Customer Information System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

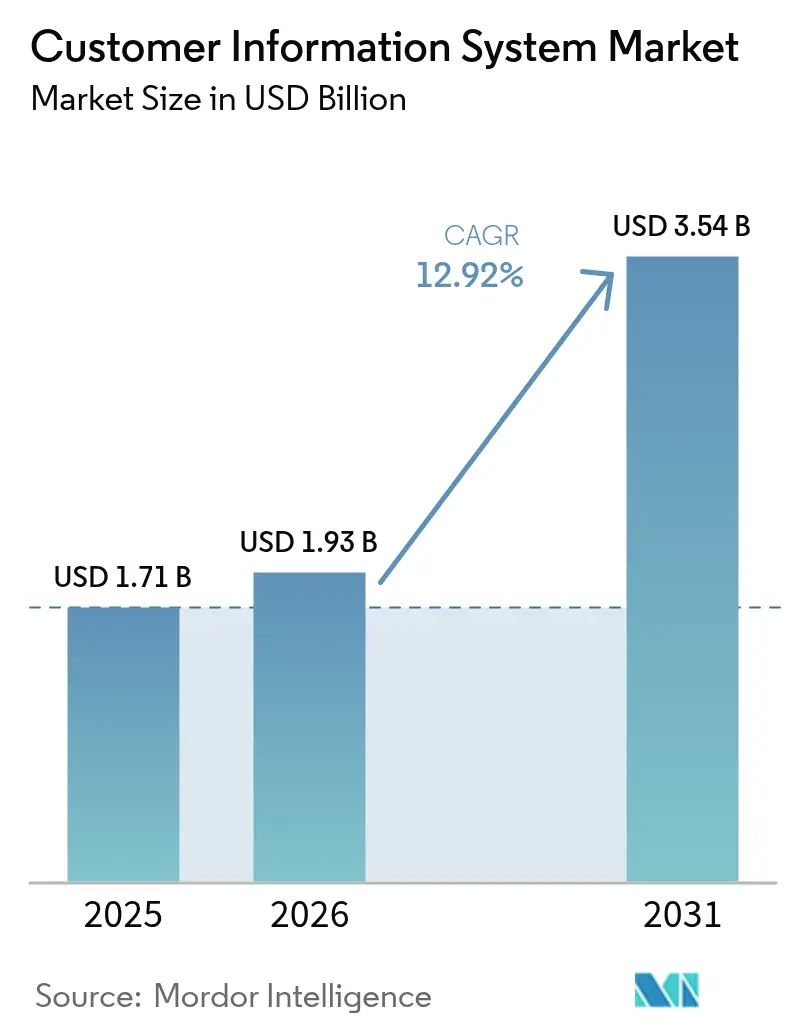

| Market Size (2026) | USD 1.93 Billion |

| Market Size (2031) | USD 3.54 Billion |

| Growth Rate (2026 - 2031) | 12.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

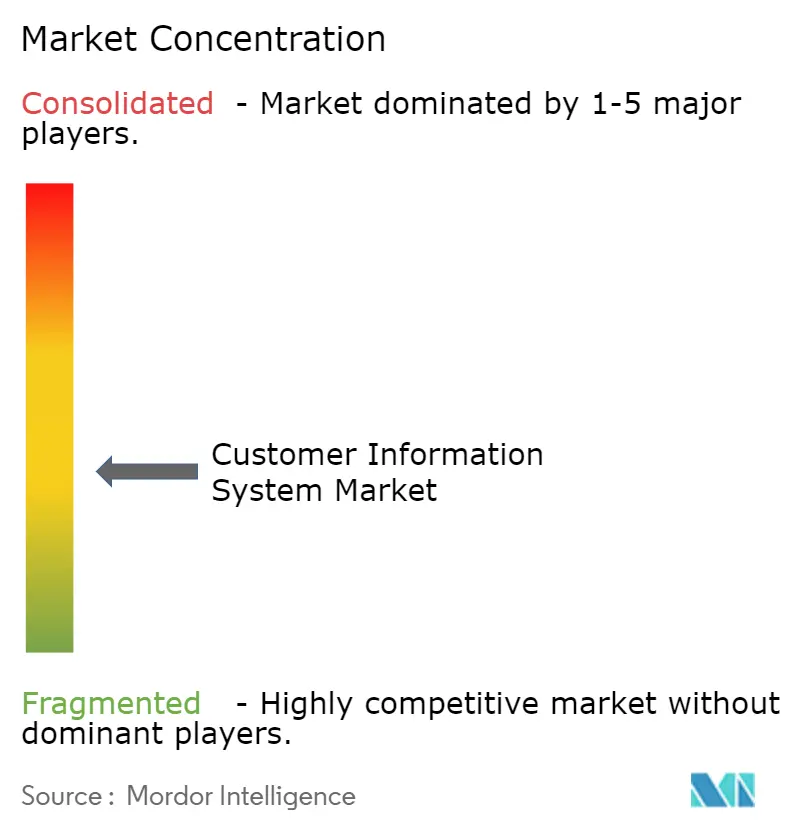

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Customer Information System Market Analysis by Mordor Intelligence

The customer information system market size is expected to grow from USD 1.71 billion in 2025 to USD 1.93 billion in 2026 and is forecast to reach USD 3.54 billion by 2031 at 12.92% CAGR over 2026-2031. Demand is rising because utilities view CIS platforms as the digital core that links metering, billing, and customer engagement. Cloud-native architectures are changing buying behavior, and cloud deployment is projected to expand 18.6% annually to 2030, noticeably faster than the overall customer information system market. Utilities are also deploying CIS to support real-time analytics for distributed energy resources, prepaid billing, and new regulatory mandates on billing accuracy.[1]Southern California Gas Company, “Customer Information System Replacement Program Testimony,” socalgas.com This evolution is occurring in parallel with cost-conscious migration strategies designed to move away from heavily customized, on-premises software without jeopardizing service continuity.

Key Report Takeaways

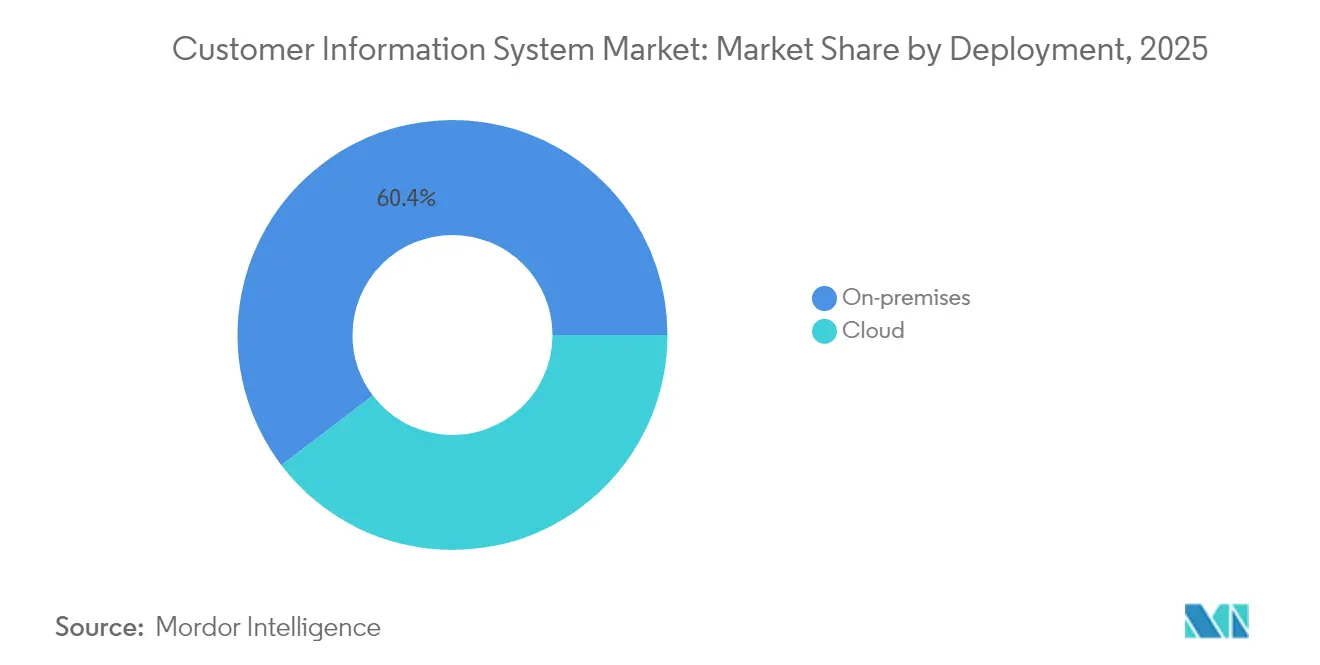

- By deployment, on-premises installations held 60.35% of customer information system market share in 2025, yet cloud models are projected to clock an 18.05% CAGR through 2031.

- By component, solutions commanded 69.85% revenue share of the customer information system market size in 2025, whereas services are forecast to expand at a 14.52% CAGR to 2031.

- By end-user, the energy and utilities segment accounted for 44.78% of the customer information system market size in 2025; retail CRM is expected to post the fastest 16.11% CAGR between 2026-2031.

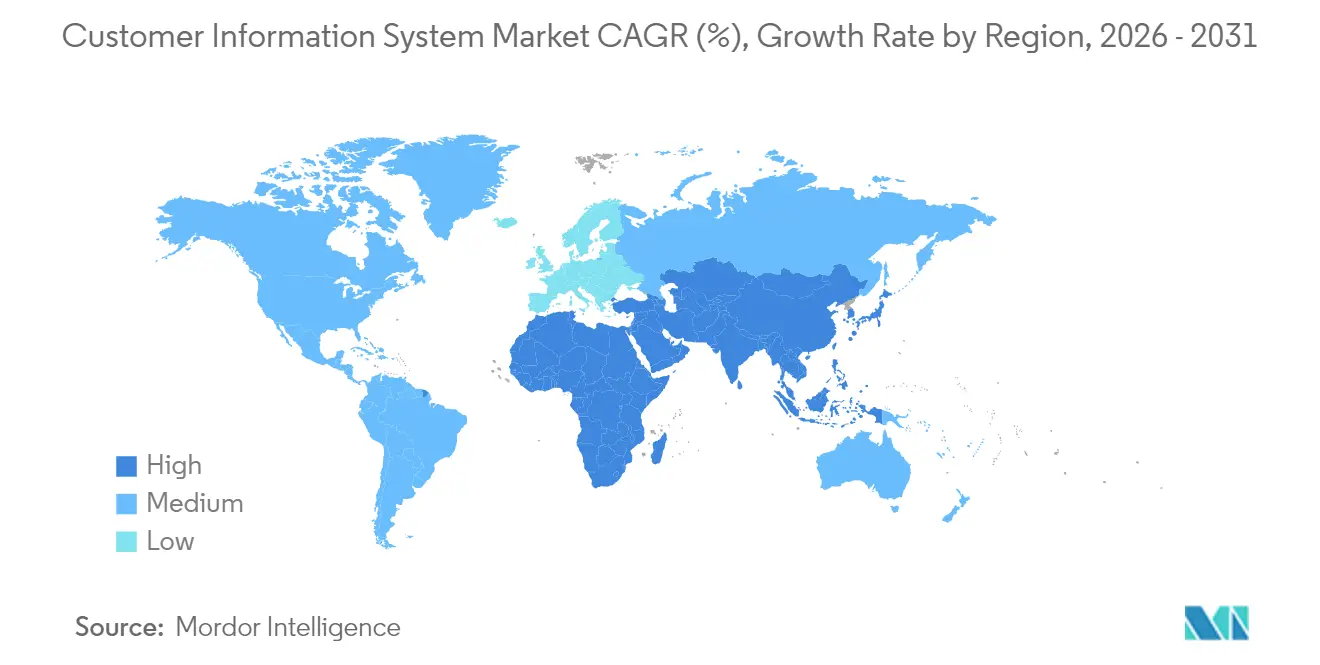

- By geography, North America led with 34.22% of customer information system market share in 2025, while Asia-Pacific is set to grow at a 15.23% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Customer Information System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital transformation initiatives by utilities | +3.50% | North America, spillover to Europe | Medium term (2-4 years) |

| Real-time customer analytics tied to DER growth | +2.80% | Global, early moves in North America and Europe | Long term (≥4 years) |

| Regulatory mandates for billing accuracy | +2.10% | Europe, influence in North America | Medium term (2-4 years) |

| CIS–AMI integration momentum | +1.90% | Asia-Pacific, spillover to MEA | Medium term (2-4 years) |

| Cloud-native CIS adoption by mid-sized utilities | +1.40% | Global, stronger in North America | Short term (≤2 years) |

| Flexible and prepaid billing in emerging markets | +1.20% | South America, Asia-Pacific, MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital Transformation Initiatives by Utilities

North American utilities are embedding CIS modernization into broader digital transformation roadmaps to lift customer experience and unlock operational efficiencies. Enhanced self-service portals, integrated workflow engines, and cross-channel communications enable utilities to orchestrate data, assets, and people in real time. Program success is evident in cases where utilities simultaneously raised renewable penetration and customer satisfaction, showing that a next-generation CIS can underpin both sustainability and service goals. Budget allocations increasingly favor modular upgrades that replace billing engines first, then layer on analytics and mobility features to spread capital costs while accelerating benefits.

Real-Time Customer Analytics Demand with DER Growth

As rooftop solar, battery storage, and electric vehicles proliferate, utilities need minute-level insights to balance the grid and engage prosumers. Modern CIS platforms process smart-meter streams, match them to tariff engines, and feed demand-response algorithms that create value for both the grid and end customers. Real-time settlement also underpins new compensation schemes for virtual power plants, tying CIS enrollment records to wholesale-market participation. Utilities adopting AI-enabled CIS modules report tangible improvements in call-center efficiency and lower truck rolls, demonstrating how analytics deliver bottom-line results while meeting rising consumer expectations.

Regulatory Mandates for Billing Accuracy

European directives now obligate utilities to issue timely, transparent bills and disclose consumption data each year. Compliance requirements trigger CIS upgrades capable of handling interval data, complex tariffs, and instant payment flows. Utilities must also reconcile regulatory asset bases and rate-of-return calculations inside billing engines to meet auditing standards.[2]Council of European Energy Regulators, “Report on Regulatory Asset Base and WACC,” ceer.eu The drive for accuracy expands CIS functionality from invoice creation to full revenue-assurance analytics, ensuring discrepancies are flagged before bills reach consumers. Implementation timelines align with upcoming reporting deadlines, making CIS projects a regulatory priority across the continent.

CIS-AMI Integration Momentum

Rapid smart-meter rollouts across Asia are pressuring utilities to couple AMI data with CIS workflows. Successful integrations route multi-protocol meter reads through edge gateways and IoT hubs before landing in the CIS for validation and billing. Utilities using unified CIS-AMI stacks can detect tampering faster, reduce technical losses, and offer usage alerts via mobile apps.[3]World Bank, “Power Sector Reforms and Smart Metering Progress,” worldbank.org Countries tackling high aggregate technical and commercial losses view integrated CIS as a strategic asset, helping utilities regain revenue while improving service reliability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High legacy migration costs for large utilities | -2.30% | Global, higher in North America and Europe | Medium term (2-4 years) |

| Data privacy and sovereignty concerns | -1.80% | Global, strongest in Europe | Long term (≥4 years) |

| Utility-specific IT-talent shortage | -1.20% | Asia-Pacific, MEA, South America | Medium term (2-4 years) |

| Vendor lock-in risks limiting flexibility | -0.90% | Global | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Legacy Migration Costs for Large Utilities

Replacing decades-old, heavily customized CIS installations demands parallel operations, rigorous data cleansing, and complex system integration. Capital programs exceeding USD 200 million highlight the financial hurdle; operating budgets also rise due to dual-running environments during cut-overs. Large utilities therefore phase projects, starting with low-risk billing territories while building reusable migration runbooks to reduce later waves’ costs.

Data Privacy and Sovereignty Concerns

Utilities managing critical infrastructure must protect personal and consumption data under an expanding patchwork of regional laws. Requirements for data residency, encryption, and sovereign-cloud hosting complicate multinational CIS rollouts, elongating vendor evaluations and increasing legal costs.[4]Rackspace, “Navigating Data Sovereignty Challenges,” rackspace.com Providers respond with regional data centers, configurable retention policies, and audit-ready security controls, but utilities still face ongoing obligations as regulations evolve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud adoption outpaces on-premises reliance

On-premises systems retained 60.35% of customer information system market share in 2025 as many large utilities value direct control and established integrations. Yet the customer information system market size for cloud deployments is projected to surge at an 18.05% CAGR, reflecting mid-sized utilities’ drive for agility and cost transparency. Utilities linking cloud CIS with modern CRM and workforce-management tools report faster product launches and fewer unplanned outages, reinforcing cloud’s business case.

Accelerated cloud take-up stems from elastic processing for bill calculations, reduced hardware refresh cycles, and embedded disaster recovery. Financial accounting rules letting cloud fees qualify as operating expense further sweeten adoption, especially in rate-regulated markets where capital budgets are tightly scrutinized. Utilities aiming to future-proof investments increasingly pursue hybrid models-maintaining critical data on-premises while shifting non-sensitive workloads to the cloud-to balance sovereignty and innovation.

By Component: Services momentum grows amid solution dominance

Solutions captured 69.85% of customer information system market revenue in 2025 and remain the foundation of billing, payment, and customer-engagement processes. Vendors are embedding AI chatbots and advanced analytics to personalize interactions, automate reconciliation, and streamline rate design. The customer information system industry nevertheless sees services rising 14.52% per year as utilities seek migration, integration, and managed-service expertise.

Skills shortages spur outsourcing of data conversion, security hardening, and compliance reporting, giving rise to multi-year managed-service contracts that guarantee service-level outcomes. Advisory firms specializing in CIS-AMI convergence design integration blueprints that limit risk and accelerate payback. As customer expectations shift toward digital self-service, utilities increasingly rely on external partners for continuous UX enhancements, refreshing portals every few months instead of multi-year cycles.

By End-User: Utilities retain top share while retail CRM accelerates

Energy and utilities represented 44.78% of customer information system market size in 2025 due to complex tariff structures, regulated billing rules, and the need to process vast smart-meter datasets. Electricity distribution utilities dominate spending, but water utilities now add CIS modules that track consumption anomalies and automate leak notifications.

Retailers are expected to post a 16.11% CAGR to 2031, making them the fastest-growing users of CIS-style CRM capabilities. Omni-channel commerce demands single views of customer transactions, prompting retailers to adopt CIS engines that synchronize product, inventory, and promotion data in near real time. Telecommunications and BFSI organizations trail but adopt similar functionality for usage-based charging and micro-service bundling.

Geography Analysis

North America accounted for 34.22% of customer information system market revenue in 2025. Early AMI penetration coupled with stringent billing-accuracy mandates sustains ongoing investment, while virtual power plant pilots require CIS enrollment workflows and near-real-time settlement. Utilities in the region actively integrate chatbots and self-service apps to deflect calls and raise customer-satisfaction metrics. High migration costs and privacy obligations temper project pace, leading many operators to adopt phased cut-over plans.

Asia-Pacific is forecast to expand at a 15.23% CAGR, the fastest of any region, as utilities pair mass smart-meter rollouts with CIS upgrades that support time-of-use tariffs and prepaid functions. National programs to curb technical and commercial losses make meter-to-cash modernization a priority, while rising middle-class expectations boost demand for digital service channels. Regional talent shortages encourage outsourcing, creating opportunities for system integrators offering turnkey CIS-AMI solutions.

Europe’s customer information system market is shaped by regulation that compels transparent invoicing, instant payments, and rigorous cybersecurity. Utilities align CIS investment schedules with annual reporting deadlines to avoid penalties. Demand-side response directives encourage flexible billing, necessitating engines that manage granular time-block tariffs. Meanwhile, emerging economies in South America and the Middle East and Africa deploy CIS to support prepaid electricity and water programs, improving revenue collection and broadening access.

Europe represents a significant market for customer information systems, demonstrating robust growth with approximately 9.85% CAGR from 2020 to 2025. The United Kingdom, Germany, France, and Spain are the key countries driving regional market growth. The region's market is characterized by increasing environmental concerns and favorable government policies supporting digital transformation initiatives. European utilities are increasingly focusing on modernizing their customer operations through advanced CIS solutions that combine billing, customer care, and uniform metering with the advantages of a common database and technological stack. The market is witnessing a significant shift towards cloud-based solutions, with many vendors developing mobile applications to offer energy insights and enhanced customer engagement. The region's strong emphasis on data privacy and security regulations has led to the development of more sophisticated and compliant CIS solutions. The integration of renewable energy sources and smart grid technologies has created new opportunities for CIS providers to develop more advanced and flexible solutions.

The Asia Pacific region is emerging as a high-growth market for customer information systems, with a projected CAGR of approximately 13.92% from 2025 to 2030. The market dynamics in this region are shaped by rapid urbanization, population growth, and increasing investments in utility infrastructure modernization. China and India are the primary growth drivers, with both countries making significant investments in smart grid technologies and digital transformation initiatives. The region is witnessing a notable shift from legacy systems to advanced CIS solutions, particularly in the electricity and power supply sectors. The increasing adoption of smart meters and advanced metering infrastructure is creating new opportunities for CIS solution providers. The market is also benefiting from various government initiatives promoting digital transformation and smart city development. The region's utilities are increasingly focusing on improving customer experience through automated billing processes and enhanced customer engagement platforms. The growing emphasis on reducing transmission and distribution losses is driving the adoption of sophisticated CIS solutions.

The Latin American market for customer information systems is experiencing steady growth, driven by the increasing need to modernize aging power grid infrastructure and enhance customer service capabilities. The region's utilities are focusing on implementing advanced and automated systems to optimize their billing capabilities, manage distribution networks in real-time, and provide consumers with enhanced data accessibility. The market is characterized by growing investments in smart city projects and digital transformation initiatives across major economies. Governments across the region are allocating budgets to modernize existing cities and establish new smart city projects to improve the overall economy. The support from governments is also driving the adoption of technologies supporting the operations of smart grids and systems. The region's utilities are increasingly recognizing the importance of digital engagement channels and customer self-service platforms to improve operational efficiency and customer satisfaction.

The Middle East and Africa region presents unique opportunities for customer information system providers, driven by the increasing focus on energy conservation and expanding deployment of smart grid technologies. The Middle Eastern region, largely an oil-based economy, is witnessing significant investments in commercial, residential, and industrial projects that require energy-efficient and accurate meter solutions. Government initiatives and policies connected with smart meter deployment are creating favorable conditions for market growth. In Africa, the market is driven by the growing need to improve utility infrastructure and reduce non-technical losses. The region is witnessing increasing adoption of smart metering solutions, particularly in urban areas. The market is also benefiting from various digital transformation initiatives aimed at improving utility operations and customer service delivery. The integration of renewable energy sources and the need for efficient billing systems are creating new opportunities for CIS solution providers in the region.

Competitive Landscape

The customer information system market features moderate concentration: global enterprise vendors such as Oracle, SAP, and IBM compete with utility-focused specialists including Fluentgrid, Gentrack, Hansen Technologies, Vertex One, and Open Smartflex. Enterprise providers leverage deep R&D budgets and adjacent ERP suites, appealing to large multi-service utilities seeking platform consistency. Specialized vendors win projects by offering configurable templates tailored to electric, water, and gas workflows, reducing deployment times for mid-sized operators.

Strategic differentiation now centers on cloud readiness, AI-driven insights, and composable architectures that avoid vendor lock-in. Vendors roll out micro-services and open APIs so utilities can swap modules without rewriting core code. Flexible pricing models based on customer count or transaction volume align vendor revenue with utility growth, further influencing selection criteria.

Utilities evaluating suppliers weigh product maturity, cybersecurity certifications, and demonstrated migration frameworks. Reference projects involving large meter counts, successful legacy data conversion, and proven regulatory compliance often tilt awards. As distributed energy resources proliferate, suppliers able to reconcile behind-the-meter generation in billing engines gain further competitive edge.

Customer Information System Industry Leaders

Oracle Corporation

IBM Corporation

SAP SE

Gentrack Group Limited

Itineris NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: L.A. Care Health Plan approved USD 50 million for workforce development and modernized claims analytics through new electronic-data-interchange contracts, demonstrating healthcare adoption of CIS-style platforms.

- April 2025: Germany’s Federal Ministry for Economic Affairs and Climate Action highlighted EUR 428 million (USD 504.08 million) in funding for Multi-Provider Cloud-Edge Continuum projects that strengthen European cloud interoperability.

- March 2025: Guidance for the AMI 2.0 era outlined steps to improve interoperability, performance-based contracting, and transparent benefit cases during metering and CIS upgrades.

Global Customer Information System Market Report Scope

The Customer Information System (CIS) is a system used by an organization to assist employees in obtaining customer information efficiently. CIS technology is helping utilities to efficiently gather and manage customer information, improve systems operations, support marketing initiatives, and provide flexible billing of services and multiple commodities.

The Customer Information System Market is segmented by Deployment (Cloud, On-Premises), Component (Solutions, Services), End-User (End User by CRM (BFSI, Retail, Telecommunication), and End User by CIS (Water and Wastewater Management, Energy and Utility)), and Geography (North America, Europe, Asia-Pacific, Latin America, and Middle & Africa). The market sizes and forecasts are provided in value (USD million) for all the above segments.

The Customer Information System (CIS) market is registering a CAGR of 12.3 % during the forecasted period.

| Cloud |

| On-Premises |

| Solutions |

| Services |

| CRM | BFSI |

| Retail | |

| Telecommunications | |

| CIS | Water and Wastewater Management |

| Energy and Utilities | |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Deployment | Cloud | |

| On-Premises | ||

| By Component | Solutions | |

| Services | ||

| By End-User | CRM | BFSI |

| Retail | ||

| Telecommunications | ||

| CIS | Water and Wastewater Management | |

| Energy and Utilities | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the customer information system market?

The market is valued at USD 1.93 billion in 2026 and is projected to grow to USD 3.54 billion by 2031 on a 12.92% CAGR.

Which region leads the customer information system market?

North America holds the largest share at 34.22% thanks to early AMI adoption and strict billing-accuracy mandates.

Why are utilities shifting to cloud-based CIS?

Cloud deployment offers faster implementation, elastic processing, and OpEx-friendly pricing, supporting an 18.05% CAGR for cloud CIS through 2031.

What segment will grow fastest through 2031?

Retail CRM applications are expected to expand at a 16.11% CAGR as retailers leverage CIS engines for omnichannel personalization.

How do legacy migration costs affect CIS projects?

Large utilities may face capital programs over USD 200 million and dual-running expenses, making phased migrations and managed services attractive mitigation tactics.

What is driving CIS investment in Asia-Pacific?

Rapid smart-meter rollouts and CIS–AMI integration to curb technical losses propel a forecast 15.23% CAGR in the region.

Page last updated on: