Correspondence Management System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

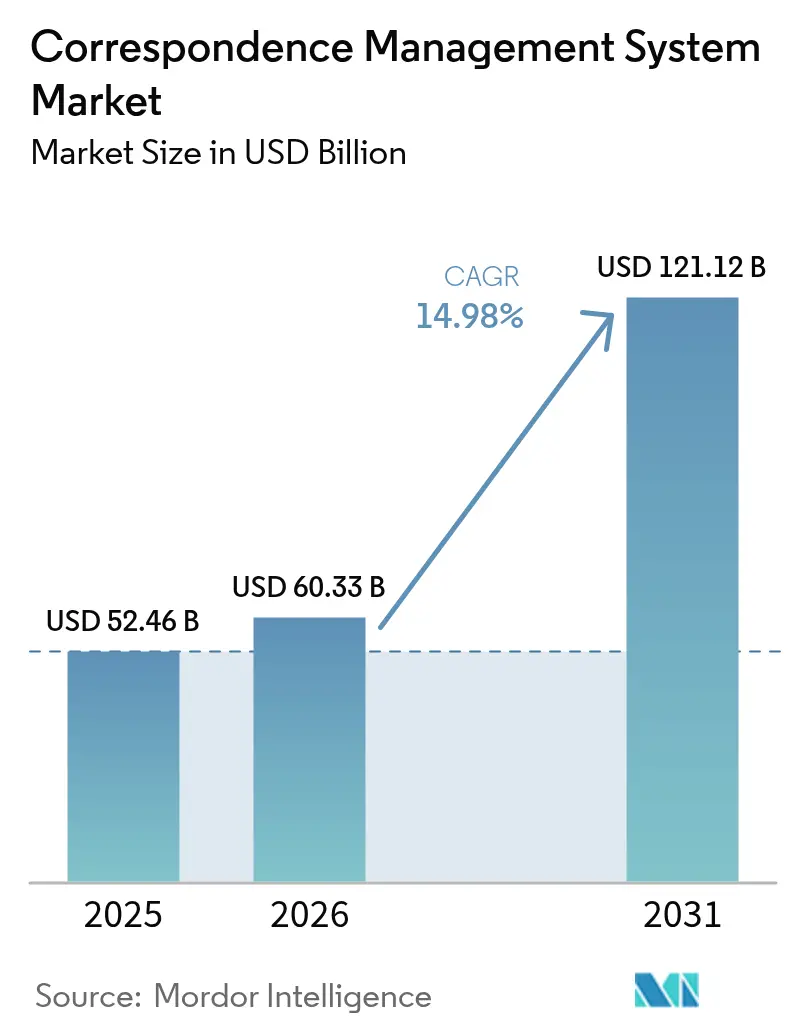

| Market Size (2026) | USD 60.33 Billion |

| Market Size (2031) | USD 121.12 Billion |

| Growth Rate (2026 - 2031) | 14.98% CAGR |

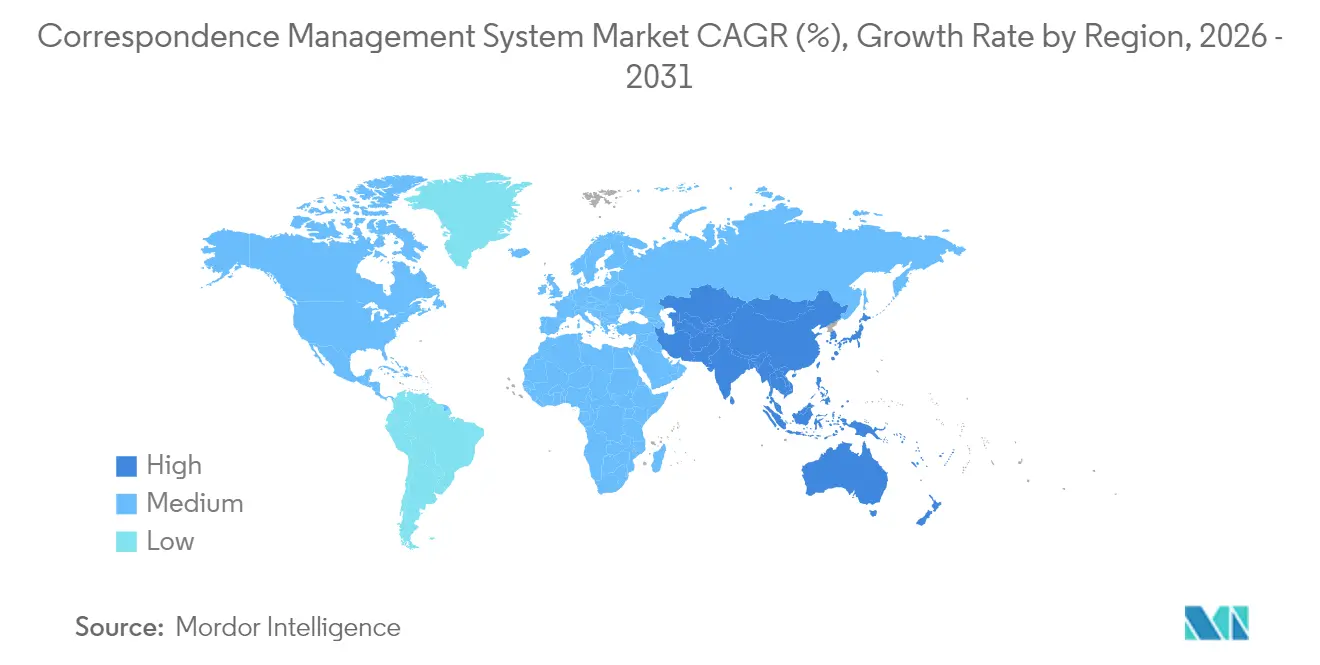

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Correspondence Management System Market Analysis by Mordor Intelligence

The correspondence management system market size is expected to grow from USD 52.46 billion in 2025 to USD 60.33 billion in 2026 and is forecast to reach USD 121.12 billion by 2031 at 14.98% CAGR over 2026-2031. Accelerated migration from batch-centric mail merges to real-time, context-aware orchestration underpins this lift, as organizations seek auditable, multi-channel communications that satisfy GDPR, HIPAA, and similar statutes. Regulatory rigor is dovetailing with omnichannel adoption; enterprises now balance email with SMS, RCS, chatbots, and print to optimize reach and cost. Cloud-native platforms dominate new deployments because hyperscalers deliver elastic compute, object storage, and API gateways that lower the total cost of ownership. Generative AI and low-code toolsets are shortening template-development cycles, while sentiment analytics help refine tone, timing, and channel in flight. Competitive pressure is rising as API-first entrants unbundle legacy suites into composable microservices, fragmenting vendor share and widening functionality gaps.

Key Report Takeaways

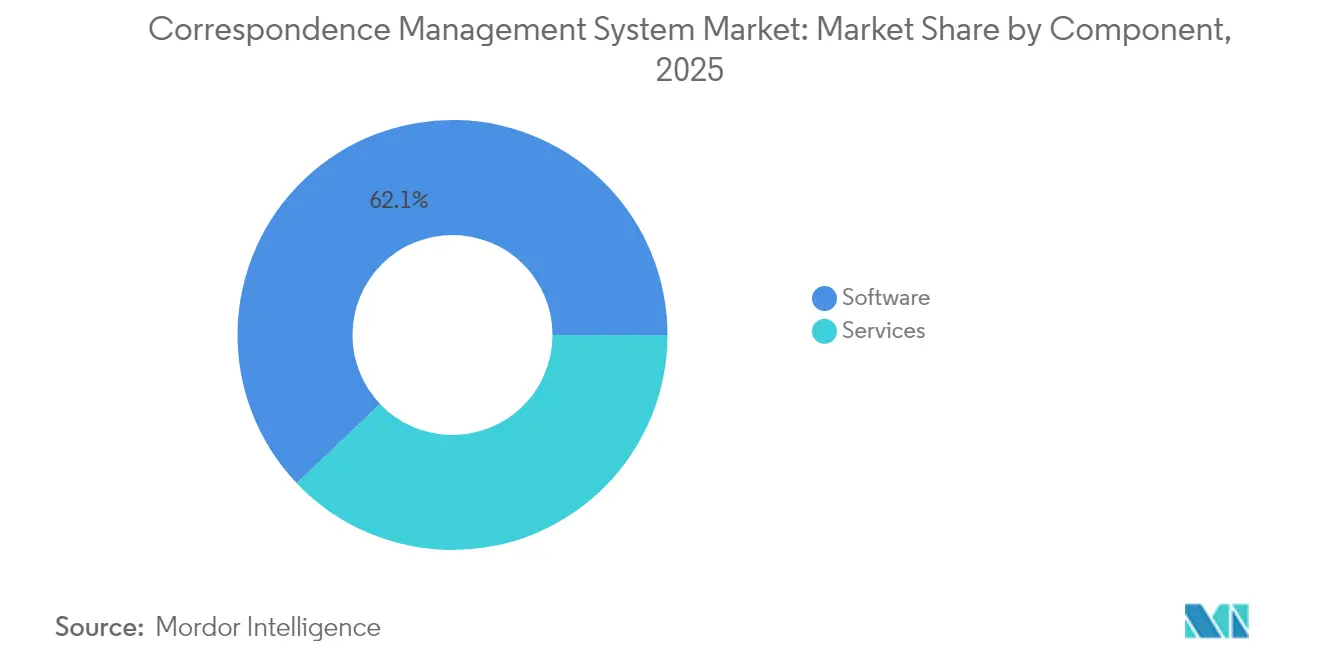

- By component, software led with 62.10% of correspondence management system market share in 2025; services are forecast to grow at a 16.18% CAGR through 2031.

- By delivery channel, web-based formats held 47.20% share of the correspondence management system market in 2025, while social and chatbot channels are advancing at a 15.89% CAGR through 2031.

- By deployment model, cloud configurations accounted for 68.05% share of the correspondence management system market in 2025, public-cloud setups are expanding at a 16.22% CAGR to 2031.

- By organization size, large enterprises captured 55.10% spending in 2025, whereas SMEs are set to rise at a 16.05% CAGR through 2031.

- By vertical, banking, financial services, and insurance commanded 25.40% revenue in 2025; healthcare and life sciences lead growth at a 15.55% CAGR.

- By geography, North America represented 35.30% share in 2025; Asia-Pacific is growing fastest at a 16.02% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Correspondence Management System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising need for automating and personalizing communication | +2.8% | Global, with peak adoption in North America and Western Europe | Medium term (2-4 years) |

| Adoption of cloud-native CCM platforms | +3.2% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Regulatory mandates for secure, auditable correspondence | +2.5% | North America, EU, with spillover to Asia-Pacific financial hubs | Long term (≥ 4 years) |

| Omnichannel engagement and digital transformation push | +2.1% | Global, accelerated in Asia-Pacific mobile-first markets | Medium term (2-4 years) |

| AI-driven sentiment analytics for real-time tailoring | +1.9% | North America, EU, select Asia-Pacific metros | Medium term (2-4 years) |

| Low-/no-code correspondence workflow enablement | +1.6% | Global, with faster uptake among SMEs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Need for Automating and Personalizing Communication

Enterprises are abandoning static mail-merge routines for dynamic engines that ingest real-time data, transaction histories, browsing behavior, and sentiment scores, to tailor message content and timing. A 2024 Journal of Business Research study showed that personalized financial-services messages boosted engagement by 34% and reduced call-center traffic by 22%. Banking providers now embed pre-approved credit limits into loan-offer letters, while insurers automate claim-status updates that outline customer-specific next steps. Mortgage servicers depend on CCM to meet Real Estate Settlement Procedures Act deadlines of three business days, a benchmark manual workflows seldom hit. Sector players increasingly treat personalized correspondence as a retention lever amid commoditization.

Adoption of Cloud-Native CCM Platforms

Cloud architectures decouple workloads from on-premises infrastructure, enabling elastic scaling during peak periods such as tax season, open enrollment, or utility billing. Microsoft incorporated Nuance Communications into Dynamics 365 to orchestrate voice, email, and SMS from one console.[1]Microsoft Corporation, “Nuance Acquisition News Release,” microsoft.com Public-cloud CCM leverages serverless compute to render millions of PDFs in parallel and route output based on customer preferences captured in CRM. Hybrid topologies remain common in regulated industries; EU banks deploy private nodes within national borders yet archive correspondence in public cloud object stores, satisfying data residency rules.[2]European Banking Authority, “Cloud Computing Guidelines,” eba.europa.eu CFOs favor pay-as-you-go models that turn fixed IT costs into variable operating expenses.

Regulatory Mandates for Secure, Auditable Correspondence

Compliance frameworks embed audit trails, version control, and tamper-evident signatures into CCM workflows. The U.S. SEC’s 2024 Rule 17a-4 amendments require broker-dealers to retain electronic communications for six years in non-erasable formats, driving blockchain-backed storage adoption. HIPAA’s Breach Notification Rule obliges providers to log delivery receipts within 60 days of an incident. Europe’s Accessibility Act mandates correspondence be screen-reader-friendly by June 2025. CCM vendors now preload templates with required disclosure language and accessibility tags, reducing remediation cycles.

Omnichannel Engagement and Digital Transformation Push

Rich Communication Services hit 1 billion monthly active users in 2024, giving enterprises a media-rich alternative to SMS.[3]GSMA, “Rich Communication Services,” gsma.com WhatsApp Business APIs achieve 89% open rates in Brazil, surpassing email response levels by a significant margin. Firms orchestrate print, portal, email, and chatbots from a single decision layer that evaluates urgency, preference, and cost. Hybrid workflows generate print-ready PDFs and digital twins simultaneously, preserving legal admissibility while ensuring digital convenience. Chatbot dialogs now trigger follow-up emails summarizing interactions to create auditable customer-service records.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front implementation costs | -1.4% | Global, acute in price-sensitive SME segments | Short term (≤ 2 years) |

| Data silos and skills shortage hinder integration | -1.2% | Global, pronounced in legacy-IT environments | Medium term (2-4 years) |

| Privacy-by-design limits on data personalization | -0.8% | EU and privacy-forward jurisdictions | Long term (≥ 4 years) |

| Proprietary template-engine vendor lock-in risks | -0.9% | Global, affecting enterprises with multi-vendor CCM stacks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Implementation Costs

Enterprise CCM projects often require USD 0.5–2 million in software, services, and infrastructure, straining budgets in sectors with thin margins. SaaS models convert licenses into monthly fees, yet variable charges for data egress, API overages, and premium support complicate cost forecasts. Small banks generating fewer than 50,000 monthly communications sometimes find cloud CCM pricier than maintaining a two-person desktop-publishing team. Extended integration timelines further amplify dual-running expenses as legacy platforms persist during cut-over.

Data Silos and Skills Shortage Hinder Integration

CCM platforms need live access to CRM, ERP, and data-lake assets, but many organizations lack the APIs and master-data governance to expose these sources. Nightly batch extracts yield stale personalization data, missing time-critical triggers. Integration specialists familiar with both legacy middleware and modern gateways remain scarce, creating six- to nine-month backlogs. Poor address hygiene and duplicate records inflate print reruns and bounce rates, eroding ROI until data-quality initiatives mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain as Complexity Rises

Software modules captured 62.10% correspondence management system market share in 2025, reflecting enterprises’ appetite for unified suites that bundle composition, automation, and workflow. Services revenue is forecast to log a 16.18% CAGR as firms hire integrators to connect CCM with CRM, ERP, and event-streaming backbones. Generative AI now drafts personalized text from structured data, shrinking template libraries and accelerating campaigns. Managed-service options appeal to organizations that lack internal CCM talent, allowing them to shift ongoing operations to external specialists.

As integration scopes widen, services conduct template migration, data-mapping, and compliance validation. Document automation capabilities move beyond PDFs to interactive HTML5 files that embed video and charts. Workflow engines tie correspondence to case milestones such as claim approval or dispute closure. The correspondence management system market size for services is expected to outpace software licensing by 2031, provided that integration complexity continues to rise.

By Delivery Channel: Social and Chatbots Disrupt Email Dominance

Web portals hosted 47.20% of 2025 outbound volume, confirming customer preference for self-service access over postal delivery. Yet social and chatbot lanes are set to post a 15.89% CAGR, driven by RCS, WhatsApp, and region-specific messengers. Email remains central for transactional notices, but inbox clutter pushes firms to adopt DMARC and BIMI to preserve deliverability.

SMS and MMS achieve 98% open rates within three minutes, sustaining premium pricing for fraud alerts and appointment reminders. Print persists for high-value documents requiring physical copies. Omnichannel orchestration evaluates urgency, cost, and preference before dispatch, a capability legacy batch systems lack. This variety positions the correspondence management system market to remain channel-agnostic, with emerging formats continuing to erode email’s share.

By Deployment Model: Public Cloud Pulls Ahead on Economics

Cloud accounted for 68.05% of 2025 deployments and is expected to dominate new projects through 2031. Public-cloud CCM uses AWS S3, Azure Cognitive Services, or Google Cloud Pub/Sub to deliver per-message economics. European banks deploy private nodes for core data while exploiting public CDNs for portal delivery, complying with residency guidance from the European Central Bank.

On-premises environments shrink annually but persist in defense and critical-infrastructure contexts. Private clouds running on OpenStack or VMware offer dedicated resources with API-driven orchestration. The correspondence management system market size within public cloud is projected to expand fastest, while hybrid models satisfy organizations balancing sovereignty against cost.

By Organization Size: SMEs Embrace SaaS Simplicity

Large enterprises generated 55.10% of 2025 outlays, reflecting massive statement and notice volumes. Still, SMEs show a 16.05% CAGR as SaaS providers offer consumption pricing and pre-built QuickBooks, HubSpot, or Zoho connectors. Drag-and-drop builders eliminate coding, letting small lenders auto-generate mortgage disclosures that satisfy CFPB formatting rules.

Skills gaps weigh heavier on large firms managing legacy templates written in proprietary languages. SMEs face fewer integration hurdles because SaaS suites house content, workflow, and delivery in one tenancy. If adoption rates hold, the correspondence management system market share gap between enterprise and SME cohorts will narrow steadily.

By Industry Vertical: Healthcare Surges on Telehealth Mandates

BFSI captured 25.40% of 2025 revenue, owing to strict disclosure timelines for fees, loan terms, and fraud alerts. Healthcare and life sciences will advance at a 15.55% CAGR as CMS rules force payers to expose claims data via APIs by January 2026. Providers automate appointment reminders and lab-result notices to ease staff workloads.

Government agencies modernize citizen communications to meet digital-by-default laws in Singapore and the United Kingdom. Retail, telecom, and utilities deploy CCM for billing and outage notices, yet uneven penetration persists where print vendors defend entrenched contracts. Manufacturers remain underserved, signaling white-space for vendors to craft warranty and recall templates. As these trends crystallize, the correspondence management system market size tied to healthcare could overtake BFSI post-2030.

Geography Analysis

Asia-Pacific is the fastest-growing region, forecast at a 16.02% CAGR as India, Indonesia, and the Philippines roll out mobile-first digital-government initiatives requiring multilingual correspondence engines. North America retains 35.30% market share, driven by early cloud CCM adoption and compliance duties stemming from Dodd-Frank and the Affordable Care Act. SEC rules demand plain-language disclosures, boosting investment in tamper-evident templates.

Canada’s Anti-Spam Legislation drives the development of robust preference-management modules, while Mexico’s fintech boom fuels CCM to meet digital lending disclosure norms. Europe, grounded in GDPR and the Accessibility Act, mandates screen-reader-compatible outputs and strict retention schedules, nudging agencies to modernize by June 2025. Brazilian open-banking rules spur banks to deliver transaction data via APIs, while the UAE’s Smart Government program compels mobile-ready Arabic correspondence by 2026. South Africa and Kenya explore similar mandates, foreshadowing fresh demand. Collectively, cross-regional policy tailwinds continue to drive the expansion of the correspondence management system market worldwide.

Regulatory Landscape

Correspondence management system deployments are increasingly shaped by records retention, digital archiving, and accessibility requirements that demand provable integrity, searchability, and long retention windows across channels. In the United States, electronic records management obligations anchored in the Federal Records Act (including 44 USC 2912) and implementing requirements under NARA policy and 36 CFR Part 1236 reinforce capture and preservation of electronic messages, supported by indexing and disposition controls. This has pushed organizations toward audit-trailed correspondence repositories rather than ad hoc mailbox-based processes.

In Europe, compliance pressure is widening from privacy to long-term preservation and accessible-by-default communications. The European Accessibility Act compliance milestone in June 2025 raised requirements for screen-reader compatible outputs, and the European Commission Implementing Regulation (EU) 2025/2532 (Dec 2025) set standards for qualified electronic archiving services linked to ISO 14721:2025 and CEN/TS 18170:2025. At the national level, modernization continues, including the Netherlands Archiefwet 2026 (May 13, 2026), which updates digital information management and archival transfer practices. This, in turn, supports demand for CCM platforms that can apply retention schedules, metadata controls, and tamper-evident archiving within correspondence workflows.

Value Chain Analysis

The correspondence management system value chain begins with upstream infrastructure and enablers, including public cloud compute and storage, identity and access management, encryption, e-signature, and API gateways. Platform vendors then deliver correspondence composition, template management, workflow, rules, and omnichannel delivery connectors. Implementation and integration partners configure data models and connectors into CRM/ERP/case systems, migrate templates, and operationalize governance through audit trails, retention schedules, accessibility tags, and monitoring.

Downstream participants include channel and output providers, such as email/SMS/RCS and messaging platforms, web portals, and print and fulfillment vendors, alongside supervised archiving and e-discovery tools that preserve communications for regulated retention. Recent deployments show the chain becoming more centered on hyperscaler ecosystems and low-code automation. For instance, Neologix implemented an enterprise correspondence management system for Beeah Group on Microsoft SharePoint Online with Power Automate, Power BI, and DocuSign, reflecting a common pattern where collaboration platforms, workflow automation, analytics, and e-signature are bundled into the correspondence process. Regulatory-driven shifts also feed procurement and operating models, including the SECs June 2026 proposed Regulation E-Delivery, which supports electronic delivery as a default for key investor communications. That proposal also pushes firms to align content rendering, preference management, and immutable retention across digital channels.

Competitive Landscape

The top five vendors, OpenText, IBM, Adobe, Microsoft, and Quadient, control about 38% of 2024 revenue, indicating a moderately concentrated field. Each bundles CCM with adjacent martech, data, or service-desk modules to raise switching costs. API-first challengers such as Messagepoint and Doxee offer composable microservices that integrate with MACH stacks, appealing to digital-native buyers.

Technology competition centers on real-time event streams that trigger responses when IoT sensors or transaction processors emit signals. Vendors rush to integrate RCS, WhatsApp, and WeChat connectors, along with AI-driven personalization that dynamically assembles content. Regulatory compliance is a differentiator; suites embedding GDPR, HIPAA, and E-Accessibility checks shorten deployment timelines for risk-averse buyers.

M&A activity remains brisk: Hyland acquired a document-intelligence startup in July 2024 to enhance its OCR and intelligent processing capabilities. Quadient shifted to consumption pricing via a hyperscaler pact in September 2024. OpenText pledged USD 150 million in 2025 to embed generative AI across its Experience Cloud. These moves underscore a race to infuse AI, expand channels, and simplify economics within the correspondence management system industry.

Correspondence Management System Industry Leaders

IBM Corporation

Adobe Inc.

Open Text Corporation

Microsoft Corporation

Rosslyn Data Technologies Inc. (enChoice, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is forming where organizations need correspondence platforms to operate as end-to-end operational systems rather than document generators, connecting inbound interactions, case workflows, and outbound delivery with a single audit trail. Public sector and regulated enterprise programs provide clear demand signals for triage automation and standardized letter generation, including the UK governments algorithmic transparency disclosures for correspondence triage (FCDO and HM Treasury) and the US Department of Veterans Affairs Enterprise Correspondence Management-Letters (ECML) platform authorization (December 2025). These efforts aim to standardize letter generation across Veterans Benefits Administration lines of business. Together, they point to opportunities for vendors and integrators that productize classification, routing, and response patterns, while packaging governance controls suitable for high-volume citizen and benefits correspondence.

A second opportunity area is modernization toward cloud-native and composable deployments that reduce template lock-in and support faster omnichannel expansion, particularly when buyers already standardize on Microsoft 365 and Power Platform. Neologix reported a 65% processing-time reduction from a SharePoint Online and Power Automate based enterprise correspondence implementation for Beeah Group (April 2026), which highlights the value attached to workflow integration and real-time visibility. On the product side, differentiation is shifting toward embedding communications into business processes and assistant-driven authoring, as Comparts Spring 2026 DocBridge Communication Suite adds Business Flows and an AI Assistant to tie communications into end-to-end processes. Across industries, these proof points support go-to-market focus on prebuilt connectors, compliance-ready archiving, and packaged workflow accelerators for government, BFSI, and healthcare deployments that must document decisions and deliveries across email, portals, chat, and print.

Recent Industry Developments

- April 2026: IBM introduced new industry solutions with Adobe for AI-powered experience orchestration, targeting real-time, intent-driven engagement across customer touchpoints. The update strengthens integration between orchestration layers and content and document experiences, supporting correspondence programs that need faster personalization while maintaining controlled templates and auditability.

- July 2025: OpenText released Cloud Editions (CE) 25.3, including a multi-tenant SaaS OpenText Core Communications platform to support customer communications management. The release deepens the shift from on-premises and single-tenant deployments toward standardized SaaS operations, which affects how buyers evaluate scalability, compliance controls, and consumption-based economics for high-volume correspondence.

- July 2024: Hyland acquired a document-intelligence startup to enhance OCR and intelligent processing capabilities. This broadened the ability to extract data and classify inbound documents, strengthening the upstream capture and automation layer that feeds correspondence workflows and reducing manual effort in regulated correspondence and case management processes.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers software and related services that help organizations create, manage, route, approve, and store business correspondence across channels, with controls for templates, tracking, and compliance. Our sizing focuses on vendor revenues earned from these platforms, plus implementation and support work.

Scope exclusions: hardware-only mailroom equipment, generic scanning and archiving tools sold without a correspondence workflow, and physical postal spend are excluded.

Segmentation Overview

- By Component

- Software

- Correspondence composition

- Document automation

- Case and workflow management

- Services

- Software

- By Delivery Channel

- Web-based

- Email-based

- SMS/MMS-based

- Social / Chatbots

- By Deployment Model

- On-Premises

- Cloud

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Organisation Size

- Small and Medium Enterprises

- Large Enterprises

- By Industry Vertical

- BFSI

- Government and Public Sector

- Telecom and IT

- Healthcare and Life Sciences

- Retail and E-commerce

- Utilities and Energy

- Manufacturing

- Other Industry Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with aligning the product boundary and buyer behavior for correspondence platforms, then mapping what typically drives spending by region and by regulated industries. We referenced public sources such as US SEC filings for listed vendors, US Census Bureau and Eurostat series for enterprise activity signals, NIST and ISO publications for security and records concepts, and government or regulator guidance that shapes communications retention, for example in healthcare and financial services.

We also used vendor annual reports, investor presentations, product documentation, and reputable press coverage to understand pricing models, cloud migration patterns, and channel mix changes, including email, web, print, and messaging. Where needed, we used paid company financials and an intelligence subscription, along with a patent database, to cross-check revenue splits and product positioning. These sources are illustrative only, and many other public references were used for data collection, validation, and clarifying assumptions.

Primary Interviews and Surveys

Primary work focused on validating adoption levels, typical contract sizes, and the split between software subscriptions and services across regulated and high-volume communication users. We spoke with a mix of solution providers, system integrators, and enterprise users across APAC, EMEA, and the Americas, so assumptions on deployment preference, channel usage, and renewal behavior could be stress-tested before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 14% | APAC: 41% |

| Mid tier: 44% | Functional/Unit leaders: 38% | EMEA: 34% |

| Smaller Players: 20% | Managers: 48% | Americas: 25% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand pool that reconstructs spend from enterprise software and services outlays, then filters it through correspondence platform penetration by industry, deployment mix, and channel intensity. To keep the numbers grounded, we corroborated totals with selective bottom-up checks, including sampled vendor revenue disclosures, partner-led implementation run rates, and ASP times estimated customer volumes for common use cases.

Key model inputs included cloud versus on-premises adoption rates, regulated industry share such as BFSI and public sector, typical communications volume and channel mix, including email, web portals, print, and messaging, average subscription pricing bands by organization size, and services attach rates for integration and template migration. When a vendor did not disclose clean product revenue, gaps were handled through peer benchmarking and primary feedback, then adjusted to match observable growth signals.

Forecasts used scenario analysis supported by variable-level expectations gathered in interviews, followed by a smoothing step so adoption and pricing do not shift unrealistically year to year. Sensitivities were run on cloud migration speed, services intensity, and multi-channel expansion, since these are the biggest budget drivers in this space.

Data Validation & Update Cycle

Model outputs were checked against independent signals, including enterprise IT spending direction, cloud adoption indicators, and publicly visible vendor performance commentary. Outliers were investigated by revisiting assumptions on pricing, channel mix, and services attach, then using peer comparisons to confirm that no single input was overstating the result.

A multi-step internal review was completed before sign-off, and follow-up calls were triggered when primary feedback showed large variance on contract size or deployment mix. Reports are refreshed annually, with interim updates made when material events occur, such as major regulation changes or sharp shifts in cloud demand. Before delivery, an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Correspondence Management System Market Estimate Compared With Other Published Estimates

Published market numbers for correspondence management systems can look far apart because firms often count different revenue streams, apply different time windows, and use different assumptions on pricing and cloud migration speed. Differences also show up when services are counted broadly, or when adjacent customer communication tools are grouped into the same bucket.

Physical mail processing and postal spend sit outside Mordor Intelligence's scope, which is why estimates that blend mailroom operations or broader customer communication suites can land higher even when the buyer set looks similar. In addition, some figures lean on older base-year pricing, apply aggressive multi-channel expansion, or use single-region extrapolation without checking deployment mix and services attach rates across industries.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 52.46 B (2025) | |

| Trade Publisher A | USD 2.62 B (2024) | Uses a narrower definition that resembles packaged correspondence software only, and it appears to exclude services and several delivery channels that are counted in full-suite deployments. |

| Industry Report B | USD 4.70 B (2025) | Leans toward a smaller vendor set and a tighter application scope, with limited evidence of adjusting for enterprise-wide rollouts and the services layer tied to integrations and template migration. |

The spread in the table mainly comes from what is counted as platform revenue versus adjacent tooling, and whether services and multi-channel delivery are included consistently. By keeping the model tied to clear adoption, pricing, and deployment indicators, the final value stays traceable to inputs that can be re-checked and updated as market conditions shift.

Key Questions Answered in the Report

How big is the correspondence management system market in 2026?

It stands at USD 60.33 billion and is projected to reach USD 121.12 billion by 2031 at a 14.98% CAGR.

Which region is expanding fastest for correspondence platforms?

Asia-Pacific leads growth, forecast at a 16.02% CAGR through 2031 due to mobile-first digital-government mandates.

Which vertical will grow quickest through 2031?

Healthcare and life sciences, propelled by telehealth adoption and CMS interoperability rules, is set to rise at a 15.55% CAGR.

What component segment is seeing the highest CAGR?

Services, encompassing implementation, integration, and managed offerings, are forecast to grow at 16.18% through 2031.

How concentrated is vendor competition?

The top five vendors account for roughly 38% of 2024 revenue, reflecting a moderately concentrated field with ongoing room for niche entrants.

Page last updated on: