Crankshaft Sensor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.8 Billion |

| Market Size (2030) | USD 2.64 Billion |

| Growth Rate (2025 - 2030) | 7.96% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Crankshaft Sensor Market Analysis by Mordor Intelligence

The crankshaft sensor market size reached USD 1.8 billion in 2025 and is projected to expand at a 7.96% CAGR to USD 2.64 billion by 2030, reflecting the tightening of global emission rules and the automotive industry's push toward refined engine controls. Heightened regulatory scrutiny compels original-equipment manufacturers to adopt more precise sensing technologies that improve combustion timing, lower tailpipe emissions, and support hybrid powertrains. Engine downsizing, turbocharging, and cylinder-deactivation strategies further lift sensor demand as each tactic relies on accurate crankshaft angle data to synchronize fuel injection and spark events. Electrification, especially in mild- and full-hybrid architectures, sustains short-term demand because hybrids still operate internal-combustion engines that require even tighter control during frequent start-stop cycles. Suppliers capable of guaranteeing high-temperature stability and electromagnetic compatibility gain a competitive advantage as the density of in-vehicle electronics rises. Meanwhile, semiconductor volatility forces automakers to dual-source sensor platforms or renegotiate long-term capacity reservations with chip foundries, favouring vertically integrated vendors that manage package assembly and front-end silicon under one roof.

Key Report Takeaways

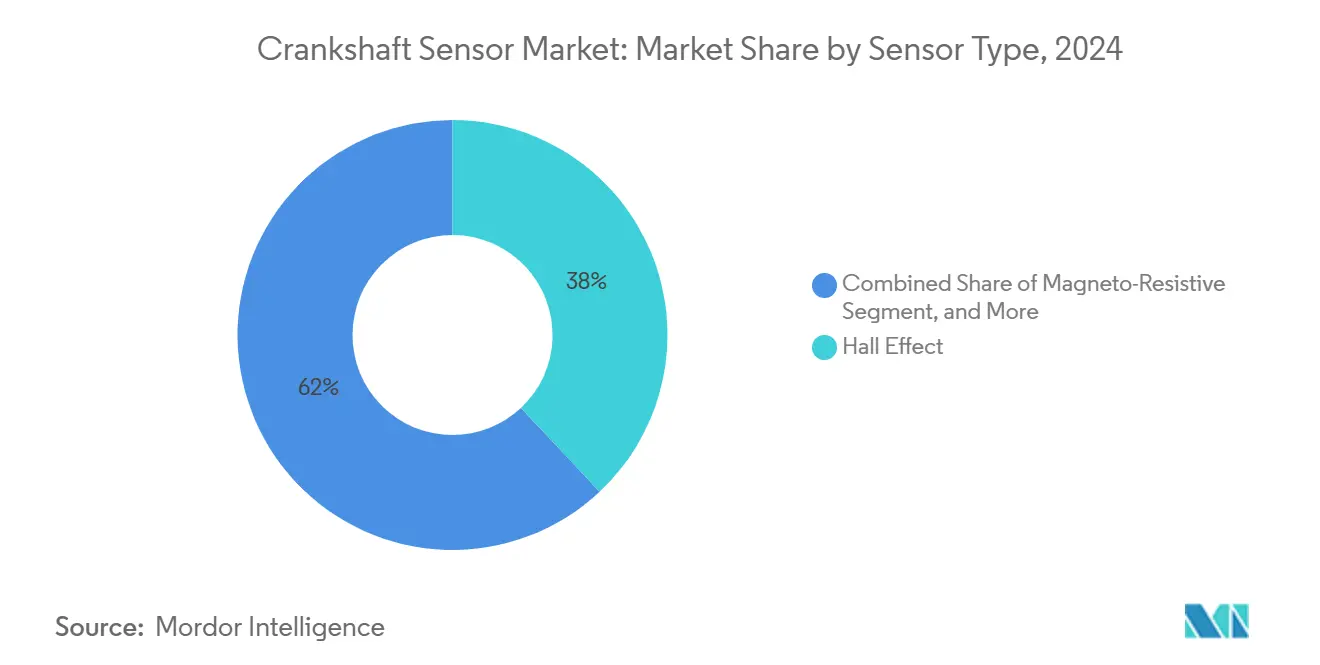

- By sensor type, Hall Effect sensors held a 38% revenue share in 2024, while Magneto-Resistive sensors are projected to grow at an 8.21% CAGR through 2030.

- By application, passenger vehicles accounted for 46% of demand in 2024, whereas electric and hybrid vehicles led growth at a 9.21% CAGR through 2030.

- By technology, digital sensors captured 51% market share in 2024, while smart sensors with embedded electronics are advancing at a 9.83% CAGR toward 2030.

- By vehicle type, gasoline engines led with a 44% share in 2024, while hybrid electric vehicles registered the fastest 8.94% CAGR to 2030.

- By distribution channel, OEM sales dominated with an 82% share in 2024 and are forecast to expand at an 8.55% CAGR up to 2030.

- By end-user industry, automotive manufacturers commanded 69% of revenue in 2024, and the same segment is expected to post the highest 9.55% CAGR through 2030.

- By geography, Asia-Pacific captured 34.56% of crankshaft sensor market share in 2024 and is projected to grow at a 10.01% CAGR to 2030.

Global Crankshaft Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification push in light-duty vehicles | +2.10% | Global, with early gains in China, Europe, California | Medium term (2-4 years) |

| Tightening global emission standards | +1.80% | Global, with EU Euro 7 and EPA MY2027-2032 leading | Short term (≤ 2 years) |

| Rapid growth of ADAS-enabled powertrains | +1.50% | North America and EU core, spill-over to APAC | Medium term (2-4 years) |

| Transition toward integrated starter-generator architectures | +1.20% | Global, with focus on premium segments initially | Long term (≥ 4 years) |

| Rising demand for predictive maintenance in fleet telematics | +0.80% | North America and EU commercial fleets | Short term (≤ 2 years) |

| Emergence of cylinder-deactivation strategies in turbo engines | +0.60% | Global, concentrated in light-duty gasoline engines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Electrification Push in Light-Duty Vehicles

Hybrid and plug-in hybrid powertrains rely on repeated engine restarts, electric-only creep, and regenerative deceleration, each of which demands sub-millisecond crank angle feedback to keep combustion events synchronized with motor torque. The EPA’s regulatory impact assessment for model years 2027-2032 confirms that hybrid configurations achieve their fuel economy targets only when sensors provide precise angular data to enable electrically assisted catalyst heating and rapid closed-loop combustion control.[1]U.S. Environmental Protection Agency, “Multi-Pollutant Emissions Standards for Model Years 2027–2032,” epa.gov As a result, automakers specify dual-redundant crankshaft sensors with on-chip self-diagnostics to pass ISO 26262 functional-safety audits, creating volume upside for suppliers offering integrated packages rated for 150 °C continuous operation.

Tightening Global Emission Standards

The EPA aims for fleet-average 85 g mi-1 CO₂ by 2032, while China’s upcoming National VII protocol and Europe’s Euro 7 framework set comparable thresholds that force combustion optimization beyond prior norms.[2]Environmental Protection Agency, “Onboard Diagnostics Requirements,” ecfr.gov Advanced variable valve timing and lean-burn modes rely on real-time crankshaft phasing, prompting OEMs to adopt magneto-resistive sensing elements that maintain accuracy across extreme temperature gradients. In parallel, on-board diagnostics now require continuous electrical integrity checks, so sensor makers embed digital signal conditioners, which raise both product complexity and the average selling price.

Rapid Growth of ADAS-Enabled Powertrains

SAE Level 3 automated driving launches link traction, braking, and propulsion subsystems through central domain controllers. Any timing error at the crank may cascade into torque-vectoring misalignment, so OEMs impose stricter electromagnetic compatibility and diagnostic standards on position sensors.[3]SAE International, “Are Today’s Sensors Ready for Next-Level Automated Driving?” sae.org Demand thus shifts toward digital or smart sensors with deterministic latency and built-in cyclic redundancy checks, benefiting vendors that co-design ASIC logic and magnetics.

Integrated Starter-Generator Architectures

Forty-eight-volt mild hybrids couple belt-driven starter-generators directly to the crank pulley, which exposes sensors to higher electromagnetic fields. Infineon’s 2024 launch of Hall-based ICs hardened for such environments illustrates market adaptation.[4]Infineon Technologies AG, “New 48-Volt Hall ICs for Mild Hybrids,” infineon.com As integrated systems proliferate in premium models, the requirements for high-temperature magnets and tighter assembly tolerances elevate bill-of-materials costs, but also raise switching costs for automakers, thereby stabilizing long-term contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in automotive semiconductor supply | -1.40% | Global, with particular impact on Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Price sensitivity in mass-market passenger cars | -0.90% | APAC core, with secondary effects in emerging markets | Medium term (2-4 years) |

| Slow replacement cycles in commercial vehicles | -0.70% | Global commercial vehicle markets | Long term (≥ 4 years) |

| Limited aftermarket data standardization for EV powertrains | -0.50% | Global, with early impact in EV-leading markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Automotive Semiconductor Supply

The surge in vehicle silicon content heightens vulnerability to wafer-fab disruptions. Because crankshaft sensors now incorporate DSP cores and non-volatile memory, they compete with ADAS processors for the same 180 nm and 130 nm automotive-grade process nodes. Suppliers with captive front-end output or multi-sourcing agreements can mitigate production gaps and secure a higher allocation priority during shortages, thereby strengthening their pricing power.

Price Sensitivity in Mass-Market Passenger Cars

Although advanced sensors lift powertrain efficiency, entry-level vehicles in India, ASEAN, and Latin America remain cost-constrained. Automakers balance emission compliance against affordability, delaying adoption of premium magneto-resistive devices in favour of mature Hall Effect designs until stricter local rules take effect. Vendors address affordability via lead frame miniaturization, automated coil winding, and platform reuse across engine families.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Magneto-Resistive Precision Gains Momentum

Magneto-Resistive devices captured 8.21% CAGR momentum through 2030 on the strength of high-resolution angular detection that satisfies hybrid combustion calibration. Hall Effect sensors nonetheless retained a 38% revenue lead in 2024 due to scale economies and pervasive validation across ICE platforms. The crankshaft sensor market size for Hall technology remains significant as legacy programs extend into emerging regions. Digital signal conditioning in next-generation magneto-resistive chips reduces electromagnetic drift and enables intrinsic self-test features that streamline ISO 26262 audits. Meanwhile, magnetic-pickup and inductive variants continue serving heavy-duty engines where vibration and oil contamination limit optical-based options. Vendors leverage backward-compatible footprints to pitch drop-in magneto-resistive upgrades that share connector standards with Hall predecessors, easing OEM migration and defending installed bases.

Shifts in sensor mix stem from powertrain electrification and emissions controls that tighten permissible timing error. Premium brands experiment with dual-track magneto-resistive topologies that provide both incremental and absolute position data, empowering real-time crank speed analysis for knock mitigation. Analog devices persist in low-cost passenger cars, yet their share gradually falls as semiconductor cost curves favour digital conversion. Optical sensors stay niche, favoured by motorsport teams demanding micro-degree accuracy but limited by debris sensitivity. Through the forecast horizon, magneto-resistive and smart Hall platforms emerge as dual pillars, consolidating supplier roadmaps and amplifying the overall crankshaft sensor market.

By Application: Hybrid Vehicle Momentum Reshapes Demand

Passenger vehicles accounted for 46% of global shipments in 2024, as light-duty platforms integrated higher sensor counts for start-stop and variable compression. Electric and hybrid vehicles deliver the fastest 9.21% CAGR, spurring the development of bespoke crankshaft packages that are tolerant of high-voltage electromagnetic interference. OEM validation plans now co-locate sensor prototypes within battery enclosures to characterize field coupling early in design cycles, a service tier led by Bosch and Continental. Commercial vehicles are expected to maintain mid-single-digit expansion, buoyed by telematics-enabled predictive maintenance mandates within fleet contracts. Engines in refuse trucks or urban delivery vans deploy double-sealed sensor assemblies to survive frequent thermal cycling alongside regenerative braking hardware.

Regulatory headwinds propel the hybrid subset of the crankshaft sensor market, yet full battery electric vehicles do eliminate certain engine sensors outright. Suppliers hedge their exposure by expanding their portfolio breadth, adding rotor-position and wheel-speed devices that fill revenue gaps as pure electric vehicles proliferate. In aftermarket channels, rising average vehicle age and longer powertrain warranties create a steady replacement cadence, preserving volume even as new-vehicle sensor content evolves.

By Technology: Digital and Smart Architectures Dominate

Digital configurations accounted for a 51% share in 2024 because they are designed to withstand the electromagnetic noise inherent to 48-volt buses and inverters. Smart sensors with embedded microcontrollers are advancing at a 9.83% CAGR, integrating edge analytics that flag magnetic signature drift before catastrophic failure. The crankshaft sensor market share for analog types narrows to cost-focused segments in South Asia and Africa.

Integrated flash memory allows field-programmable thresholds, reducing SKU count for multinational platforms and simplifying global homologation. Continental’s 2024 rollout of multi-protocol digital sensors exemplifies cross-domain flexibility, as they communicate either SENT or PSI5, depending on the host ECU firmware. Regulatory updates that demand line-fault detection further cement the shift toward intelligent devices, driving incremental revenue through value-added diagnostics.

By Vehicle Type: Gasoline Engines Retain Scale During Transition

Gasoline programs held 44% market share in 2024, anchored by widespread adoption in North America, Europe, and Japan. The crankshaft sensor market size for hybrid electric configurations rises the fastest because these drivetrains double the number of engine-start events and amplify timing precision requirements. Diesel adoption softens in light-duty cars, yet remains pivotal in heavy-duty and off-road segments, where electrification remains cost-prohibitive.

Suppliers tailor diesel-specific sensors with reinforced housings to withstand higher torsional vibration. Fully electric vehicles eliminate conventional crank triggers altogether, but vendors offset the lost volume by repositioning their magnetics expertise into rotor or resolver sensors that serve motor-drive applications. OEM technical-roadmap disclosures suggest that gasoline engines will continue to anchor global light-vehicle output past 2030, giving suppliers a runway to amortize next-generation Hall and magneto-resistive R&D.

By Distribution Channel: OEM Dominance Strengthens

OEM contracts accounted for 82% of shipments in 2024, reflecting the integration of supply chains and the stringent approval process for production parts. The crankshaft sensor market size flowing through aftermarket channels rises moderately as vehicle age climbs in key regions and electronic diagnostics help independent repair shops identify emerging failures. Standard Motor Products’ 2024 SKU expansion underscores sustained replacement demand despite shifts in drivetrain.

E-commerce platforms in the United States and Europe increase price transparency, pressuring independent brands to publish operating curves and cross-reference catalogs. Meanwhile, OEM purchasing departments push cost-down initiatives while accepting premium prices for smart sensors that reduce warranty claims through predictive analytics.

By End-User Industry: Automakers Drive Volume, Fleets Push Intelligence

Automotive manufacturers absorbed 69% of total demand in 2024, championing platform-wide sensor standardization to reduce assembly complexity. Auto repair shops and service centers constitute the secondary usage block, driven by more complex diagnostics that encourage proactive replacement. Industrial machinery, though modest in share, values extended temperature rating and mechanical robustness for stationary backup generators that face stricter emissions rules from the EPA.

Suppliers are now adopting configurable output protocols, enabling their hardware to serve both automotive CAN networks and industrial Modbus controllers. By integrating such flexibility into their products, suppliers can cater to diverse application requirements across multiple industries. This shift not only broadens their market reach but also eliminates the need for new production tooling, reducing costs and improving operational efficiency. Additionally, it allows suppliers to respond more effectively to evolving customer demands and technological advancements.

Geography Analysis

The Asia-Pacific region continued to hold 34.56% of global revenue in 2024 and posted a leading 10.01% CAGR from 2024 to 2030. Chinese OEMs are accelerating the adoption of magneto-resistive sensors to meet the National VI and upcoming VII standards, while also deploying 48-volt hybrids in compact SUV segments. Local Tier-1s leverage domestic wafer fabs to secure allocation, yet global brands retain a competitive edge through process maturity and proven quality. Supply-chain diversification moves low-cost assembly to Vietnam and Thailand, cushioning firms against wage inflation in coastal China.

North America, still dominated by light-duty gasoline models, sustains mid-single-digit growth under the EPA’s MY2027-2032 framework. High adoption of pickup trucks with integrated starter-generators lifts per-vehicle sensor counts, offsetting gradual EV penetration. Aftermarket sales thrive as average fleet age edges past 12 years, keeping replacement volumes resilient.

Europe remains an innovation hub owing to the Euro 7 phase-ins and a strong premium-vehicle mix. OEMs lead in smart sensor rollouts, requiring suppliers to validate functional safety metrics under TÜV protocols. Nevertheless, regional volumes trail Asia-Pacific because of slower vehicle output recovery.

The Middle East and Africa along with South America register smaller but steady contributions, powered by relaxed emission schedules and a large influx of used imports. Local assemblers still adopt Hall Effect technology due to cost prioritization, yet regulators announce future alignment with Euro 5 equivalents, paving paths for gradual uptakes of higher-grade sensing solutions. Currency volatility and limited-service infrastructure constrain immediate smart-sensor adoption but provide long-term opportunity as connected-fleet models expand.

Competitive Landscape

The crankshaft sensor market exhibits moderate concentration. Bosch, Continental, and DENSO collectively supply approximately 45% of the global volume by maintaining extensive product ranges and long-term platform agreements with major automakers. Bosch broadened its aftermarket catalogue by 100 new references in November 2024, signalling a commitment to replacement channels. Continental is rolling out 700 advanced engine-management parts by 2025, targeted at hybrids and mild hybrids. DENSO partners with Chinese automakers to co-develop sensing modules tailored to National VII requirements.

Second-tier competitors, such as Infineon, Sensata, and STMicroelectronics, differentiate themselves through their prowess in ASIC design and packaging. STMicroelectronics’ USD 950 million purchase of NXP’s MEMS assets in September 2024 bolsters its smart-sensor roadmap and secures captive micro-machining capacity. Meanwhile, Standard Motor Products focuses on the breadth of aftermarket SKUs to secure shelf space in retail chains and e-commerce portals.

Supply-chain resilience is an emerging competitive axis. Vendors with multi-regional wafer fronts or close foundry partnerships lessen allocation shocks, winning preference among automakers wary of production halts. Portfolio diversification into EV-centric rotor-position sensors also hedges against long-term ICE volume contraction. Intellectual-property barriers centered on magnetic circuit design and auto-grade encapsulants restrain new entrants despite apparent component simplicity.

Crankshaft Sensor Industry Leaders

Robert Bosch GmbH

Continental AG

DENSO Corporation

BorgWarner Inc. (Delphi Technologies)

Hitachi Astemo Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: STMicroelectronics announced the acquisition of NXP Semiconductors' MEMS sensors business for up to USD 950 million, encompassing automotive safety sensors for airbags and vehicle dynamics, as well as monitoring sensors for tire pressure and engine management, and industrial pressure sensors and accelerometers. The transaction is expected to close in the first half of 2026.

- May 2025: DENSO Corporation and ROHM Semiconductor have reached a basic agreement to establish a strategic semiconductor partnership, focusing on integrating automotive system design expertise with analog IC technologies to support vehicle electrification, automated driving, and connected vehicle applications. Plans include considering the strengthening of capital ties.

- March 2025: Tamagawa Seiki opened its seventh factory, Tamagawa Vietnam, in Quang Ninh province with an investment of USD 35 million to USD 35.75 million, specializing in angle sensors for electric vehicle engines with an estimated annual capacity of 14.49 million items and employment of approximately 1,000 workers, positioning the facility as a global manufacturing and distribution hub.

- February 2025: Senstronic acquired a majority stake in German sensor specialist Metallux AG, combining Senstronic's expertise in inductive, magnetic, capacitive, and optoelectronic sensor technologies with Metallux's thick-film technology sensors for pressure, linear, and rotary applications, with Metallux maintaining operational independence and existing management

Global Crankshaft Sensor Market Report Scope

The Crankshaft Sensor Market Report is Segmented by Sensor Type (Hall Effect Sensors, Magnetic Pickup Sensors, Inductive Sensors, Optical Sensors, Magneto-Resistive Sensors), Application (Passenger Vehicles, Commercial Vehicles, Electric Vehicles and Hybrid Vehicles, Others), Technology (Analog Sensors, Digital Sensors, Smart Sensors with Embedded Electronics), Vehicle Type (Gasoline Vehicles, Diesel Vehicles, Electric Vehicles, Hybrid Electric Vehicles), Distribution Channel (OEM, Aftermarket), End-User Industry (Automotive Manufacturers, Auto Repair Shops and Service Centers, Industrial Machinery Manufacturers), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Hall Effect Sensors |

| Magnetic Pickup Sensors |

| Inductive Sensors |

| Optical Sensors |

| Magneto-Resistive Sensors |

| Passenger Vehicles |

| Electric Vehicles (EVs) And Hybrid Vehicles |

| Commercial Vehicles (Trucks, Buses, Heavy Machinery) |

| Other Applications (Racing, Industrial Engines) |

| Digital Sensors |

| Analog Sensors |

| Smart Sensors with Embedded Electronics |

| Diesel Vehicles |

| Gasoline Vehicles |

| Electric Vehicles (EVs) |

| Hybrid Electric Vehicles (HEVs) |

| OEM (Original Equipment Manufacturer) |

| Aftermarket |

| Automotive Manufacturers |

| Industrial Machinery Manufacturers |

| Auto Repair Shops and Service Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Sensor Type | Hall Effect Sensors | |

| Magnetic Pickup Sensors | ||

| Inductive Sensors | ||

| Optical Sensors | ||

| Magneto-Resistive Sensors | ||

| By Application | Passenger Vehicles | |

| Electric Vehicles (EVs) And Hybrid Vehicles | ||

| Commercial Vehicles (Trucks, Buses, Heavy Machinery) | ||

| Other Applications (Racing, Industrial Engines) | ||

| By Technology | Digital Sensors | |

| Analog Sensors | ||

| Smart Sensors with Embedded Electronics | ||

| By Vehicle Type | Diesel Vehicles | |

| Gasoline Vehicles | ||

| Electric Vehicles (EVs) | ||

| Hybrid Electric Vehicles (HEVs) | ||

| By Distribution Channel | OEM (Original Equipment Manufacturer) | |

| Aftermarket | ||

| By End-User Industry | Automotive Manufacturers | |

| Industrial Machinery Manufacturers | ||

| Auto Repair Shops and Service Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of the crankshaft sensor market by 2030?

It stands at USD 2.9 billion and is projected to reach USD 4.21 billion by 2030.

Which segment shows the highest yield monitoring market share by device type?

Mass flow sensors accounted for 38.5% of 2024 revenue.

Which geography is expanding fastest for yield monitoring solutions?

The Middle East and Africa region is growing at a 9.27% CAGR through 2030.

Why are individual farmers adopting yield monitoring faster than corporations?

Falling sensor prices, lease-to-own financing, and simplified user interfaces cut barriers for smallholders.

What key restraint affects adoption in tropical climates?

High humidity accelerates sensor calibration drift, increasing maintenance cycles and costs.

How does carbon credit monetization influence sensor uptake?

Verified yield data is required to claim credits, turning monitoring systems into revenue enablers for regenerative practices.

Page last updated on: