GNSS Simulators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

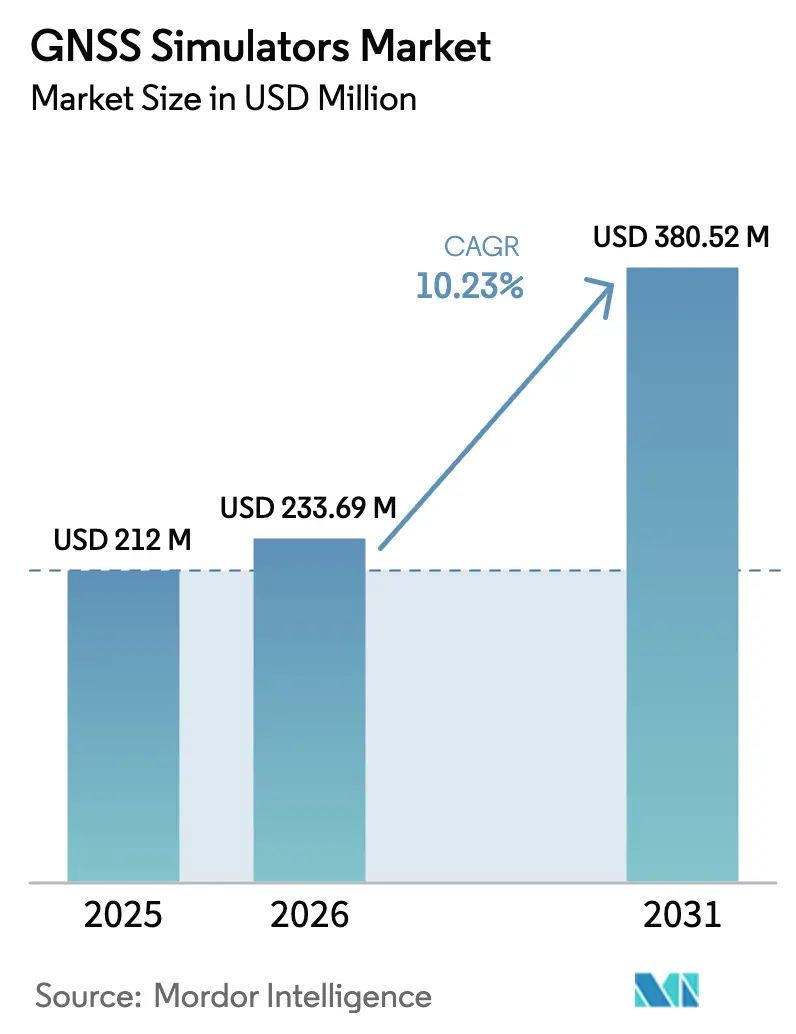

| Market Size (2026) | USD 233.69 Million |

| Market Size (2031) | USD 380.52 Million |

| Growth Rate (2026 - 2031) | 10.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GNSS Simulators Market Analysis by Mordor Intelligence

The GNSS simulators market size is expected to grow from USD 212 million in 2025 to USD 233.69 million in 2026 and is forecast to reach USD 380.52 million by 2031 at 10.23% CAGR over 2026-2031. Demand has been fuelled by rapid migration from single- to multi-constellation receivers, surging requirements for secure positioning, navigation, and timing (PNT) testing, and steady advances in software-defined radio (SDR) platforms. Hardware suppliers expanded channel capacity, while software vendors introduced cloud-based scenario generation to shorten test cycles. Autonomous-vehicle development, LEO-based PNT signals, and stringent defense procurement for anti-jamming solutions collectively kept the GNSS simulators market on a strong growth trajectory across aerospace, automotive, maritime, and IoT domains. Export-controlled technology, however, constrained sales to certain regions, and high capital costs slowed adoption among smaller laboratories.

Key Report Takeaways

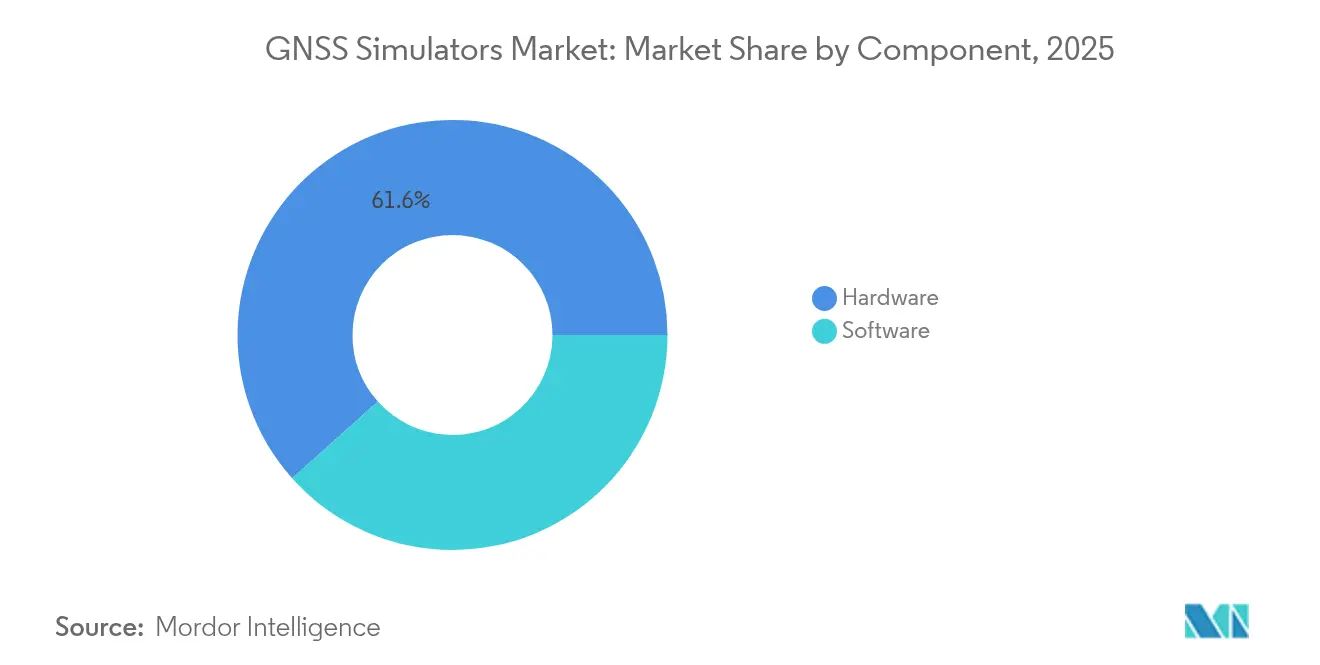

- By component, hardware held 61.60% of GNSS simulators market share in 2025; software licenses and SDR add-ons are projected to grow at a 14.12% CAGR to 2031.

- By channel type, multichannel (≤16) platforms led with 56.60% revenue share in 2025, while wavefront/CRPA systems are advancing at a 14.63% CAGR through 2031.

- By GNSS receiver compatibility, GPS-based testing accounted for 45.70% of demand in 2025; BeiDou-ready solutions are forecast to expand at a 13.74% CAGR between 2026-2031.

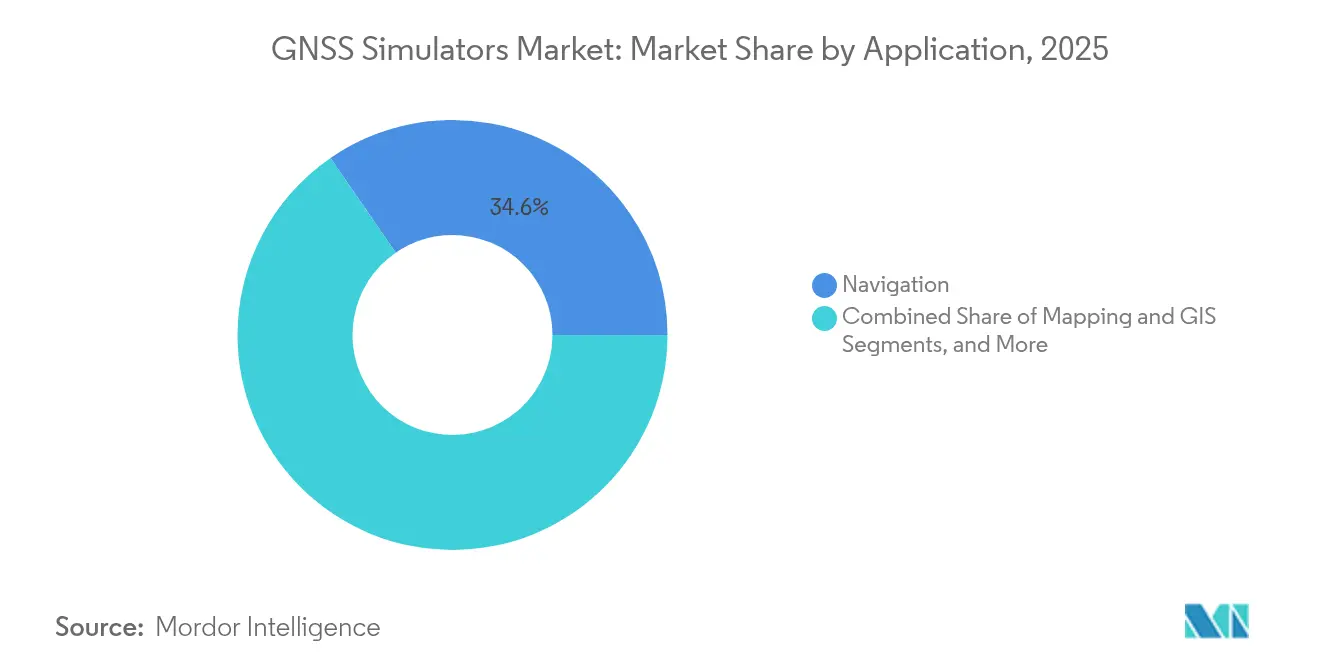

- By application, navigation R&D captured 34.60% of the GNSS simulators market size in 2025, and space-systems validation is set to climb at a 16.28% CAGR to 2031.

- By industry vertical, military and defense commanded 41.70% of revenue in 2025, while automotive and autonomous vehicles will post the fastest 17.39% CAGR through 2031.

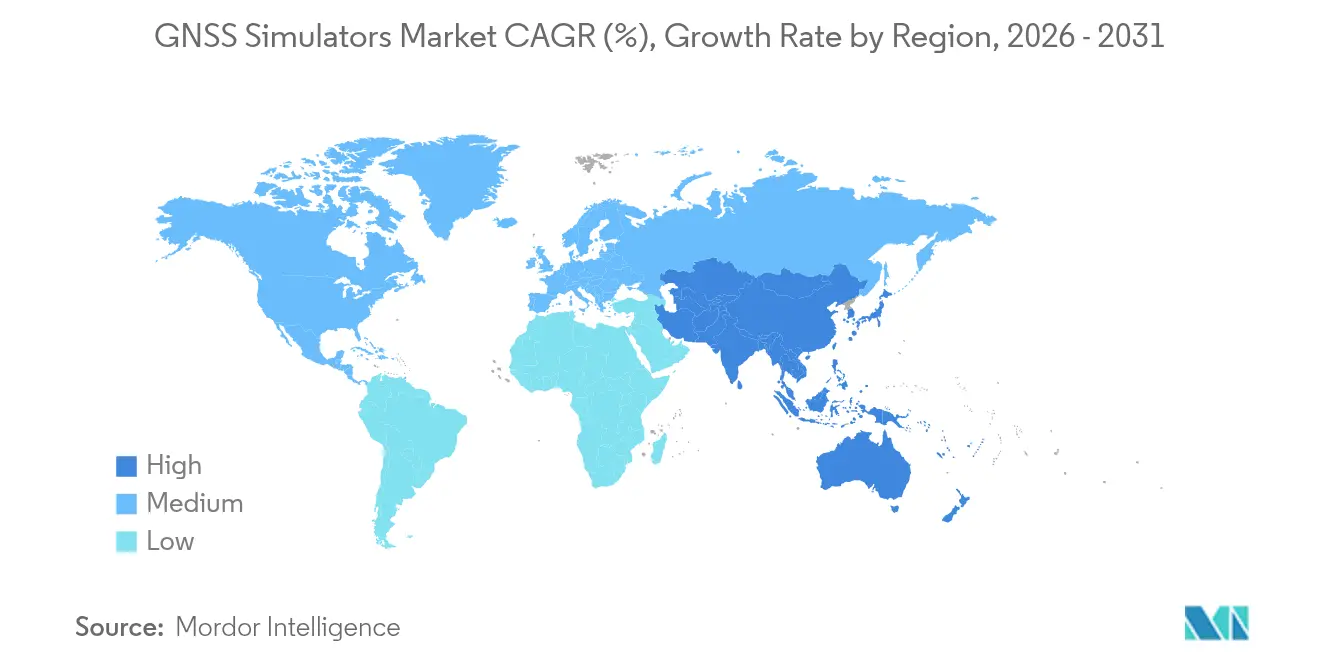

- By region, North America dominated with a 37.80% share in 2025; Asia-Pacific will register the highest 12.64% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global GNSS Simulators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision navigation boom | +3.1% | Global, higher in North America and Europe | Medium term (2-4 years) |

| IoT and consumer devices expansion | +2.6% | Global, higher in Asia-Pacific | Medium term (2-4 years) |

| Autonomous-vehicle HIL testing needs | +2.1% | North America, Europe, China, Japan | Long term (≥4 years) |

| PNT-resilience mandates | +1.6% | North America, Europe | Short term (≤2 years) |

| LEO-PNT constellation momentum | +1.0% | Global | Long term (≥4 years) |

| SDR simulators for on-orbit servicing | +0.5% | North America, Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Precision navigation boom reshaped testing requirements

Industries such as agriculture, surveying, and automated machinery moved from meter-level to centimeter-level accuracy, forcing vendors to replicate correction streams, multi-constellation signals, and RTK/PPP workflows. The European Space Agency funded projects that benchmarked authentication schemes and visual-inertial integrations, underscoring how sovereign navigation capabilities rely on advanced simulation laboratories.[1]European Space Agency, “Element 1 – Innovation in Satellite Navigation,” esa.int

IoT integration drove miniaturization and cost optimization

Mass-market chipsets inserted GNSS into asset trackers, wearables, and consumer electronics, prompting demand for compact simulators that reproduce urban multipath and low-power receiver behavior. Quectel’s multi-band active antenna launch illustrated the scale of component innovation in 2025.

Autonomous-vehicle development accelerated hardware-in-the-loop testing

Car makers and defense agencies synchronized GNSS signal generation with lidar, radar, and camera models to validate safe navigation under urban-canyon and tunnel conditions. The U.S. Army’s VANE tool suite integrated such multi-sensor simulation to shorten development cycles.

PNT-resilience mandates elevated military testing requirements

U.S. and European defense buyers procured wavefront systems to rehearse jamming and spoofing scenarios. Safran Federal Systems’ CMOSS-compliant C-PNT card showcased modular architectures combining GNSS with alternative signals to protect mission-critical assets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost | -1.6% | Global, higher in emerging markets | Short term (≤2 years) |

| Satellite-signal changes | -1.0% | Global | Medium term (2-4 years) |

| Export-control limits | -0.8% | China, Russia, the Middle East | Medium term (2-4 years) |

| Open-source spoof tools | -0.5% | Global | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High capital costs limited market penetration

Advanced systems exceeding 16 channels or incorporating wavefront antennas commanded prices in the hundreds of thousands of dollars, keeping many universities and start-ups on legacy or SDR-based test rigs. Joint NI and M3 Systems projects demonstrated lower-cost alternatives yet could not fully match high-fidelity RF performance.

Satellite-signal changes increased update complexity

Ongoing modernization of GPS, Galileo, and BeiDou generated evolving signal structures that forced regular hardware and firmware upgrades, stretching program budgets and prolonging validation cycles. Hardware suppliers introduced modular chassis and remote-update features, but qualification testing still required significant downtime for system recertification.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Gains on Hardware Dominance

Hardware platforms accounted for 61.60% of revenue in 2025, highlighting the importance of precision RF generation for aerospace and defense test campaigns. Their rack-mount architectures hosted multi-constellation channels, phase coherency, and high dynamic ranges demanded by guided-weapons validation. Yet software licenses and SDR add-ons grew fastest at a 14.12% CAGR, driven by cloud-hosted scenario builders and pay-as-you-go licensing that lowered entry barriers for start-ups and academia.

Software-defined approaches enabled continuous updates to reflect new GNSS message formats and interference models. Vendors embedded AI-powered scenario generation that cut manual script time by 35%. The GNSS simulators market size for software innovations is projected to expand alongside the adoption of container-based deployment in DevSecOps environments. Hybrid configurations pairing SDR front-ends with COTS PCs allowed engineering teams to iterate quickly while reserving high-end hardware time for final acceptance testing.

By Channel Type: Wavefront Technology Disrupts Traditional Simulators

Multichannel (≤16) units delivered 56.60% of 2025 revenue, balancing cost and capability for commercial avionics, maritime, and surveying applications. Wavefront/CRPA systems, however, are forecast to post a 14.63% CAGR as militaries prioritize anti-jamming. These platforms reproduce spatially separated beams that stimulate controlled reception pattern antennas and measure null-forming performance against hostile interference.

High-channel (>16) simulators occupied a middle tier for integrators that needed multiple constellations but not full spatial emulation. Meanwhile, single-channel boxes served manufacturing test lines for consumer receivers. The GNSS simulators market share for wavefront solutions is expected to widen as automotive makers evaluate array antennas for Level-4 autonomous functions and seek realistic over-the-air test chambers compliant with ISO 26262

By GNSS Receiver Compatibility: BeiDou Adoption Accelerates

GPS support remained indispensable, covering 45.70% of 2025 compatibility requests. BeiDou inclusion climbed rapidly as version 3 offered global coverage and decimeter-level PPP-B2b services, triggering a 13.74% forecast CAGR in related simulator demand. Galileo and GLONASS maintained relevance for multi-frequency timing markets, while regional systems such as NavIC and QZSS appeared in new automotive mandates across Asia.

Vendors updated firmware to stream OSNMA-authenticated Galileo signals and new BeiDou civil codes. The GNSS simulators market size tied to comprehensive constellation coverage grew as regulators mandated multi-constellation receivers for aviation and maritime safety. Test labs valued configurable signal masks that reproduced scheduled outages, satellite almanac anomalies, and differential correction streams to validate resilience strategies.

By Application: Space Systems Validation Leads Growth

Navigation R&D captured 34.60% of spending in 2025, underpinning laboratory prototyping across industrial, academic, and governmental entities. Yet space-systems validation is projected to outpace all other uses at a 16.28% CAGR as LEO constellations, lunar exploration, and on-orbit servicing programs proliferate. NASA and ESA laboratories installed zero-delay loopbacks that mimic Doppler shifts and signal dynamics encountered above 1,000 km altitude.

Mapping/GIS, surveying, and vehicle-assistance workflows continued to rely on multipath and ionospheric error modeling. The GNSS simulators market continues to benefit from tight coupling with inertial sensors in hardware-in-the-loop environments that reduce field-test iterations. Timing applications remained niche yet essential for telecom synchronization, where phase-noise performance dictated equipment selection.

By Industry Vertical: Automotive Sector Challenges Military Dominance

Military and defense users maintained a 41.70% revenue share in 2025, driven by range testing, munition guidance, and electronic-warfare resilience. However, automotive and autonomous vehicles will exhibit the highest 17.39% CAGR through 2031 as Level-3+ functionalities rely on lane-level positioning. China’s GB/T 45086.1-2024 standard, effective June 2025, has already pushed OEMs to extend GNSS simulator coverage for compliance audits.

Consumer electronics manufacturers pursued affordable test beds to characterize smartphone dual-frequency performance under blocked-sky scenarios. Maritime and aerospace operators demanded multi-antenna phase-center calibration for precision approach and landing. The GNSS simulators industry also addressed telecom edge data-center timing, ensuring 5G network slices met microsecond-level synchronization.

Geography Analysis

North America led the GNSS simulators market with a 37.80% share in 2025, buoyed by Pentagon funding for wavefront solutions and space-force test ranges. Contracts for anti-jam CRPA validation sustained high-ticket procurements among primes such as Safran Electronics and Defense and Spirent Communications. The region’s vibrant autonomous-vehicle ecosystem amplified demand for hardware-in-the-loop rigs that merge GNSS with lidar and radar feeds.

Asia-Pacific has been the fastest-growing geography, expected to register a 12.64% CAGR through 2031. China’s BeiDou adoption in logistics, ride-hailing, and smart-city infrastructure spurred simulator upgrades at R&D institutes and provincial test centers. India’s NavIC augmentation for agriculture and disaster management created procurement pipelines for dual-mode simulators. Local manufacturing strengths lowered price points, enabling wider uptake among universities.

Europe maintained a significant stake, supported by ESA’s NAVISP innovation funding and Galileo modernization. Automotive tier-1 suppliers in Germany and Sweden integrated simulator banks into functional-safety verification flows. The region emphasized authenticated navigation, driving upgrades that replicate OSNMA use cases and resilient PNT scenarios for rail and aviation. Collaborative research projects across universities and small-medium enterprises fostered open-architecture SDR test frameworks, ensuring the GNSS simulators market remained competitive and technologically diverse.

Competitive Landscape

The GNSS simulators market displayed moderate consolidation, with the top five suppliers accounting for roughly 65% of revenue. Spirent Communications held the lead through its PNT X platform, offering up to 2,000 independently controllable signals and sub-nanosecond timing. Rohde and Schwarz leveraged its broader RF expertise to integrate broadband interference sources within a single enclosure, reducing rack space at automotive labs.

M&A reshaped competitive positioning. Hexagon closed its purchase of Septentrio in April 2025, strengthening positioning for autonomous and mission-critical solutions while adding ASIC-level receiver knowledge to its portfolio.[4]Hexagon, “Hexagon Completes the Acquisition of Septentrio NV,” hexagon.com VIAVI Solutions completed its Inertial Labs acquisition in December 2024, broadening offerings to include visual-aided inertial navigation for GPS-denied operations. Patent filings—such as Spirent’s multi-channel over-the-air emulation—highlighted sustained intellectual-property investment essential for premium differentiation.

Niche vendors targeted software-only models that employ open-source SDRs, appealing to budget-constrained academia and start-ups. Competitive pressure encouraged full-stack solution bundles pairing simulators with record-and-playback analyzers, GNSS/inertial integration toolkits, and cloud-hosted analytics dashboards. White-space opportunities remain in maritime autonomous surface vessels and urban air mobility corridors, where high-dynamics testing is still nascent.

GNSS Simulators Industry Leaders

Spirent Communications

Rhode & Schwarz

Orolia

VIAVI Solutions

Hexagon AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Hexagon completed the acquisitions of the Geomagic software suite and Septentrio NV, incurring transaction costs of 40 MEUR.

- March 2025: Safran Federal Systems unveiled a CMOSS-compliant C-PNT card supporting GNSS, AltNav, LEO, and M-Code signals at the AUSA Global Force Symposium.

- January 2025: Quectel Wireless Solutions introduced the YEGN103W8A active multi-band GNSS antenna at CES 2025, enhancing precision for IoT devices.

- December 2024: VIAVI Solutions acquired Inertial Labs for USD 150 million, adding USD 50 million to projected 2025 revenue.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the GNSS simulators market as the sale of hardware and software systems that recreate multi-constellation satellite signals, GPS, Galileo, GLONASS, BeiDou, QZSS, and similar, in a laboratory or production setting so engineers can test receivers under repeatable orbital, atmospheric, and interference conditions.

Scope Exclusion: Signal generators that output a single fixed-frequency GPS tone without satellite motion modeling are not covered.

Segmentation Overview

- By Component

- Hardware

- Software

- By Type

- Single Channel

- Multichannel

- By GNSS Receiver

- GPS

- Galileo

- Glonass

- Beidou

- By Application

- Navigation

- Mapping

- Surveying

- Location-Based Services

- Vehicle Assistance Systems

- Others

- By Industry Vertical

- Military & Defense

- Automotive

- Consumer Electronics

- Marine

- Aerospace

- Geography***

- North America

- United States

- Canada

- Europe

- Germany

- United Kingdom

- France

- Spain

- Asia

- India

- China

- Japan

- Australia and New Zealand

- Latin America

- Brazil

- Argentina

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed hardware designers, validation managers, and program leads across North America, Europe, and Asia-Pacific to verify price bands, channel preferences, and emerging use cases (for example, automotive hardware-in-the-loop). Follow-up surveys with aerospace and defense integrators helped us adjust adoption curves and refine growth triggers flagged during desk work.

Desk Research

We gathered foundational data from open sources such as the International GNSS Service, the US National Space-Based PNT Office, the European Union Space Program Agency, and standards documents from RTCA and ETSI, which describe required accuracy envelopes for navigation devices. Trade statistics from UN Comtrade and Volza helped us approximate global shipments of navigation test equipment, while defense budget line-items available through SIPRI illustrated military procurement appetite. Company 10-Ks, investor decks, and peer-reviewed articles on spoofing mitigation rounded out technology and pricing insights.

Complementing public material, Mordor analysts drew selectively on D&B Hoovers for vendor revenues and Dow Jones Factiva for deal flow, creating a time series of addressable demand. Numerous additional secondary references informed granular checks, yet the list above is not exhaustive.

Market-Sizing & Forecasting

A top-down demand-pool build rooted in new receiver production, satellite launches, and defense test hours establishes annual spending. Results are then cross-checked with selective bottom-up roll-ups of leading suppliers' GNSS simulator sales and sampled average selling prices to reconcile gaps. Key variables include: (1) average simulator ASP, (2) annual GNSS receiver shipments, (3) defense procurement outlay for positioning test gear, (4) volume of autonomous vehicle development programs, and (5) satellite constellation expansion rate. Forecasts through 2030 rely on multivariate regression coupled with scenario analysis that accounts for regulatory pushes on anti-jamming compliance. Assumption shortfalls inside the bottom-up layer are bridged by regional channel check ratios agreed with industry respondents.

Data Validation & Update Cycle

Before sign-off, our analysts run variance checks against historical import data, public earnings, and independent traffic from bestsellingcarsblog style demand proxies. An internal senior review follows, and the model is refreshed each year, with interim revisions when material events, say, a major constellation outage, shift demand.

Why Mordor's GNSS Simulators Baseline Commands Reliability

Published estimates differ because firms choose dissimilar scopes, pricing corridors, and update cadences. According to Mordor Intelligence, clarity around what constitutes a "true" simulator and how multi-frequency capability is priced is vital.

Key gap drivers include broader "all simulators" grouping used by some providers, conservative ASP assumptions that ignore recent inflation in RF component costs, or, conversely, aggressive growth paths that hinge on unverified mass-market automotive uptake. Our annual refresh and mixed top-down/bottom-up crosswalk keep totals grounded in observable metrics.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 212 M (2025) | Mordor Intelligence | - |

| USD 224.6 M (2024) | Global Consultancy A | Includes calibration signal generators; uses static five-year CAGR without primary checks |

| USD 189.1 M (2024) | Industry Research Firm B | Applies lower ASP drawn from legacy single-channel products |

| USD 210.4 M (2025) | Regional Consultancy C | Omits software-only licensing revenue and refreshes biennially |

The comparison shows that while totals cluster, deviations arise from scope stretch, product mix, and update frequency. Mordor's disciplined variable selection, yearly model audit, and transparent assumptions give decision-makers a dependable, repeatable baseline.

Key Questions Answered in the Report

What is the current size of the GNSS simulators market?

The GNSS simulators market was valued at USD 233.69 million in 2026 and is projected to reach USD 380.52 million by 2031.

Which component segment is growing fastest?

Software licenses and SDR add-ons are expanding at a 14.12% CAGR thanks to lower entry costs and quick update cycles.

Why are wavefront simulators important?

Wavefront or CRPA simulators replicate spatial signal characteristics, enabling anti-jamming validation critical for defense and high-autonomy automotive systems.

Which region will see the strongest growth by 2031?

Asia-Pacific is forecast to record a 12.64% CAGR, driven by the scale-up of BeiDou applications and new regulatory standards in China and India.

How do high capital costs affect market adoption?

The price of high-channel simulators restricts uptake among small labs; this restraint subtracts 1.6 percentage points from the forecast CAGR.

What role does the automotive sector play in future demand?

Automotive and autonomous-vehicle applications are projected to grow at an 17.39% CAGR, challenging military dominance and driving investment in integrated HIL test frameworks.

Page last updated on: