Automotive Simulation Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

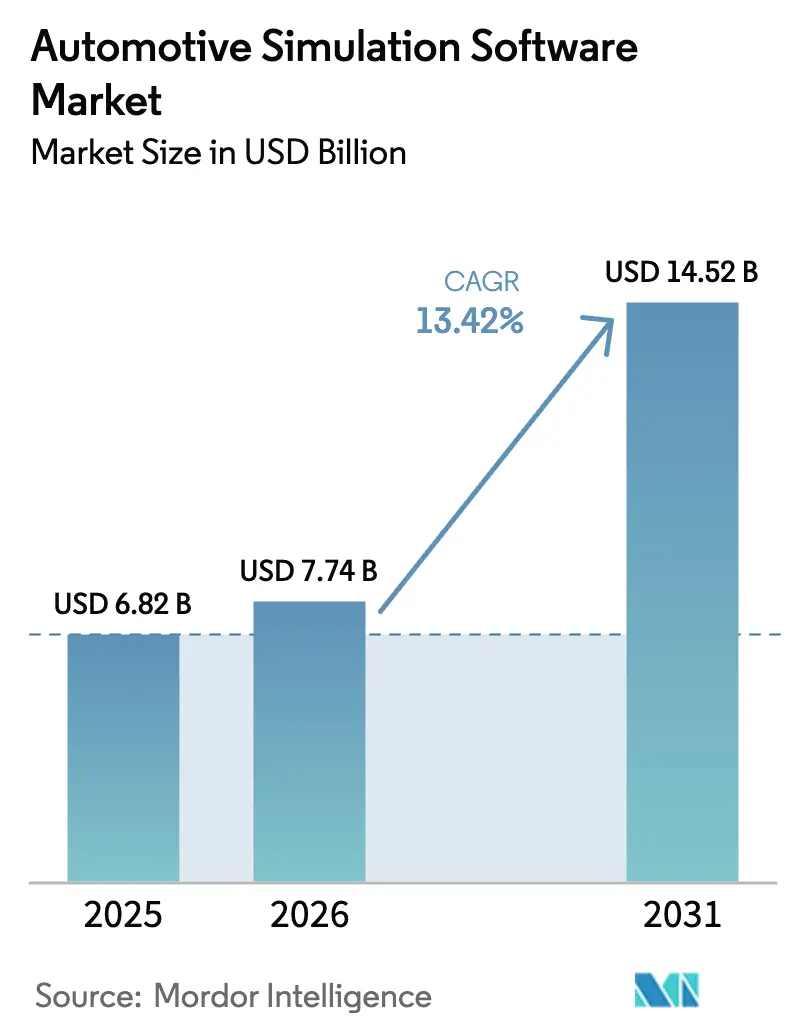

| Market Size (2026) | USD 7.74 Billion |

| Market Size (2031) | USD 14.52 Billion |

| Growth Rate (2026 - 2031) | 13.42% CAGR |

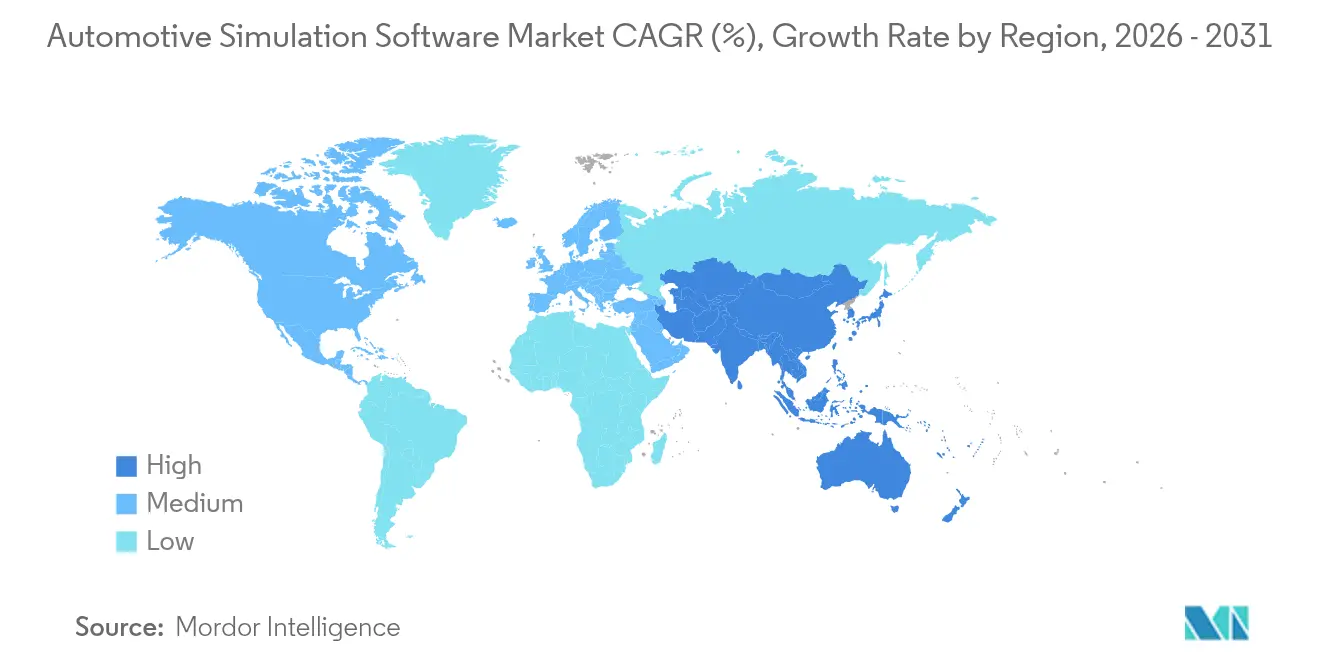

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Simulation Software Market Analysis by Mordor Intelligence

The automotive simulation software market size was valued at USD 6.82 billion in 2025 and estimated to grow from USD 7.74 billion in 2026 to reach USD 14.52 billion by 2031, at a CAGR of 13.42% during the forecast period (2026-2031). Growth is propelled by the shift from hardware-centric design to virtual prototyping, the need to validate complex electric-vehicle (EV) and autonomous-driving systems, and the rapid maturation of cloud-based high-performance computing. Regulatory mandates such as the EU General Safety Regulation II and UN R171 are embedding virtual testing in approval workflows, while simulation-as-a-service business models broaden access for smaller firms. Leading vendors are embedding AI in scenario generation, shortening development cycles and lowering total cost of ownership. At the same time, moderate competitive intensity and ongoing consolidation signal a race to offer end-to-end platforms that cover mechanical, electrical and software domains.

Key Report Takeaways

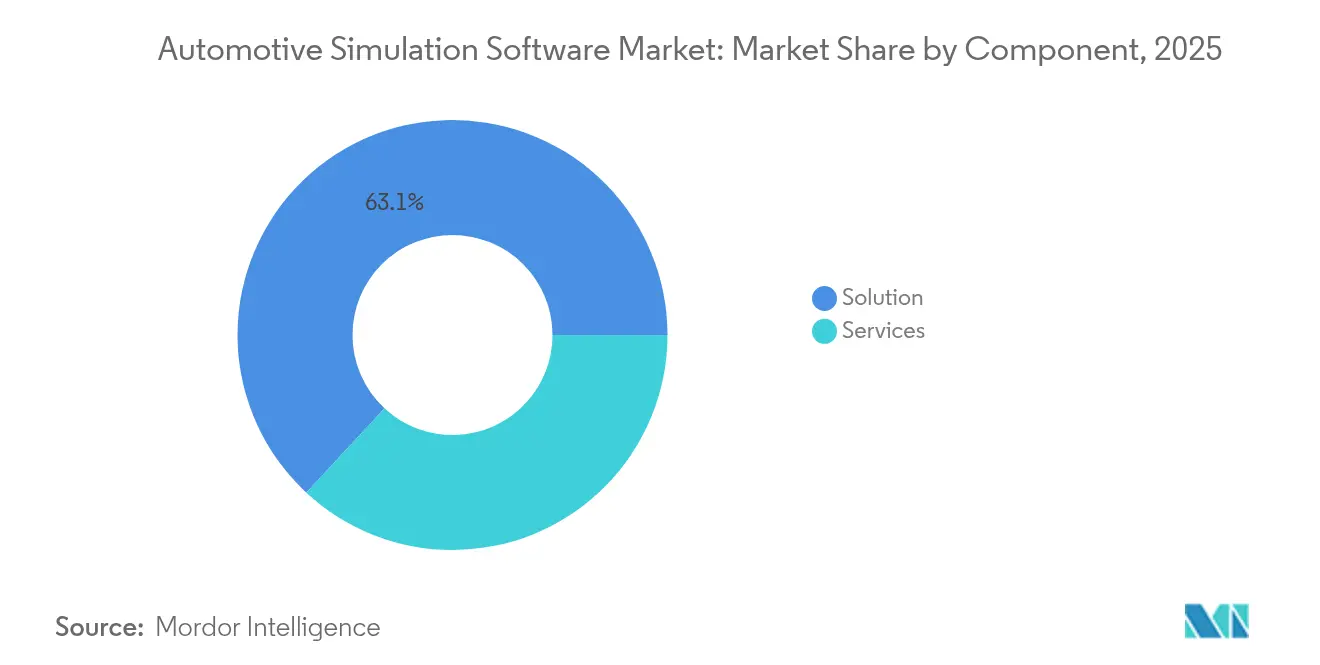

- By component, solutions led with 63.10% of the automotive simulation software market share in 2025; services are projected to expand at a 15.44% CAGR to 2031.

- By deployment model, on-premises installations held 56.90% share of the automotive simulation software market size in 2025, while cloud deployments are forecast to grow at 17.95% CAGR through 2031.

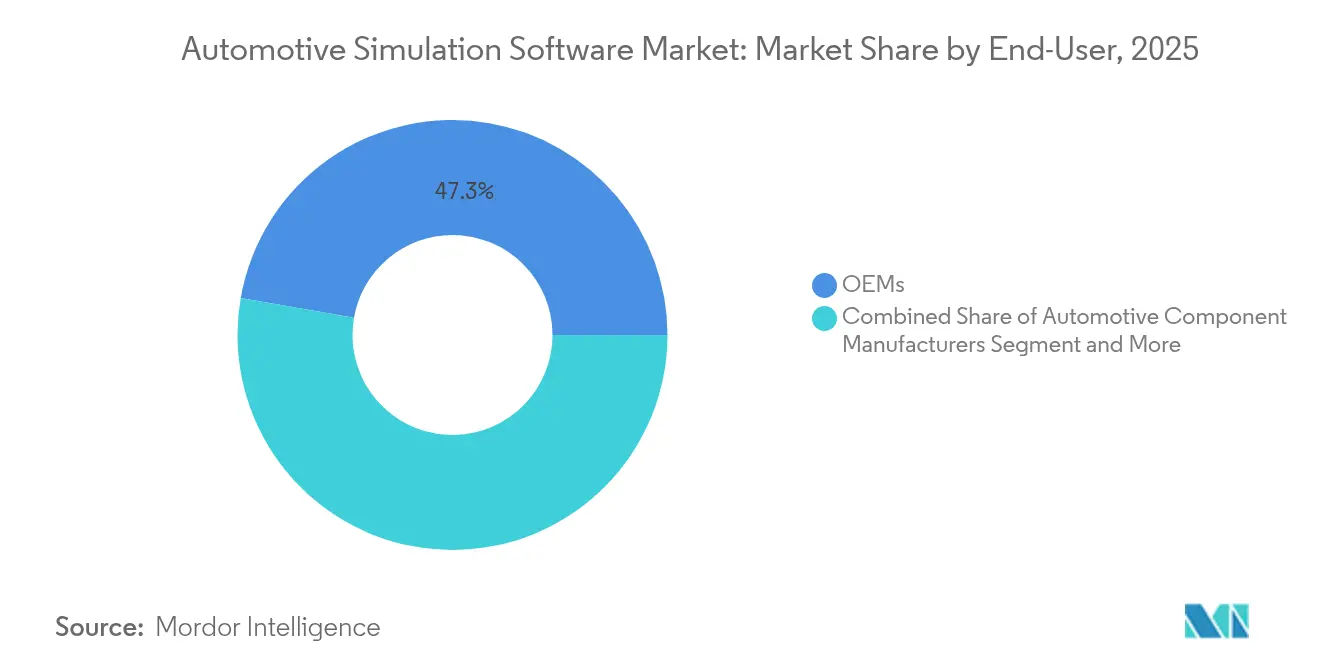

- By end user, OEMs accounted for 47.25% share of the automotive simulation software market size in 2025 and engineering service providers are advancing at a 14.39% CAGR to 2031.

- By application, vehicle dynamics captured 31.60% of the automotive simulation software market share in 2025; autonomous-driving simulation is poised for the fastest 19.85% CAGR to 2031.

- By geography, Asia-Pacific commanded 37.40% revenue share in 2025 and is set to record a 13.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Simulation Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for virtual prototyping | +3.2% | North America and Europe | Medium term (2–4 years) |

| Accelerated EV/AV programs require software-centric validation | +4.1% | Asia-Pacific core; spill-over to North America | Short term (≤ 2 years) |

| Shift toward cloud-based HPC and SaaS licensing | +2.8% | Global, led by North America and Europe | Medium term (2–4 years) |

| Safety-driven regulations encouraging virtual testing | +1.9% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| OEM subscription revenue models for simulation-as-a-service | +1.2% | Global, early adoption in North America | Medium term (2–4 years) |

| Venture-capital inflow into SimOps automation platforms | +0.6% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing demand for virtual prototyping

Virtual factories pioneered by BMW cut planning costs 30% and compress collision-check cycles from four weeks to three days, demonstrating how immersive digital twins shrink lead times and improve resource efficiency. EV programs rely on simulation to optimise thermal management and battery integration before physical builds commence, while academic studies report productivity gains of 14.53% and energy savings of 13.9% in flexible lines when digital twins steer decision-making. The approach also supports the software-defined vehicle paradigm by enabling over-the-air update scenarios to be validated across domains.

Accelerated EV/AV programs require software-centric validation

Autonomous-vehicle developers employ AI-ready simulation suites that replicate millions of edge-case scenarios, slashing on-road testing costs. Applied Intuition’s platform, built on 25 years of vehicle-dynamics modelling, exemplifies this shift toward high-fidelity virtual validation. Research published on arXiv underscores the need for synthetic data generation and instance-level fidelity to assure safety in corner-case conditions. Regulators reinforce the trend by recognising virtual testing in UN R171, further embedding simulation in homologation pipelines.

Shift toward cloud-based HPC and SaaS licensing

Partnerships such as Siemens with Rescale have trimmed software outlays by up to 60% and enabled engineers to run parallel simulations that formerly required costly on-premises clusters. Hexagon’s Nexus Compute delivers cloud elasticity that lets small suppliers execute workloads previously out of reach, powering multi-disciplinary optimisation without capital expenditure. Organisations report surges in compute demand for design-of-experiments studies and digital-twin synchronisation, making cloud the preferred pathway for burst capacity and global collaboration.

Safety-driven regulations encouraging virtual testing

The EU General Safety Regulation II, effective July 2024, mandates virtual validation for advanced driver-assistance functions, turning simulation from an option into a compliance imperative[1]Markus Schäfer, “EU General Safety Regulation II Drives Virtual Validation,” continental-automotive.com. ISO 26262 Version 3 and SOTIF guidelines extend coverage to machine-learning components, demanding probabilistic assessments that are only feasible in silico. Ansys, TÜV SÜD and Microsoft have responded with a cloud-based homologation toolchain that condenses certification lead times while assuring traceability.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost and integration complexity | –2.1% | Global, affecting SMEs | Medium term (2–4 years) |

| Enterprise IP and data-security concerns in multi-tenant clouds | –1.4% | Europe and North America | Short term (≤ 2 years) |

| Shortage of skilled CAE simulation engineers | –1.8% | North America and Europe | Long term (≥ 4 years) |

| AI-scenario model fidelity gaps for edge-case validation | –0.9% | Global, critical for AV | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High upfront cost and integration complexity

Enterprise-grade licences, specialised hardware and process re-engineering impose multimillion-dollar outlays that deter small suppliers. Stellantis’ adoption of AutoForm Assembly R12 illustrates the burden: extensive body-in-white process restructuring was required before savings materialised[2]James Anderton, “BMW Virtual Factory Cuts Planning Time,” assemblymag.com. Cross-domain integration adds difficulty as firms must harmonise powertrain, thermal and electromagnetic simulations within continuous-integration workflows.

Shortage of skilled CAE simulation engineers

Ninety-four percent of automotive employers report difficulty filling AI and advanced simulation roles, especially those requiring three to seven years of experience[3]“Engineering Skills Gap Widens in Automotive,” ethrworld.com. University curricula lag the fast-evolving toolchain that now includes AI-driven scenario generators and cloud-native SimOps. Competition from tech companies and retirements of veteran engineers tighten the labour market, limiting adoption speed even where budgets exist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Dominate Despite Services Acceleration

Solutions generated the largest revenue, equivalent to 63.10% of the automotive simulation software market in 2025, underscoring the enduring reliance on physics-based engines from Ansys, Siemens and Dassault Systèmes. The automotive simulation software market size attributed to services, although smaller, is projected to rise at 15.44% CAGR as enterprises seek managed simulation, training and scenario-generation expertise.

Growth in services mirrors the scarcity of in-house CAE talent and the need to embed AI in simulation pipelines. Investments such as BMW i Ventures’ USD 20 million in Simr highlight demand for SimOps automation that simplifies multi-tool orchestration. Integration specialists are also capitalising on the move to cloud HPC, helping clients migrate legacy workflows and ensure IP protection.

By Deployment Model: Cloud Disruption Accelerates

On-premises systems retained 56.90% share in 2025 because many OEMs prioritise data sovereignty. Yet cloud deployments are scaling at an 17.95% CAGR as usage-based pricing mitigates capital constraints and hyperscale compute supports massive scenario sweeps. The automotive simulation software market size captured by cloud offerings is therefore expected to expand rapidly over the forecast horizon.

Platforms such as Hexagon’s Virtual Test Drive X provide autonomous-driving validation with consumption pricing, while Siemens’ Simcenter-as-a-service enables global teams to run thousands of jobs in parallel. Persistent concerns over multi-tenant security and export-control rules temper uptake, but vendor roadmaps centred on confidential-compute and sovereign-cloud zones are narrowing the trust gap.

By End User: Engineering Service Providers Emerge as Growth Leaders

OEMs controlled 47.25% of 2025 revenue thanks to long-term digital-twin programs that span design to after-sales. However, engineering service providers are forecast to grow 14.39% CAGR, capturing clients that lack internal CAE bandwidth. Their share of the automotive simulation software market is set to rise as outsourcing counteracts the talent squeeze.

Acquisitions such as Hinduja Tech’s purchase of TECOSIM show service firms scaling domain breadth from crash to battery modelling. Component suppliers remain steady adopters of simulation for powertrain and thermal optimisation, while research institutes push the frontier on perception-stack testing using MATLAB-Simulink co-simulation environments.

By Application: Autonomous Driving Simulation Leads Innovation

Vehicle dynamics held a 31.60% stake in 2025, reflecting decades of deployment across chassis optimisation. The automotive simulation software market size for autonomous-driving and ADAS simulation is, however, projected to exhibit a 19.85% CAGR as firms tackle perception, prediction and planning validation.

Applied Intuition and MORAI deliver stochastic scenario libraries that help OEMs cover edge cases impossible to reproduce safely on public roads. Battery-thermal and crash-safety simulations remain essential for EV homologation, while process-level tools like ESI Group’s BM-Stamp fuel interest in stamping-line digital twins that shrink time-to-launch.

Geography Analysis

Asia-Pacific dominated the automotive simulation software market with 37.40% revenue share in 2025, buoyed by national EV targets, smart-mobility subsidies and a widening pool of local software talent. The region is forecast to grow 13.25% CAGR, driven by large-scale digital-twin factory rollouts such as NIO’s collaboration with Unity China that streamlines body shop commissioning. Government-backed autonomous-driving sandboxes across China, Japan and South Korea further accelerate software-centric validation.

North America remains a technological pacesetter thanks to the concentration of CAE vendors and vibrant venture-capital funding. Start-ups like Vsim and Coval collectively secured over USD 25 million in fresh capital during 2024, targeting AI-first scenario generation that complements traditional finite-element solvers. Regulatory clarity from NHTSA on virtual-testing data acceptance is expected to boost uptake among Tier-1 suppliers seeking faster ADAS certification cycles.

Europe leverages stringent safety and sustainability frameworks to foster simulation adoption. The automotive simulation software market benefits from EU Green Deal incentives that reward material-efficient design validated through multiphysics simulation. Cloud-sovereignty initiatives such as GAIA-X underpin vendor commitments to European data-residency, reducing IP-exposure fears for German luxury brands and French commercial-vehicle makers.

Emerging regions in South America, the Middle East and Africa display rising demand as OEMs establish regional R&D hubs that rely on virtual collaborative platforms rather than expensive proving-ground expansions.

Competitive Landscape

The automotive simulation software market is moderately concentrated. Siemens’ USD 10.6 billion takeover of Altair in March 2025 produced the industry’s most extensive AI-powered multiphysics suite and tightened competition with Dassault Systèmes and Ansys. Ansys itself is poised to join Synopsys in a USD 35 billion deal, signalling closer integration of semiconductor, software and system-level simulation. Vendors are racing to infuse large-language-model assistants that reduce scripting needs and make complex solvers usable by non-experts.

Commercial strategy is shifting toward cloud marketplaces and consumption-based licences that undercut perpetual models. Siemens’ Simcenter on Rescale, Hexagon’s VTDx on Microsoft Azure and Dassault’s 3DEXPERIENCE on AWS exemplify the pivot. These channels lower entry barriers for mid-tier suppliers while giving vendors recurring revenue visibility. Niche challengers such as MORAI target unmanned-air-mobility test beds, while Simr focuses on SimOps automation that unifies disparate solver silos.

White-space innovation is clustering around AI-generated scenarios, confidential computing for IP protection, and verticalised toolchains for emerging domains like vehicle-to-everything communications. Partnerships with cloud hyperscalers deliver elastic compute, whereas collaborations with certification bodies integrate digital evidence directly into homologation dossiers. Collectively, these moves suggest a market moving from standalone point solvers to federated, AI-augmented platforms covering concept to after-sales.

Automotive Simulation Software Industry Leaders

Ansys, Inc.

Siemens AG

Dassault Systèmes

Autodesk, Inc.

PTC Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Siemens finalised its USD 10.6 billion acquisition of Altair Engineering, expanding AI-powered mechanical and electromagnetic simulation across the Siemens Xcelerator portfolio.

- February 2025: Dassault Systèmes and Volkswagen deployed the 3DEXPERIENCE cloud platform to streamline vehicle development with virtual-twin experiences.

- January 2025: Ansys, TÜV SÜD and Microsoft launched a cloud-based virtual-homologation toolchain to accelerate regulatory compliance.

- January 2025: Hexagon introduced Virtual Test Drive X on Azure, offering consumption-priced, hyperscale validation for ADAS and AV systems.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the automotive simulation software market as licensed or subscription-based digital platforms that enable vehicle makers and suppliers to model, test, and optimize complete vehicles, systems, or components across dynamics, powertrain, crash, ADAS, and manufacturing process domains.

Scope Exclusion: generic Computer-Aided Engineering suites sold for non-automotive industries and hardware-in-the-loop rigs are kept outside this sizing.

Segmentation Overview

- By Component

- Solution

- Physics-based simulation platforms

- Data-management and integration tools

- Services

- Implementation and Integration

- Consulting and Training

- Managed Simulation Services

- Solution

- By Deployment Model

- On-Premises

- Cloud

- By End User

- OEMs

- Automotive Component Manufacturers

- Engineering Service Providers

- Academic and Research Institutes

- By Application

- Vehicle Dynamics

- Powertrain and Battery Simulation

- Crash and Safety

- Autonomous Driving and ADAS

- Manufacturing Process Simulation

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview simulation product managers at global OEMs, CAE engineers at Tier 1 suppliers, cloud-platform integrators, and certification assessors across Asia-Pacific, Europe, and North America. These conversations validate price corridors, license volumes, and emerging use cases.

Desk Research

We start with authoritative public data, drawing trend lines from global vehicle output (OICA), electric-vehicle penetration (IEA), and safety rulebooks such as UN R135 and FMVSS that directly shape virtual validation demand. Trade association white papers, SAE technical journals, and company 10-Ks enrich context, while paid resources like Marklines and D&B Hoovers let us cross-reference fleet mix and vendor revenue. The list is illustrative only, and many additional sources inform the evidence base.

Market-Sizing & Forecasting

A single top-down and bottom-up hybrid model underpins the numbers. We reconstruct the demand pool from worldwide light-vehicle and commercial build volumes, apply region-specific simulation spend per platform, and then test outputs against sampled supplier roll-ups and channel checks. Key inputs include EV share, average ECU count, ADAS regulation milestones, cloud HPC cost curves, and selling price shifts of physics-based and AI-driven solvers. Multivariate regression, chosen for clarity, projects 2025-2030 values, with scenario analysis adjusting for regulatory pace and build volatility.

Data Validation & Update Cycle

Model outputs undergo anomaly scans, senior review, and sign-off. Reports refresh each year, and interim updates are triggered when material events such as new regulations or major acquisitions alter underlying assumptions.

Why Mordor's Automotive Simulation Software Baseline Commands Confidence

Published estimates often diverge because definitions, input variables, and refresh timing differ across firms.

Key Gap Drivers include whether revenue from consulting services is counted, the choice between perpetual and subscription pricing, treatment of cloud consumption fees, and the currency year used for conversion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.82 B (2025) | Mordor Intelligence | - |

| USD 6.03 B (2024) | Regional Consultancy A | excludes cloud usage fees and updates less frequently |

| USD 1.80 B (2023) | Global Consultancy B | limits scope to prototyping applications and omits services revenue |

| USD 6.15 B (2024) | Trade Journal C | applies aggressive EV ramp and longer forecast base that inflate totals |

The comparison shows that clients rely on Mordor's disciplined variable selection, annual refresh, and reproducible steps to secure a balanced baseline that supports confident strategic planning.

Key Questions Answered in the Report

What is the current value of the automotive simulation software market?

The market is valued at USD 7.74 billion in 2026 and is projected to reach USD 14.52 billion by 2031.

Which segment is growing fastest in the automotive simulation software market?

Cloud deployment is the fastest-growing segment with an 17.95% CAGR through 2031 thanks to elastic compute and usage-based pricing.

Why is Asia-Pacific the largest regional market?

High EV production, government-funded autonomous-driving programs and expanding digital-twin factories give Asia-Pacific 37.40% revenue share and a 13.25% CAGR outlook.

How are new safety regulations influencing adoption?

EU General Safety Regulation II and UN R171 embed virtual testing in approval processes, making simulation mandatory for ADAS and autonomous features.

What is the biggest challenge limiting market expansion?

A shortage of skilled CAE engineers—reported by 94% of employers—slows deployment of advanced simulation workflows despite strong demand.

Which companies are reshaping competitive dynamics?

Siemens (via Altair), Ansys (via Synopsys), Applied Intuition and MORAI are redefining platform breadth, cloud delivery and AI-driven scenario generation within the market.

Page last updated on: