Online Simulation Games Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

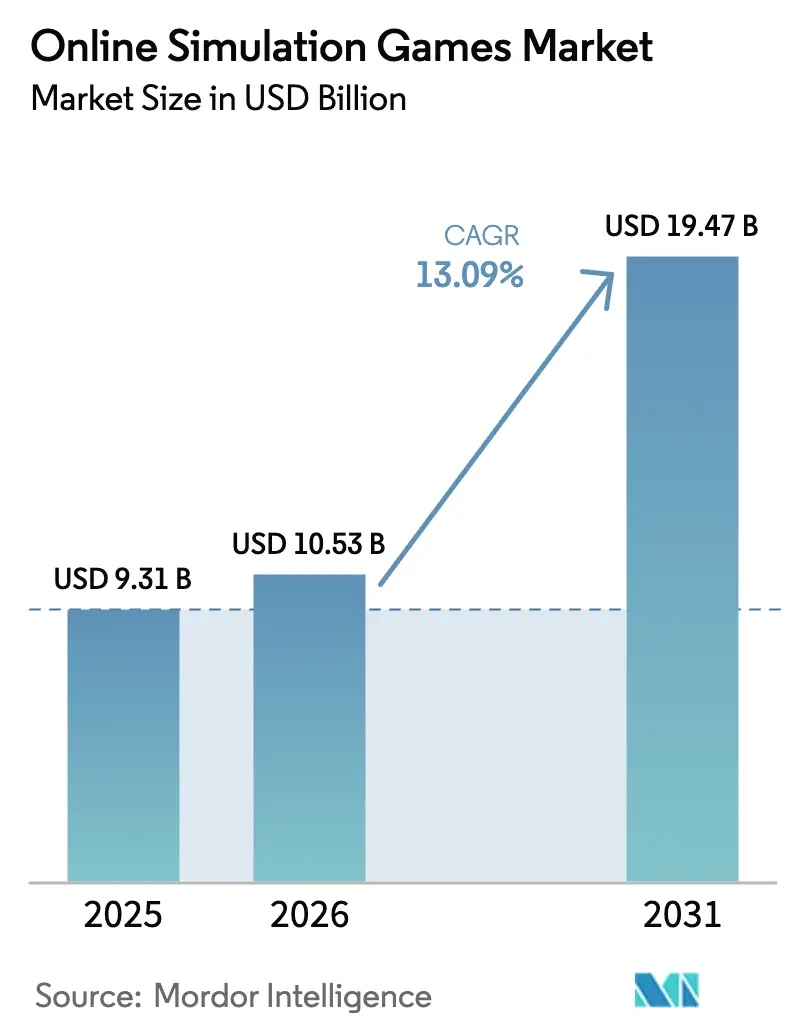

| Market Size (2026) | USD 10.53 Billion |

| Market Size (2031) | USD 19.47 Billion |

| Growth Rate (2026 - 2031) | 13.09% CAGR |

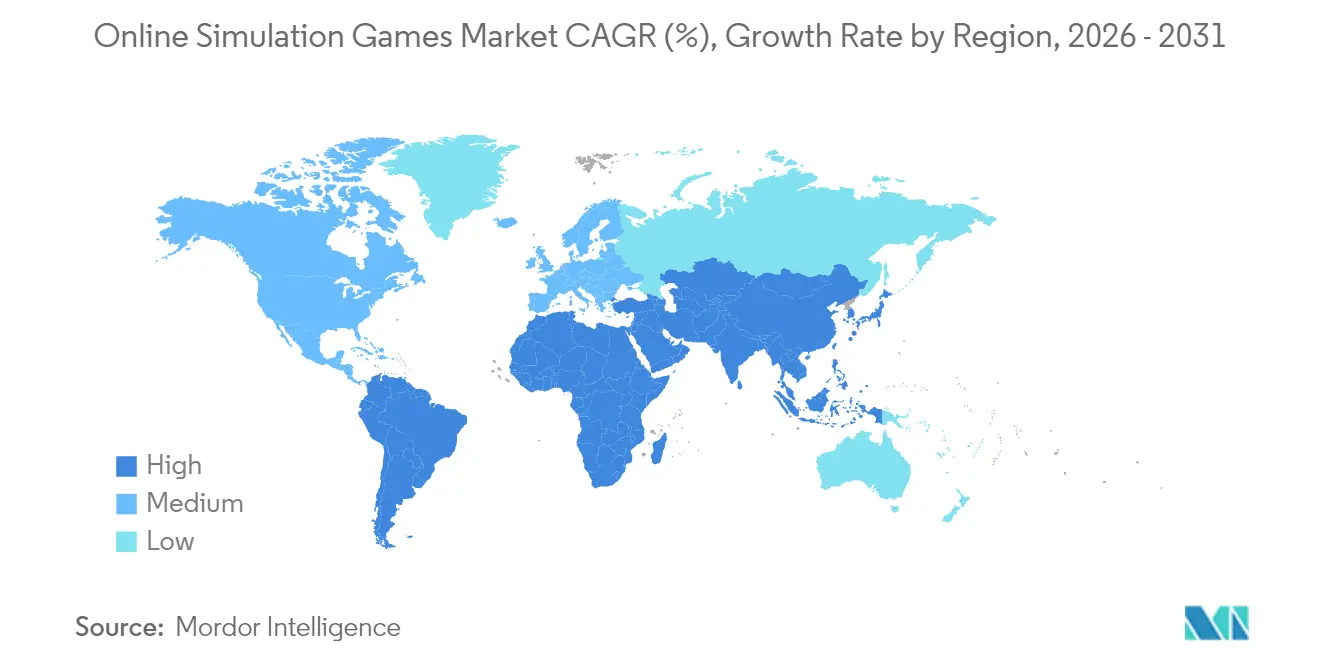

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Online Simulation Games Market Analysis by Mordor Intelligence

The online simulation games market size in 2026 is estimated at USD 10.53 billion, growing from 2025 value of USD 9.31 billion with 2031 projections showing USD 19.47 billion, growing at 13.09% CAGR over 2026-2031. Robust spending on photorealistic physics engines, growing cross-platform adoption, and the convergence of entertainment with professional training keep the growth curve steep. Advanced cloud infrastructure is reducing latency and hardware barriers, widening the user pool from dedicated PC players to casual mobile segments. Publisher consolidation, led by Microsoft’s post-Activision strategy, is concentrating intellectual property and talent pools, even as it extends smaller studios’ reach into premium distribution networks. Meanwhile, generative AI is reshaping design pipelines; 62% of studios already use it to generate worlds and assets, compressing development timelines and costs. Regulatory headwinds around loot boxes in Europe are prompting a pivot toward subscriptions and hybrid revenue models that can better withstand compliance scrutiny.

Key Report Takeaways

- By platform, Mobile captured 59.40% of the online simulation games market in 2025; VR/AR devices post the fastest growth at a 19.45% CAGR to 2031.

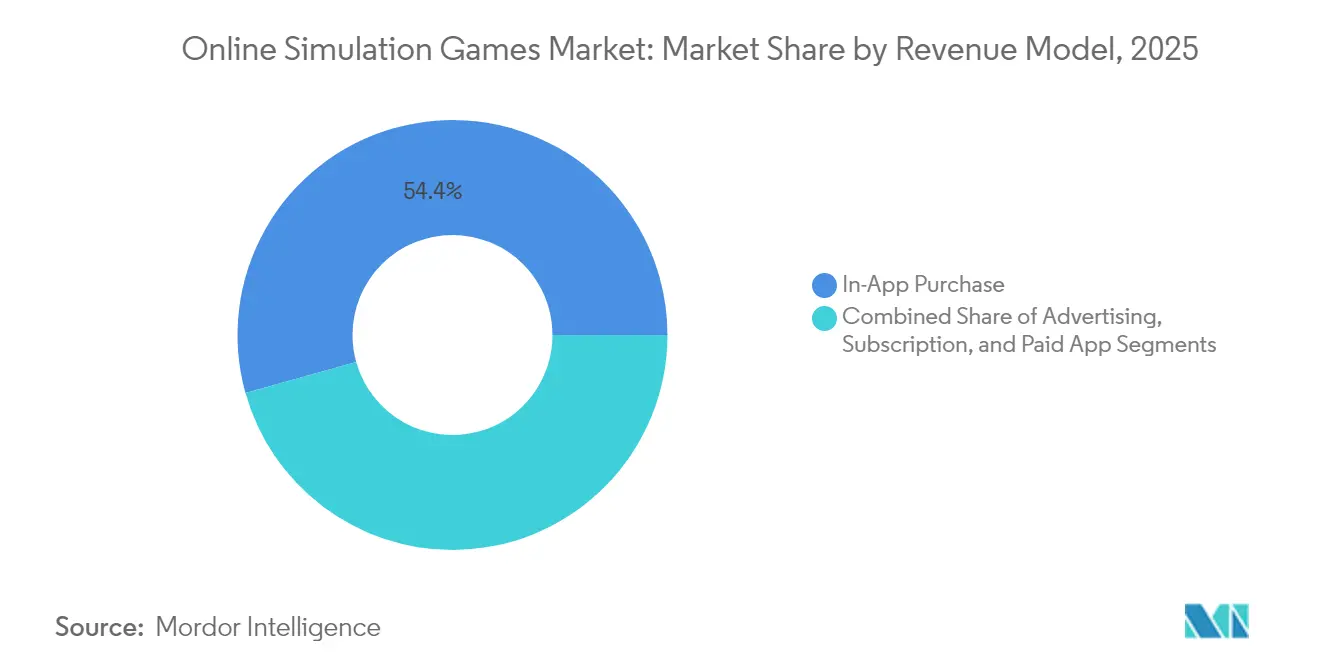

- By revenue model, In-App Purchases held 54.35% share of the online simulation games market size in 2025, while subscriptions are advancing at a 15.55% CAGR between 2026-2031.

- By game type, Life Simulation commanded 34.60% share of the online simulation games market in 2025; Training & Education simulations are set to grow at an 17.62% CAGR to 2031.

- By geography, Asia-Pacific led with 44.70% of online simulation games market share in 2025, while the Middle East & Africa region is projected to expand at an 17.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Online Simulation Games Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in mobile-first gaming uptake across emerging Asian markets | +3.2% | Asia-Pacific; spillover to Middle East & Africa | Medium term (2-4 years) |

| Growth of cloud gaming infrastructure enabling low-latency simulations in North America | +2.5% | North America; Europe | Medium term (2-4 years) |

| Integration of generative AI for real-time world-building boosting player engagement | +2.8% | Global; early adoption in North America & Europe | Short term (≤ 2 years) |

| Expansion of esports broadcasting rights for simulation titles in Europe | +1.9% | Europe; North America; East Asia | Medium term (2-4 years) |

| Government-backed digital economy initiatives fueling indie simulation studios in South America | +1.5% | South America (Brazil, Argentina, Chile) | Long term (≥ 4 years) |

| Increasing adoption of VR flight & driving simulators for training in the Middle East | +1.8% | Middle East; North Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise in Mobile-First Gaming Uptake across Emerging Asian Markets

Mobile downloads touched 4.2 billion in Southeast Asia during H1 2024, with Indonesia alone contributing 41%.[1]Z.com Engagement Team, “Let’s Survey the Usage Trends of Mobile Games in Asia,” engagement.z.com Spending willingness now exceeds 60% across Indonesia, Malaysia, and Thailand, motivating publishers to localize content and lean on culturally resonant food- and sports-themed simulations. Expanding 5G coverage is unlocking complex physics previously limited to PCs, reinforcing the online simulation games market’s mobile dominance in the region. Studios exploiting these conditions gain rapid scale without high upfront console or PC marketing costs.

Growth of Cloud Gaming Infrastructure Enabling Low-Latency Simulations in North America

Edge-based architectures such as AccelByte’s Multiplayer Servers integrated with Microsoft Azure now offer diverse virtual-machine families tuned for simulation workloads.[2]Thomas Burelli et al., “It’s Official: The Olympic Esports Games Will Be Held in 2025,” The Conversation, theconversation.com CableLabs’ Low Latency DOCSIS further trims lag, letting bandwidth-heavy flight or city-building simulations run flawlessly over ordinary connections. By abstracting performance away from end-user hardware, developers unlock new regions where high-spec GPUs remain scarce, broadening the online simulation games market addressable base.

Integration of Generative AI for Real-Time World-Building Boosting Player Engagement

Krafton’s inZOI launched in March 2025 with AI-driven non-player characters and tools that convert 2D images into playable 3D assets, selling 1 million copies in its first week. Players now expect emergent stories instead of predefined quests, pushing designers to supply infinite variables. Production pipelines that once required months of manual asset creation now complete tasks in days, accelerating updates that keep the online simulation games market cycling fresh content. AI also localizes dialogue on demand, shrinking time-to-enter for new territories and fueling retention metrics that justify subscription pricing.

Expansion of esports broadcasting rights for simulation titles in Europe

European media contracts for simulation esports gain value as viewership grows alongside a regional esports sector projected to exceed USD 1 billion in 2025.[3]AccelByte Engineering, “VM Provider for Game Server Management,” accelbyte.io The Olympic Esports Games, debuting in Saudi Arabia, place flight, farming, and motorsport simulators on a global stage. Broadcast exposure recruits new players who identify with real-world sports yet seek interactive control. Publishers monetize through sponsorship overlays and tournament passes, diversifying the online simulation games market away from dependence on microtransactions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High GPU demand outpacing supply, inflating hardware costs for PC simulations | -1.7% | North America, Europe | Short term (≤ 2 years) |

| Stringent loot-box regulations in Europe curtailing monetization options | -1.2% | Europe, spillover to North America | Medium term (2-4 years) |

| Bandwidth limitations in rural Africa hindering real-time multiplayer experiences | -0.8% | Select African & South American rural areas | Long term (≥ 4 years) |

| Rising development costs for photorealistic physics engines | -1.5% | Global independent studios | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High GPU demand outpacing supply, inflating hardware costs for PC simulations

Nvidia’s 86% share in discrete gaming GPUs gives shortages direct influence on retail prices.[4]Charlie Peng, “Nvidia Corporation: PC Gaming Industry Strategic Audit,” digitalcommons.unl.edu Consumers postpone upgrades, shrinking the premium PC slice of the online simulation games market size. Developers downscale texture packs or add cloud-rendered modes that shift compute to data centers. While streaming bridges the gap, it diverts spending toward platform fees and leaves razor-thin margins for titles reliant on fixed hardware sales.

Stringent loot-box regulations in Europe curtailing monetization options

The European Commission’s 2025 enforcement action against youth-targeted in-game sales adds disclosure rules and age ratings. Belgium’s prohibition already set precedent; Germany now flags titles containing loot boxes at point of sale. Studios redesign reward loops into transparent probability tables or switch to season passes. Diversification protects revenue but prolongs user acquisition costs, placing pressure on smaller developers and tightening liquidity in the online simulation games industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Revenue Model: Subscription momentum reshapes spending patterns

In-app purchases delivered 54.35% of 2025 revenue, reflecting their low entry barrier and impulse-driven psychology. The online simulation games market size for subscriptions is forecast to expand at a 15.55% CAGR from 2026-2031 as studios value predictable cash flow. Loot-box regulation accelerates that migration, and hybrid structures emerge where optional microtransactions supplement monthly passes. Advertising spend in simulation titles increased 26.7% year over year, fueled by rewarded-video formats that maintain engagement without paywalls. Paid download models persist among niche aircraft or industrial simulators that serve professional communities willing to invest upfront.

Higher annual retention correlates with subscription bundles that include exclusive expansion packs and cross-platform cloud saves. Loyalty metrics demonstrate that users enrolled longer than twelve months average 42% more playtime, evidence that predictable updates secure mindshare. As telecom operators bundle game subscriptions into data plans, the online simulation games market broadens into demographics previously price sensitive.

By Platform: VR/AR immersion challenges mobile supremacy

Mobile owns 59.40% of current volume due to widespread smartphone penetration and app-store convenience. Yet headset prices dipped below USD 400 in 2025, pushing VR/AR sales forward at a 19.45% CAGR. Smaller form factors and inside-out tracking lower motion sickness rates, attracting casual audiences to driving and flight simulators. Cloud streaming extends console-grade visuals to Chromebooks and smart TVs, merging platform boundaries.

PC retains loyal modding communities that extend life cycles for city-building and farming titles, preserving a lucrative, if niche, corner of the online simulation games market. Consoles supply standardized hardware targets, simplifying optimisation and assuring stable frame rates. Cross-play participation grew 40% in 2024 as studios commit to universal matchmaking pools, reducing fragmentation and maximizing reach.

By Game Type: Training & Education surges as enterprises adopt gamified learning

Life Simulation titles held 34.60% of revenue in 2025, spanning social sandboxes where player-generated content drives virality. Corporate interest pushes Training & Education simulation forward at an 17.62% CAGR. Aviation academies integrate extended-reality flight modules that regulators accept as loggable hours, cutting operational costs. Medical schools employ patient-diagnosis scenarios to practice rare conditions without clinical risk.

Vehicle Simulation advances with physics that approximate real telemetry to within single-digit variance, earning endorsements from professional bodies. Construction & Management simulators migrate into classroom lesson plans, fostering strategic thinking in engineering curricula. Sports Simulation retains a steady fan base, amplified by esports leagues that sync game patches with real-season calendars, keeping athletes and viewers aligned.

Geography Analysis

Asia-Pacific contributes the largest slice of the online simulation games market, holding 44.70% of 2025 revenue. China, Japan, and South Korea supply high-ARPU users, while Indonesia, Thailand, and Malaysia drive install volumes after mobile downloads reached 4.2 billion in early 2024. Local publishers adopt language packs and culturally themed assets to extend average session length and in-app purchase depth.

The Middle East & Africa region charts the fastest trajectory with an expected 17.62% CAGR to 2031, propelled by sovereign investment funds allocating capital to gaming accelerators and esports arenas. The National Gaming & Esports Strategy in Saudi Arabia outlines job-creation and studio-incubation targets that integrate simulation IP into tourism and education initiatives. Infrastructure rollouts of fiber and 5G networks shrink latency, aligning region-wide with global competitive standards for online titles.

North America maintains technical leadership in cloud delivery and AI tooling, recording USD 2 billion in mobile simulation revenue in April 2025. Europe sets monetization norms, with consumer-protection directives influencing global design choices. South America leverages Brazil’s Law 14.852 to grant gaming cultural status, fostering public grants and tax incentives for developers. Rural bandwidth gaps persist, so studios embed offline progression to ensure accessibility, keeping growth steady across diverse economic tiers in the online simulation games market.

Competitive Landscape

The landscape is moderately fragmented. Electronic Arts, Take-Two Interactive, and Microsoft together hold roughly 45% of publisher revenue, yet none exceed a quarter of the total. Microsoft signals ongoing acquisition ambitions to broaden its mobile and geographic footprint. Independent studios leverage cloud services and generative AI to deliver AAA-quality assets with lean teams, fostering innovation that compels incumbents to iterate faster.

Training & Education simulations invite aerospace and healthcare partners into co-development agreements, blending entertainment and vocational outcomes. Proprietary engines become strategic hedges, insulating studios from middleware licensing fees but demanding steep R&D budgets. Cross-play titles logged a 10% revenue upswing in 2023 and project another 7% in 2024, incentivizing publishers to abandon platform exclusivity and nurture holistic ecosystems inside the online simulation games market.

Investment flows also reach peripheral sectors such as haptic hardware and cloud-rendering start-ups that reduce time-to-launch. Competitive differentiation now focuses on content cadence, user-generated tools, and ecosystem services rather than single-purchase releases, reaffirming the online simulation games industry’s shift toward ongoing engagement metrics.

Online Simulation Games Industry Leaders

Sony Interactive Entertainment Inc.

Tencent

Nintendo

Microsoft

NetEase, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Krafton released AI-driven inZOI, reaching 1 million unit sales in its launch week and showcasing real-time asset-generation pipelines.

- April 2025: The European Commission advanced enforcement against child-targeted in-game monetization, compelling design revisions before regional launches.

- March 2025: EU regulators issued seven principles for in-game virtual currencies, establishing transparency baselines affecting simulation economies.

- February 2025: he International Olympic Committee confirmed the Olympic Esports Games, opening long-term exposure for simulation titles to mainstream audiences.

- January 2025: GIANTS Software launched Farming Simulator 25, selling 2 million copies within a week and outlining expansion roadmaps with fresh vehicles and seasons.

Global Online Simulation Games Market Report Scope

Online simulation games are video games that allow players to simulate and engage in various real-world or fictional activities, scenarios, or experiences within an online multiplayer environment. These games are often played on various platforms, including PC, console, mobile devices, and even in virtual reality environments.

The online simulation games market is segmented by type (advertising, in-app purchase, and paid app) and geography (North America, Europe, Asia Pacific, Middle East and Africa, and the Rest of the World). The market sizes and forecasts are provided in value (USD) for all the above segments.

| Advertising |

| In-App Purchase |

| Subscription |

| Paid App |

| Mobile |

| PC |

| Console |

| VR/AR Devices |

| Life Simulation |

| Vehicle Simulation |

| Construction and Management Simulation |

| Sports Simulation |

| Training and Education Simulation |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Revenue Model | Advertising | |

| In-App Purchase | ||

| Subscription | ||

| Paid App | ||

| By Platform | Mobile | |

| PC | ||

| Console | ||

| VR/AR Devices | ||

| By Game Type | Life Simulation | |

| Vehicle Simulation | ||

| Construction and Management Simulation | ||

| Sports Simulation | ||

| Training and Education Simulation | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the online simulation games market?

The online simulation games market is worth USD 10.53 billion in 2026 and is projected to reach USD 19.47 billion by 2031.

Which region leads the online simulation games market?

Asia-Pacific leads with 44.70% market share in 2025, driven by high smartphone use and culturally tailored mobile content.

Which platform segment is growing fastest?

VR/AR devices represent the fastest-growing platform, expanding at a 19.45% CAGR from 2026-2031.

How are European regulations affecting monetization?

Stringent loot-box rules are pushing developers toward subscriptions and cosmetic-only passes to ensure compliance and revenue stability.

Why is generative AI important for simulation games?

Generative AI enables real-time world-building and autonomous NPC behavior, improving engagement and reducing development time, as seen with Krafton’s inZOI.

What is driving growth in the Training & Education simulation segment?

Corporate, aviation, and healthcare sectors are adopting gamified simulation for skill development, propelling an 17.62% CAGR through 2031.

Page last updated on: