Torque Sensor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

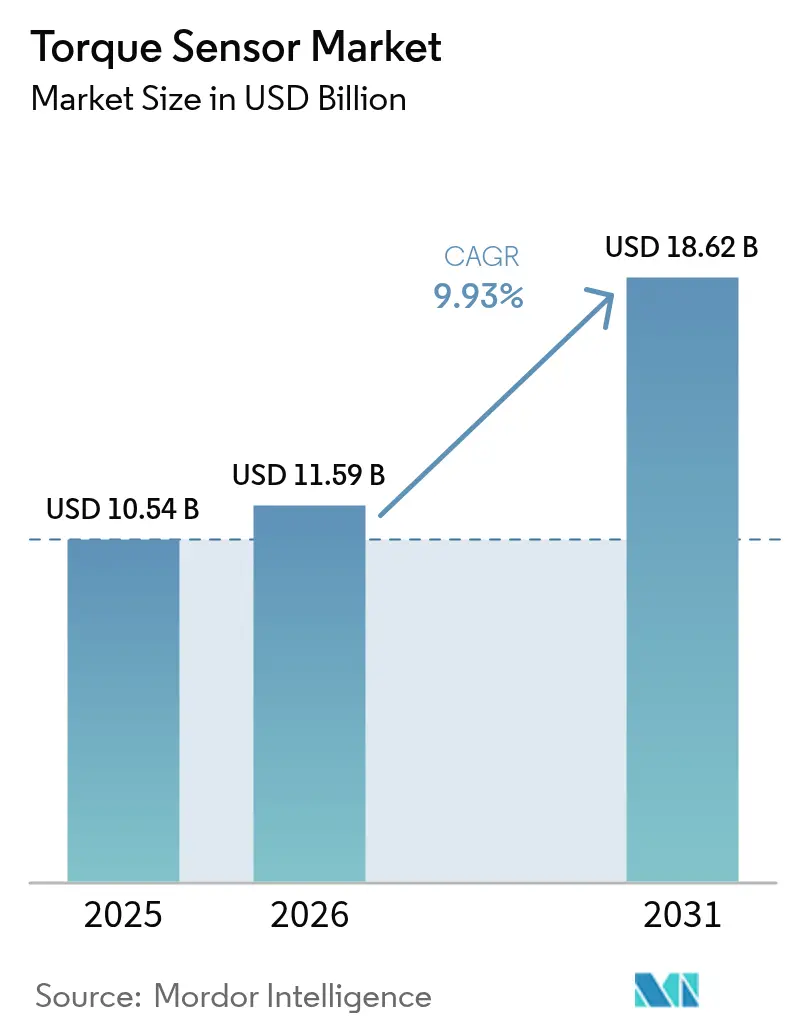

| Market Size (2026) | USD 11.59 Billion |

| Market Size (2031) | USD 18.62 Billion |

| Growth Rate (2026 - 2031) | 9.93% CAGR |

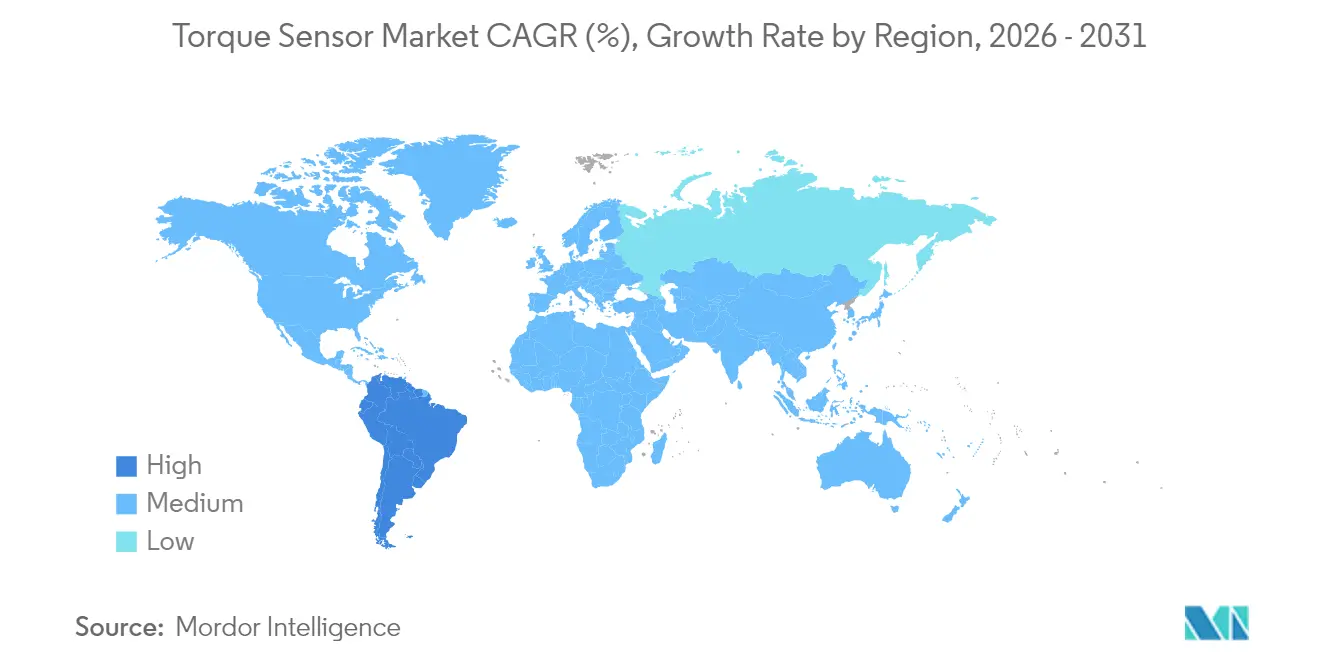

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Torque Sensor Market Analysis by Mordor Intelligence

The global torque sensor market size in 2026 is estimated at USD 11.59 billion, growing from 2025 value of USD 10.54 billion with 2031 projections showing USD 18.62 billion, growing at 9.93% CAGR over 2026-2031. Momentum has been underpinned by the rapid electrification of vehicle powertrains, deepening industrial automation, and stricter precision-measurement requirements in infrastructure, energy and medical equipment. Automotive electrification continued to anchor demand as torque feedback became integral to electric power-steering, drivetrain control and advanced driver-assistance functions. Parallel growth in collaborative robots increased the sensor content per machine, while e-bike and other micromobility platforms multiplied high-volume, low-cost opportunities. Vendors shifted differentiation away from raw accuracy toward electromagnetic-interference resilience, wireless telemetry, and integration with predictive-analytics platforms. Supply chain exposure to high-grade magnetoelastic alloys remained a limiting factor, although regional sourcing initiatives in India and South America sought to ease dependence on Chinese rare-earth metals.

Key Report Takeaways

- By product type, rotational sensors held 64.78% of torque sensor market share in 2025, while reaction sensors posted the fastest 11.32% CAGR to 2031

- By technology, strain-gauge devices led with 47.85% revenue share in 2025; surface acoustic wave sensors are on track for a 12.74% CAGR through 2031

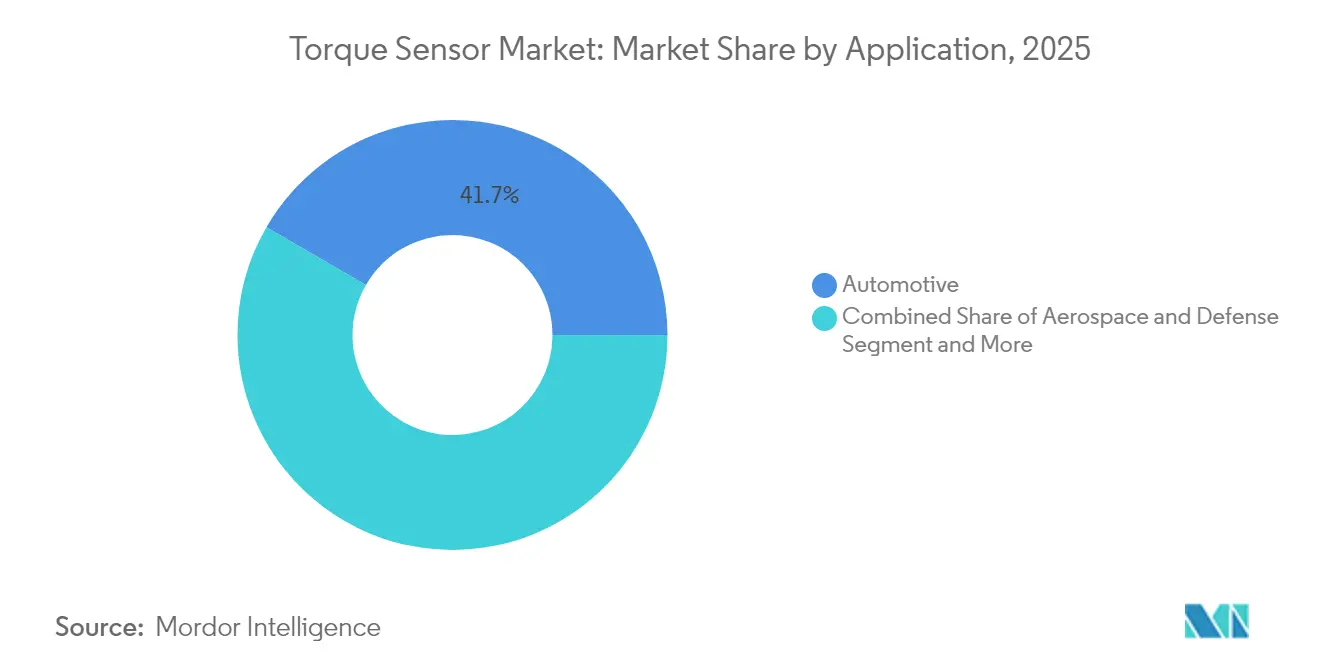

- By application, automotive accounted for 41.65% of the torque sensor market size in 2025; medical and healthcare robotics are set to expand at a 13.52% CAGR to 2031

- By end-user industry, OEM test-stand and QA dominated with 43.76% share of the torque sensor market size in 2025, while in-process monitoring is growing at 11.65% CAGR

- By geography, Asia-Pacific led with 35.92% of torque sensor market share in 2025; South America is projected to record the quickest 10.98% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Torque Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification of power-steering systems | +2.8% | North America, Europe, China | Medium term (2-4 years) |

| Rising automation and cobots in manufacturing | +2.1% | Asia-Pacific core; spill-over to North America, Europe | Long term (≥ 4 years) |

| Surge in e-bike and micromobility production | +1.9% | Europe, Asia-Pacific; emerging North America | Short term (≤ 2 years) |

| Growing use in axial-flux EV motors | +1.4% | Global; early adoption in premium EVs | Medium term (2-4 years) |

| On-board monitoring in smart wind turbines | +0.7% | Europe, North America, global offshore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electrification of Power-Steering (EPS) Systems

Mandated torque monitoring for electric power-steering hardened demand even during economic slow-downs. European regulations issued in 2024 required continuous steering-torque feedback for autonomous-readiness, obligating every EPS unit to embed at least one sensor. OEMs adopted dual-redundant designs to satisfy functional-safety targets, effectively doubling sensor volumes per vehicle. Suppliers such as Vitesco cited EPS torque sensing as a core enabler for semi-autonomous lane-keeping and driver-intention prediction. [1]Vitesco Technologies, “Trend Report 2024,” vitesco-technologies.com The same data channel is reused in over-the-air analytics, increasing lifetime service revenue for integrators. As legacy hydraulic steering platforms sunset, the addressable automotive base shifted irreversibly toward EPS architectures.

Rising Automation and Cobots in Manufacturing

Collaborative robots required instantaneous torque detection to comply with ISO 10218 safety limits, creating a one-to-one relationship between cobot shipments and sensor units. Global cobot sales outpaced conventional industrial robots in 2024, inducing a steep ramp in EMI-resistant, multi-axis torque sensors destined for electronics, food and light-assembly lines. Certification guidelines enforced redundant sensing, effectively raising bill-of-materials value for each robot. Penetration remained only 26% among Polish SMEs in 2024, illustrating vast latent upside across European manufacturing. Long-term impact spans beyond discrete automation as smart work-cells propagate into textile and agri-processing plants.

Surge in E-Bike and Micromobility Production

Torque-based pedal-assist systems achieved regulatory preference in European markets, obligating accurate measurement of rider effort for legal speed cut-offs. Magnetic position sensors have begun replacing strain-gauges on entry-level models to ease calibration and assembly costs. Producer volumes rose sharply as urban congestion policies pushed commuters toward e-bikes and lightweight cargo trikes. Each vehicle integrates at least one crank or rear-hub torque unit, ensuring proportional growth between unit shipments and sensor demand. Rapid iteration cycles in consumer mobility encouraged module-level standardization, supporting scalable supply for Asia-based contract manufacturers.

Growing Use in Axial-Flux Motors for EV Drivetrains

Axial-flux designs delivered double the power density of radial motors yet required fine torque control to manage distinctive magnetic saturation behaviors. Prototype passenger-car platforms entering pre-series production in 2024 added shaft-end or stator-embedded sensors to capture real-time torque ripple for inverter optimization. Smaller gear ratios amplified the importance of direct drive monitoring, and premium EV brands positioned axial-flux torque feedback as a ride-quality differentiator. Research in 2025 confirmed that optimized axial-flux motors achieved superior lumped-parameter performance once equipped with closed-loop torque measurement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity in volume automotive programs | -1.6% | Global; acute in emerging markets | Short term (≤ 2 years) |

| Reliability issues under electromagnetic interference | -0.9% | Global; larger impact in industrial, aero | Medium term (2-4 years) |

| Supply bottlenecks for high-grade magnetoelastic alloys | -0.7% | Asia-Pacific-centered supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity in Volume Automotive Programs

OEM cost-down targets capped sensor pricing near USD 50 per unit in mainstream EV platforms, pressuring suppliers to strip auxiliary features. The need to offset battery-pack costs heightened scrutiny of every drivetrain component, with platform standardization further commoditizing specifications. Rare-earth magnet supply disruptions in 2024 exacerbated the dilemma, forcing Indian and South American automakers to weigh substitute materials that risked lower precision. Suppliers countered with modular electronics, allowing optional conditioning boards for premium trims while preserving a low-cost core for entry variants.

Reliability Issues under Electromagnetic Interference

High-voltage inverters and fast-switching power electronics in EVs and industrial drives generated EMI levels capable of distorting millivolt-level torque signals. A 2025 study showed an 87.5% enhancement in computational efficiency after implementing predictive EMI-suppression algorithms, though additional shielding and filtering raised total system cost. [2]HBK, “Torque Measurement in Wind Turbines,” hbkworld.com Aerospace and UAV programs cited similar interference-induced mis-reads that compromised fly-by-wire redundancies. The trade-off between cable-based strain-gauges and wireless SAW or optical architectures remained unresolved for many volume customers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rotational Sensors Dominate Applications

Rotational units captured 64.78% of torque sensor market share in 2025 on the strength of drivetrain, wind-turbine and process-control deployments. They offered continuous, in-situ measurement that supported closed-loop control in EVs and turbines. Reaction types, while smaller in base, posted an 11.32% CAGR as automated test-stands proliferated across machining and battery-cell wrap processes. Digital telemetry elevated rotational designs by removing slip rings, boosting reliability in harsh industrial settings.

Rotational sensors evolved into edge-computing nodes, streaming data to cloud dashboards for predictive maintenance. In-process machining adopted reaction units to catch torque spikes indicative of tool wear, advancing zero-defect programs in aerospace structural milling. The torque sensor market benefits as OEMs retrofit older assembly lines to meet traceability mandates, ensuring both sensor categories sustain parallel growth.

By Technology: Strain-Gauge Leadership Faces SAW Challenge

Strain-gauges retained 47.85% revenue in 2025, favored for cost and proven ruggedness. Yet, SAW sensors recorded a 12.74% CAGR and gained share where EMI immunity and wireless data mattered most. Magnetoelastic variants served sealed, non-contact duties in pump shafts, whereas optical fibers targeted lab and aerospace calibration where nano-radian resolution justified premium pricing.

SAW innovations in 2024 achieved temperature tolerance to 1,000 °C and 10 µm displacement resolution. Such capabilities unlocked extreme-environment markets like gas turbines and deep-well drilling. The torque sensor market thus witnessed technology bifurcation: low-cost strain-gauges for commoditized automotive steering, and high-value SAW or optical units for hazardous or mission-critical niches.

By Application: Automotive Leads, Healthcare Accelerates

Automotive applications commanded 41.65% of torque sensor market size in 2025, buoyed by EPS and traction-motor control loops. Medical and healthcare robotics, however, registered the swiftest 13.52% CAGR to 2031 as surgical platforms multiplied across private hospitals. Aerospace turbine testing and industrial manufacturing held mid-single-digit trajectories, supported by Industry 4.0 retrofits.

Surgical-robot OEMs embedded multi-axis strain-gauges at each joint to assure haptic feedback fidelity, driving per-system sensor counts higher than in automotive steering columns. Regulatory scrutiny over patient safety cemented torque sensing as a non-negotiable bill-of-materials line item, accelerating the torque sensor market across healthcare use cases.

By End-User Industry: OEM Testing Dominates, In-Process Monitoring Surges

OEM laboratory and end-of-line test-stands accounted for 43.76% share of the torque sensor market size in 2025 thanks to stringent validation protocols in automotive, aerospace and energy sectors. In-process monitoring logged a 11.65% CAGR, mirroring the shift from post-hoc QC toward real-time control envisioned in Industry 4.0 roadmaps.

Digital performance-management pilots in 2024 showed torque data outperforming legacy OEE indices for early fault detection. Cloud-linked sensors enabled hour-level drill-downs into spindle performance, reducing unplanned downtime. As manufacturers standardize such analytics, sensor volumes will decouple from new-equipment sales and follow retrofit cycles instead.

Geography Analysis

Asia-Pacific generated 35.92% of 2025 revenue and sustained leadership through dense automotive assembly, semiconductor fabrication and robotics adoption. China led EPS volumes, Japan supplied precision strain-gauge substrates, and South Korea’s electronics majors deployed high-resolution torque feedback in battery and display lines. India’s push to localize rare-earth magnet production, with 500-tonne annual capacity targeted by 2026, promised to moderate raw-material risk across the region.

North America maintained its premium niche as aerospace and defense integrators employed high-temperature optical sensors for engine testing. US EV start-ups leveraged axial-flux motors requiring sophisticated torque control loops, bolstering demand for SAW and magnetoelastic devices. Mexico’s growing role as an automotive export hub amplified mid-volume, cost-sensitive orders for steering and drivetrain sensing.

Europe advanced steadily on regulatory mandates that embedded torque measurement into collaborative robot safety standards and vehicle autonomous-readiness rules. Germany’s automation vendors integrated sensor gateways into programmable-logic controllers, while France’s nuclear maintenance contractors adopted wireless torque heads to accelerate outage turnarounds. South America, led by Brazil, posted the fastest 10.98% CAGR as OEMs installed new stamping and powertrain lines requiring extensive test-stand instrumentation.

Competitive Landscape

The torque sensor market remained moderately fragmented: the top five suppliers controlled roughly 45% of revenue, leaving space for specialist challengers. ABB packaged sensors within full electric-drive solutions, leveraging its USD 32.2 billion motion portfolio to cross-sell into factory retrofits. Honeywell exploited aerospace certifications to sustain premium pricing in extreme-temperature programs. [4]Honeywell, “Aerospace,” honeywell.com TE Connectivity’s automotive dominance helped push lower-cost strain-gauges into emerging-market steering assemblies.

Kistler capitalized on dynamic measurement expertise to win EV powertrain test benches, while Sensor Technology’s 2025 launch of compact split-head TorqSense offered installers a drop-in option for cramped driveline architectures. Smaller firms carved niches around wireless SAW modules and cloud analytics, often partnering with MES vendors to bundle data dashboards. Competition thus pivoted on integration agility and EMI resilience more than on baseline accuracy, resetting differentiation rules in the torque sensor market.

Torque Sensor Industry Leaders

ABB Ltd

Crane Electronics Ltd

Honeywell International

Hottinger Brüel & Kjær (HBK – Spectris plc)

Applied Measurements Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: TDK expanded temperature and magnetic sensor lines for automotive and industrial platforms, reinforcing multi-sensor integration trends.

- March 2025: Sensor Technology unveiled TorqSense SGR530/540 with detachable heads for tight EV drivelines.

- January 2025: HBK issued rotating torque-sensor selection guidelines to reduce field failures.

- December 2025: European factories deployed AI-enabled in-process inspection systems incorporating torque sensors for zero-defect goals.

Global Torque Sensor Market Report Scope

The study tracks revenues generated by vendors manufacturing and providing torque sensors for various applications in industries, such as automotive, aerospace and defense, and manufacturing, among others. Actuators are excluded from the scope of the study, and transducers mentioned in the study are exclusively for sensors. Further, the market estimation tracks the revenue from torque sensors offered to different end-user applications' customers. The revenues tracked for the study exclusively include hardware. Moreover, torque sensors used in surgical robots are considered under the medical application segment. In contrast, other robots, such as collaborative robots that use torque sensors, are considered under the other applications segment. The report covers and analyses the impact of the COVID-19 pandemic on the market, its stakeholders, and the same has been considered while arriving at the current market estimation and for future projections.

| Reaction Torque Sensors |

| Rotational / Rotary Torque Sensors |

| Strain-Gauge |

| Magnetoelastic |

| Optical |

| SAW (Surface Acoustic Wave) |

| Others |

| Automotive |

| Aerospace and Defense |

| Industrial Manufacturing and Robotics |

| Medical and Healthcare |

| Energy and Power |

| OEM Test-Stand and QA |

| In-Process Monitoring |

| Research and Development |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Reaction Torque Sensors | ||

| Rotational / Rotary Torque Sensors | |||

| By Technology | Strain-Gauge | ||

| Magnetoelastic | |||

| Optical | |||

| SAW (Surface Acoustic Wave) | |||

| Others | |||

| By Application | Automotive | ||

| Aerospace and Defense | |||

| Industrial Manufacturing and Robotics | |||

| Medical and Healthcare | |||

| Energy and Power | |||

| By End-User Industry | OEM Test-Stand and QA | ||

| In-Process Monitoring | |||

| Research and Development | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What was the global torque sensor market size in 2026 and where is it heading?

The market reached USD 11.59 billion in 2026 and is projected to hit USD 18.62 billion by 2031, reflecting a 9.93% CAGR.

Which segment holds the largest torque sensor market share today?

Rotational sensors led with 64.78% share in 2025, driven by drivetrain and turbine uses.

Why are torque sensors critical for electric power-steering systems?

EPS platforms rely on continuous torque feedback to modulate motor assistance and fulfil autonomous-readiness safety rules.

Which region is growing fastest for torque sensors?

South America is forecast to expand at 10.98% CAGR through 2031 on rising manufacturing investment.

How are collaborative robots influencing torque sensor demand?

Cobots mandate redundant torque sensing for human-safety compliance, increasing sensor content per robot and driving long-term demand.

Page last updated on: