SIP Trunking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

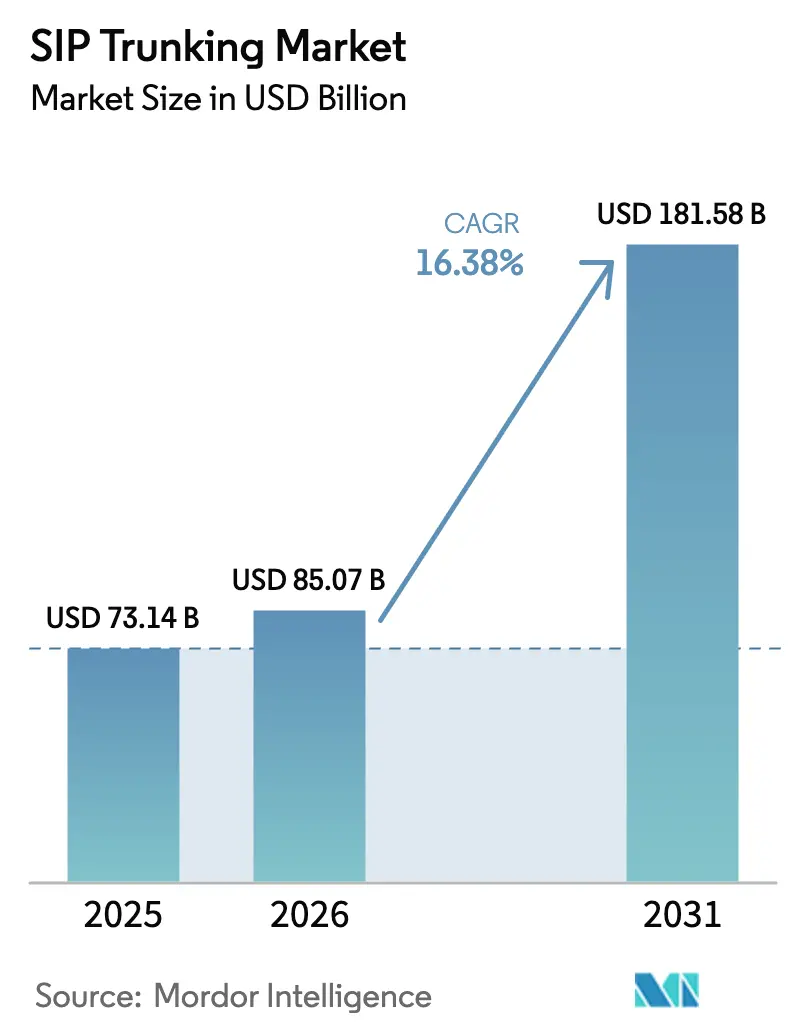

| Market Size (2026) | USD 85.07 Billion |

| Market Size (2031) | USD 181.58 Billion |

| Growth Rate (2026 - 2031) | 16.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

SIP Trunking Market Analysis by Mordor Intelligence

The SIP trunking market size is expected to grow from USD 73.14 billion in 2025 to USD 85.07 billion in 2026 and is forecast to reach USD 181.58 billion by 2031 at 16.38% CAGR over 2026-2031. The current expansion reflects enterprises’ shift toward Internet-Protocol voice services, rising PSTN decommissioning mandates, and bundling with unified-communications platforms. Cost savings between 25% and 65% over legacy PRI lines continue to be the single strongest economic pull, especially for high-volume, multi-site users[1]Ryan Daily, “Why Businesses Are Moving to SIP Trunking,” Telus, telus.com. Mature fiber networks, rapid 5G roll-outs, and cloud adoption by small firms reinforce demand momentum. At the same time, mounting fraud risks, inter-carrier fee revisions, and quality-of-service (QoS) concerns on public internet links temper near-term growth ambitions.

Key Report Takeaways

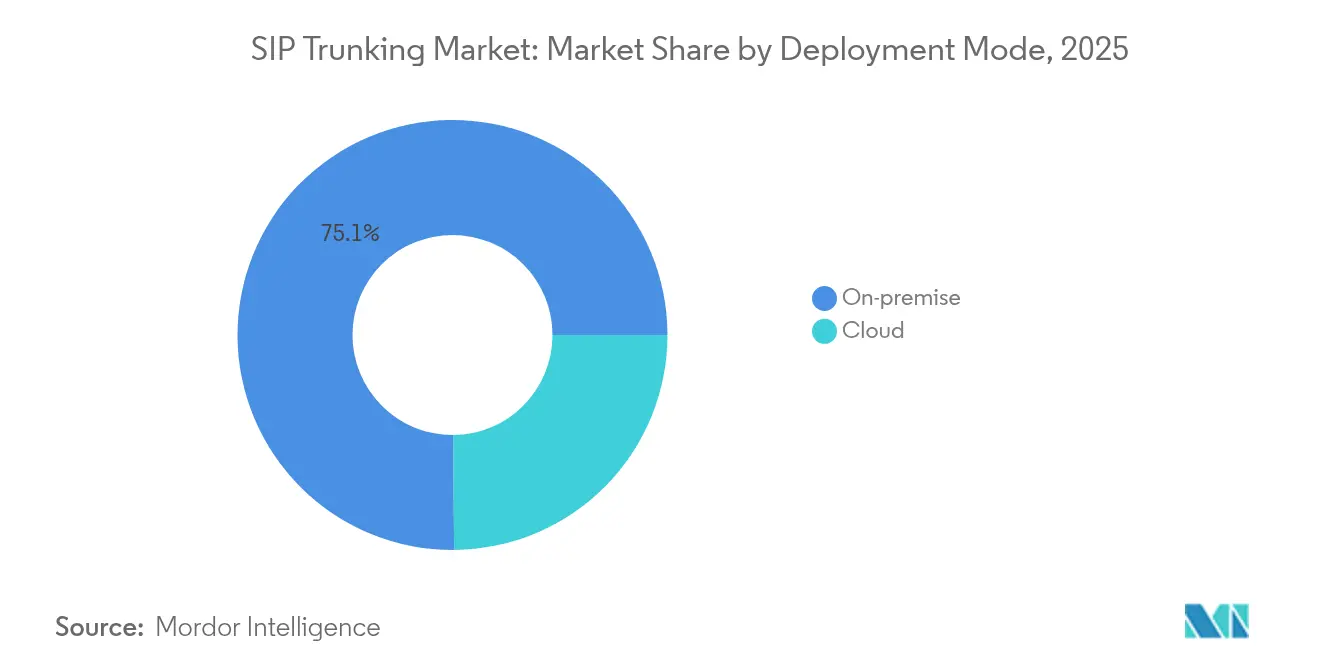

- By deployment mode, on-premise solutions held 75.12% of SIP trunking market share in 2025; cloud deployment is set to grow at a 15.05% CAGR to 2031.

- By organization size, large enterprises accounted for 60.41% share of the SIP trunking market size in 2025, while the SME segment is expanding at 15.12% CAGR.

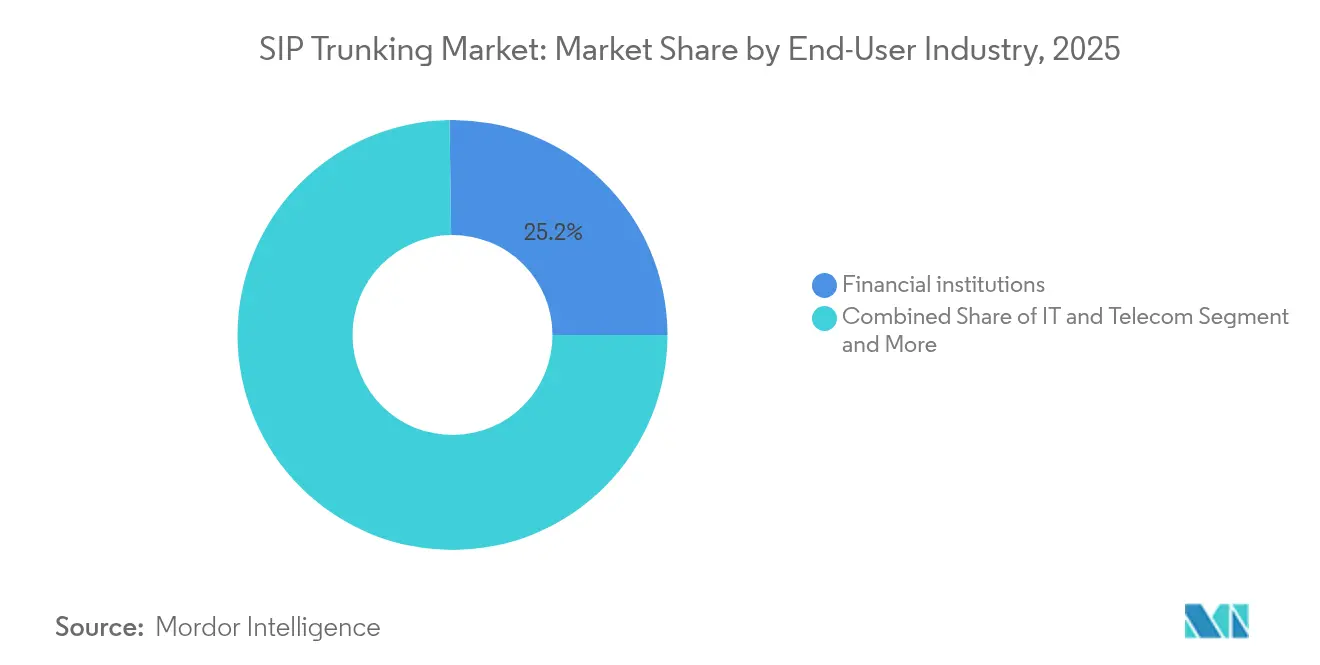

- By end-user industry, the BFSI sector led with 25.22% revenue share in 2025; healthcare is advancing at a 13.52% CAGR through 2031.

- By call type, domestic accounted for 62.35% share of the SIP trunking market size in 2025, while the International segment is expanding at 15.88% CAGR.

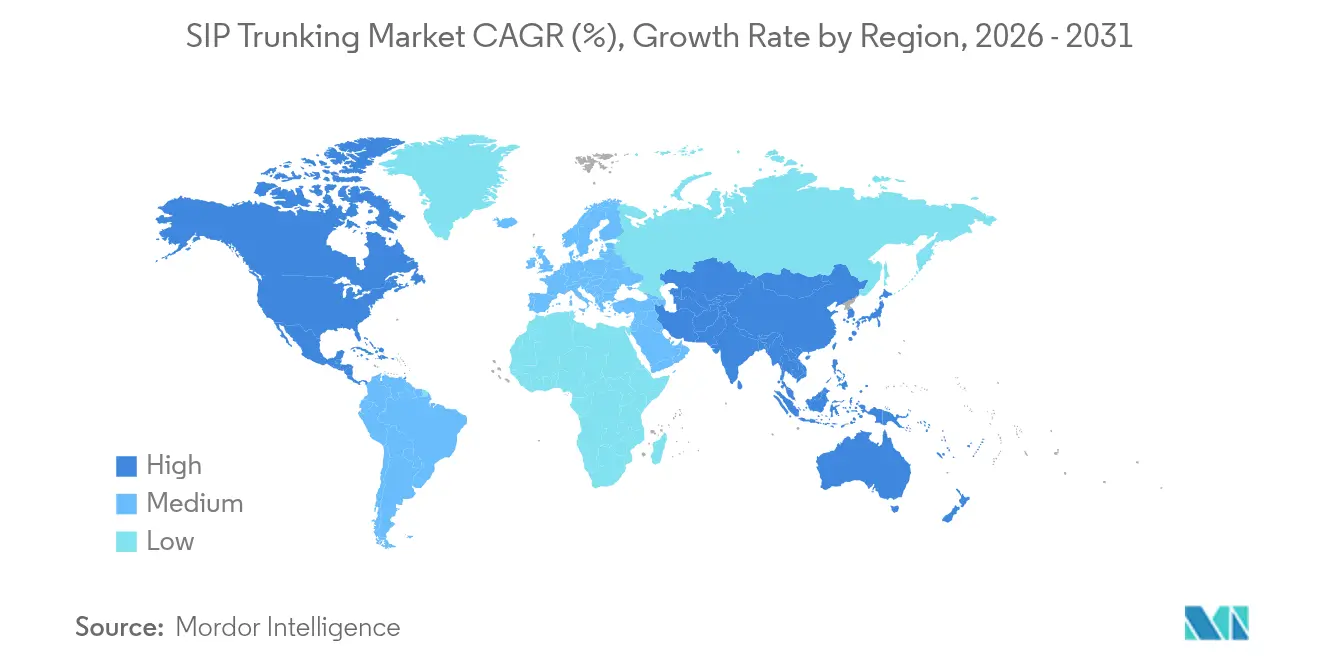

- By geography, North America commanded 62.15% of the SIP trunking market size in 2025; Asia-Pacific is forecast to grow at 16.27% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of SIP Trunking Market*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-efficiency versus legacy PRI/ISDN | +4.2% | Global, highest in North America and Europe | Medium term (2-4 years) |

| Demand for UCaaS bundling | +3.8% | Global, led by North America and Asia-Pacific | Short term (≤2 years) |

| Global PSTN switch-off deadlines | +3.1% | Global, with mandates in UK, Australia, Europe | Long term (≥4 years) |

| SME digitization in emerging markets | +2.7% | Asia-Pacific core, spill-over to Latin America and MEA | Medium term (2-4 years) |

| AI-optimised dynamic call routing | +1.9% | North America and Europe, expanding to Asia-Pacific | Short term (≤2 years) |

| 5G private-network voice interconnect needs | +1.5% | Global, early adoption in developed markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Cost-efficiency versus legacy PRI/ISDN

Enterprises migrating from Primary Rate Interface or ISDN circuits cite headline savings that often exceed 50% on international traffic because SIP lets voice ride on existing data bandwidth and eliminates duplicate access lines. When combined with AI-assisted least-cost routing, firms reclaim further gains by dynamically selecting the lowest-price carrier path for each call. The switch also frees teams from hardware lock-in, eases scalability, and reduces outage exposure tied to single-vendor PBXs.

Demand for UCaaS bundling

Unified-communications-as-a-service providers position SIP trunks as the anchor connectivity layer that allows businesses to merge voice, video, and messaging. The bundling model simplifies procurement and deepens vendor stickiness, particularly as firms roll out hybrid-work frameworks that require seamless hand-off between on-premise and cloud endpoints.

Global PSTN switch-off deadlines

- Regulators are shutting down copper lines on strict timelines. The UK extended its deadline to 2027, while European operators target full shut-off by 2030, forcing millions of legacy connections to migrate[2]Alexander Harrowell, “UK’s Full-Fibre Roll-Out and PSTN Switch-Off Pushed Back,” Computer Weekly, computerweekly.com. Carriers actively promote SIP trunks to avoid operating dual infrastructures, aligning cost incentives with compliance.

SME digitization in emerging markets

Asia-Pacific SMEs bypass legacy circuits altogether. For example, Jio Business markets low-entry SIP bundles that pair internet access with pay-as-you-grow channels, making enterprise-grade features affordable to first-time buyers[3]“SIP Trunking for Your Business,” Jio Business, jio.com.

Restraints Impact Analysis of SIP Trunking Market*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| QoS and jitter on public Internet paths | -2.1% | Global, especially developing regions | Short term (≤2 years) |

| SIP fraud and toll-bypass security risks | -1.8% | Global, highest where regulation is weak | Medium term (2-4 years) |

| Rising inter-carrier access fees in developing regions | -1.3% | Asia, Africa, Latin America | Long term (≥4 years) |

| Shortage of SIP-skilled engineers | -0.9% | Global, acute in high-growth markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

QoS and jitter on public Internet paths

Voice packets traveling over best-effort internet face sporadic latency spikes and packet loss, degrading call quality during peak-traffic windows. Enterprises mitigate the risk with dedicated internet access, multiple carriers, and session-border controllers, but these measures raise cost and complexity.

SIP fraud and toll-bypass security risks

Poorly secured trunks invite toll fraud that drained USD 9 billion worldwide in 2021, largely through SIP registration hijacking and international-rate abuse. Organizations now budget for encryption, multi-factor authentication, and 24 × 7 threat monitoring, elongating deployment cycles and tempering adoption among security-sensitive verticals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

SIP Trunking Market Segment Analysis

By Deployment Mode:

On-premise Dominance PersistsThe on-premise segment captured 75.12% of SIP trunking market share in 2025 because many enterprises are unwilling to relinquish physical control of voice traffic that intersects with regulated data. Retaining on-site PBXs lets them extend asset life and comply with audit requirements, while layering SIP connectivity for cost savings and inbound number flexibility.

Cloud deployment is the fastest riser, expanding at a 15.05% CAGR. SMEs gravitate toward fully managed trunks that eliminate server rooms, deliver instant scale, and include disaster-recovery fail-over—capabilities once reserved for Fortune 500 budgets. Hybrid architectures gain traction as mid-market firms keep a primary PBX in house yet direct branch-office or work-from-home calls to cloud SBCs, balancing security with agility.

By Organization Size:

Enterprise Hold with SME AccelerationLarge organizations commanded 60.41% of the SIP trunking market size in 2025 thanks to multi-site footprints, high call-volume savings, and integrations with CRM, contact-center, and workforce-management suites. Their deployments commonly feature geo-redundant SBC clusters and diverse carriers to meet five-nines uptime mandates.

SMEs, however, post a 15.12% CAGR as providers slash onboarding times to days and bundle trunks with broadband. In many emerging markets, SIP serves as first-generation voice rather than a migration step, letting smaller retailers, clinics, and service firms adopt auto-attendants and click-to-call analytics without CapEx.

By End-user Industry:

BFSI Leadership with Healthcare MomentumFinancial institutions led with 25.22% revenue share. They depend on call recording, trade-desk voice analytics, and strong encryption to meet MiFID II and Dodd-Frank record-keeping rules, making SIP the default backbone for omnichannel contact-center upgrades.

Healthcare is the quickest mover at 13.52% CAGR. Tele-consultations, appointment hotlines, and HIPAA-aligned encryption shape hospital demand, while SIP integration with electronic health-record systems provides automatic call logging for care-team coordination.

By Call Type:

Domestic Strength, International UpswingDomestic traffic formed the majority at 62.35% in 2025 as customer-service lines, intra-country supplier calls, and local compliance needs anchor day-to-day usage. QoS is easier to guarantee within a single national network, expediting migrations.

International calling is rising at 15.88% CAGR. SIP trunks tap least-cost routing that slices 40-70% off legacy tariffs and offer local inbound numbers in over 50 countries, a boon to exporters and remote-first software firms.

Geography Analysis

North America SIP Trunking Market

North America kept its leadership at 62.15% of the SIP trunking market size in 2025. Fiber saturation, proactive FCC backing for IP transitions, and service diversity among ATand T, Verizon, and Lumen anchor adoption. Canadian carriers such as Telus report double-digit trunk uptake across resource, retail, and public-sector clients.

Europe SIP Trunking Market

Europe follows as PSTN switch-off deadlines loom. Operators in Germany, France, and the Nordics accelerate marketing around SIP as a compliance pathway, with multinational enterprises demanding a single pane of glass for numbers across 27 member states. Local data-sovereignty rules prompt many firms to house SBCs on-premise, sustaining hardware revenues even as cloud traffic grows.

APAC SIP Trunking Market

Asia-Pacific is the fastest-growing territory at 16.27% CAGR through 2031. India and Indonesia leapfrog copper lines, installing SIP-ready fiber to micro-enterprises. Japan and South Korea showcase edge-AI routing that scales traffic during peak shopping seasons, while Australia’s completed PSTN sunset drives late-cycle equipment swaps. China’s 5G coverage provides low-latency underlay, letting factories extend SIP endpoints to IoT handhelds on industrial floors.

Competitive Landscape

Competition spans incumbent telcos, cloud-native communication-platform providers, and niche SIP specialists. Incumbents leverage nationwide fiber and regulatory mindshare to win large enterprises, bundling trunks with managed SD-WAN and mobile plans. Cloud entrants such as RingCentral and Twilio differentiate through open APIs, AI-driven call insights, and out-of-the-box CRM connectors, capturing SMEs and developers.

Strategic acquisitions continue. Alianza’s December 2024 purchase of Microsoft’s Metaswitch assets deepened its control of soft-switch technology and signals consolidation toward full-stack voice-platform ownership. Comcast Business moved for Nitel in April 2025, scooping fiber-access and SD-WAN clients that create cross-sell lanes for SIP services. Providers further invest in SBC analytics, AI fraud detection, and end-to-end encryption to justify premium pricing and stem commoditization risk.

Regional specialists focus on vertical compliance. In finance, vendors embed call-recording storage that meets seven-year retention policies. In healthcare, packages bundle HIPAA attestations and direct-secure-messaging gateways. Differentiators now center on security certifications and turnkey integrations rather than raw minutes rates.

SIP Trunking Industry Leaders

Lumen Technologies

AT&T Inc.

Verizon Communications Inc.

Twilio Inc.

Bandwidth Inc.

- *Disclaimer: Major Players sorted in no particular order

SIP Trunking Market Companies Covered in this Report

- Lumen Technologies (CenturyLink)

- AT&T Inc.

- Verizon Communications Inc.

- Twilio Inc.

- 8x8 Inc.

- RingCentral Inc.

- Bandwidth Inc.

- Vonage Holdings Corp.

- Broadvoice

- Nextiva Inc.

- Flowroute Inc.

- BT Group plc

- Sangoma Technologies Corp.

- Telnyx LLC

- Gamma Network Solutions Ltd.

- NTT Communications Corp.

- GTT Communications Inc.

- Ribbon Communications

- Allstream Inc.

- Cisco Systems Inc.

Recent Industry Developments in SIP Trunking Market

- May 2025: RingCentral reported Q1 2025 revenue of USD 612 million, achieved GAAP operating income of USD 10 million, and unveiled deeper integration with Salesforce Service Cloud Voice.

- April 2025: Comcast Business expanded its enterprise footprint by acquiring Nitel.

- December 2024: Alianza signed a definitive agreement to acquire Metaswitch from Microsoft.

- October 2024: Clarion Communications completed the acquisition of IPitomy Communications, adding 2,000 end-user customers.

SIP Trunking Market Report Scope and Research Methodology

Market Definition and Coverage

Our study views the SIP trunking market as the worldwide spend that enterprises, carriers, and public agencies commit each year to virtual "trunk" channels that link any IP-PBX or UC platform to the public switched telephone network via Session Initiation Protocol. These values capture set-up fees and recurring voice or fax traffic charges for on-premise, cloud, and hybrid trunks.

Scope exclusion: We exclude consumer over-the-top VoIP apps, wholesale inter-carrier minutes, and standalone UCaaS seat subscriptions.

Segments Covered in This Report

- By Deployment Mode

- Cloud

- On-premise

- By Organization Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By End-user Industry

- IT and Telecom

- BFSI

- Government

- Retail and E-commerce

- Healthcare

- Manufacturing

- Education

- Media and Entertainment

- Others

- By Call Type

- Domestic

- International

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- North America

Data Sources, Market Sizing, and Validation

Primary Research

We interviewed SIP service architects, procurement heads, SBC vendors, and Tier-1 carriers across North America, Europe, and Asia-Pacific. Their insights shaped uptake assumptions, verified regional price dispersion, and clarified the pace at which legacy PRI ports are replaced.

Desk Research

We drew baseline volume and revenue indicators from open sources such as ITU telecom statistics, FCC and Ofcom tariff filings, GSMA operator databases, Eurostat trade codes, and regional cloud-telephony association white papers. Company 10-Ks, carrier price lists, patent filings from Questel, and news flows in Dow Jones Factiva helped us size service adoption, average selling prices, and migration timelines. Our analysts also checked traffic data from NetNumber and spectrum auction records to benchmark trunk capacity build-outs. The sources cited above are illustrative; many others fed our desk review and cross-checks.

Market-Sizing & Forecasting

We start with a top-down construct that rebuilds the demand pool from business telephone lines in service. These are split by trunk penetration, channel density, and prevailing ASPs, which are then validated through selective bottom-up carrier revenue roll-ups and partner channel checks. Key model levers include copper-to-IP port conversion rates, hybrid-work seat growth, Teams Direct Routing licenses, SBC shipment trends, exchange-rate movements, and regulatory PSTN switch-off deadlines. Forecasts employ multivariate regression blended with scenario analysis to reflect macro cycles and tariff re-pricing windows; expert consensus gathered earlier guides variable trajectories. Gaps in bottom-up data are bridged by anchored price corridors and regional adoption proxies.

Data Validation & Update Cycle

Our team re-runs anomaly checks, compares outputs with external traffic benchmarks, and triggers re-contacts when variance exceeds preset thresholds. The model is refreshed annually, with mid-cycle updates when material events, such as spectrum auctions or major carrier mergers, shift market fundamentals.

How Mordor Intelligence's SIP Trunking Market Size Compares to Other Published Estimates

We acknowledge that published market values differ because research firms choose distinct scopes, price baskets, and refresh cadences.

Key gap drivers include whether cloud trunks are bundled with UCaaS, if international channels are priced at blended or list rates, and how quickly each analyst assumes PSTN switch-offs push enterprises to IP. Mordor's base case reports the full enterprise service stack, converts regional revenues at constant 2025 dollars, and applies a balanced cloud-migration slope vetted in quarterly carrier interviews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 73.14 B (2025) | Mordor Intelligence | - |

| USD 70.40 B (2024) | Global Consultancy A | Counts SMB voice access only, narrower call-type coverage |

| USD 54.20 B (2023) | Trade Journal B | Omits on-prem trunk upgrades and uses conservative cloud-adoption pace |

| USD 18.52 B (2025) | Regional Consultancy C | Measures revenue in North America only |

The comparison shows that when variables, geography, and service layers are aligned, our number sits at the midpoint of plausible ranges, giving decision-makers a transparent, repeatable baseline anchored to clearly documented inputs and steps.

Key Questions Answered in the Report

What is driving the rapid growth of the SIP trunking market?

Cost savings over PRI lines, mandated PSTN shutdowns, and the rise of UCaaS bundles are the core growth catalysts highlighted in this report.

Why do on-premise deployments still dominate despite cloud hype?

Enterprises with legacy PBX assets and strict compliance rules prefer on-site control, sustaining 75.12% share of deployments in 2025.

Which industry adopts SIP trunks the most today?

The BFSI sector leads with 25.22% revenue share because financial regulations require secure, recorded voice interactions.

How big is the opportunity in Asia-Pacific?

Asia-Pacific posts the fastest CAGR at 16.27% through 2031 as SMEs skip legacy circuits and tap 5G-ready SIP services.

What are the primary security risks with SIP trunking?

Toll fraud, SIP registration hijacking, and inadequate encryption can expose firms to millions in losses, making robust SBC and monitoring essential.

Is international call traffic significant?

Yes. While domestic calls hold 62.35% share today, international traffic is growing at 15.88% CAGR due to globalization and least-cost routing economics.

Page last updated on: