Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.86 Billion |

| Market Size (2031) | USD 2.99 Billion |

| Growth Rate (2026 - 2031) | 9.96% CAGR |

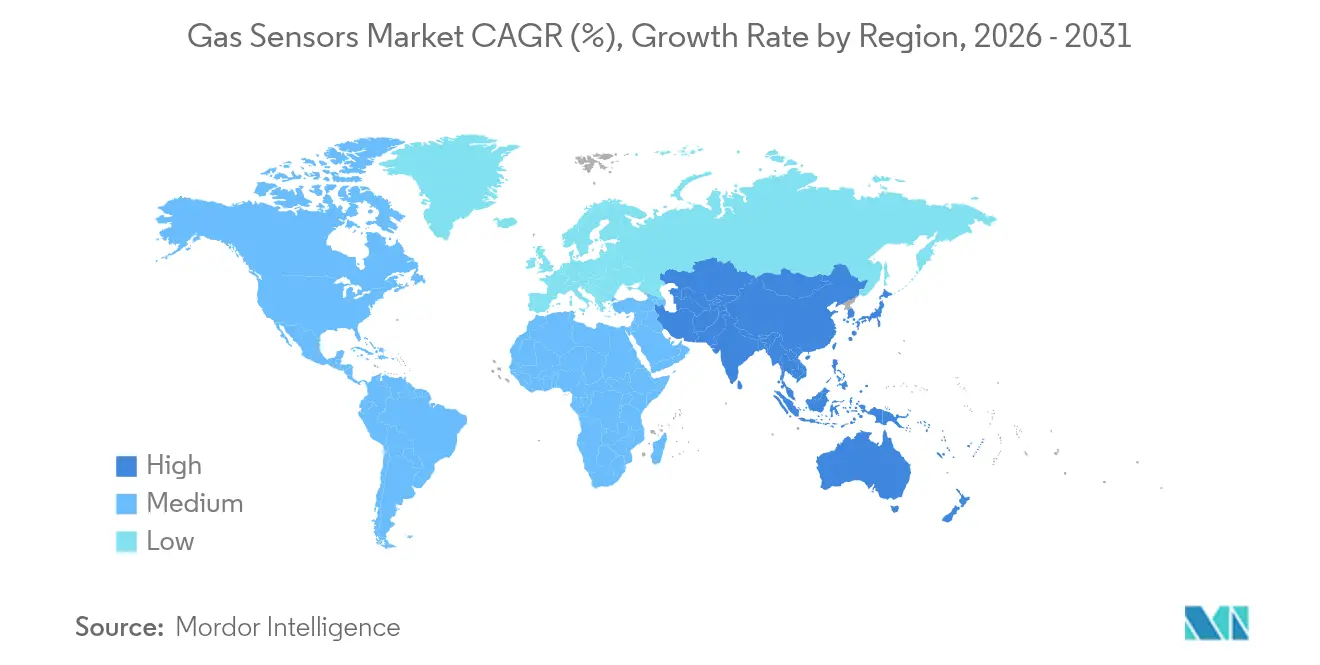

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gas Sensors Market Analysis by Mordor Intelligence

The gas sensors market size is expected to increase from USD 1.67 billion in 2025 to USD 1.86 billion in 2026 and reach USD 2.99 billion by 2031, growing at a CAGR of 9.96% over 2026-2031. Tightening vehicle-emission rules, large smart-city air-quality programs, and the rapid build-out of hydrogen production sites are combining to lift annual sensor shipments across automotive, industrial, and municipal end users. Electrochemical cells still dominate toxic-gas detection because they offer sub-ppm accuracy, yet multi-channel MEMS-optical arrays are scaling quickly as designers shrink footprints for wearables and IoT edge nodes. Demand is also migrating from wired 4-20 mA loops to wireless protocols that slash installation labour in brownfield plants. Meanwhile, the competitive field remains moderately fragmented, giving mid-tier specialists room to differentiate on ultra-low power draw, cross-sensitivity mitigation, or bundled cloud analytics.

Key Report Takeaways

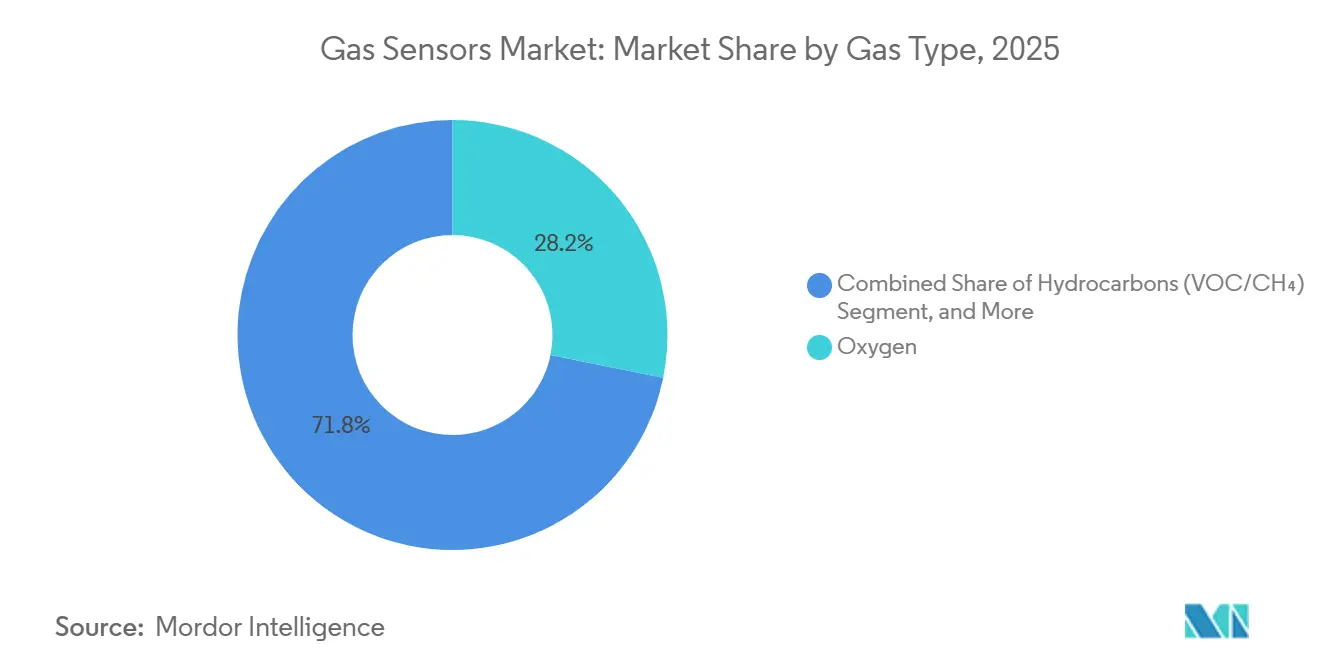

- By gas type, oxygen led with 28.19% of gas sensors market share in 2025, while hydrocarbons are projected to advance at an 11.77% CAGR to 2031.

- By technology, electrochemical sensors held 35.45% of the gas sensors market size in 2025, and MEMS-optical arrays record the fastest growth at 11.95% CAGR through 2031.

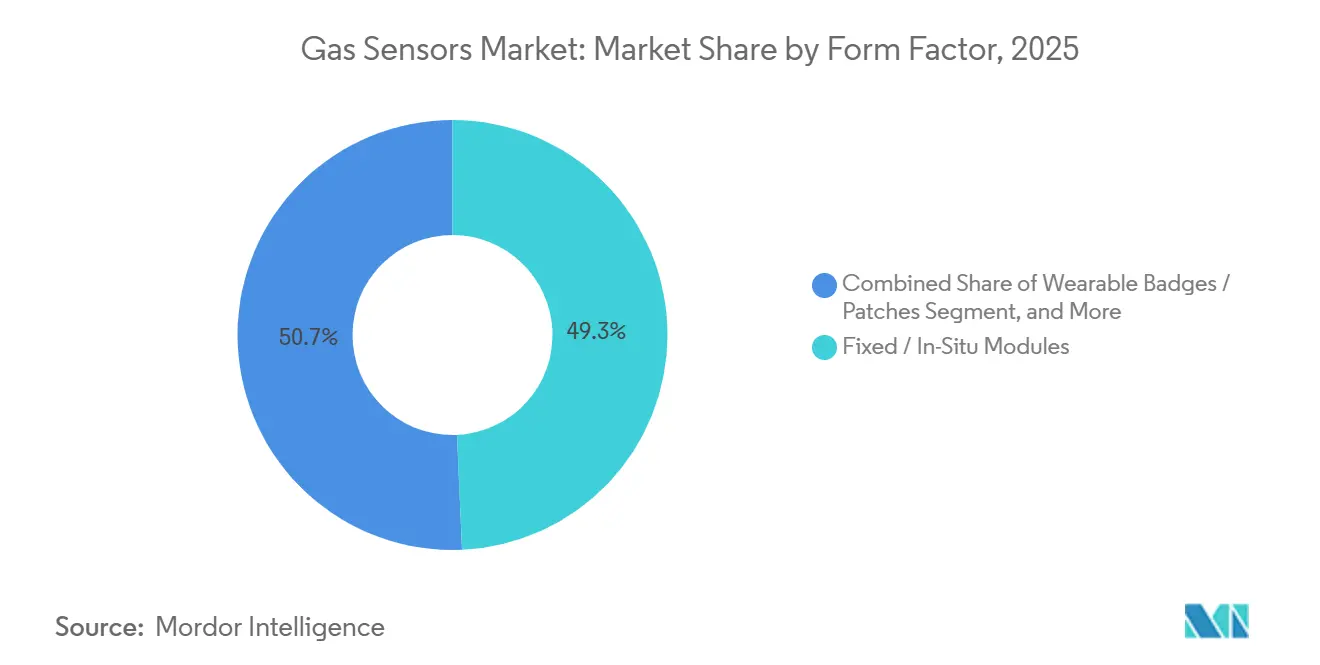

- By form factor, fixed modules accounted for 49.29% of revenue in 2025, whereas wearables are forecast to expand at an 11.82% CAGR to 2031.

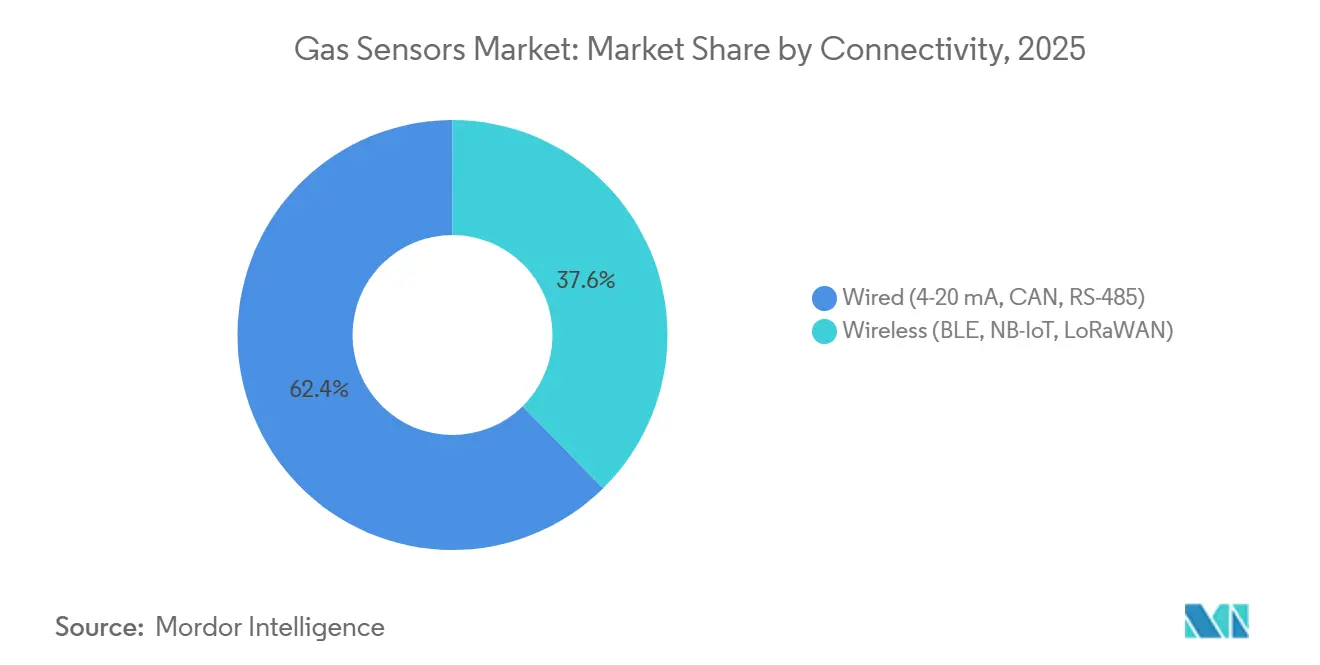

- By connectivity, wired links retained 62.37% share in 2025, yet wireless nodes are rising at a 12.11% CAGR through 2031.

- By end-use, industrial safety captured 31.86% share in 2025, while environmental monitoring is set to grow at a 12.06% CAGR to 2031.

- Asia-Pacific contributed 36.12% of 2025 revenue and is also the fastest-advancing region at an 11.59% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gas Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Vehicle On-Board Diagnostics (Euro 7, EPA Tier 3) | +2.80% | Europe, North America, China (National VI-b) | Medium term (2-4 years) |

| IoT-Enabled Air-Quality Monitoring Roll-Outs (Smart Cities) | +2.10% | Global, with concentration in Asia-Pacific megacities and European Union urban zones | Medium term (2-4 years) |

| Surging Demand from Hydrogen Production and Fuel-Cell Value Chain | +1.60% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Workplace Safety Mandates (OSHA, REACH, ISO 45001) | +1.40% | Global, strongest enforcement in North America and Europe | Short term (≤ 2 years) |

| Emerging Methane-Leak Detection Rules for Oil and Gas (OGMP 2.0) | +1.20% | Global, early adoption in North America and Middle East | Medium term (2-4 years) |

| Miniaturised MEMS-Based Multi-Gas Arrays (< 3 mm) Driving ASP Uplift | +0.90% | Global, led by consumer electronics and wearable device manufacturers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Vehicle On-Board Diagnostics

Euro 7 rules effective July 2025 cut allowable nitrogen-oxide slip to 10 mg km⁻¹ for the full vehicle life, forcing automakers to install dual NOₓ probes with self-diagnostic redundancy.[1]European Commission, “Questions and Answers: Euro 7 Standards,” ec.europa.eu In the United States, EPA Tier 3 tightened fleet-average NOₓ to 30 mg mile⁻¹, while China’s National VI-b mirrors the same thresholds, together covering close to 90 million light-duty vehicles per year. Tier-1 suppliers now specify zirconia cells that survive 850 °C exhaust streams and deliver sub-5 s response. Larger order volumes are compressing average selling prices but are also boosting total unit demand. Multi-gas modules that simultaneously read NOₓ, ammonia slip, and hydrocarbons are emerging to trim wiring and ECU costs.[2]Sensirion AG, “Product Roadmaps,” sensirion.com

IoT-Enabled Air-Quality Monitoring Rollouts

Cities are moving from one regulatory-grade station per 100 000 residents to grid densities of 10-50 low-cost nodes km⁻², generating hyperlocal maps in real time. The European Union cut annual PM₂. ₅ limits to 10 µg m⁻³ and NO₂ to 20 µg m⁻³ in 2024, prompting Milan, Warsaw, and Athens to deploy supplementary electrochemical and NDIR arrays. China has surpassed 5 000 automated stations and plans another 2 000 township nodes by 2027.[3]Ministry of Ecology and Environment of the People’s Republic of China, “National Air Quality Network,” english.mee.gov.cn India budgeted INR 22 billion (USD 265 million) in 2025 for networks across 132 non-attainment cities. Platforms from Siemens, ABB, and Teledyne upload data to cloud dashboards that apply drift correction, trimming field service visits by 25%.[4]Siemens AG, “Digital Industries Automation Products,” siemens.com

Surging Demand from Hydrogen Production and Fuel-Cell Value Chain

Global electrolyzer additions reached 8 GW in 2025, and the pipeline exceeds 50 GW, propelled by production credits of up to USD 3 kg⁻¹ in the United States and the European Repower EU plan. Electrolyzers require trace oxygen sensors below 10 ppm at 70 bars, while fuel-cell vehicles integrate three hydrogen leak detectors per unit to comply with SAE J2578. Refuelling stations now exceed 1 200 worldwide, each using catalytic bead pairs for emergency shut off. Solid-state MOS probes are replacing carrier-gas chromatographs in steam-methane reformers, lowering five-year ownership cost by 40%.

Workplace Safety Mandates

OSHA cut the 8-hour hydrogen-sulfide limit to 5 ppm and imposed a 10 ppm 15-minute ceiling in 2024, triggering plant-wide deployment of personal gas badges. Europe’s REACH added formaldehyde and benzene to its very high concern list in 2025, mandating continuous monitoring in pharma and specialty-chemical lines. ISO 45001 accreditation now demands real-time alert logs, driving Bluetooth-enabled wearables from Honeywell and Dräger that stream live readings to supervisory tablets. OSHA penalties for inadequate detection rose 35% year on year to USD 120 million in 2025, pushing firms toward proactive exposure prevention.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sub-10 ppm Cross-Sensitivity Challenges in Mixed-Gas Matrices | -1.80% | Global, most acute in chemical processing and confined-space applications | Medium term (2-4 years) |

| Silicon Supply Volatility Inflating Wafer Prices | -1.20% | Global, concentrated impact on MEMS and solid-state sensor manufacturers | Short term (≤ 2 years) |

| Lack of Global Calibration Standards Hampers Interchangeability | -0.90% | Global, regulatory fragmentation between North America, Europe, and Asia | Long term (≥ 4 years) |

| Cost Pressure from Low-End Chinese Electrochemical Suppliers | -0.70% | Global, strongest impact in building automation and consumer segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sub-10 ppm Cross-Sensitivity Challenges in Mixed Gas Matrices

Platinum-based CO cells respond to hydrogen at about 50% of CO sensitivity, while H₂S cells cross-respond 20-30% to SO₂, leading to costly application-specific validation that can add 25% to project budgets. MOS sensors have even wider interference bands, and ISO 17025 covers only single-gas calibrations, leaving end users to design custom test regimes. Alphasense released a Kalman-filter front-end chip in 2025 that cuts transient false positives yet adds USD 15-30 to each module.

Silicon Supply Volatility Inflating Wafer Prices

A 15% jump in 150-200 mm wafer prices in early 2025 lengthened lead times from 12 to 20 weeks, squeezing fabless designers such as Sensirion and ScioSense. Bosch and STMicroelectronics leveraged captive fabs, but total 200 mm capacity additions of 150 000 wpm in 2025 fell short of demand, a gap that IC Insights expects to persist beyond 2028. Alternative substrates like glass or SOI require fresh process qualification, delaying volume rollouts by two years or more.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Gas Type: Oxygen Sustains Scale While Hydrocarbons Accelerate

Oxygen probes delivered 28.19% of 2025 revenue thanks to universal use in lambda control, industrial combustion tuning, and ventilators. The gas sensors market size for oxygen detection remains buoyed by zirconia cells that achieve sub-1% accuracy across −40 °C to 850 °C. Hydrocarbons, including VOCs and methane, are advancing at an 11.77% CAGR because OGMP 2.0 compels quarterly surveys at upstream sites, boosting sales of photo-ionization detectors and open-path laser spectrometers.

Hydrogen-rich atmospheres in electrolyzers and fuel-cell vehicles are pushing demand for trace oxygen and nitrogen sensors able to measure below 10 ppm at 70 bars. CO₂ sensors benefited from HVAC retrofits that hold in-room levels under 800 ppm. Nitrogen-oxide probes rose sharply after Euro 7 but saw unit price erosion from USD 45 to 38. Premium pricing persists for SO₂, NH₃, and Cl₂ modules that ship in explosion-proof enclosures.

By Technology: Electrochemical Dominates, MEMS-Optical Gains Share

Electrochemical devices held 35.45% of 2025 value, backed by high selectivity in single-gas contexts. MEMS-optical arrays are climbing at an 11.95% CAGR, integrating micro-mirrors and IR detectors within 3 mm packages that fit wearables and phones. The gas sensors market share of MEMS modules is widening as ASPs stay high relative to discrete designs.

PID instruments remain niche for hazmat teams, whereas MOS parts offer the lowest bill-of-materials but drift under humidity swings, requiring frequent zeroing. NDIR remains indispensable for CO₂ and hydrocarbon analysis in ambient stations where 15-year lifetimes justify USD 50-150 pricing. Catalytic beads still dominate residential methane alarms, though silicone poisoning is nudging premium installations toward infrared options.

By Form Factor: Wearables Rise Beside Established Fixed Modules

Fixed in-situ modules kept 49.29% share in 2025 because process plants need line-powered, wired analyzers certified for hazardous zones. Yet wearables are growing at 11.82% CAGR as rules force every worker in confined areas to carry a personal badge. The gas sensors market size for wearables is swelling on the back of clip-on devices that now weigh 120 g and run 48 h on a lithium-polymer cell. GPS and accelerometer functions support man-down alerts.

Portable handheld meters occupy the middle ground for maintenance crews. Design priorities are shifting toward ruggedized plastics that resist caustic washdowns and toward wireless uplinks that automate exposure logbooks under ISO 45001.

By Connectivity: Wireless Protocols Unlock Retrofit Applications

Wired links still accounted for 62.37% of 2025 shipments, favoured in refineries that demand deterministic latency. NB-IoT, LoRaWAN, and BLE nodes are scaling at a 12.11% CAGR, cutting conduit labour and enabling five-year battery life. The gas sensors market size attributable to wireless shipments is expanding fastest where building codes allow battery nodes to serve as secondary monitors.

NB-IoT excels in dense urban grids, while LoRaWAN covers landfills and farms across 15 km ranges. BLE dominates consumer and occupational badges that sync directly to phones. Cybersecurity fears lead many plants to keep primary alarms on wired loops and place wireless units on segregated VPN gateways that add USD 500-2 000 per site.

By End-Use Industry: Environmental Monitoring Overtakes Growth Leadership

Industrial safety topped 31.86% of 2025 revenue but faces mid-single-digit growth as many legacy plants already comply with baseline rules. Environmental monitoring nodes are climbing at a 12.06% CAGR because municipal air-quality grids qualify for green-bond financing and must meet WHO limits. The gas sensors market share for city networks is broadening as average node counts rise from hundreds to tens of thousands per metropolis.

Automotive powertrains are absorbing dual NOₓ and CO₂ sensors, especially in plug-in hybrids that switch combustion modes frequently. Building automation retrofits accelerated after ASHRAE 62.1 moved the CO₂ trigger from 1 000 ppm to 800 ppm. Medical, food, and cold-chain niches remain small in volume yet command premium ASPs up to USD 800 per module.

Geography Analysis

Asia-Pacific generated 36.12% of 2025 revenue and is forecast to grow at an 11.59% CAGR, the fastest regional pace. China operates more than 5 000 government air-quality stations and will add 2 000 township nodes by 2027, each specified for <10% annual drift. India budgeted INR 22 billion (USD 265 million) under its National Clean Air Programme, mandating NDIR SO₂ and NOₓ probes in thermal plants. Japan aims for 1 000 hydrogen stations by 2030, boosting demand for catalytic bead detectors certified to ISO 19881, while South Korea’s Green New Deal earmarked KRW 1.8 trillion for smart factories with wireless sensor grids.

North America provided roughly 28% of 2025 turnover. OSHA’s stricter hydrogen-sulfide limits triggered plant-wide badge issuance, and the Inflation Reduction Act’s USD 3 kg⁻¹ hydrogen credit stimulated more than 15 GW of electrolyzer projects needing trace oxygen sensors. Canada’s methane rule mandates quarterly leak checks, while Mexico expanded continuous monitoring across 1 200-point sources.

Europe held about 24% share in 2025. The EU cut PM₂. ₅ and NO₂ limits, forcing southern capitals to deploy dense IoT nodes. Germany extended continuous emission rules to medium combustion plants, adding 8 000 new installations. The United Kingdom fixed a binding PM₂. ₅ target under the Environment Act 2021, and France introduced indoor-air monitoring in all schools.

Middle East and Africa contributed close to 8% of revenue. Saudi Aramco’s Jafurah gas field is fitting H₂S networks across wellheads, and the UAE installed 150 ambient stations in 2025. South Africa lowered diesel particulate limits in mines, prompting retrofits with BLE badges.

South America accounted for 4% of revenue, led by Brazil’s sugarcane ethanol complexes and Argentina’s Vaca Muerta shale pads, both of which now mandate fixed methane and CO detectors on compressor skids.

Competitive Landscape

The gas sensors market remains moderately fragmented; the top five suppliers Bosch, Honeywell, Sensirion, Drägerwerk, and Figaro Engineering held an estimated 42% share in 2025. Bosch expanded Reutlingen MEMS output by 30 million automotive NOₓ and O₂ dies after a EUR 150 million (USD 165 million) investment, shaving die cost by 20%. Honeywell bought Carrier’s industrial refrigeration detection line, adding ammonia leak systems that extend its City Technology cell range.

Sensirion closed its acquisition of Senseair in 2024, consolidating CO₂ sensing for HVAC and vehicle cabins, and in January 2026 released the SCD42 photoacoustic module that draws just 15 mW. Patent filings show Honeywell focusing on machine-learning drift compensation, while Bosch is co-packaging NOₓ and NH₃ heaters to halve power draw. NevadaNano’s molecular property spectrometer uses acoustic resonance to all but eliminate calibration for combustible-gas alarms, positioning the firm as a disruptive entrant.

Chinese challengers such as Zhengzhou Winsen sell CO₂ and VOC cells at 30-40% lower prices, rapidly gaining share in smart homes and building automation. Yet shorter calibration cycles and higher cross-sensitivity limit penetration in safety-critical use cases. Foundry constraints remain a strategic lever: firms with captive 200 mm lines secure priority wafers amid ongoing silicon shortages, while fabless rivals sign multi-year take-or-pay deals that squeeze gross margins.

Gas Sensors Industry Leaders

-

Robert Bosch GmbH

-

Honeywell International Inc. (City Technology)

-

Drägerwerk AG & Co. KGaA

-

Figaro Engineering Inc.

-

Sensirion Holding AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Sensirion launched the SCD42 miniature CO₂ sensor targeting battery-powered wearables with a 10-year maintenance-free life.

- November 2025: Honeywell acquired Carrier Global’s industrial refrigeration gas-detection portfolio, adding ammonia and freon leak products to its range.

- September 2025: Bosch opened a USD 165 million MEMS line in Reutlingen, boosting annual NOₓ and oxygen sensor capacity by 30 million units. .

- July 2025: Drägerwerk integrated its X-am 8000 wearables with Siemens Simatic PCS 7, enabling automatic ventilation when H₂S or CO alarms trigger.

Global Gas Sensors Market Report Scope

The Gas Sensors Market Report is Segmented by Gas Type (Oxygen, Carbon Monoxide, Carbon Dioxide, Nitrogen Oxides, Hydrocarbons, Other Gases), Technology (Electrochemical, Photo-Ionisation, Solid-State/MOS, Catalytic Bead, NDIR, MEMS-Semiconductor Optical), Form Factor (Fixed/In-Situ, Portable/Hand-Held, Wearable), Connectivity (Wired, Wireless), End-Use Industry (Industrial Safety, Automotive, Building Automation, Medical, Food and Beverage, Environmental Monitoring), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

By Gas Type

| Oxygen |

| Carbon Monoxide (CO) |

| Carbon Dioxide (CO?) |

| Nitrogen Oxides (NO?) |

| Hydrocarbons (VOC/CH?) |

| Other Gases (SO?, H?S) |

By Technology

| Electrochemical |

| Photo-Ionisation (PID) |

| Solid-State / MOS |

| Catalytic Bead |

| Non-Dispersive Infra-Red (NDIR) |

| MEMS-Semiconductor Optical |

By Form Factor

| Fixed / In-Situ Modules |

| Portable / Hand-Held Devices |

| Wearable Badges / Patches |

By Connectivity

| Wired (4-20 mA, CAN, RS-485) |

| Wireless (BLE, NB-IoT, LoRaWAN) |

By End-Use Industry

| Industrial Safety and Process (Oil and Gas, Chemicals) |

| Automotive Powertrain and HVAC |

| Building Automation / Smart Homes |

| Medical and Life-Science Equipment |

| Food, Beverage and Cold-Chain Logistics |

| Environmental Monitoring and Smart City Nodes |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Gas Type | Oxygen | ||

| Carbon Monoxide (CO) | |||

| Carbon Dioxide (CO?) | |||

| Nitrogen Oxides (NO?) | |||

| Hydrocarbons (VOC/CH?) | |||

| Other Gases (SO?, H?S) | |||

| By Technology | Electrochemical | ||

| Photo-Ionisation (PID) | |||

| Solid-State / MOS | |||

| Catalytic Bead | |||

| Non-Dispersive Infra-Red (NDIR) | |||

| MEMS-Semiconductor Optical | |||

| By Form Factor | Fixed / In-Situ Modules | ||

| Portable / Hand-Held Devices | |||

| Wearable Badges / Patches | |||

| By Connectivity | Wired (4-20 mA, CAN, RS-485) | ||

| Wireless (BLE, NB-IoT, LoRaWAN) | |||

| By End-Use Industry | Industrial Safety and Process (Oil and Gas, Chemicals) | ||

| Automotive Powertrain and HVAC | |||

| Building Automation / Smart Homes | |||

| Medical and Life-Science Equipment | |||

| Food, Beverage and Cold-Chain Logistics | |||

| Environmental Monitoring and Smart City Nodes | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the gas sensors market be by 2031?

It is projected to reach USD 2.99 billion by 2031, growing at a 9.96% CAGR from 2026.

Which gas type segment is expanding the fastest?

Hydrocarbon sensors, driven by stricter methane-leak rules, are advancing at an 11.77% CAGR through 2031.

Why are wireless gas sensors gaining ground in plants?

NB-IoT, LoRaWAN, and BLE models cut conduit labor costs and enable five-year battery life, spurring a 12.11% CAGR for wireless nodes.

Which region leads in gas sensor demand?

Asia-Pacific holds the largest share at 36.12% of 2025 revenue and also posts the fastest growth at an 11.59% CAGR.

How fragmented is supplier competition?

The top five vendors command around 42% of sales, indicating moderate fragmentation with room for niche entrants.

What is the impact of Euro 7 on sensor uptake?

Euro 7 forces dual NO? probes in every diesel vehicle, increasing annual automotive sensor demand and compressing unit prices.

Page last updated on: