Electromagnetic Simulation Software Market Size and Share

Market Overview

| Study Period | 2023 - 2031 |

|---|---|

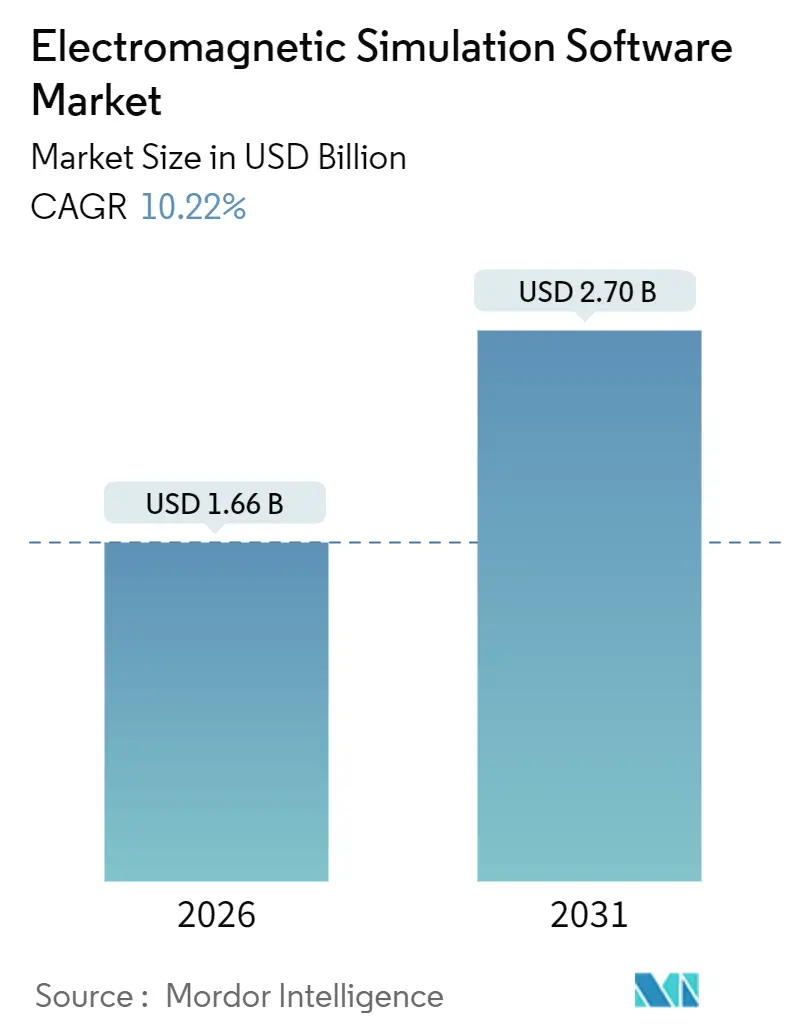

| Market Size (2026) | USD 1.66 Billion |

| Market Size (2031) | USD 2.70 Billion |

| Growth Rate (2026 - 2031) | 10.22% CAGR |

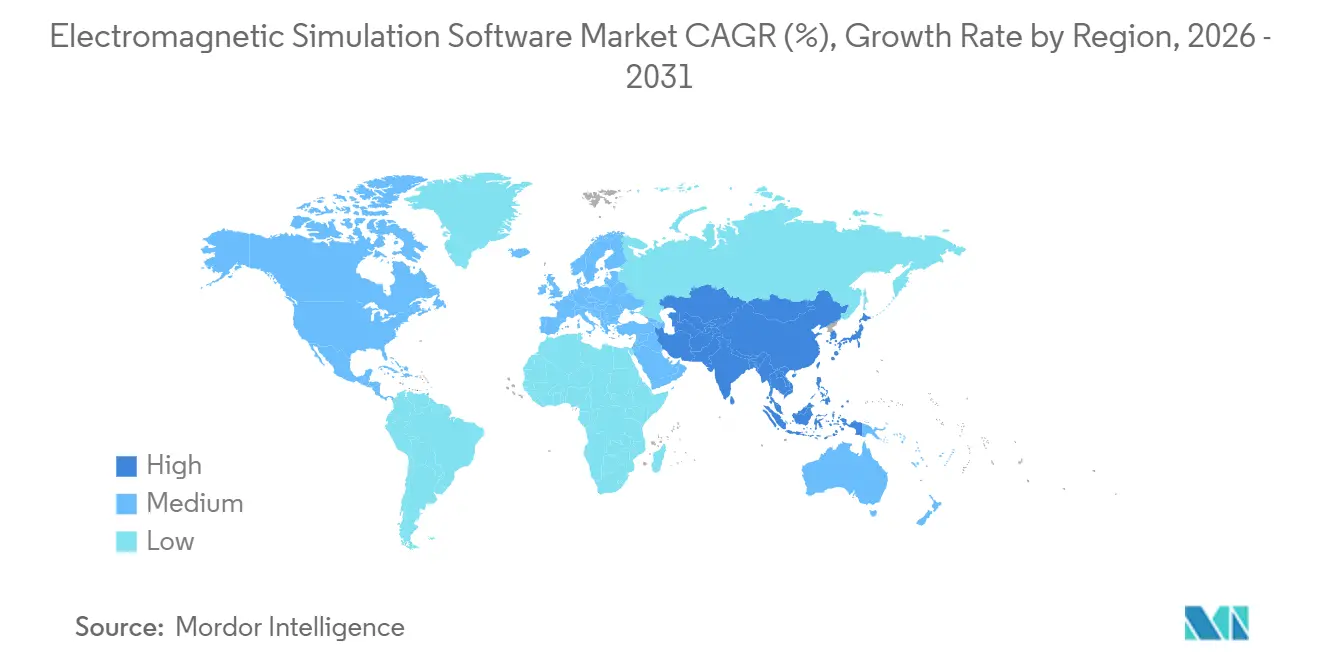

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electromagnetic Simulation Software Market Analysis by Mordor Intelligence

The electromagnetic simulation software market size reached USD 1.66 billion in 2026 and is projected to advance to USD 2.70 billion by 2031, reflecting a robust 10.22% CAGR during 2026-2031. This momentum is fueled by millimeter-wave 5G and early 6G testbeds that demand sub-wavelength antenna optimization, hybrid-cloud deployments that shift capital spending from hardware to elastic compute, and AI-driven surrogate models that shorten multi-day solver runs to hours. Telecommunications equipment suppliers, automotive radar developers, and defense contractors are the earliest beneficiaries, while mid-sized manufacturers adopt subscription pricing to avoid large perpetual-license outlays. Vendor consolidation is reshaping competitive dynamics following Synopsys’ acquisition of Ansys, and cloud partnerships with Amazon Web Services and Microsoft Azure lower entry barriers for start-ups. Automotive original equipment manufacturers (OEMs) are accelerating simulation adoption as 77 GHz and 79 GHz imaging radar modules migrate from premium to mid-range vehicle platforms, and compliance regimes such as CISPR 25 and ISO 11452 heighten the need for virtual electromagnetic interference validation.

Key Report Takeaways

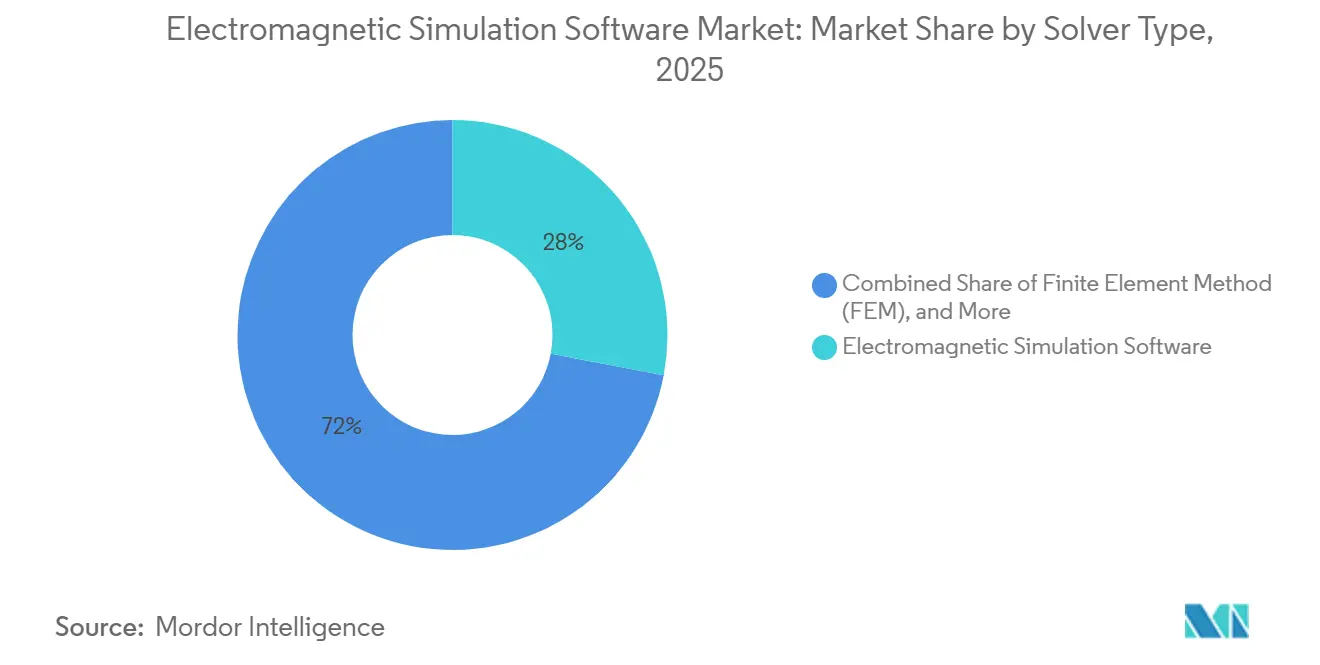

- By solver type, finite element method tools led with 28% revenue share in 2025 while finite difference time domain is advancing at a 13.5% CAGR through 2031.

- By deployment model, on-premise licensing accounted for 58% of 2025 revenue whereas cloud-based platforms are expanding at a 16.5% CAGR to 2031.

- By application, antenna design and analysis contributed 26% of 2025 revenue, but automotive radar simulation is escalating at a 16.0% CAGR through 2031.

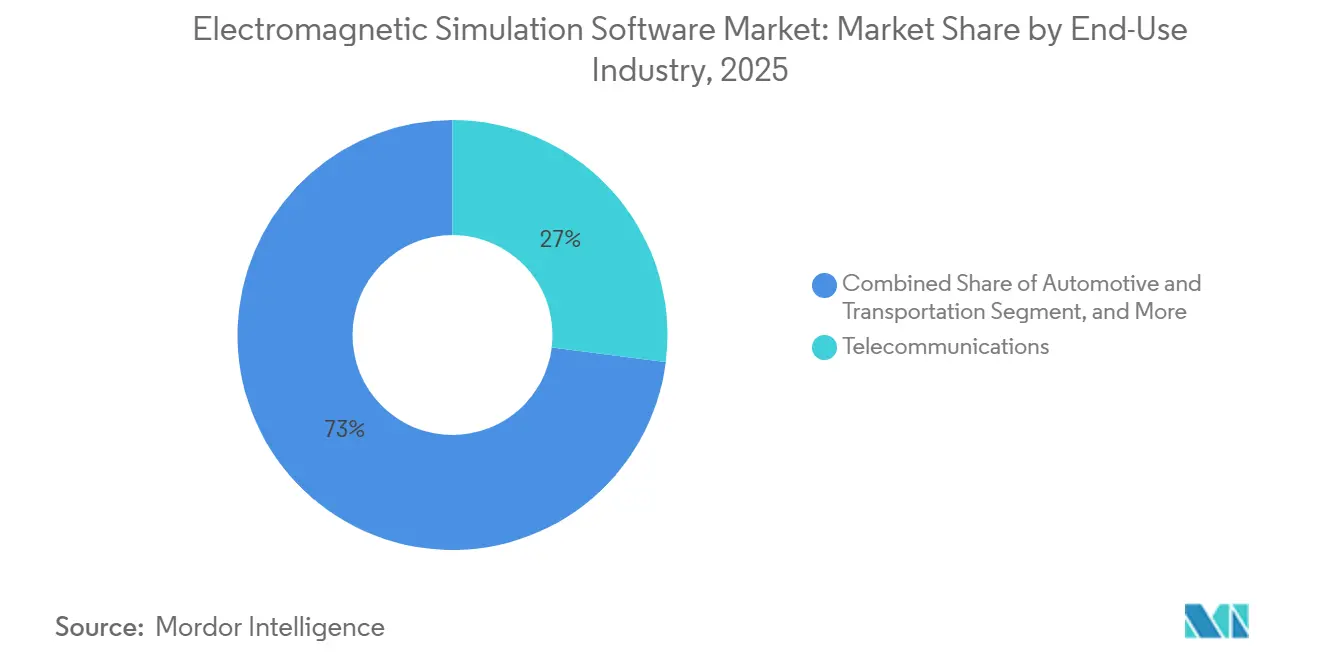

- By end-use, telecommunications commanded 27% revenue share in 2025, and automotive and transportation is growing fastest at a 14.5% CAGR to 2031.

- By frequency, microwave bands (3-30 GHz) held 36% usage in 2025, yet millimeter wave (30-300 GHz) is expanding at a 17.5% CAGR through 2031.

- By geography, North America captured 36% of 2025 revenue, while Asia-Pacific is projected to increase at a 12.8% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electromagnetic Simulation Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of 5G/6G infrastructure demanding advanced antenna and RF design tools | +2.8% | Global, led by North America, China, Japan, South Korea | Medium term (2-4 years) |

| Shift toward cloud-based simulation platforms for collaborative engineering workflows | +2.3% | North America and Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Increasing use of AI-powered surrogate models to accelerate design cycles | +1.9% | Global, centered in Taiwan, South Korea, United States | Medium term (2-4 years) |

| Growing adoption of automotive radar and ADAS sensors in electric and autonomous vehicles | +2.1% | Asia-Pacific, Europe, North America | Long term (≥ 4 years) |

| Rising stringency of global EMI/EMC regulations across industries | +1.4% | Global, strong enforcement in European Union and North America | Long term (≥ 4 years) |

| Deployment of digital twins for real-time system health and predictive maintenance | +1.2% | North America, Europe, Middle East and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of 5G/6G Infrastructure Demanding Advanced Antenna and RF Design Tools

Operators activated more than 1.5 million 5G base stations during 2025, and the migration from sub-6 GHz macro cells to millimeter-wave small cells exposes electromagnetic phenomena that older ray-tracing software cannot handle at the required accuracy. Full-wave solvers model mutual coupling, scan impedance drift, and grating-lobe suppression across large phased arrays, prompting telecom equipment vendors to invest in hybrid finite element-integral equation methods. Japan’s Beyond 5G Promotion Consortium budgeted JPY 50 billion (USD 340 million) in 2024 for terahertz transceiver research, which obliges simulation vendors to extend solver ranges beyond 300 GHz and to incorporate quantum-corrected material models for graphene-based metasurfaces. Keysight’s PathWave Design 2025 uses machine-learning-assisted antenna synthesis to cut design iterations by 40%, enhancing competitiveness in time-sensitive base-station programs. Compliance with forthcoming ITU IMT-2030 guidelines will push vendors to simulate reconfigurable intelligent surfaces and holographic beamforming, use-cases that exceed the fidelity of classical asymptotic techniques.

Shift Toward Cloud-Based Simulation Platforms for Collaborative Engineering Workflows

Cloud deployments represented 42% of new electromagnetic simulation licenses in 2025, rising from 28% in 2023, as engineering teams replace capital expenditure on high-performance clusters with per-core-hour billing. Cadence OnCloud provisions Clarity 3D Solver instances on Amazon Web Services and Microsoft Azure, paring total ownership cost by roughly 30% for bursty workloads. Ansys Cloud Direct embeds elastic scaling inside the Electronics Desktop interface, allowing engineers to offload finite difference time domain sweeps without writing batch scripts. OnScale, a cloud-native platform, logged a 150% year-on-year rise in electromagnetic jobs during H1 2025 as medical-device makers accelerated specific absorption rate studies for wireless implants under IEC 62209. Security mandates keep defense and semiconductor users on-premise, but hybrid architectures that keep sensitive geometry in local vaults while executing field solves in private clouds are gaining momentum.

Increasing Use of AI-Powered Surrogate Models to Accelerate Design Cycles

Surrogate models trained on solver outputs trimmed design cycles by 60-80% in 2025 among semiconductor packaging houses and RF-integrated-circuit designers.[1]IEEE, “AI Surrogate Models in Electromagnetics,” ieee.org Neural networks, Gaussian processes, and polynomial chaos expansions learn the complex mapping from geometry to S-parameters, enabling real-time what-if analysis during schematic capture. TSMC adopted AI-assisted electromagnetic extraction at 3-nm and 2-nm nodes, cutting sign-off time by 35% and freeing compute capacity for additional design tape-outs. Ansys added PyAnsys libraries in 2025 R2 so users can export trained models as ONNX files for external optimization loops. Keysight’s RFPro 2024 applies active-learning algorithms to select the most informative sample points, reducing the number of full-wave simulations required to achieve 95% accuracy from more than 1,000 to fewer runs.

Growing Adoption of Automotive Radar and ADAS Sensors in Electric and Autonomous Vehicles

Automotive radar shipments surpassed 150 million units in 2025, with 77 GHz and 79 GHz imaging radar capturing 40% share as OEMs move from 2D to 4D sensing.[2]Continental, “2025 Automotive Radar Outlook,” continental.com Electromagnetic simulation is mandated for homologation under CISPR 25 and ISO 11452, forcing suppliers to validate emission levels before series production. Bosch invested EUR 800 million (USD 880 million) in radar development during 2024, emphasizing full-wave modeling of coupling between antennas, power-management ICs, and vehicle chassis grounds. Tesla’s Hardware 4 platform integrated eight imaging radar modules that required more than 10,000 finite difference time domain runs to minimize mutual coupling below -40 dB across 76-81 GHz. NXP’s S32R45 radar processor, released March 2025, ships with pre-validated electromagnetic models that shrink supplier design cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of ownership for HPC licenses and hardware requirements | -1.8% | Global, acute in South America, Middle East and Africa | Short term (≤ 2 years) |

| Shortage of skilled computational electromagnetics engineers | -1.3% | Global, pronounced in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Integration complexity with legacy CAD and EDA workflows | -0.9% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Accuracy limitations at terahertz frequencies for large-scale models | -0.6% | Global, concentrated in research and defense | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership for HPC Licenses and Hardware Requirements

Tier-1 electromagnetic solvers carry list prices between USD 50,000 and USD 150,000 per seat, with annual maintenance adding up to 22% of the initial fee. Production workloads often demand clusters with 128-512 CPU cores, graphics processing units for finite difference time domain acceleration, and low-latency interconnects that can lift hardware budgets beyond USD 500,000. Small and medium enterprises in South America, Middle East and Africa lack vendor financing and regional cloud centers, resulting in extended solver runtimes on underpowered workstations. Altair’s token-based HyperWorks license improves flexibility, yet uptake remains concentrated in North America and Europe where enterprise agreements dominate.[3]Altair Engineering, “HyperWorks Token Licensing FAQs,” altair.com GPU shortages through early 2025, caused by demand from generative-AI training, stretched workstation delivery times by up to six months, squeezing design schedules.

Shortage of Skilled Computational Electromagnetics Engineers

Fewer than 5,000 students earned advanced computational electromagnetics degrees in 2024, leaving more than 12,000 unfilled industry positions worldwide. Asia-Pacific semiconductor foundries and telecom equipment makers compete for scarce talent versed in the method of moments, multilevel fast multipole method, and finite integration technique formulations. A 2025 Remcom survey found that 70% of users lack the expertise to deploy advanced hybrid solvers or time-domain physical optics. Siemens launched a 12-week Simcenter FEKO certificate in January 2025, yet completion rates sit below 40% due to steep learning curves in Maxwell’s equations and mesh generation. University partnerships with Cadence and Altair will improve the pipeline, but the benefit will materialize gradually as graduates enter the workforce in 2027-2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solver Type: Hybrid Methods Balance Scale and Fidelity

The electromagnetic simulation software market size for solver type shows finite element method solutions holding 28% revenue in 2025, anchored by electric-motor, transformer, and MRI-coil design needs. Finite difference time domain is forecast to grow at a 13.5% CAGR as semiconductor fabs adopt it for on-chip antenna co-simulation at sub-3-nm nodes, where electromagnetic coupling interacts with transistor models in a single time-marching loop, driving incremental revenue across the electromagnetic simulation software market. Method of moments remains a staple for electrically large radar cross-section problems but requires multilevel fast multipole method acceleration to scale beyond 10 wavelengths. Altair’s Feko 2024.1 leverages graphics processing units to deliver a six-fold speed-up on NVIDIA A100 clusters, widening its appeal among phased-array developers.

Hybrid finite element-integral equation solvers bridge material versatility with open-boundary efficiency, explaining their growing share of the electromagnetic simulation software market. CST Studio Suite, now integrated within Dassault Systèmes’ 3DEXPERIENCE platform, reported a 25% uplift in hybrid-solver licenses in 2025 as 5G massive MIMO designers partition antenna arrays into finite element regions and free-space boundaries. Asymptotic techniques physical optics, geometric optics, and uniform theory of diffraction retain utility for radar signature prediction where the wavelength is much smaller than platform dimensions; however, they represent only 12% revenue as accuracy demands climb. Finite integration technique and transmission-line matrix solvers serve niche transient lightning-strike and electromagnetic compatibility studies where structured grids offset curved-surface limitations.

By Deployment Model: Elastic Compute Outpaces On-Premise Capital Spend

On-premise deployments captured 58% of 2025 revenue as defense, automotive, and semiconductor users shield proprietary geometry from public networks. Despite this base, cloud revenue is rising at a 16.5% CAGR and is poised to erode on-premise dominance in the electromagnetic simulation software market. The electromagnetic simulation software market share of hybrid cloud reached 18% in 2025 as vendors rolled out federated token licensing that tracks consumption across local and cloud nodes, smoothing budget forecasting.

Latency concerns once hindered interactive workflows, yet edge-compute zones adjacent to design offices now offer sub-50 ms round-trip times. Siemens’ Simcenter Cloud HPC delivers dedicated instances in European and North American data centers backed by service-level agreements, and uptake has been brisk among tier-1 automotive suppliers, balancing intellectual property control with compute elasticity. OnScale’s serverless architecture eliminates local installation and reduces ramp-up time to minutes, appealing to start-ups in medical devices that cannot fund hardware clusters.

By Application: Automotive Radar Leads Future Growth

Antenna design and analysis, the historical mainstay, represented 26% of 2025 revenue, yet growth is decelerating as handset and Wi-Fi antennas stabilize. Automotive radar and advanced-driver-assistance-system simulation is accelerating at 16.0% annually, lifting the electromagnetic simulation software market size for application segments. Intensifying CISPR 25 and ISO 11452 enforcement drives OEMs to conduct full-wave field solves before prototype builds, replacing physical chamber tests with digital homologation.

Electromagnetic compatibility and interference validation accounted for 18% of revenue as electric-vehicle power electronics introduce higher harmonic content. Biomedical applications grew 11%, propelled by wireless implants subject to IEC 62209 exposure limits. Metamaterials remain under 5% share but attract research grants aimed at terahertz photonics and cloaking, an early-stage opportunity that may mature post-2031. Circuit co-simulation and signal integrity remain essential for 56 Gbps and faster serial links, ensuring continued demand for S-parameter extraction within the electromagnetic simulation software industry.

By End-Use Industry: Automotive Narrows the Gap with Telecom

Telecommunications maintained a 27% revenue share in 2025, yet the automotive and transportation segment is expanding at 14.5% annually through 2031, pulling it closer to sector leadership in the electromagnetic simulation software market. Regulatory mandates for imaging radar and vehicle-to-everything (V2X) modules reinforce the need for early virtual validation. Aerospace and defense grew 8% as budgets shifted toward software-defined radio and directed-energy weapons, still maintaining high simulation workloads for radar cross-section and antenna placement.

Consumer electronics accounted for 15% of revenue but faces price pressure as OEMs consolidate supply chains. Healthcare advanced 11%, supported by neurostimulators and continuous glucose monitors that require specific absorption rate modeling. Industrial automation and Internet of Things grew 10% as factories deploy private 5G networks, and energy and utilities contributed 8% as silicon carbide converters raise electromagnetic interference concerns.

By Frequency Range: Millimeter Wave Surges, Terahertz Stays Experimental

Microwave frequencies (3-30 GHz) comprised 36% usage in 2025, tied to cellular base stations and satellite earth stations, but millimeter wave (30-300 GHz) is climbing at a 17.5% CAGR as fixed-wireless access and 4D automotive radar proliferate. Low-frequency solvers below 30 MHz remain vital for induction heating and wireless power transfer, steady at 9% share. Static and DC solvers, important for electric motor design, expand with electric-vehicle production, representing 8% revenue.

Terahertz (>300 GHz) constitutes under 3% of solver usage because material property models are immature and mesh requirements balloon for structures larger than a few centimeters. Keysight pushed its transient solver to 1 THz with adaptive mesh refinement that concentrates elements at material interfaces, cutting solve times by 40%. Adoption remains confined to university labs and defense research where budget and compute capacity exist to explore early 6G concepts.

Geography Analysis

North America accounted for largest share in 2025

North America accounted for 36% of 2025 revenue thanks to defense primes modeling radar signatures, hyperscalers performing electromagnetic compatibility studies on liquid-cooled racks, and automotive tier-1s validating radar modules for electric vehicles. The United States Department of Defense budgeted USD 1.2 billion in FY 2025 for electronic-warfare systems, a portion allocated to electromagnetic simulation software licenses. Canada auctioned 3.8 GHz spectrum in mid-2024, spurring antenna-array R&D investments. Mexico’s production of more than 3.5 million vehicles in 2024 pressed OEMs to perform in-country electromagnetic compatibility simulations before export under the United States-Mexico-Canada Agreement rules.

Asia-Pacific is projected to grow at a 12.8% CAGR from 2026-2031. China Mobile rolled out over 700,000 5G base stations in 2025, catalyzing demand for massive-MIMO array simulation. Japan’s Beyond 5G Promotion Consortium funds terahertz research, while South Korea schedules 6G field trials for 2028. India’s Reliance Jio earmarked USD 500 million in January 2025 for indigenous telecom equipment, underpinning domestic electromagnetic simulation spending. Japan integrated 4D radar into 30% of new vehicles during 2025, boosting CISPR 25-driven solver licenses.

Europe generated 22% of 2025 revenue, led by Airbus and Thales purchasing solvers for avionics electromagnetic compatibility under DO-160 and STANAG 4370 standards. Germany’s production of 4.1 million vehicles in 2024 necessitated solver capacity to certify electronic control units, and the United Kingdom’s GBP 250 million (USD 315 million) 5G diversification fund backed open-radio-access-network vendors requiring advanced antenna design. South America and Middle East and Africa together formed 6% of 2025 revenue, constrained by high total cost of ownership and limited compute infrastructure, but regional data centers in São Paulo, Dubai, and Johannesburg are widening cloud accessibility.

Competitive Landscape

The top five vendors, Ansys, Dassault Systèmes, Keysight Technologies, Cadence Design Systems, and Altair Engineering, held roughly 60% of 2025 revenue, indicating a moderately concentrated market. Synopsys’ USD 35 billion purchase of Ansys in January 2025 forged the largest electronic-design-automation and multiphysics simulation portfolio, signaling that chip-to-system workflows will hinge on integrated electromagnetic solvers. Niche suppliers such as Remcom, WIPL-D, and Sonnet offer perpetual licenses at 40-50% discounts and direct support, attracting cost-sensitive users but lacking resources to extend solvers into terahertz domains.

COMSOL’s unified multiphysics environment resonates with universities and small enterprises that prioritize workflow simplicity, contributing to a 20% license uptick in 2025. Technology investments concentrate on GPU acceleration for finite difference time domain solvers, adaptive mesh refinement around material interfaces, and federated cloud licensing that enables enterprises to balance on-premise and cloud compute budgets. Vendors are also embedding AI-powered design-space exploration to shorten optimization loops and differentiate offerings in an increasingly saturated core solver market.

Electromagnetic Simulation Software Industry Leaders

Remcom Inc.

Altair Engineering Inc.

Mician GmbH

Sonnet Software, Inc.

ElectroMagneticWorks, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Synopsys completed its USD 35 billion acquisition of Ansys, integrating electromagnetic solvers into a unified silicon-to-systems design platform.

- March 2025: Keysight Technologies introduced PathWave Design 2025 with machine-learning-based antenna synthesis and 1 THz solver capability.

- February 2025: Ansys released PyAnsys libraries in 2025 R2, enabling users to export surrogate models as ONNX files for external optimization.

Global Electromagnetic Simulation Software Market Report Scope

Electromagnetic simulation software is a modern technology that is primarily used to simulate electromagnetic devices based on different simulation methods. This software has become popular and has successfully replaced the costly traditional practice of prototyping. These packages are largely divided into two groups, namely circuit simulators and field simulators. These can readily be used to design a range of electromechanical, power electronics, RF and microwave, and high-frequency electronics devices and applications, such as sensors, transformers, antennas, and radomes.

The Electromagnetic Simulation Software Market Report is Segmented by Solver Type (FEM, FDTD, MoM, MLFMM, Asymptotic, Hybrid), Deployment (On-Premise, Cloud, Hybrid), Application (Antenna, Radar, EMC/EMI, Biomedical), End-Use (Telecom, Automotive, Aerospace, Electronics), Frequency (RF, Microwave, Millimeter Wave), and Geography (North America, Europe, Asia-Pacific, South America, MEA). Forecasts in Value (USD).

| Integral and Differential Equation Solvers | Finite Element Method (FEM) |

| Finite Difference Time Domain (FDTD) | |

| Method of Moments (MoM) | |

| Multilevel Fast Multipole Method (MLFMM) | |

| Finite Integration Technique (FIT) | |

| Transmission Line Matrix (TLM) | |

| Asymptotic Techniques | Physical Optics (PO) |

| Geometric Optics (GO) | |

| Uniform Theory of Diffraction (UTD) | |

| Hybrid and Other Numerical Methods | Hybrid FEM-IE Solvers |

| Finite Integral Method (FIM) |

| On-Premise |

| Cloud-Based |

| Hybrid |

| Antenna Design and Analysis |

| Mobile Device Electromagnetics |

| Automotive Radar and ADAS Sensors |

| Electromagnetic Compatibility (EMC/EMI) |

| Wireless Propagation and Channel Modelling |

| Other Applications (Biomedical and Healthcare Circuit Co-Simulation and Signal Integrity, Metamaterials and Photonics, and others) |

| Telecommunications |

| Automotive and Transportation |

| Aerospace and Defense |

| Consumer Electronics |

| Healthcare and Medical Devices |

| Industrial Automation and IoT |

| Other End-Use Industries |

| Static / DC |

| Low Frequency (< 30 MHz) |

| Radio Frequency (30 MHz - 3 GHz) |

| Microwave (3 - 30 GHz) |

| Millimeter Wave (30 - 300 GHz) |

| Terahertz (> 300 GHz) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Solver Type | Integral and Differential Equation Solvers | Finite Element Method (FEM) |

| Finite Difference Time Domain (FDTD) | ||

| Method of Moments (MoM) | ||

| Multilevel Fast Multipole Method (MLFMM) | ||

| Finite Integration Technique (FIT) | ||

| Transmission Line Matrix (TLM) | ||

| Asymptotic Techniques | Physical Optics (PO) | |

| Geometric Optics (GO) | ||

| Uniform Theory of Diffraction (UTD) | ||

| Hybrid and Other Numerical Methods | Hybrid FEM-IE Solvers | |

| Finite Integral Method (FIM) | ||

| By Deployment Model | On-Premise | |

| Cloud-Based | ||

| Hybrid | ||

| By Application | Antenna Design and Analysis | |

| Mobile Device Electromagnetics | ||

| Automotive Radar and ADAS Sensors | ||

| Electromagnetic Compatibility (EMC/EMI) | ||

| Wireless Propagation and Channel Modelling | ||

| Other Applications (Biomedical and Healthcare Circuit Co-Simulation and Signal Integrity, Metamaterials and Photonics, and others) | ||

| By End-Use Industry | Telecommunications | |

| Automotive and Transportation | ||

| Aerospace and Defense | ||

| Consumer Electronics | ||

| Healthcare and Medical Devices | ||

| Industrial Automation and IoT | ||

| Other End-Use Industries | ||

| By Frequency Range | Static / DC | |

| Low Frequency (< 30 MHz) | ||

| Radio Frequency (30 MHz - 3 GHz) | ||

| Microwave (3 - 30 GHz) | ||

| Millimeter Wave (30 - 300 GHz) | ||

| Terahertz (> 300 GHz) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current electromagnetic simulation software market size?

The market generated USD 1.66 billion in 2026 and is forecast to reach USD 2.70 billion by 2031.

Which segment will drive the highest CAGR through 2031?

Automotive radar simulation is expected to rise at a 16.0% CAGR as OEMs adopt 77 GHz and 79 GHz imaging radar modules.

How fast is the cloud deployment model growing?

Cloud-based platforms are expanding at a 16.5% CAGR as engineering teams favor elastic compute over capital equipment.

Which region is projected to add the most incremental revenue?

Asia-Pacific is set to increase at a 12.8% CAGR, propelled by massive 5G rollouts and 6G research investments.

Who are the top players in the market?

Ansys, Dassault Systèmes, Keysight Technologies, Cadence Design Systems, and Altair Engineering collectively hold about 60% revenue share.

What is the main barrier for small organizations adopting simulation software?

High total cost of ownership for licenses and hardware remains the leading obstacle, particularly in emerging economies.

Page last updated on: