Fluid Sensor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

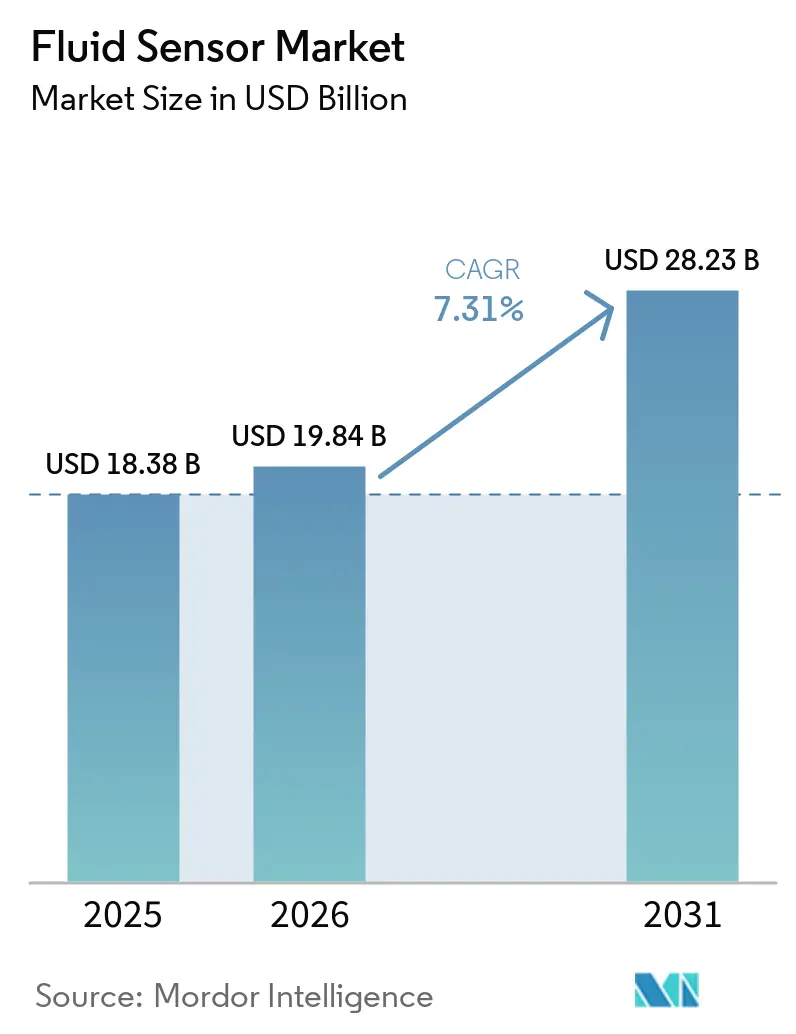

| Market Size (2026) | USD 19.84 Billion |

| Market Size (2031) | USD 28.23 Billion |

| Growth Rate (2026 - 2031) | 7.31% CAGR |

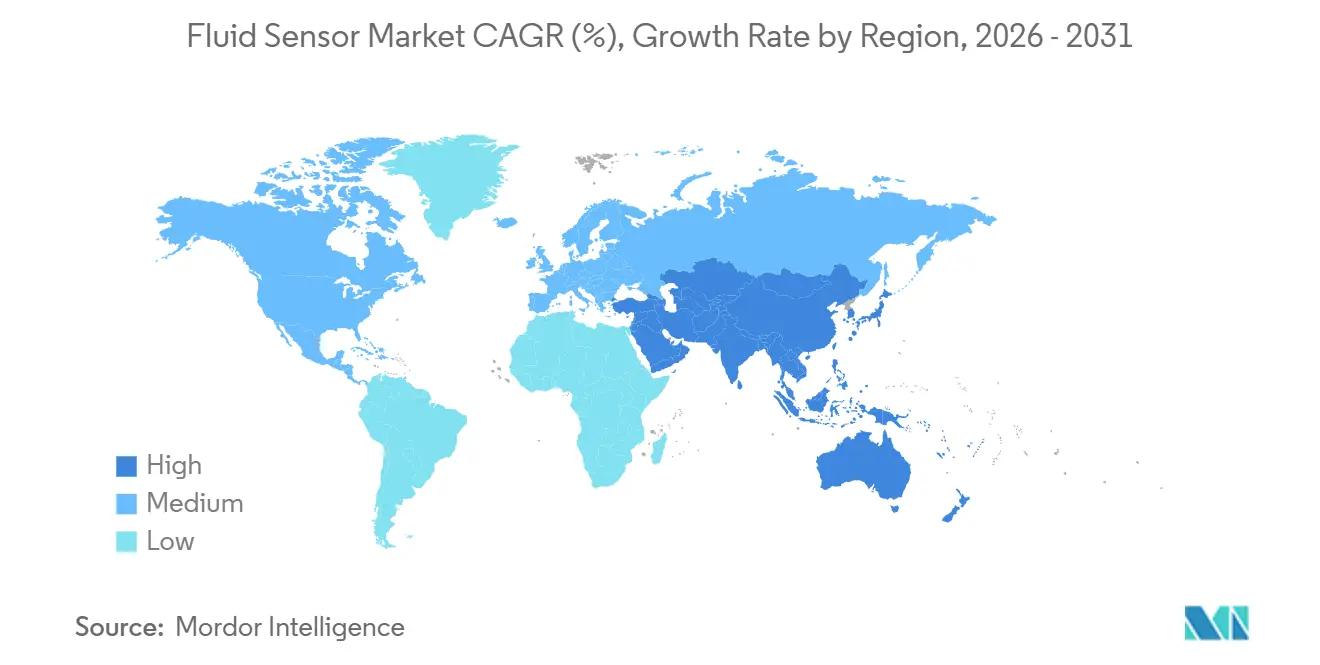

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

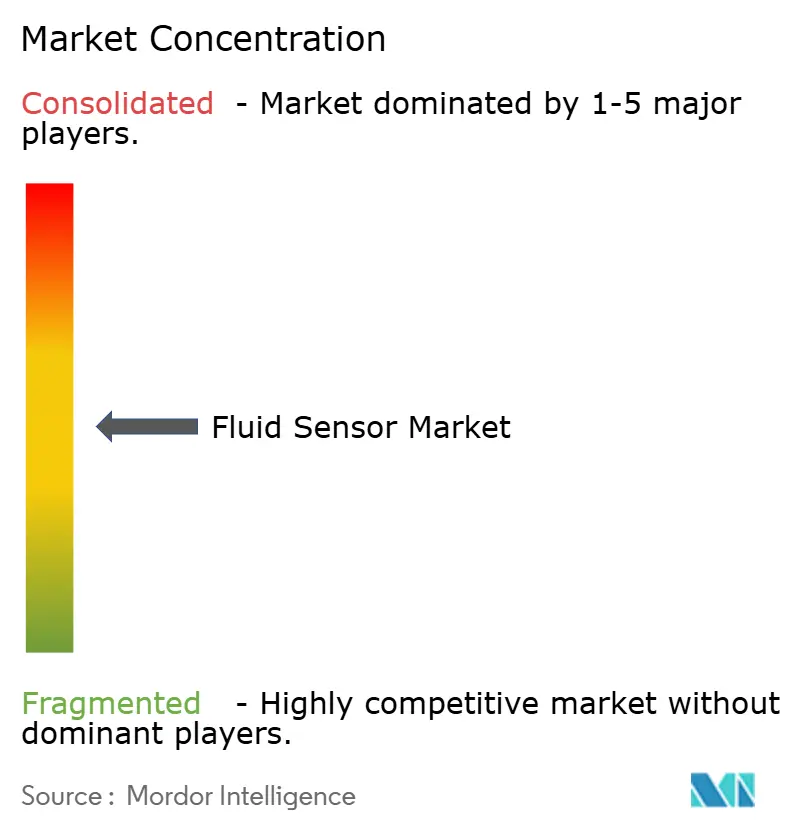

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fluid Sensor Market Analysis by Mordor Intelligence

The fluid sensor market size is projected to expand from USD 18.38 billion in 2025 and USD 19.84 billion in 2026 to USD 28.23 billion by 2031, registering a CAGR of 7.31% between 2026 and 2031. Heightened digitization across factories, tightening environmental mandates, and the shift of sensor intelligence to edge devices are accelerating demand. Spending is moving from discrete transducers toward integrated sensor-to-enterprise platforms that embed predictive analytics and wireless connectivity. Flow sensing dominated 2025 revenue, yet radar- and ultrasonic-based non-contact level devices are growing faster as maintenance-heavy floats are retired. Gas detection is scaling on the back of emissions rules, while single-use hygienic probes are penetrating biopharmaceutical suites. Tariff-driven semiconductor supply fragmentation is reshaping sourcing, prompting relocation of assembly to Mexico, Vietnam, and Eastern Europe.

Key Report Takeaways

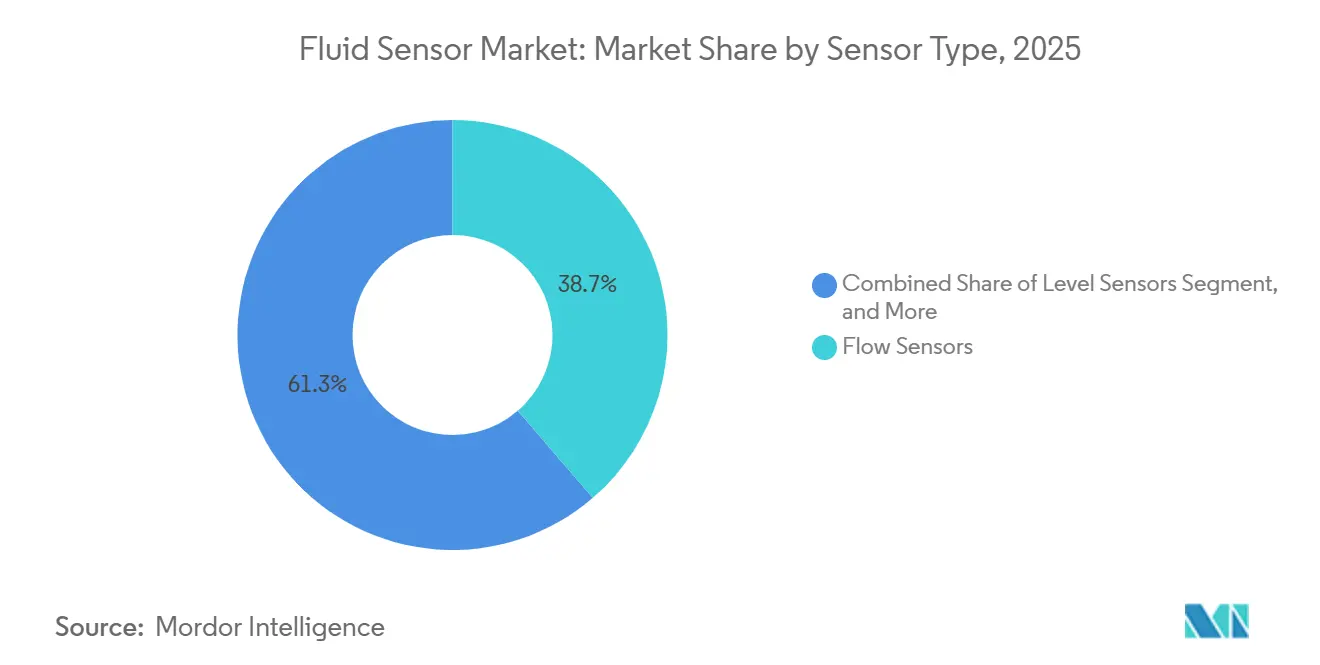

- By sensor type, flow sensors led with 38.68% of the fluid sensor market share in 2025, and non-contact level sensors are advancing at an 8.11% CAGR through 2031.

- By detection medium, liquid sensing captured 64.24% share of the fluid sensor market size in 2025, whereas gas sensing is forecast to expand at an 8.05% CAGR to 2031.

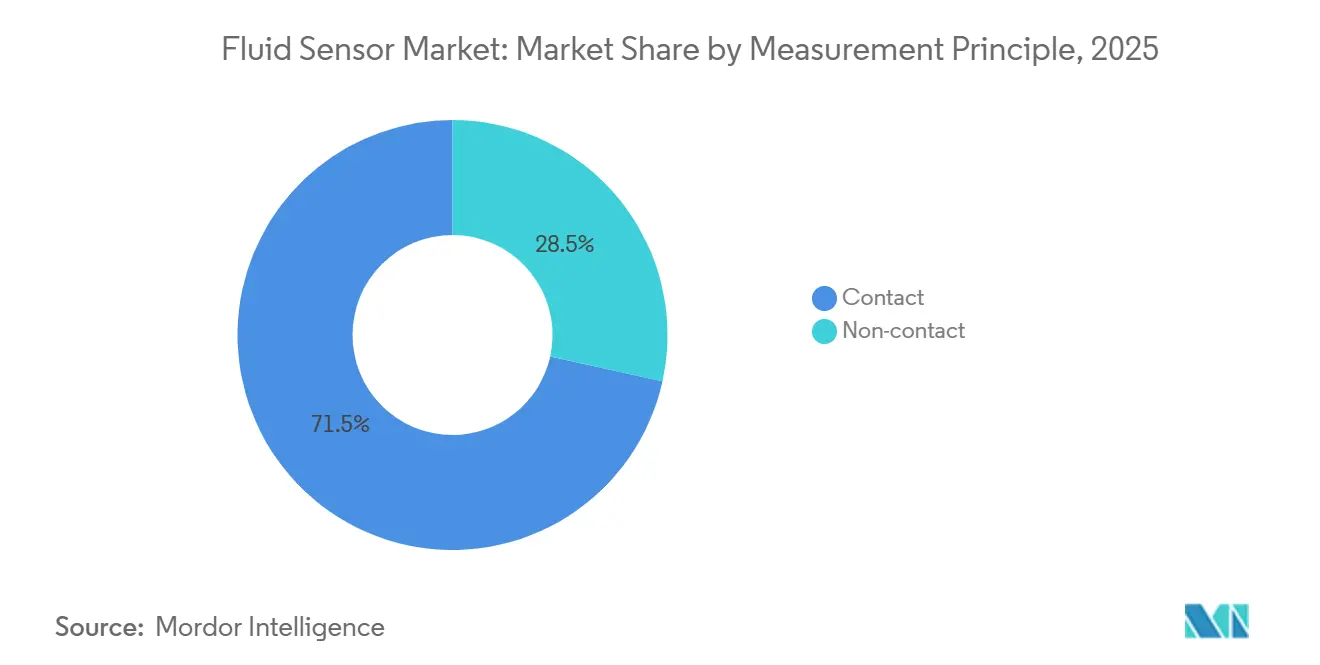

- By measurement principle, contact methods held 71.54% of the fluid sensor market in 2025 revenue, and non-contact solutions are projected to grow at 7.78% CAGR between 2026 and 2031.

- By end-use industry, oil and gas accounted for 27.93% of the fluid sensor market in 2025, while pharmaceuticals and biotechnology had the fastest 7.93% CAGR during 2026-2031.

- By geography, Asia-Pacific captured 36.82% of the global revenue of the fluid sensor market in 2025 and is rising at a 7.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fluid Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IIoT-Driven Demand for Real-Time Monitoring | +1.8% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Stringent Water and Wastewater Regulations | +1.5% | North America and Europe, emerging in Asia-Pacific cities | Long term (≥ 4 years) |

| Pipeline Integrity Mandates in Oil and Gas | +1.2% | North America, Middle East, Russia | Medium term (2-4 years) |

| Process-Industry Need for Hygienic Sensors | +1.0% | Global, concentrated in North America and Europe pharma hubs | Short term (≤ 2 years) |

| AI-Enabled Self-Calibrating Sensors | +0.9% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Micro-Fluidic Lab-on-Chip Diagnostics | +0.6% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

IIoT-Driven Demand for Real-Time Monitoring

Continuous telemetry is replacing periodic manual rounds, cutting anomaly-detection time from hours to seconds. A 2025 retrofit on twelve CNC machines in India trimmed unplanned downtime by 95% and paid back in under three months by pairing low-cost microcontrollers with pressure and flow probes that publish data over. Predictive models built on these time-series streams now forecast pump seal failures up to two weeks in advance, averting emergency shutdowns that cost process plants USD 50,000-200,000 per event.[1]Yokogawa Electric Corp., “Energy Transition Solutions,” yokogawa.com LoRaWAN and cellular narrowband IoT extend coverage to remote well sites, with a single 4G gateway aggregating 50-100 devices at annual connectivity costs of USD 200-800 per node.[2]Pipeline and Hazardous Materials Safety Administration, “Pipeline Integrity Management,” phmsa.dot.gov Vendors such as Yokogawa overlay SCADA-grade visualizations atop distributed assets, surfacing degradation early and enabling spare-part staging before production is threatened.

Stringent Water and Wastewater Regulations

The United States Environmental Protection Agency now caps per- and polyfluoroalkyl substances at 2-5 ng/L, forcing utilities to adopt lab-grade chromatography and high-resolution sensors on line directives impose similar rules with phased enforcement through 2027, pressuring legacy plants to move from grab sampling to continuous pH, turbidity, and dissolved-oxygen telemetry.[3]United States Environmental Protection Agency, “Per- and Polyfluoroalkyl Substances National Primary Drinking Water Regulation,” epa.govNanomaterial-based electrochemical probes combined with machine-learning filters resolve sub-ppb concentrations in turbid matrices where older cells saturated IEC.CH. Smaller rural systems face 3-5 times higher per-capita capital cost than large utilities, energizing a low-cost segment that favors field-serviceable units and pay-as-you-go cloud analytics.

Pipeline Integrity Mandates in Oil and Gas

PHMSA regulations compel real-time pressure, flow, and leak monitoring on high-consequence pipelines, yet coverage gaps persist on thousands of legacy kilometers. New intrinsically safe transmitters rated to 6,000 bar and 200 °C extend sensing into sour-gas and supercritical CO₂ pipelines. Hydrogen blending introduces embrittlement risks, so titanium diaphragms and specialized seals add 30-50% to unit cost but avoid premature failure. Energy-harvesting wireless nodes powered by vibration or thermal gradients eliminate batteries and trenching, lowering retrofit cost for operators in remote deserts or tundra.[4]Intertek, “Navigating Gas Detector Standards,” intertek.com

Process-Industry Need for Hygienic Sensors

Single-use sensors are displacing stainless probes in cell and gene therapy suites, removing cleaning-in-place cycles that consumed 20-30% of batch time. The BioPAT Viamass biomass sensor, launched in November 2025, illustrates how disposable probes now deliver real-time cell density data without autoclaving. Designs follow 3-A Sanitary Standards with flush diaphragms and electropolished surfaces to eliminate bacterial dead-legs. Regulatory guidance on closed-loop control encourages embedding sensor feedback directly into automation, boosting first-pass yield by up to 10 percentage points.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Advanced Sensors | -1.2% | Global, especially price-sensitive Asia-Pacific and South America | Short term (≤ 2 years) |

| Accuracy Drift Under Extreme Conditions | -0.8% | Global, concentrated in oil and gas, chemical, and power sectors | Medium term (2-4 years) |

| Cyber-Security Risks in Wireless Devices | -0.6% | Global, acute in critical infrastructure | Medium term (2-4 years) |

| Tariff-Driven Silicon Wafer Shortages | -0.5% | Asia-Pacific and North American supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Advanced Sensors

Hazardous-area pressure transmitters certified to ATEX and IECEx can cost triple a standard unit, while laser level meters priced above USD 10,000 dwarf ultrasonic alternatives that sit near USD 3,000. Total cost of ownership balloons once integration, calibration, cloud hosting, and maintenance are included; a 10-machine IoT roll-out in India averages INR 800,000 (USD 9,600) with recurring cloud fees up to USD 15,000 per year. SMEs grapple with capital constraints when ROI stretches past two years. Volume orders cut unit pricing by up to 40%, but dispersed end users rarely hit pallet-scale thresholds.

Accuracy Drift Under Extreme Conditions

Measurement precision can erode 15-20% annually in fouling or high-temperature zones unless recalibration is performed. Export controls now restrict OEM servicing in some jurisdictions, forcing operators either to live with degraded accuracy or replace instruments early. Temperature shifts of 10 K can inject 0.4%-of-span error into pressure readings. Self-cleaning ultrasonics mitigate buildup but add 30-50% to device cost. Safety Integrity Level 3 loops require diagnostics that force a safe state on a fault, yet these features remain absent from budget product lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Non-Contact Level Devices Gain Momentum

Flow sensors led 2025 revenue with 38.68% of the fluid sensor market share, underscoring their ubiquity in custody transfer and energy balancing. Nonetheless, radar and ultrasonic level sensors are forecast to post an 8.11% CAGR, the fastest among major categories. This momentum stems from maintenance avoidance, as non-contact designs sidestep wear and fouling that plague floats. WIKA’s compact radar launch in March 2026 targets cramped pharmaceutical vessels, while OndoSense’s 70-meter solution broadens reach to mining silos. Pressure probes remain essential in wellhead and hydrogen applications where 6,000-bar ratings are now routine. Bundling digital temperature elements with these sensors enables density compensation, advancing multiparameter accuracy.

Across the forecast horizon, non-contact adoption accelerates once the total lifecycle cost is tallied. Quarterly calibrations on wetted probes consume labor and pose contamination risk, a pain point for sterile manufacturing. Radar units slash maintenance visits to an annual cadence, trimming operating expenditure despite a higher upfront ticket. Safety standards also tilt the table; IEC 61511-compliant overfill systems increasingly specify SIL-rated radar devices. Vendors thus emphasize self-diagnostics that flag buildup, verify health, and feed proof-test data to asset management suites, helping operators demonstrate compliance without intrusive checks.

By Detection Medium: Gas Sensing Accelerates Under Emissions Mandates

Liquid measurement still accounts for 64.24% of 2025 sales, covering water, fuels, and solvents, while gas sensing is growing faster at an 8.05% CAGR as governments crack down on air pollutants. Honeywell’s 4-Series nondispersive infrared module doubles calibration intervals, lowering total cost for fixed safety systems in refineries. Emerson’s QX1000 continuous analyzer brings ppb detection to SO₂, NOx, and CO stacks, aligning with tightening power-plant permits. In commercial buildings, updated International Mechanical Code rules require carbon monoxide and nitrogen dioxide detectors in parking garages.

Liquid lines nonetheless anchor high-revenue verticals such as fiscal oil custody transfer, where Coriolis and ultrasonic meters deliver ±0.1% accuracy. Pharmaceutical bioreactors rely on single-use pH, conductivity, and dissolved-oxygen probes to maintain sterility. Meanwhile, hydrogen infrastructure creates a niche for embrittlement-resistant elements, such as titanium or gold plating. These units are priced 30-50% above stainless versions but avoid micro-cracking under high-pressure H₂ service. Regulatory divergence complicates vendor roadmaps, devices must clear ATEX and IECEx globally, then layer UL or CSA for North America, which extends test cycles and costs.

By Measurement Principle: Contact Methods Remain Majority but Gap Narrows

Contact sensing retained a 71.54% revenue share in 2025, shielding its lead through accuracy advantages in opaque or conductive fluids. Guided-wave radar with inserted probes can capably track dual-phase interfaces, immune to foam and vapor. Nevertheless, non-contact modalities are projected to grow at a 7.78% CAGR as the prices of radar and laser hardware decline. Emerson’s Rosemount 3408 illustrates the value proposition, wirelessHART eliminates cabling, while non-contact architecture slashes cleaning downtime in food and beverage tanks.

The economic calculus favors non-contact when sites weigh long-term maintenance. Cleaning-in-place regimens steal hours of production and use caustic media that erode sensor life. A radar retrofit at a European chemical depot reduced calibration labor by 60% in the first year. Still, contact pH and conductivity cells are irreplaceable where regulations demand direct wetted measurement linked to traceable reference standards. Hybrid offerings now embed inductive toroidal coils inside flow-through housings, blending contact accuracy with non-contact fouling resistance.

By End-Use Industry: Pharma and Biotech Outpace Legacy Sectors

Oil and gas accounted for 27.93% of the fluid sensor market revenue in 2025, driven by a growing number of upstream and midstream assets. Yet pharmaceutical and biotechnology plants will log a brisk 7.93% CAGR, buoyed by single-use manufacturing formats that multiply probe counts per reactor. FDA guidance on closed-loop control pushes firms to wire sensors directly into advanced process control schemes, cutting deviation events. Water utilities closely follow, swapping grab sampling for continuous telemetry to meet NPDES permit requirements and PFAS thresholds.

Petrochem and specialty chemical operators invest in explosion-proof, IEC 62443-encrypted transmitters that withstand aggressive media. Food and beverage processors lean on inline sensors for pasteurization and cleaning-validation proof, driven by HACCP and FSMA. Auto and transport segments diversify beyond oil pressure into battery coolant flow and hydrogen detection for fuel cells. Power generators seek radiation-resistant sensors for next-generation reactors, as illustrated by a nanotechnology prototype that withstands 800 °C and neutron flux in test loops.

Geography Analysis

Asia-Pacific accounted for 36.82% of global revenue in 2025 and is forecast to expand at a 7.83% CAGR. China’s Bengbu Sensor Valley aims to reach CNY 30 billion (USD 4.1 billion) in output by 2027, backed by an 8-inch MEMS line. India’s Sensor Center of Excellence projects a domestic market of INR 31,000 crore (USD 3.7 billion) by 2027, fueled by automotive and IoT programs. Japan and South Korea channel subsidies into chiplet architectures to sidestep barriers to extreme-ultraviolet lithography, while Australia deploys wireless probes across remote mines.

North America and Europe together accounted for roughly half of the 2025 turnover. United States Section 301 tariffs that doubled to 50% on Chinese semiconductors in late 2024 inflated bill-of-material costs 15-30%, prodding OEMs toward Mexican, Vietnamese, and Eastern European assembly. Endress and Hauser’s USD 50.9 million Greenwood, Indiana, plant began shipping in mid-2025, shrinking lead times to six weeks. The European Green Deal steers funding toward renewables and carbon capture, with STMicroelectronics scaling its Agrate fab to 4,000 wafers per week and onsemi building a USD 1.91 billion silicon-carbide site in the Czech Republic.

South America, the Middle East, and Africa, though smaller, present focused opportunities. Brazil and Argentina upgrade municipal water treatment, demanding analytical sensors that sniff pesticides and heavy metals. Middle Eastern operators specify ATEX-rated probes for sour-gas fields and hydrogen pipelines, while desalination plants in Saudi Arabia adopt corrosion-resistant level and flow devices. In Africa, South African mines deploy vibration-powered wireless nodes in deep shafts, whereas Nigerian pipelines add leak-detection strings despite limited telecoms backbones.

Competitive Landscape

The fluid sensor market is moderately fragmented. Global automation giants such as Honeywell, Siemens, Emerson, and ABB compete with specialized instrumentation players like Endress+Hauser, Yokogawa, and Flowserve, as well as sensor-focused suppliers such as Sensata Technologies and TE Connectivity. The commoditization of hardware has led to shrinking margins on entry-level pressure and temperature probes, pushing companies to differentiate through advancements in functional safety, cybersecurity compliance, and embedded analytics. For instance, Honeywell’s USD 2.16 billion acquisition of Sundyne in March 2025 enabled the company to integrate pumps, compressors, and sensors into comprehensive turnkey packages, helping it capture a larger share of capital budgets. Similarly, ABB’s acquisition of Sensorfact in early 2025 added plug-and-play energy monitors to its portfolio, which can be retrofitted onto legacy motors without requiring engineering downtime, enhancing its market competitiveness.

Emerging players in the market are leveraging cutting-edge technologies such as MEMS, lab-on-chip microfluidics, and edge AI to develop sensors that are smaller, more energy-efficient, and higher-performing. These advancements are enabling the creation of innovative solutions for challenging environments. For example, the University of Maine has developed a nanotechnology-based sensor capable of operating in nuclear cores at temperatures as high as 800 °C, showcasing the potential of academia-industry collaborations to address critical measurement challenges in harsh conditions. To achieve global reach, vendors are now focusing on obtaining simultaneous certifications, such as ATEX, IECEx, UL, CSA, and NEPSI, to reduce product variants and accelerate launch cycles. The introduction of IEC 60730-2-23:2025 provides a harmonized safety standard that could facilitate broader cross-border acceptance for compliant products, further driving market growth.

White-space opportunities in the fluid sensor market are emerging in areas such as battery-free sensor nodes, AI-driven predictive maintenance platforms, and hygienic single-use probes designed for fast-turnover therapies. These innovations are addressing unmet needs across various industries, creating new avenues for growth. Battery-free nodes, for instance, are gaining traction due to their ability to operate in remote or hard-to-access locations without requiring frequent maintenance. AI-driven predictive platforms are helping industries optimize operations by providing real-time insights and reducing downtime. Meanwhile, single-use probes are becoming increasingly popular in the pharmaceutical and biotechnology sectors, enabling faster and more efficient production of therapies while maintaining strict hygiene standards. These developments highlight the dynamic nature of the fluid sensor market and its potential for continued innovation and expansion.

Fluid Sensor Industry Leaders

Honeywell International Inc.

Siemens AG

Emerson Electric Co.

ABB Ltd

Endress+Hauser Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: WIKA introduced a compact radar level sensor with IP69K sealing for hygienic tanks, supporting non-contact installs in space-restricted sites.

- March 2026: Honeywell rolled out the 4-Series nondispersive infrared gas module, extending calibration intervals to 12 months and cutting false alarms by 30%.

- March 2026: Yokogawa opened an autonomous machine center and automated warehouse in Newnan, Georgia, localizing transmitter and flowmeter production and reducing lead times by 60%.

- February 2026: Emerson unveiled the Rosemount QX1000 continuous gas analyzer, delivering ppb sensitivity for SO₂, NOx, and CO without consumable reagents.

Global Fluid Sensor Market Report Scope

The Fluid Sensor Market encompasses devices and systems used to measure, monitor, and analyze the physical properties and behavior of liquids and gases across various environments. These sensors detect parameters such as flow rate, pressure, level, temperature, and fluid composition to ensure efficient and safe operation of industrial and commercial processes. Fluid sensors are widely deployed across sectors, including oil and gas, water and wastewater management, healthcare, automotive, and manufacturing.

The Fluid Sensor Market Report is Segmented by Sensor Type (Pressure Sensors, Flow Sensors, Level Sensors, and Temperature and Other Sensors), Detection Medium (Liquid, and Gas), Measurement Principle (Contact, and Non-contact), End-Use Industry (Oil and Gas, Water and Wastewater, Chemicals and Petrochemicals, Food and Beverage, Pharmaceuticals and Biotechnology, Automotive and Transportation, Power Generation, and Other End-Use Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Pressure Sensors |

| Flow Sensors |

| Level Sensors |

| Temperature and Others |

| Liquid |

| Gas |

| Contact |

| Non-contact |

| Oil and Gas |

| Water and Wastewater |

| Chemicals and Petrochemicals |

| Food and Beverage |

| Pharmaceuticals and Biotechnology |

| Automotive and Transportation |

| Power Generation |

| Other End-Use Industries |

| North America | United States | |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Africa | South Africa | |

| Nigeria | ||

| By Sensor Type | Pressure Sensors | ||

| Flow Sensors | |||

| Level Sensors | |||

| Temperature and Others | |||

| By Detection Medium | Liquid | ||

| Gas | |||

| By Measurement Principle | Contact | ||

| Non-contact | |||

| By End-use Industry | Oil and Gas | ||

| Water and Wastewater | |||

| Chemicals and Petrochemicals | |||

| Food and Beverage | |||

| Pharmaceuticals and Biotechnology | |||

| Automotive and Transportation | |||

| Power Generation | |||

| Other End-Use Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| South America | Brazil | ||

| Argentina | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Africa | South Africa | ||

| Nigeria | |||

Key Questions Answered in the Report

What is the projected value of the fluid sensor market by 2031?

The fluid sensor market size is forecast to reach USD 28.23 billion by 2031.

Which sensor category is expected to grow the fastest through 2031?

Non-contact level sensors are projected to expand at an 8.11% CAGR between 2026 and 2031.

Why are gas sensors gaining traction now?

Tougher emissions and safety regulations are driving an 8.05% CAGR for gas detection devices.

Which region is leading demand growth?

Asia-Pacific, already holding 36.82% of revenue in 2025, is advancing at a 7.83% CAGR through 2031.

How are tariffs affecting fluid sensor sourcing?

Higher United States tariffs on Chinese semiconductors have pushed many manufacturers to relocate assembly to Mexico, Vietnam, and Eastern Europe.

What opportunities exist for new entrants?

Growth niches include battery-free wireless probes, AI-enabled predictive maintenance platforms, and single-use hygienic sensors for biopharma processes.

Page last updated on: