Tilt Sensor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

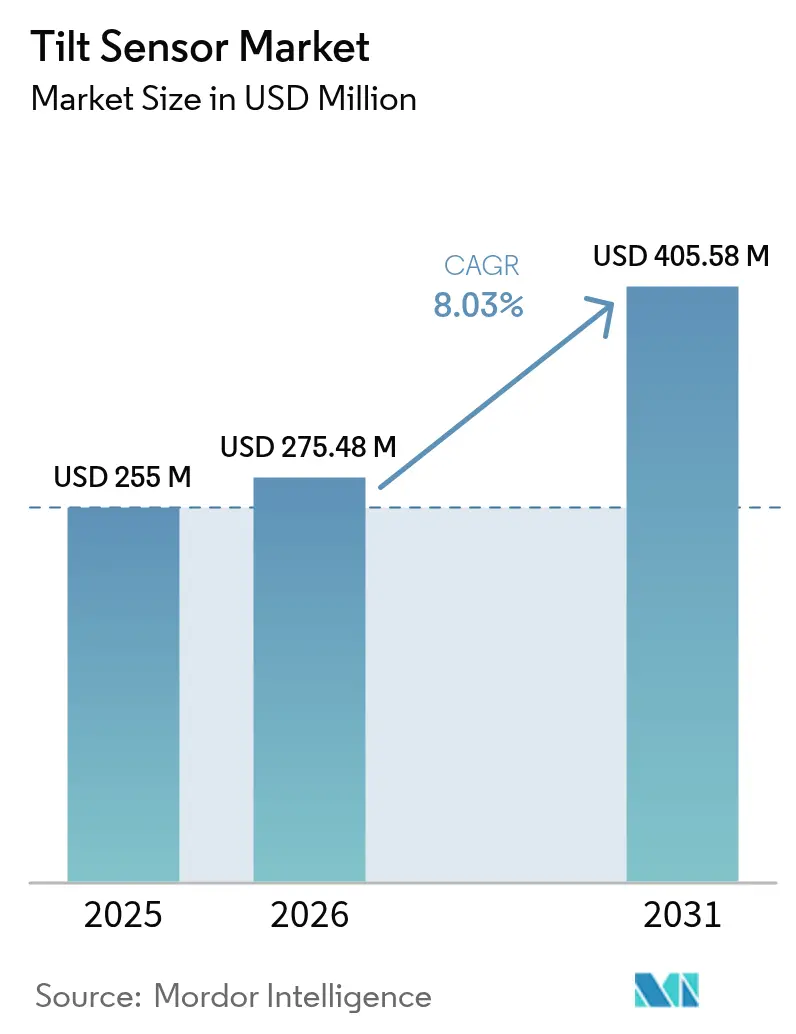

| Market Size (2026) | USD 275.48 Million |

| Market Size (2031) | USD 405.58 Million |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

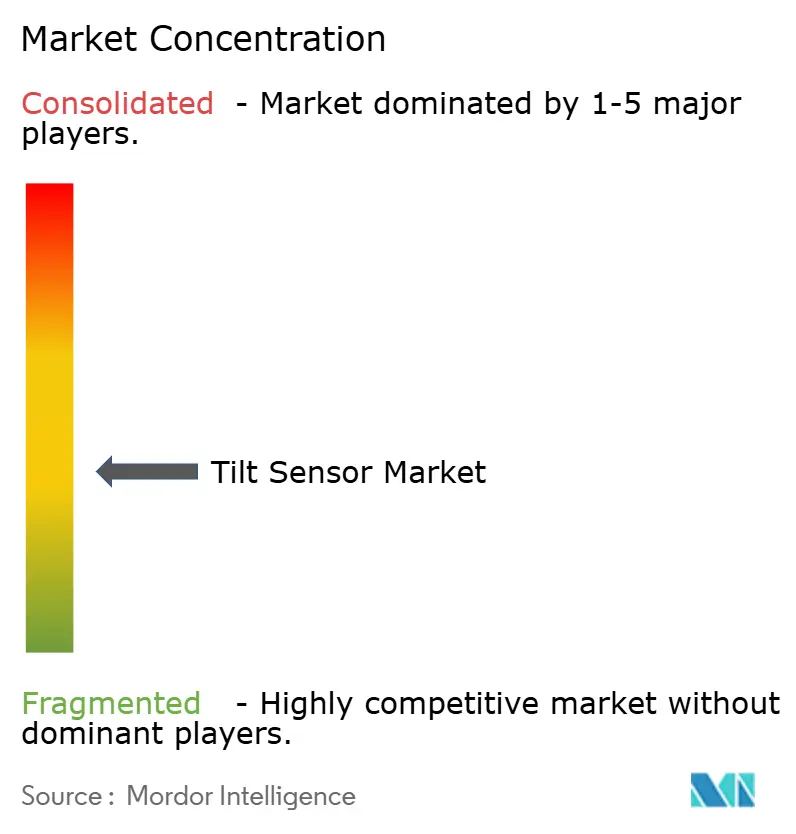

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tilt Sensor Market Analysis by Mordor Intelligence

The Tilt Sensor Market size was valued at USD 255 million in 2025 and estimated to grow from USD 275.48 million in 2026 to reach USD 405.58 million by 2031, at a CAGR of 8.03% during the forecast period (2026-2031).

Heightened demand for precise angular measurement in automation, renewable energy, and heavy machinery is sustaining double-digit unit growth even as average selling prices edge lower. Manufacturers are responding with miniaturized designs that withstand vibration, moisture, and EMI while delivering sub-degree accuracy, fuelling rapid adoption in Industry 4.0 retrofits and new equipment platforms. Fiber-optic tilt sensing has moved from niche civil-engineering projects to broader industrial use, where its electromagnetic immunity gives it an edge over MEMS solutions near high-voltage assets. Concurrently, design wins for dual-axis and multi-axis devices inside GNSS-guided construction machinery and wind-turbine monitoring systems are expanding revenue streams beyond traditional single-axis products, reinforcing the tilt sensor market momentum in the medium terms.

Key Report Takeaways

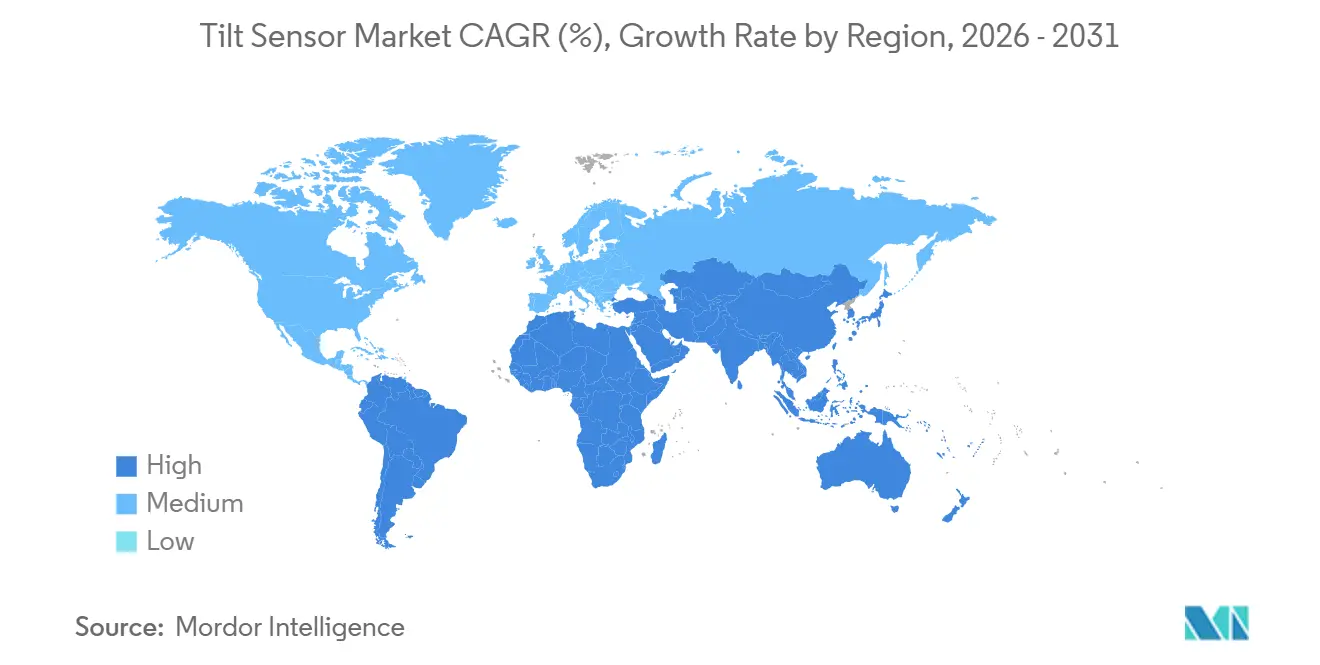

- By geography, Asia-Pacific led with 35.62% revenue share in 2025, while South America is projected to expand at a 9.62% CAGR through 2031.

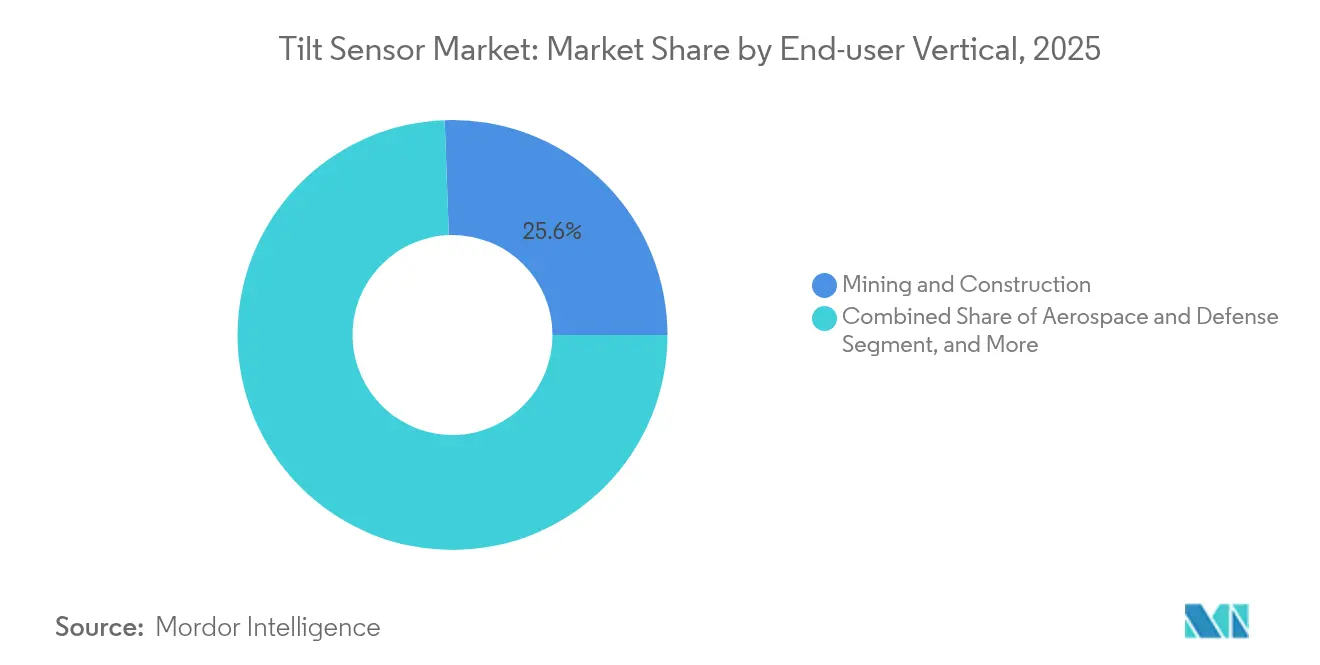

- By end-user vertical, mining and construction accounted for 25.58% of the tilt sensor market size in 2025, whereas renewable energy is set to grow at 11.74% CAGR to 2031.

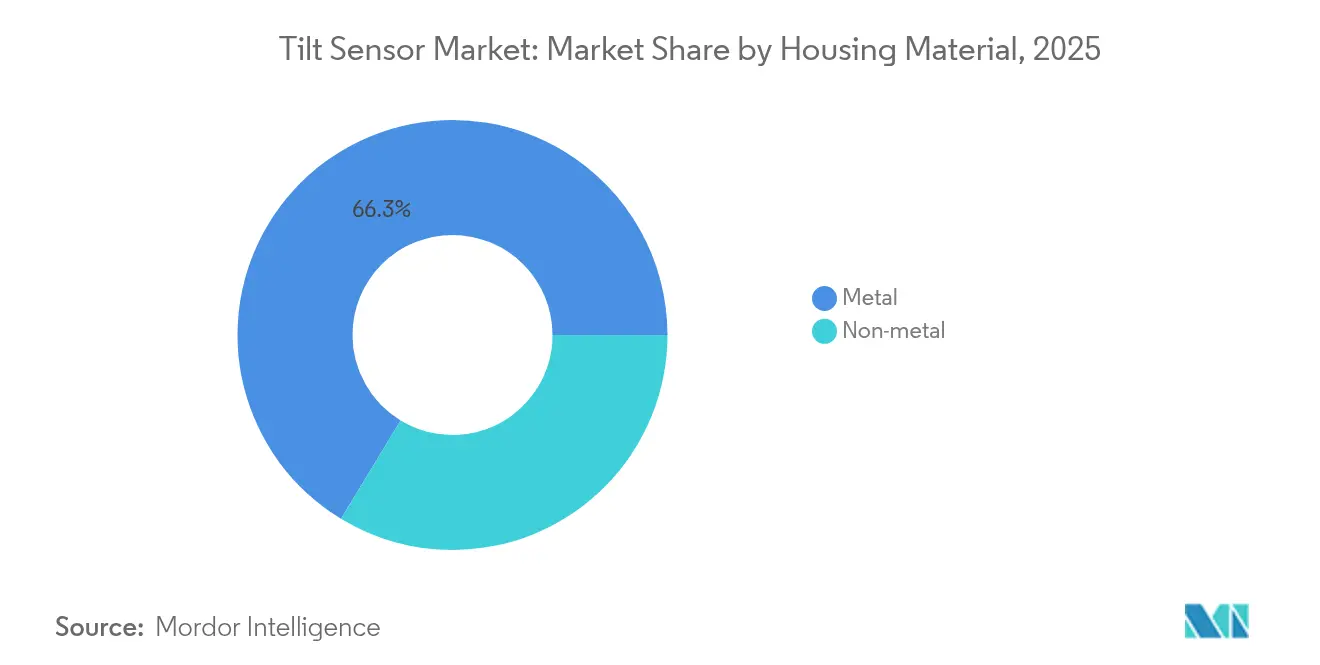

- By housing material, metal enclosures dominated with 66.32% share in 2025; non-metal alternatives are on track for a 9.84% CAGR.

- By technology, MEMS devices held 44.48% of the tilt sensor market share in 2025 and optical fiber Bragg grating sensors are poised for a 11.43% CAGR to 2031.

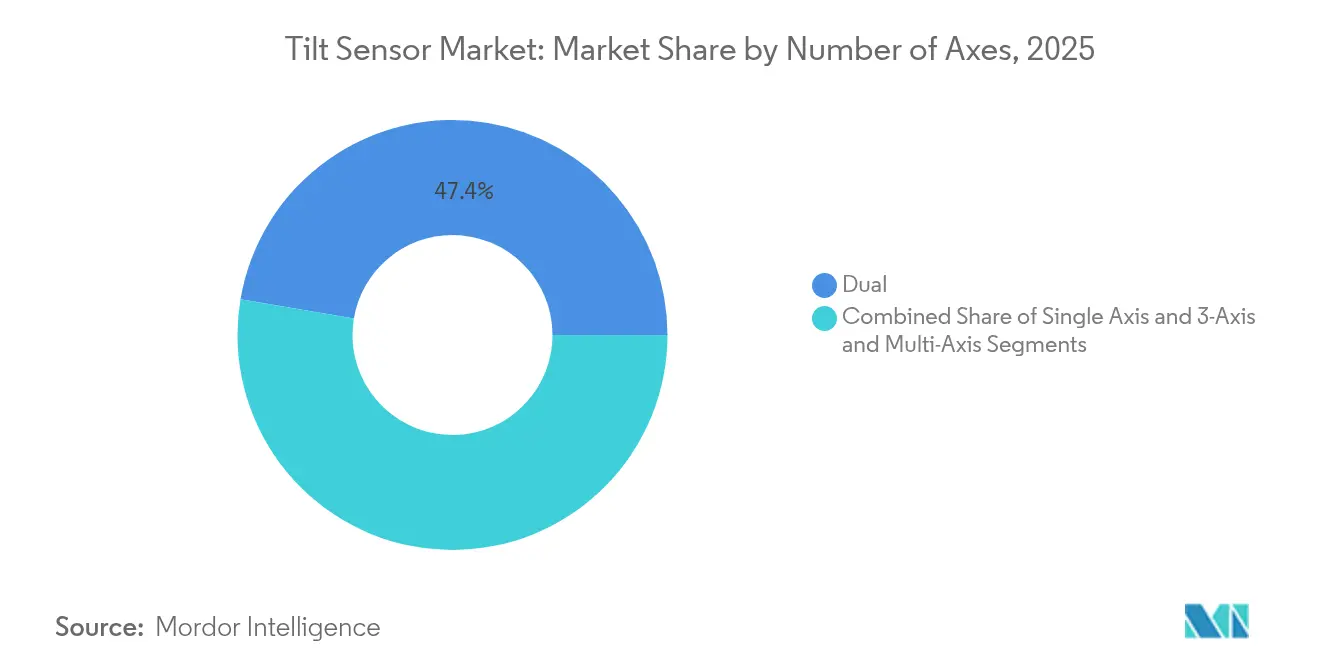

- By number of axes, dual-axis products commanded 47.35% of 2025 revenue, while 3-axis and multi-axis variants are forecast to rise at an 10.42% CAGR.

- By output interface, analog voltage/current models represented 39.62% share in 2025, whereas industrial Ethernet solutions are advancing at a 11.28% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tilt Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Proliferation of MEMS-Based IoT Nodes in Industrial Automation Across Asia | +2.1% | Asia-Pacific, with spillover to North America | Medium term (2-4 years) |

| Mandatory Tilt Monitoring Regulations for Wind Turbine Towers in Europe | +1.8% | Europe, with adoption spreading to North America | Short term (≤ 2 years) |

| Accelerated Deployment of High-Precision GNSS-Guided Construction Equipment in North America | +1.5% | North America, Europe | Medium term (2-4 years) |

| Expansion of Underground Mining Projects in Australia & South America Demanding Rugged Tilt Sensing | +1.3% | Australia, South America | Medium term (2-4 years) |

| Rising Adoption of Active Suspension and Stability Control in Electric Commercial Vehicles | +0.9% | Global, with early adoption in Europe and North America | Long term (≥ 4 years) |

| Telecom 5G mmWave Antenna Alignment Requirements in Urban Skyscrapers (Middle East) | +0.7% | Middle East, with expansion to Asia-Pacific urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Proliferation of MEMS-Based IoT Nodes in Industrial Automation Across Asia

Factory digitalization programs in China, Japan, and South Korea increasingly depend on compact MEMS inclinometers that reveal micro-deflections preceding machine failure. Deployments cut unplanned downtime by 37% and extend wireless-node battery life beyond five years, catalyzing repeat orders as return-on-investment becomes visible.

Mandatory Tilt Monitoring Regulations for Wind-Turbine Towers in Europe

EU safety rules now require continuous inclination tracking, prompting wind-farm operators to retrofit dual-redundant sensor arrays. Power-output losses of 1.5% per 0.5° misalignment and the potential for 2-3% performance gains from blade-pitch optimization encourage rapid compliance.

Accelerated Deployment of High-Precision GNSS-Guided Construction Equipment in North America

Bulldozers and graders fitted with sub-0.1° tilt sensors paired to GNSS receivers cut rework by 60% and lower diesel consumption by 15%. Equipment orders that include factory-installed inclinometers rose 43% in 2024, signalling mainstream acceptance among contractors facing skilled-labour shortages.

Telecom 5G mmWave Antenna Alignment Requirements in Urban Skyscrapers (Middle East)

Urban telecom installers use single-axis tilt sensors to align millimeter-wave panels within ±0.1°, preventing signal degradation caused by the narrow beamwidths of 5G. Demand for retrofit kits is climbing in Doha, Riyadh, and Dubai as operators densify rooftop networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Premium of Force-Balance Sensors vs. MEMS in Cost-Sensitive OEMs | -1.2% | Global, with highest impact in emerging markets | Medium term (2-4 years) |

| Calibration Drift in Fluid-Filled Sensors under Extreme Temperatures | -0.8% | Regions with extreme climates (Middle East, Northern Europe, Canada) | Short term (≤ 2 years) |

| Supply-Chain Concentration of High-End MEMS ASICs in Taiwan Creating Geopolitical Risk | -0.6% | Global, with highest impact on North American and European manufacturers | Medium term (2-4 years) |

| Limited Awareness Among SME Construction Contractors in Africa & Caribbeans | -0.4% | Africa, Caribbean regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Premium of Force-Balance Sensors vs. MEMS in Cost-Sensitive OEMs

Ultrahigh-resolution force-balance devices remain 5–7 times pricier than MEMS units even though they deliver 0.0013° resolution. More than 65% of prospective buyers in India and Indonesia switch to lower-cost MEMS alternatives, restricting the addressable market for premium suppliers.

Calibration Drift in Fluid-Filled Sensors under Extreme Temperatures

Electrolytic inclinometers can drift 0.5° per 10 °C, forcing maintenance crews in Alberta and the Arabian Peninsula to recalibrate up to three times more often than with solid-state devices, inflating lifecycle costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Housing Material: Non-metal Gains in Harsh Environments

Metal housings delivered 66.32% of 2025 revenue, anchoring the tilt sensor market where impact resistance and thermal stability matter. They retain dominance in mining, heavy construction, and high-EMI locations near powerful generators. Meanwhile, non-metal composites are expanding at a 9.84% CAGR as polymer-ceramic blends shed 40% weight and reach IP69K ingress ratings, opening use cases on offshore turbines and marine vessels.

Lightweight corrosion-proof casings permit direct mounting on nacelle structures and drone airframes. Hybrid architectures that combine metal backbones with composite exteriors merge shielding with weight reduction, creating a bridge between legacy and next-generation designs. As a result, designers can embed inclinometers inside moulded polymer components, simplifying assembly and improving long-term reliability. The tilt sensor market size for composite housings is projected to climb steadily as total installed offshore wind capacity accelerates through 2030.

By Technology: Optical Sensing Disrupts Traditional Methods

MEMS held 44.48% market share in 2025 due to established supply chains and attractive price-performance ratios. Yet optical fiber Bragg grating devices are set for 11.43% CAGR as interrogation-unit costs fall 35%, enabling their deployment at substations, rail tunnels, and electric-arc-furnace sites where EMI cripples electronics. These optical units now match the ±0.05° accuracy of premium MEMS while remaining immune to lightning-induced surges.

Force-balance instruments serve scientific and aerospace missions that need 0.001° resolution at any orientation, although their price premium narrows uptake. Fluid-filled electrolytic solutions persist in static-structure monitoring but face drift issues in dynamic or hot-cold cycles. Capacitive designs capture wearables and automotive dashboards where moderate accuracy suffices. Together, these technology tiers keep the tilt sensor market diversified, ensuring customers can align performance with budget.

By Number of Axes: Multi-Axis Solutions Enable Complex Applications

The tilt sensor market size for dual-axis units reached a robust 47.35% share in 2025, mirroring the ubiquity of two-dimensional levelling in scissor lifts and platform stabilizers. The segment expands steadily alongside construction-equipment output. Nevertheless, 3-axis and multi-axis variants are on an 10.42% CAGR trajectory because automation, robotics, and autonomous vehicles need full spatial awareness.

Sensor-fusion algorithms that blend gyroscope and accelerometer data with inclinometer outputs now maintain orientation even during motion. Industrial mobile-robot makers integrate these multi-axis inclination blocks to navigate tight aisles and handle uneven flooring. As factories adopt flexible production cells, the demand for comprehensive orientation sensing supports sustained multi-axis growth, reshaping the tilt sensor market.

By Output Interface: Industrial Ethernet Enables Smart-Factory Integration

Analog current and voltage outputs still command 39.62% revenue in 2025 as legacy PLCs rely on 4–20 mA loops for dependable long-cable transmission. However, industrial Ethernet formats such as Profinet and EtherCAT are scaling at 11.28% CAGR. Plant operators favor deterministic, real-time data for digital-twin models, preventative maintenance, and cloud analytics.

CANopen maintains a foothold in off-highway vehicles while I²C and SPI dominate embedded boards. Wireless links tackle remote mines and solar farms where cabling is impractical. Vendors now layer remote configuration and over-the-air firmware updates on their Ethernet models, reducing field-service calls. This digital shift underpins the broader tilt sensor market transformation toward connected platforms.

By End-User Vertical: Renewable Energy Drives Innovation

Mining and construction contributed 25.58% of 2025 revenue, safeguarding the tilt sensor market foundation through large installed machine fleets. Yet renewable-energy applications are accelerating at 11.74% CAGR, propelled by wind-farm tower monitoring and dual-axis solar trackers that optimize irradiance capture. Each 2-3% turbine-output gain makes premium sensors economically compelling.

Aerospace, defence, and telecommunications consume high-precision devices for navigation, platform stabilization, and mmWave antenna alignment. Automotive OEMs adopt tilt data for battery-pack levelling and rollover detection, especially in electric vehicles. Robotics and factory automation embed inclinometers for adaptive tooling, underpinning smart-manufacturing objectives. Collectively, these verticals diversify income streams and mitigate cyclical exposure.

Geography Analysis

Asia-Pacific held 35.62% of global sales in 2025, benefiting from extensive MEMS fabrication capacity and a vast base of industrial customers. Chinese infrastructure expansion fuels bulk orders for structural-health monitoring, while Japanese factories specify sub-0.1° sensors for precision robotics. South Korean shipyards now integrate inclinometers into hull blocks to track deformation during launch, adding another growth layer. Government incentives for local semiconductor production have trimmed regional device costs by 30%, reinforcing Asia’s price leadership.

South America is the fastest-growing region, with the tilt sensor market forecast to rise 9.62% yearly through 2031. Brazil’s iron-ore giants and Chile’s copper mines deploy wireless inclination arrays on tailings dams after several notable failures. Solar-powered gateways make remote deployments feasible in the Andes and Amazon basin. Infrastructure upgrades across Colombia and Peru further expand addressable demand, especially for landslide-hazard zones that require early-warning systems.

Europe remains a premium market driven by regulation and renewable-energy penetration. Offshore-wind build-outs in the North Sea create sustained pull for IP-rated, corrosion-proof sensors. Germany leads volume shipments thanks to its machinery exports, while the United Kingdom and France accelerate retrofits on aging bridges and tunnels. Integrated monitoring suites that deliver actionable insights rather than raw measurements differentiate local suppliers, cementing Europe’s role as an innovation hub within the tilt sensor market.

Competitive Landscape

The tilt sensor market demonstrates moderate fragmentation. TE Connectivity, Murata, and Honeywell capitalize on broad catalogues and strong distribution relationships in high-volume OEM programs. Jewell Instruments and The Fredericks Company dominate force-balance and electrolytic niches by leveraging decades of application know-how. Meanwhile, semiconductor houses bundle ASIC signal-conditioning and MEMS structures on a single die, shrinking bill-of-materials and challenging module vendors.

Strategic differentiation is shifting toward software. Vendors now bundle calibration routines, temperature compensation, and predictive diagnostics that enhance raw hardware. Patent filings covering micro-lever force amplification and resonant strain-gauge detection show momentum in fundamental sensor-element innovation. Partnerships with automation-platform providers are deepening, because end users increasingly request pre-validated, plug-and-play solutions that reduce integration time and engineering overhead.

Acquisition activity centers on filling technology gaps. Large conglomerates target start-ups with optical or multi-axis specializations to broaden portfolios. Conversely, niche specialists license firmware or ASIC IP to volume manufacturers, accessing scale without heavy capital investment. This collaborative dynamic keeps price competition in check while sustaining a rich pipeline of differentiated offerings, supporting healthy tilt sensor market growth.

Tilt Sensor Industry Leaders

TE Connectivity Ltd.

Murata Manufacturing Co., Ltd.

Sick AG

Pepperl+Fuchs Vertrieb GmbH & Co. KG

IFM Electronic GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: TE Connectivity launched the AXISENSE-G series of dynamic-condition tilt sensors delivering 0.1° accuracy during motion for autonomous construction equipment.

- March 2025: Resensys LLC won a USD 15 million contract to install wireless tilt networks across 250 European wind turbines.

- April 2025: Calypso Instruments paired wind and tilt measurement in one device for renewable-energy monitoring.

- February 2025: Level Developments added EtherCAT and Profinet models to its industrial Ethernet range, easing Industry 4.0 integration.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence treats the global tilt sensor market as the annual revenue generated by stand-alone electronic devices that detect angular displacement on one, two, or three axes and transmit that output through analog or digital interfaces into host systems such as construction equipment, wind-turbine controllers, industrial robots, and vehicle stability modules. Integrated inertial measurement units, purely mechanical bubble levels, and mobile-phone accelerometers fall outside this definition.

Scope exclusion: smartphone motion sensors and full IMUs are not counted.

Segmentation Overview

- By Housing Material Type

- Metal

- Non-metal (Polymer, Ceramic, Composite)

- By Technology

- MEMS

- Force Balance

- Fluid Filled Electrolytic

- Capacitive

- Optical (Fibre Bragg)

- By Number of Axes

- Single-Axis

- Dual-Axis

- 3-Axis and Multi-Axis

- By Output Interface

- Analog Voltage/Current

- Digital (I2C, SPI, UART)

- CAN / CANopen / SAE J1939

- Industrial Ethernet (Profinet, EtherCAT)

- By End-user Vertical

- Mining and Construction

- Aerospace and Defense

- Automotive and Transportation

- Telecommunications Infrastructure

- Industrial Automation and Robotics

- Renewable Energy (Wind, Solar Tracking)

- Marine and Offshore

- Others (Healthcare, Consumer Electronics)

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Argentina

- Rest of South America

- Caribbeans

- Puerto Rico

- Dominican Republic

- Rest of Caribbeans

- Europe

- United Kingdom

- Germany

- France

- Italy

- Nordics

- Rest of Europe

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Rest of Asia-Pacific

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with component suppliers, heavy-equipment OEM engineers, automation system integrators, and regional distributors across North America, Europe, and Asia-Pacific provided live insights on typical sensor volumes, preferred output buses (CAN, Ethernet), warranty failure rates, and forward pricing expectations that secondary data alone could not capture.

Desk Research

Our analysts screened open datasets from agencies such as the U.S. Geological Survey, Eurostat trade files, and the International Energy Agency to size addressable demand in mining machinery, civil infrastructure, and renewable energy. We then layered shipment and ASP indicators gleaned from company 10-Ks, investor decks, and patent families accessed through D&B Hoovers, Dow Jones Factiva, and Questel. Trade association white papers from the Association of Equipment Manufacturers and the International Federation of Robotics helped benchmark penetration rates of MEMS and optical tilt sensing. The sources cited illustrate only a portion of the wider literature consulted for cross-checks and context.

Market-Sizing & Forecasting

A top-down reconstruction began with production and trade data for excavators, wind nacelles, telecom towers, and other anchor applications, which are then adjusted by sensor installation ratios to create the demand pool. Select bottom-up rolls of sampled supplier shipments and channel checks validate totals and resolve gaps. Key variables like average selling price shifts from analog to digital interfaces, MEMS share progression, ANSI A92 safety code adoption, and Asia-Pacific wind-farm additions drive the model. Multivariate regression combined with scenario analysis projects 2025-2030 outcomes while expert feedback fine-tunes elasticity assumptions.

Data Validation & Update Cycle

Outputs pass three-layer variance checks against historical series, peer signals, and prior editions. Senior analysts sign off only after anomalies are reconciled. Reports refresh every twelve months, with interim updates triggered by material events such as a major regulatory change or a supply-chain shock.

Why Mordor's Tilt Sensor Baseline Commands Reliability

Published estimates often diverge because firms pick different device scopes, application sets, and refresh cadences.

Key gap drivers include whether multi-sensor IMUs are blended with tilt-only units, how aggressively ASP erosion is modeled as digital interfaces proliferate, and the frequency of direct phone checks with factory buyers, which Mordor conducts annually while several publishers rely on desk data for longer stretches.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 255 million | Mordor Intelligence | |

| USD 288.7 million | Global Consultancy A | Includes smartphone tilt functions and assumes uniform 6% yearly ASP rise |

| USD 257.65 million | Industry Journal B | Excludes aftermarket replacements and uses 2023 currency averages without inflation adjustment |

These contrasts show that Mordor's disciplined scope selection, live pricing verification, and yearly refresh give executives a balanced, traceable baseline they can rely on for forecasting and strategic planning.

Key Questions Answered in the Report

What is the forecast size of the tilt sensor market by 2031?

The market is projected to reach USD 405.58 million by 2031 on an 8.03% CAGR.

Which region currently leads the tilt sensor market?

Asia-Pacific held 35.62% revenue share in 2025, driven by large-scale industrial automation and local semiconductor manufacturing capacity.

Why are optical fiber Bragg grating tilt sensors growing so quickly?

They offer total immunity to electromagnetic interference and now cost 35% less than earlier generations, enabling deployment near high-voltage equipment.

Which end-user vertical is expanding the fastest?

Renewable energy applications, especially wind-turbine monitoring and solar tracking, are advancing at 11.74% CAGR through 2031.

How are industrial Ethernet interfaces changing the tilt sensor landscape?

Profinet and EtherCAT enable real-time data streaming, remote configuration, and firmware updates, aligning tilt sensors with digital-twin and predictive-maintenance strategies.

What keeps force-balance sensors from wider adoption despite their accuracy?

Their price is 5–7 times higher than comparable MEMS units, which deters cost-sensitive OEMs in emerging markets even when high precision is desirable.

Page last updated on: