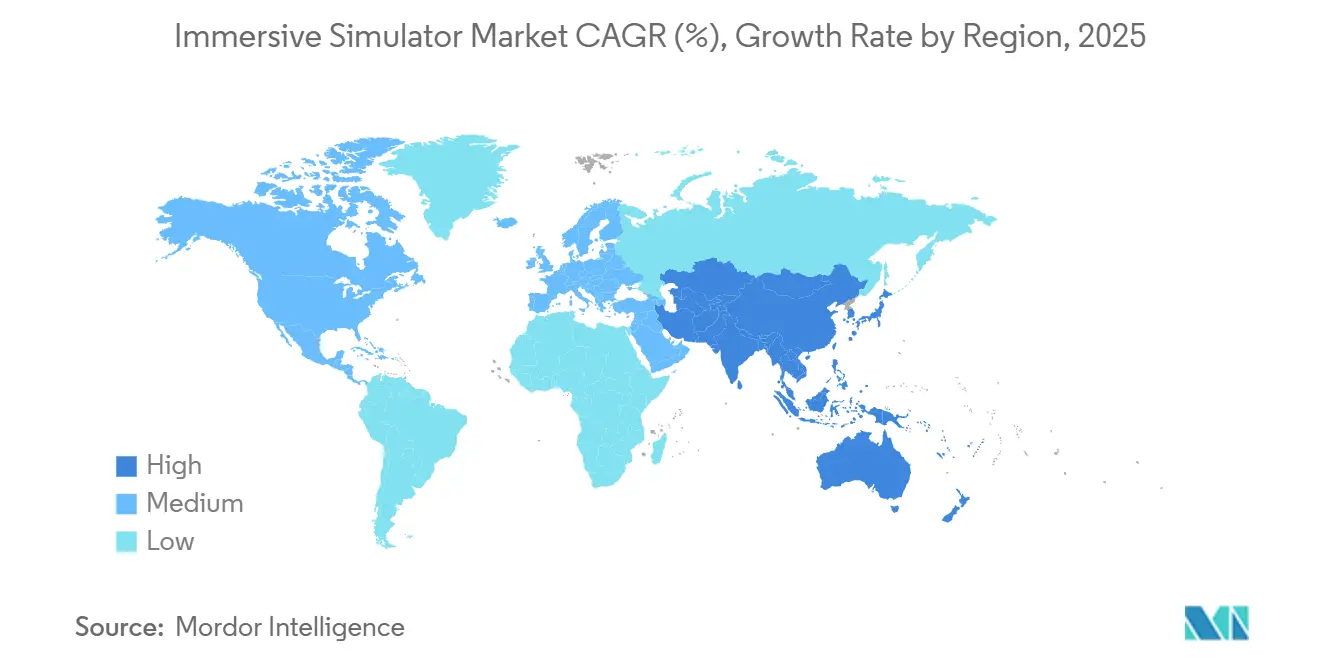

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Immersive Simulator Market Analysis by Mordor Intelligence

The Immersive Simulator market size stands at USD 22.09 billion in 2025 and is forecast to reach USD 72.11 billion by 2030, reflecting a 26.69% CAGR during the period. Robust demand for risk-free training in hazardous industries, falling headset prices, and enterprise digital-twin strategies underpin this expansion. Industrial operators report double-digit reductions in incident rates after adopting virtual reality (VR) safety programs, validating the technology’s return on safety investment. Hardware retains the greatest revenue share because organizations must first build reliable visualization and compute infrastructure, yet service-centric training-as-a-service models are compounding growth as firms outsource content creation and lifecycle support. Rising availability of 5G and edge computing is also shifting multi-user immersive experiences from pilot deployments to scaled rollouts, while regulatory agencies increasingly accept virtual environments as evidence of compliance, shortening qualification cycles and broadening addressable use cases. Competition remains moderate; industrial automation majors are integrating immersive functionality into existing portfolios even as niche XR specialists secure vertical-specific wins.

Key Report Takeaways

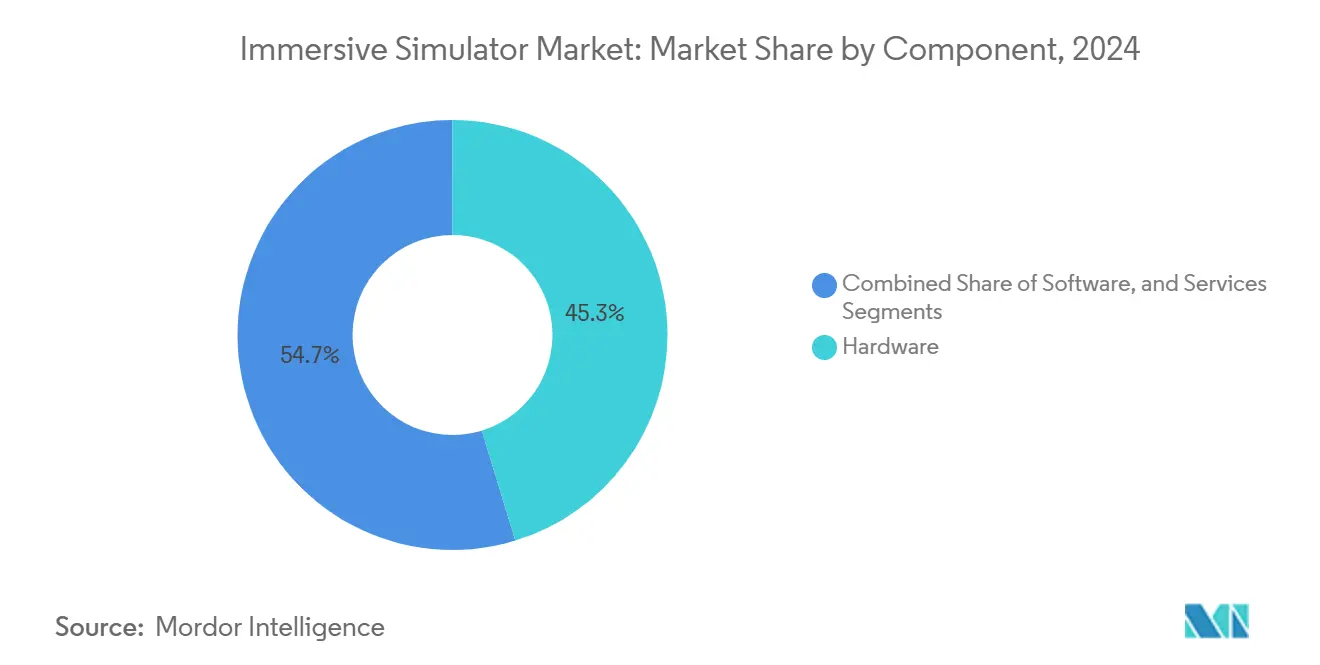

- By component, hardware led with 45.28% of Immersive Simulator market share in 2024; services are projected to expand at a 27.39% CAGR through 2030.

- By simulation technology, virtual reality captured 38.57% revenue share in 2024, while mixed reality is forecast to advance at a 26.97% CAGR to 2030.

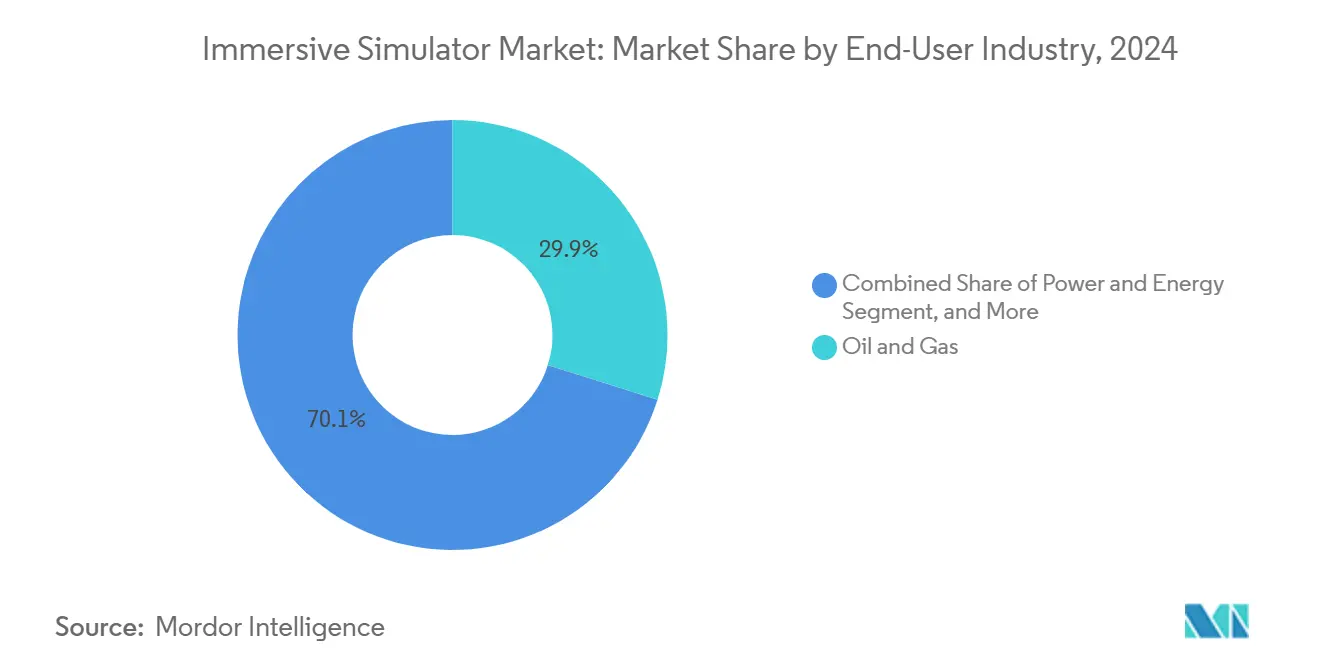

- By end-user industry, oil and gas accounted for 29.87% of the Immersive Simulator market size in 2024; pharmaceuticals and healthcare is poised for 26.73% CAGR growth to 2030.

- By application, training and education commanded 42.34% share of the Immersive Simulator market size in 2024 and safety and emergency management is progressing at a 27.19% CAGR through 2030.

- By geography, North America held 32.86% of the Immersive Simulator market share in 2024, while Asia-Pacific posts the fastest 27.11% CAGR to 2030.

Global Immersive Simulator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened safety-training mandates in hazardous industries | +4.2% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Growing availability of cost-effective VR hardware | +3.8% | Global, accelerated in Asia-Pacific markets | Short term (≤ 2 years) |

| Adoption of digital twins for process optimization | +3.5% | North America and EU industrial corridors | Long term (≥ 4 years) |

| Enterprise upskilling initiatives for Gen-AI-ready workforce | +3.1% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Edge-rendered multi-user simulation platforms | +2.7% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) |

| Government climate-risk drills using immersive tech | +2.4% | EU and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heightened Safety-Training Mandates

Occupational safety bodies now endorse VR modules as acceptable proof of competency, triggering a surge in immersive procurement for confined-space, explosion-risk, and high-voltage scenarios. Oil-and-gas operators adopting VR safety drills recorded 43% fewer injuries within one year. European refineries such as IPLOM validated higher learner confidence after virtual emergency rehearsals. Construction studies show statistically significant knowledge retention when fall-protection content is delivered immersively.[1]Ammar Alzarrad et al., “Introducing a Cutting-Edge VR Interactive System for Construction Safety,” Frontiers in Built Environment, frontiersin.org Regulatory acceptance expands the technology from optional pilot to essential compliance tool, compelling investment even during capital-expenditure freezes. The greatest impact centers on regions with stringent safety enforcement, notably the United States Occupational Safety and Health Administration (OSHA) and the European Agency for Safety and Health at Work.

Growing Availability of Cost-Effective VR Hardware

Average headset selling prices dropped below USD 700 in 2025, and enterprise bulk purchases secure discounts of up to 30%. Industrial buyers now access consumer-priced devices with 4K optics and inside-out tracking, narrowing the performance gap with premium tethered rigs. Suppliers such as Varjo launched cloud-rendered pipelines that shift graphical load to edge servers, extending hardware life cycles and lowering entry costs.[2]Varjo, “Varjo Reality Cloud,” varjo.com The pricing inflection unlocks adoption among small and medium manufacturers that previously deemed immersive initiatives unaffordable. Short refresh cycles further accelerate replacement and fleet expansion, magnifying unit shipments during the forecast window.

Adoption of Digital Twins for Process Optimization

Immersive simulators increasingly connect with high-fidelity digital twins to enable virtual commissioning and predictive maintenance. Semiconductor fabs integrating twin-based training achieved 25% logistics cost cuts and 50% transfer-time reductions. Certification bodies collaborated with software providers to approve digital-twin-driven testing in lieu of physical prototypes, trimming months off regulatory cycles and cementing virtual environments as part of mandatory design workflows. The convergence of sensor streams, AI analytics, and photorealistic graphics allows operators to rehearse rare fault conditions and optimize procedures before plant-floor execution, creating durable demand for simulation licenses and content refreshes.

Enterprise Upskilling for Gen-AI Workforce

Organizations deploying AI-enabled automation require employees capable of collaborating with virtual agents. Immersive experiential learning improves skill retention by 40% relative to classroom formats, according to longitudinal nursing-education research. U.S. defense agencies adopted VR behavioral-skills modules for leadership and mental-health interventions, demonstrating the medium’s versatility beyond technical tasks. Grant programs from solution vendors underwrite large-scale rollout in vocational institutions, expanding the talent pool trained in spatial-computing workflows. The emphasis on continuous reskilling sustains multi-year service contracts and recurring content-library revenues.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital expenditure | -2.8% | Global, particularly impacting SMEs | Short term (≤ 2 years) |

| Integration complexity with legacy control systems | -2.1% | North America and EU industrial regions | Medium term (2-4 years) |

| Content-authoring bottlenecks for domain-specific scenarios | -1.9% | Global, with concentration in specialized industries | Medium term (2-4 years) |

| Data-sovereignty concerns in cross-border cloud deployments | -1.6% | EU and Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure

Despite cheaper headsets, comprehensive deployments involve spatial cameras, work-station-grade GPUs, content-authoring tools, and facility retrofits. Subscription licensing for immersive authoring software can exceed USD 65 per user monthly, burdening organizations with significant operating outlays. Smaller firms struggle to quantify return on investment when disruptions, user on-boarding, and content iteration costs are included. Financial barriers restrict early adoption in emerging economies and slow penetration in low-margin industries, tempering overall market velocity.

Integration Complexity with Legacy Control Systems

Many industrial assets operate on proprietary protocols lacking real-time data exposure, complicating synchronization with simulators. Utilities attempting to link 1990-era distributed control systems with modern 3D engines face cybersecurity and latency hurdles. Emerson’s DeltaV Mimic Field 3D tackles some challenges by ingesting existing CAD and laser-scan files while maintaining protocol compatibility.[3]Emerson, “DeltaV Mimic Field 3D,” emerson.com Yet full read-write integration still demands bespoke engineering and multi-phase rollouts, elongating project timelines and delaying revenue realization for vendors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Infrastructure Underpins Adoption

Immersive Simulator market size for hardware reached USD 10.01 billion in 2025, equivalent to 45.28% of total value. Robust demand for head-mounted displays, motion platforms, and GPU-accelerated servers cements hardware’s leadership within the Immersive Simulator market. Standardization around open XR protocols is enlarging compatible device ecosystems, while edge-rendering pipelines reduce on-device compute requirements and enable lighter, cheaper headsets. Although hardware revenues grow at a mid-teens pace, services command the highest 27.39% CAGR as enterprises outsource content design, systems integration, and lifecycle management.

Service providers bundle curriculum development, analytics dashboards, and continuous updates, often via multiyear managed-service agreements that amortize upfront investment. The shift favors vendors with cross-disciplinary teams spanning instructional design and 3D modeling. Software platforms, meanwhile, are evolving toward drag-and-drop authoring that empowers in-house subject-matter experts, creating an upsell pathway from basic viewers to AI-powered adaptive-learning engines.

By Simulation Technology: Mixed Reality Accelerates

Virtual reality retained 38.57% Immersive Simulator market share in 2024, yet mixed-reality devices achieve the fastest 26.97% CAGR by blending digital instructions over physical assets. Automotive plants deploy head-mounted displays to overlay torque specifications onto engines, reducing rework and shortening training cycles. Augmented-reality glasses enable remote experts to annotate live worker viewpoints, slashing travel costs and downtime. Non-immersive 3D desktop simulators persist for theory-based learning where situational immersion is less critical, maintaining relevance in academia and cost-sensitive vocational centers.

Emerging 4D and 5D haptic rigs enrich training for high-consequence tasks such as robotic surgery, delivering tactile feedback that mimics tissue resistance. Northwestern University’s wearable force-feedback prototype illustrates near-term commercial potential for lightweight haptics that complement visual immersion. As AI inference moves to the edge, simulation engines dynamically adjust scenario difficulty, personalizing sessions and enhancing competency validation.

By End-User Industry: Healthcare Overtakes Traditional Leaders

Oil and gas preserved the single largest 29.87% slice of Immersive Simulator market share in 2024, leveraging virtual well-control and refinery turn-around simulations to minimize downtime and accidents. Nonetheless, pharmaceuticals and broader healthcare settings register a 26.73% CAGR on rising adoption for surgical rehearsal, nursing education, and patient engagement. U.S. regulators cleared multiple VR tools for cardiology, legitimizing immersive modalities for clinical use and hastening hospital procurement cycles.

Aerospace and defense remain early adopters, pairing high-fidelity visuals with physics-based flight dynamics. NASA’s mixed-reality cockpit research reports lower motion-sickness scores than legacy panoramic screens, signaling a generational shift in simulator design. Manufacturing deployments are proliferating through welding, painting, and assembly lines as companies chase quality gains and faster onboarding. Transportation, logistics, mining, and chemicals round out adoption landscapes where hazardous conditions or complex workflows justify advanced simulation budgets.

By Application: Safety and Emergency Management Outpaces Base-Training

Training and education currently represent 42.34% of Immersive Simulator market size, covering everything from basic equipment orientation to soft-skill coaching. Yet safety and emergency management scenarios exhibit the steepest 27.19% CAGR as corporate boards prioritize zero-harm mandates. Companies report 43% injury-rate reductions post-VR adoption, bolstering budget justification. Public-sector agencies procure immersive incident command modules to rehearse mass-casualty and climate-risk events without field mobilization, broadening opportunity beyond private industry.

Process optimization and design simulations integrate real-time plant data with gaming-engine visualization to debug layouts before steel is cut. Maintenance and repair overlays step-by-step guides onto equipment, enabling junior technicians to achieve expert-level accuracy and freeing senior staff for higher-value tasks. Across applications, analytics dashboards quantify dwell time, error frequency, and knowledge checks, feeding continuous-improvement loops that cement recurring software and service revenues.

Geography Analysis

North America accounted for 32.86% Immersive Simulator market share in 2024 thanks to early Department of Defense and energy-sector investments. The U.S. Army’s Synthetic Training Environment uses high-resolution terrain data to build earth-scale virtual drills, anchoring a robust domestic supplier base. OSHA’s evolving guidelines around crystalline silica exposure, meanwhile, increase employer demand for compliant virtual modules.

Asia-Pacific clocks the fastest 27.11% CAGR as governments embed XR into digital-industrial blueprints. Chinese ministries funded VR driver, aviation, and disaster-response simulators across more than a dozen provinces, while Indian manufacturing clusters pilot headset-based upskilling to mitigate skilled-labor shortages. High smartphone penetration and local headset OEMs compress costs, accelerating enterprise proof-of-concept conversions.

Europe shows steady uptake driven by industrial safety directives and sustainability imperatives; Siemens and BASF lead factory-of-the-future initiatives that weave immersive simulation into daily operations. The Middle East’s hydrocarbon sector deploys well-intervention simulators to train expatriate workforces, and African mining firms use AR for remote maintenance support. South American adoption concentrates in Chilean and Brazilian mines, where remote sites necessitate virtual training to reduce travel constraints.

Competitive Landscape

Established automation vendors including Siemens, Honeywell, and ABB are embedding immersive functionality into supervisory control, manufacturing-execution, and digital-twin stacks, leveraging installed customer bases to cross-sell simulation modules. Siemens’ USD 10.6 billion Altair acquisition adds multiphysics engines and AI generative design, tightening integration between engineering and immersive runtime. Honeywell’s purchase of Com Dev strengthens satellite-communications hardware and positions the firm to extend XR training to space-operations contexts.

Specialist vendors such as CAE, EON Reality, Varjo, and VirtaMed differentiate through vertical focus whether pilot training, factory onboarding, or medical procedure rehearsal. EON Reality’s conversational-XR platform couples generative AI with spatial learning, offering adaptive guidance that adjusts to learner responses. Hardware makers pursue photorealistic optics, hand-tracking, and cloud-rendering pipelines to raise immersion fidelity while reducing client-side compute investment.

Market entry barriers center on proprietary content libraries, regulatory certifications, and integration expertise. Partnerships therefore dominate strategic activity: equipment OEMs align with XR software firms to package turnkey offerings, and cloud providers court simulator companies to drive edge consumption. Competitive intensity remains moderate with the five largest players controlling roughly 45% of revenue, leaving room for regional and niche entrants.

Immersive Simulator Industry Leaders

AVEVA Group plc

Honeywell International Inc.

Siemens AG

ABB Ltd.

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Honeywell acquired Com Dev International for CAD 455 million (USD 345 million), expanding connectivity components for satellite-based simulation services.

- June 2025: EON Reality launched a global freemium XR education platform, widening access to immersive learning content beyond enterprise clients.

- May 2025: Siemens unveiled AI agents for industrial automation, enabling autonomous process execution and linking agents to immersive operator training modules.

- March 2025: ABB completed the acquisition of Siemens’ wiring-accessories business in China, enhancing building-automation portfolios that integrate AR work-instructions.

Global Immersive Simulator Market Report Scope

| Hardware |

| Software |

| Services |

| Virtual Reality (VR) |

| Augmented Reality (AR) |

| Mixed Reality (MR) |

| 3D Non-immersive Simulation |

| 4D/5D and Haptic-enabled Simulation |

| Oil and Gas |

| Power and Energy |

| Chemicals |

| Metals and Mining |

| Pharmaceuticals and Healthcare |

| Aerospace and Defence |

| Transportation and Logistics |

| Manufacturing |

| Other End-User Industry |

| Training and Education |

| Safety and Emergency Management |

| Maintenance and Repair |

| Process Optimisation and Design |

| Other Application |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Simulation Technology | Virtual Reality (VR) | ||

| Augmented Reality (AR) | |||

| Mixed Reality (MR) | |||

| 3D Non-immersive Simulation | |||

| 4D/5D and Haptic-enabled Simulation | |||

| By End-User Industry | Oil and Gas | ||

| Power and Energy | |||

| Chemicals | |||

| Metals and Mining | |||

| Pharmaceuticals and Healthcare | |||

| Aerospace and Defence | |||

| Transportation and Logistics | |||

| Manufacturing | |||

| Other End-User Industry | |||

| By Application | Training and Education | ||

| Safety and Emergency Management | |||

| Maintenance and Repair | |||

| Process Optimisation and Design | |||

| Other Application | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the Immersive Simulator market in 2025?

The Immersive Simulator market size is USD 22.09 billion in 2025.

What CAGR is expected for Immersive Simulator revenues through 2030?

Revenues are projected to grow at a 26.69% CAGR between 2025 and 2030.

Which component segment grows fastest?

Services record the highest 27.39% CAGR as organizations outsource content and lifecycle support.

Which region leads in current revenue?

North America contributes 32.86% of 2024 revenue owing to strict safety regulations and defense spending.

Why are mixed-reality simulators gaining momentum?

Mixed reality overlays digital guidance onto physical assets, producing the fastest 26.97% CAGR by combining immersive learning with real-world task execution.

What holds back wider adoption?

High upfront capital expenditure and integration challenges with legacy control systems remain the primary restraints.

Page last updated on: