Motion Sensor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.69 Billion |

| Market Size (2031) | USD 3.36 Billion |

| Growth Rate (2026 - 2031) | 4.61% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Motion Sensor Market Analysis by Mordor Intelligence

The motion sensor market size is expected to grow from USD 2.57 billion in 2025 to USD 2.69 billion in 2026 and is forecast to reach USD 3.36 billion by 2031 at 4.61% CAGR over 2026-2031. Consistent demand created by mandatory automotive safety systems, rising smart-home deployments, and the semiconductor sector’s cyclical rebound underpins this steady expansion. Government safety regulations in the United States and European Union continue to standardize technology requirements, giving suppliers clear production roadmaps. Parallel growth in edge artificial intelligence and ultra-low-power design shortens upgrade cycles, while incremental innovations in multi-axis solutions sustain pricing power. Competitive intensity remains moderate as vertically integrated chipmakers leverage in-house design, packaging, and software stacks to secure design wins.

Key Report Takeaways

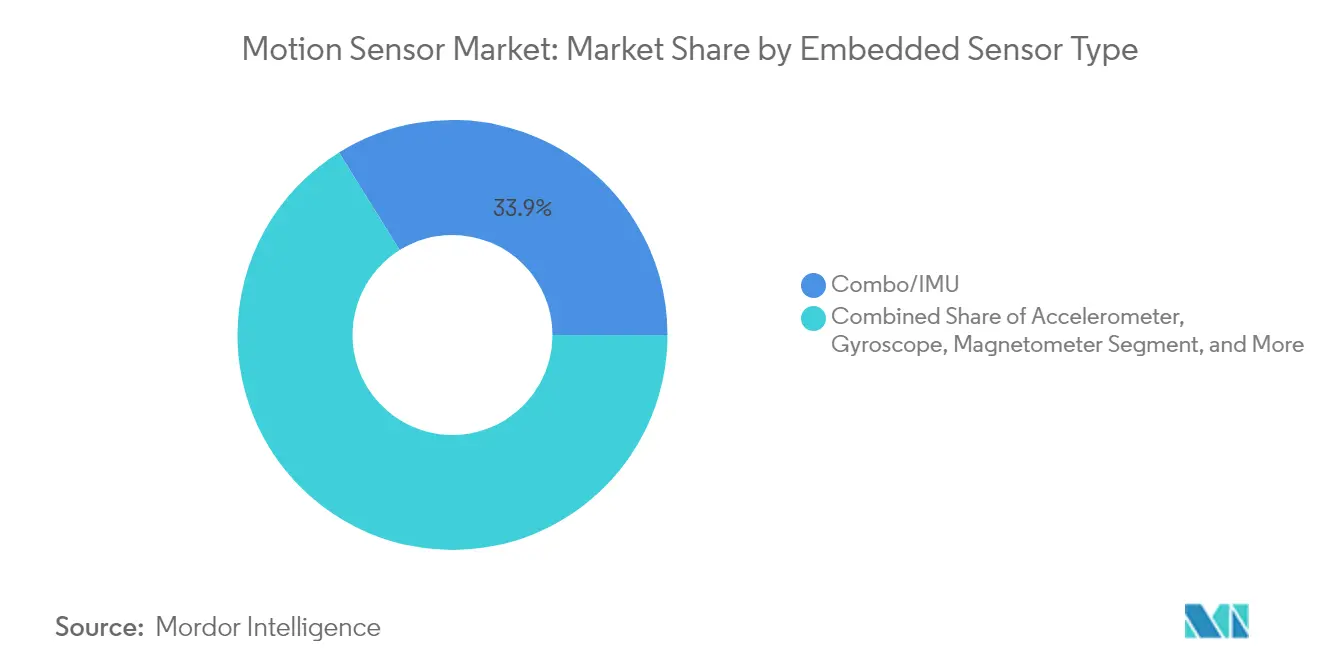

- By embedded sensor type, Combo/IMU solutions captured 33.85% of motion sensor market share in 2025 and are advancing at a 4.72% CAGR through 2031.

- By application, consumer electronics led with 41.65% revenue share in 2025, while smart-home and building automation is projected to expand at a 6.88% CAGR to 2031.

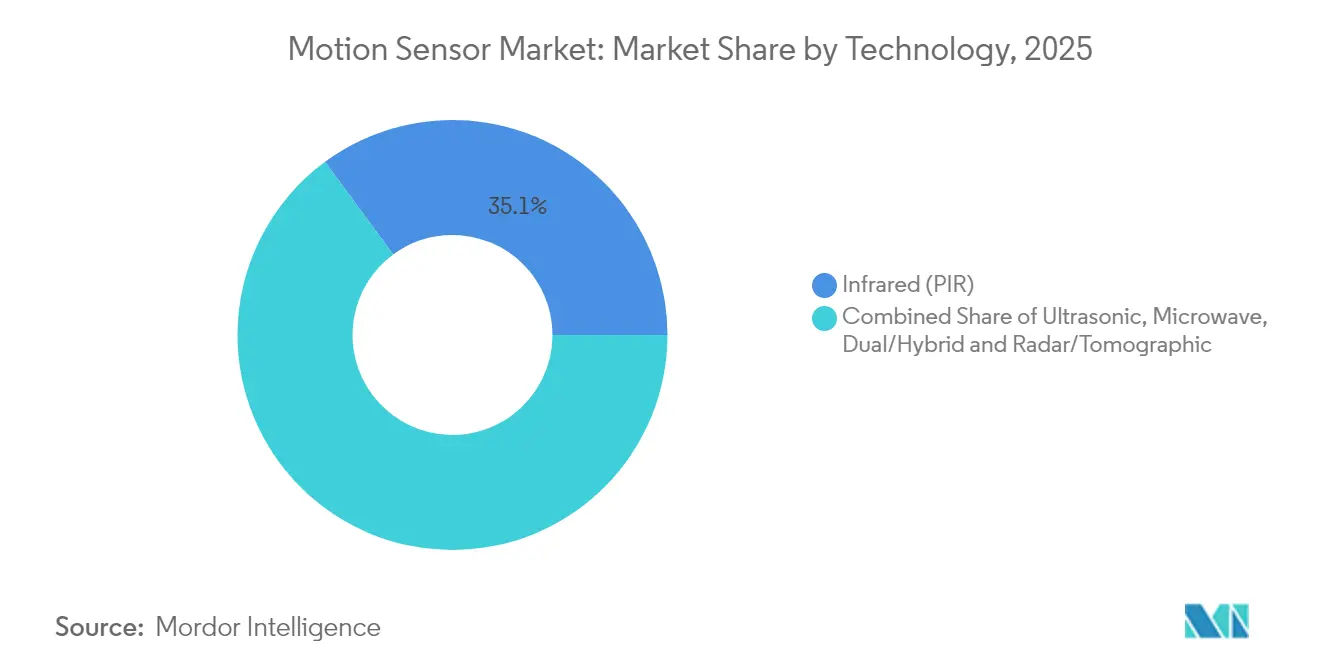

- By technology, infrared sensors held 35.10% share of the motion sensor market size in 2025; radar/tomographic solutions post the fastest CAGR at 5.42% through 2031.

- By functionality, fully automatic systems accounted for 55.70% share of the motion sensor market size in 2025 and are growing at 4.95% CAGR between 2026-2031.

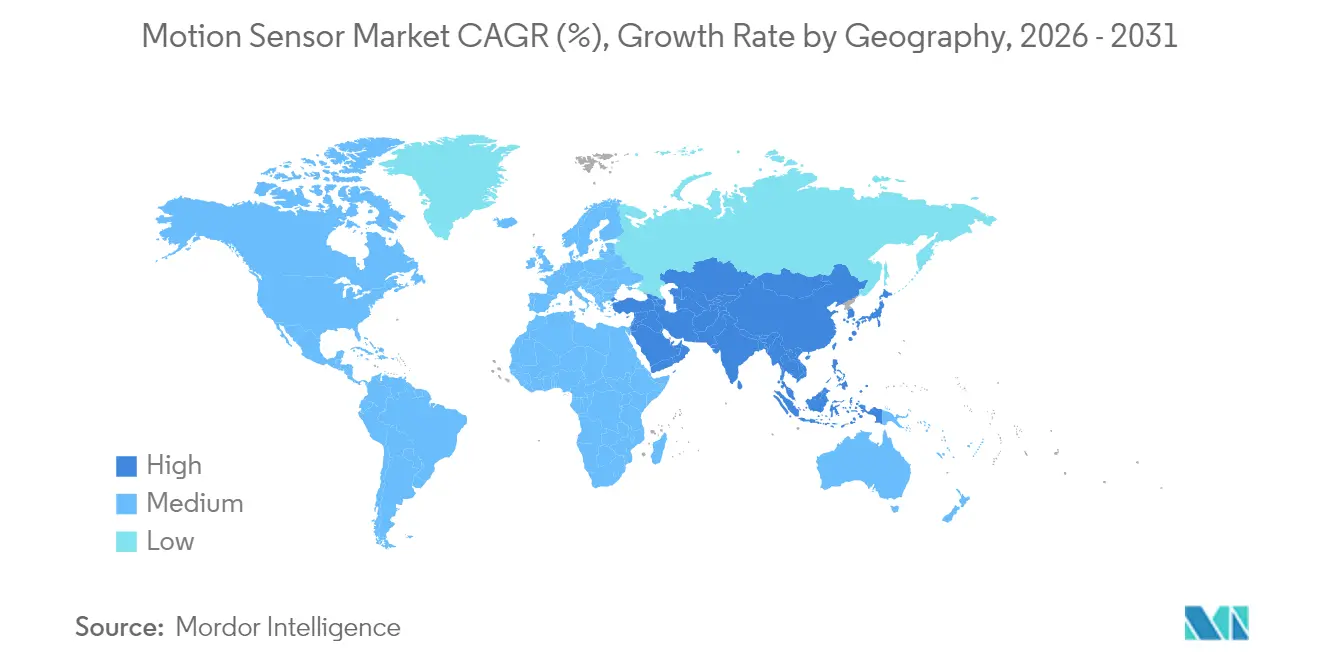

- By geography, Asia-Pacific dominated with 36.95% revenue share in 2025, whereas the Middle East & Africa region is forecast to record the highest 5.04% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Motion Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| MEMS penetration in automotive and mobile devices | +1.2% | Global (APAC, North America) | Medium term (2-4 years) |

| Surge in motion-enabled gaming and AR/VR | +0.8% | North America, EU, expanding to APAC | Short term (≤ 2 years) |

| Smart-home and building-automation rollout | +1.1% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Edge-AI ultra-low-power sensor innovations | +0.6% | North America & EU technology hubs | Long term (≥ 4 years) |

| Wearable and IoT sensor-fusion demand | +0.7% | Global urban centers | Medium term (2-4 years) |

| ADAS-mandate-led demand for inertial combos | +1.0% | Global, regulation driven | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

MEMS Penetration in Automotive and Mobile Devices

Regulators have locked in long-range roadmaps for advanced driver assistance functions, and each incremental feature requires added inertial sensing. The National Highway Traffic Safety Administration’s 2024 decision to rate vehicles on blind-spot, lane-keeping, and pedestrian automatic braking incentives ensures that each new model refresh carries more motion sensing content.[1]National Highway Traffic Safety Administration, “New Car Assessment Program Final Decision Notice-Advanced Driver Assistance Systems and Roadmap,” nhtsa.govSmartphone vendors meanwhile embed multiple micro-electro-mechanical sensors to power augmented reality interfaces and gesture controls, creating overlapping demand cycles that cushion suppliers from sector-specific slowdowns. Vertically integrated chipmakers benefit most because they can shift foundry capacity between automotive and mobile runs without redesigning core sensor elements. Centralized vehicle compute architectures may temper total unit volumes later in the decade, yet higher per-device complexity should offset any volume erosion.

Surge in Motion-Enabled Gaming and AR/VR

Immersive gaming platforms need sub-millisecond tracking accuracy; a 2025 study showed that acoustic injection attacks can mislead inertial measurement units in leading headsets, distorting virtual content and inducing motion sickness These vulnerabilities spur demand for redundant sensor arrays and secure fusion algorithms that raise overall bill-of-materials value. Controller vendors, exemplified by haptic-rich console accessories, already combine accelerometers, gyroscopes, and capacitive touch to improve realism. As mixed-reality adoption spreads to enterprise training and field maintenance, the motion sensor market gains a diversified customer base that is less tied to consumer spending cycles.

Smart-Home and Building-Automation Rollout

Commercial smart-building pilots have demonstrated average electricity savings of 36.8 kW per site by using networked motion detectors to tailor HVAC and lighting schedules.[2]Hakilo Sabit and Thit Tun, “IoT Integration of Failsafe Smart Building Management System,” mdpi.com Sony’s 2024 deployment of edge-AI vision detection in 500 Japanese convenience stores highlights how retailers use privacy-preserving analytics to optimize labor and reduce energy costs without exporting raw video.[3]Sony Semiconductor Solutions, “Edge AI-Driven Vision Detection Solution Introduced at 500 Convenience Stores in Japan,” sony-semicon.comAs payback periods shorten, building owners integrate multiple sensing modalities-passive infrared, radar, and vision-to cover varied occupancy scenarios. Federated learning frameworks further allay privacy concerns by keeping data on-premise, though higher system complexity raises integrator skill requirements and may slow uptake among smaller installers.

Edge-AI Ultra-Low-Power Sensor Innovations

Industrial maintenance now favors embedded analytics at the sensor node rather than streaming vibration data to cloud engines. Analog Devices’ Voyager4 platform illustrates this shift by combining a MEMS accelerometer with local machine-learning inference to flag bearing faults in real time while extending battery life.[4]Analog Devices, “Designing Edge Sensors with Artificial Intelligence-Part 1,” analog.comThe Semiconductor Research Corporation’s decadal plan singles out intelligent sensing as a strategic priority, reinforcing US federal funding proposals to underwrite domestic R&D and shorten supply chains. Success in merging AI cores and motion detection will depend on continued breakthroughs in sub-threshold circuitry and neuromorphic co-processors that limit heat dissipation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced MEMS alternatives | -0.9% | Global, price-sensitive markets | Medium term (2-4 years) |

| Semiconductor supply-chain bottlenecks | -0.7% | Global, acute in APAC | Short term (≤ 2 years) |

| Privacy backlash against ubiquitous sensing | -0.5% | EU & North America | Long term (≥ 4 years) |

| Calibration drift in multi-axis IMUs | -0.4% | Global precision-critical use cases | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced MEMS Alternatives

Photonic and quantum-scale motion sensors promise ten-fold precision gains but remain several cost curves away from high-volume deployment. Packaging complexity and lack of common test standards inflate per-unit pricing, deterring adoption in commodity smart-lighting and budget appliance lines. Research groups are pursuing machine-learning-based calibration schemes that reduce production tuning steps to under 10 seconds while maintaining accuracy. Widespread commercialization, however, depends on shared manufacturing infrastructure that can amortize capital outlays across multiple sensor families.

Semiconductor Supply-Chain Bottlenecks

The United States still relies on offshore fabrication for complementary metal–oxide–semiconductor (CMOS) image sensors used in automotive and security cameras, exposing OEMs to geopolitical risk. Policy measures such as the CHIPS for America Act and the European Chips Act aim to localize lithography and packaging, yet greenfield fabs typically take three to five years to reach volume. Just-in-time inventories prevalent in automotive manufacturing magnify the impact of any wafer shortage, forcing OEMs to redesign platforms around more readily available sensor combinations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Infrared Stability, Radar Upswing

Passive infrared devices held 35.10% share of the motion sensor market size in 2025 due to low cost and proven reliability in lighting automation. Adoption of radar-based tomographic systems is growing at a 5.42% CAGR because millimeter-wave chips offer material penetration and object-classification advantages needed for advanced automotive safety.

Infrared shipments remain high for budget security installations, but multi-technology nodes that blend radar with PIR are emerging in premium residential kits. Laboratories are also refining segmented thermal calibration for MEMS gyroscopes, trimming drift across temperature swings and thereby widening usable ranges for high-end robotics. Photonic interference sensors under early trial could eventually disrupt both radar and infrared if packaging barriers fall.

By Functionality Level: Automation Preference

Fully automatic systems commanded 55.70% share in 2025, reflecting buyer preference for “install-and-forget” devices that optimize lighting, HVAC, or driver assistance without human input. The segment’s 4.95% CAGR rests on expanding smart-building retrofits where self-learning algorithms reduce commissioning labor.

Semi-automatic designs endure in industrial lines requiring manual overrides, yet the gradual rollout of AI-enabled auto-calibration trims their configuration time. Edge inference engines now embedded in sensors shrink latency from hundreds of milliseconds to single-digit milliseconds, meeting stricter safety thresholds for collaborative robots on factory floors.

By Embedded Sensor Type: IMU Consolidation

Combo inertial measurement units account for 33.85% share of the motion sensor market and are growing at 4.72% CAGR as designers consolidate accelerometers, gyroscopes, and magnetometers to cut board area. Stand-alone accelerometers and gyros continue in ultra-cost-sensitive toys and appliances, yet sophisticated wearables now depend on fused, nine-axis devices to improve gesture resolution.

Academic work on joint magnetometer-IMU calibration reduces heading error by applying maximum a-posteriori algorithms that run on microcontrollers, yielding high precision without cloud aid. Remaining challenges include long-term bias drift, which demands periodic field calibration or adaptive filtering.

By Application: Consumer Electronics Lead, Smart Homes Accelerate

Consumer electronics maintained 41.65% share of the motion sensor market in 2025, spanning smartphones, tablets, and game controllers. Growth remains solid yet incremental as penetration nears saturation. Smart-home and building automation, by contrast, advances at 6.88% CAGR, underpinned by energy codes and corporate decarbonization targets that reward sensor-based occupancy management.

Healthcare monitors benefit from progress in micro-flow sensing, allowing wearable patches to capture joint angles and acceleration for remote rehabilitation programs. Security integrators increasingly bundle motion detection with AI video analytics to cut nuisance alarms, opening a mid-tier channel between entry-level DIY kits and enterprise surveillance suites.

Geography Analysis

Asia-Pacific generated 36.95% of motion sensor market revenue in 2025, enabled by dense electronics supply chains in China, Japan, and South Korea. Local fabs specialize in bulk CMOS and wafer-level chip-scale packaging, allowing regional OEMs to launch new sensor-rich mobile devices on compressed timelines. Regulatory pushes for advanced driver assistance systems in Japan and South Korea further reinforce baseline demand.

North America and Europe remain technology pace-setters rather than high-volume production centers. The U.S. New Car Assessment Program revisions obligate automakers to integrate blind-spot detection, lane-keeping, and pedestrian braking, guaranteeing a multi-year uplift for inertial combos and radar subsystems. Europe’s General Safety Regulation II places similar requirements on new car models sold from mid-2024 onward, synchronizing demand across both mature markets.

The Middle East & Africa, though only a modest share contributor today, is projected to grow at 5.04% annually to 2031 as Gulf smart-city budgets prioritize intelligent lighting, security, and traffic-monitoring infrastructure. Broad-spectrum motion sensors suited to harsh desert climates gain traction in large-scale perimeter security installations and rapid-transit projects. Local assembly partnerships help circumvent import tariffs and align with regional content rules.

Competitive Landscape

The motion sensor market displays moderate concentration. Tier-one semiconductor houses integrate design, wafer processing, and software toolchains, enabling them to bundle inertial combos with power management and wireless subsystems for smart-edge nodes. Sony’s expansion into edge AI vision, Analog Devices’ condition-monitoring suite, and Infineon’s automotive safety focus exemplify diversified strategic bets.

Smaller innovators target photonic gyroscopes and quantum tunneling accelerometers, but high capital intensity and lengthy qualification cycles limit their immediate competitive threat. Collaboration models such as SEMI’s MEMS & Sensors Executive Congress foster co-development of packaging standards that shorten time-to-revenue for niche suppliers.

Strategic alliances between sensor vendors and AI accelerator startups accelerate feature integration at the edge, allowing incumbents to upsell value-added firmware updates. Privacy-preserving designs are emerging as a new differentiation axis, particularly for European enterprise customers who must comply with the General Data Protection Regulation. Supply-chain relocation incentives in the United States and Europe could re-rank leaders if onshore capacity lags demand spikes.

Motion Sensor Industry Leaders

Murata Manufacturing Co. Ltd

Analog Devices Inc

NXP Semiconductor NV

TDK Corporation

Bosch Sensortec GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Researchers documented acoustic injection attacks on IMUs inside leading XR headsets, prompting calls for tamper-resistant sensor architectures.

- November 2024: NHTSA added four ADAS functions to its New Car Assessment Program, locking sensor requirements through 2033.

- July 2024: EU General Safety Regulation II took effect, mandating emergency braking and driver-state monitoring in new vehicles.

- April 2024: Sony Semiconductor rolled out edge AI vision detection across 500 Japanese convenience stores

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the motion sensor market as the revenue generated from standalone or embedded devices that detect object or human movement through active (ultrasonic, microwave, radar / tomographic) or passive (infrared, MEMS inertial) principles and ship inside consumer electronics, automotive safety systems, building-automation nodes, and industrial equipment.

Scope exclusion: modules purely supplying camera image data without motion-specific functionality are not included.

Segmentation Overview

- By Technology

- Ultrasonic

- Microwave

- Infrared (PIR)

- Dual/Hybrid

- Radar/Tomographic

- By Functionality Level

- Fully Automatic

- Semi-Automatic

- By Embedded Sensor Type

- Accelerometer

- Gyroscope

- Magnetometer

- Combo/IMU (6-axis, 9-axis)

- Pressure/Barometric

- By Application

- Consumer Electronics

- Automotive and Transportation

- Healthcare and Medical Devices

- Security and Surveillance

- Lighting Controls

- Smart Home and Building Automation

- Industrial and Robotics

- Gaming and Entertainment

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- South East Asia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- Turkey

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts subsequently interview fabrication service providers in East Asia, module integrators across Europe and North America, and procurement managers at appliance, lighting, and Tier-1 automotive firms. These conversations confirm technology adoption rates, average selling prices, inventory corrections, and regional design-win pipelines that secondary sources rarely capture.

Desk Research

We initiate every cycle by mining publicly available tier-1 sources such as the International Trade Center's export codes for MEMS and infrared modules, US ITC and Eurostat production indices for electronic components, United Nations Comtrade shipment data, and statistics from industry bodies like the Semiconductor Industry Association and OICA. Company 10-Ks, investor decks, major trade-press articles, and patent volumes accessed via Questel further anchor supply visibility. D&B Hoovers screens corporate revenue splits that help separate motion sensing lines from broader sensor portfolios. The sources listed illustrate our foundation; many additional references guide validation, clarification, and context gathering.

Market-Sizing & Forecasting

Our core model begins with a top-down reconstruction of annual demand pools using production volumes of smartphones, vehicles, smart-home nodes, and industrial robots, matched with sensor penetration ratios suggested by primary interviews. Results are then corroborated through selective bottom-up roll-ups of leading supplier revenues and sampled ASP × unit calculations to refine totals. Key variables like smartphone output, ADAS attach rates, residential IoT node growth, semiconductor silicon wafer starts, and average combo-sensor pricing drive both historical estimates and projections. Multivariate regression with scenario analysis projects each variable, and ARIMA smoothing checks short-term inflections. Where bottom-up gaps exist, ratios from the most comparable peer group are applied before cross-checks.

Data Validation & Update Cycle

Outputs undergo three-step analyst review, anomaly scans against independent KPIs, and variance thresholds that trigger re-contact of experts. Reports refresh annually, while significant policy shifts or supply shocks prompt interim revisions. A brief final pass ensures clients receive the latest calibrated view.

Why Mordor's Motion Sensor Baseline Inspires Confidence

Published figures often diverge because firms pick different product mixes, treat combo sensors inconsistently, or refresh models on uneven cadences.

Key gap drivers include varied inclusion of hybrid radar modules, whether smartphone IMUs are booked at full ASP or blended, and currency translation points. According to Mordor Intelligence, our 2025 base year of USD 2.57 billion reflects only motion-specific hardware and excludes cameras, whereas other publishers frequently fold broader sensing or imaging IC revenue, inflating totals. Some also project aggressive consumer-electronics rebounds without cross-checking foundry capacity or OEM inventory data before adjusting growth curves.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.57 B | Mordor Intelligence | - |

| USD 8.72 B | Global Consultancy A | includes imaging sensors and counts packaged modules twice |

| USD 9.30 B | Industry Association B | converts FY2019 USD at 2025 rates, assumes uniform 8 % ASP rise |

Taken together, the contrast shows how Mordor's disciplined scoping, dual-path validation, and yearly refresh cadence give decision-makers a dependable, transparent baseline aligned with real supply and demand markers.

Key Questions Answered in the Report

What is the current size of the motion sensor market?

The motion sensor market stands at USD 2.69 billion in 2026 and is projected to reach USD 3.36 billion by 2031.

Which application segment is growing the fastest?

Smart-home and building automation is expanding at a 6.88% CAGR, outpacing traditional consumer electronics demand.

Why are Combo/IMU sensors gaining share?

They integrate multiple axes of motion detection in one package, reducing board size and enabling advanced sensor-fusion features that designers need for wearables and ADAS.

How do new automotive safety rules affect demand?

US and EU regulations make features like blind-spot detection and driver-state monitoring compulsory, ensuring steady multi-year orders for inertial and radar sensors.

What are the main obstacles to faster market growth?

High costs of next-generation MEMS, supply-chain fragility in advanced wafer nodes, and privacy concerns surrounding ubiquitous sensing temper adoption rates.

Which region leads the motion sensor market?

Asia-Pacific holds the largest regional share at 36.95%, supported by dense electronics manufacturing ecosystems and expanding electric-vehicle production.

Page last updated on: