Sensors In Oil And Gas Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

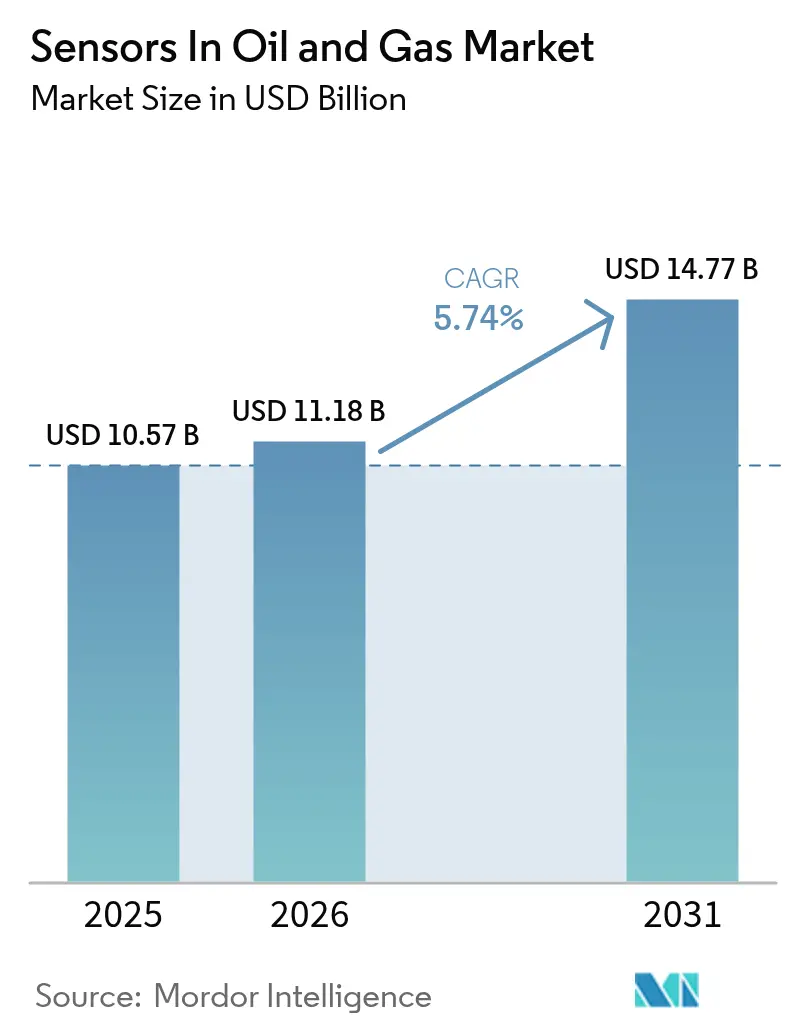

| Market Size (2026) | USD 11.18 Billion |

| Market Size (2031) | USD 14.77 Billion |

| Growth Rate (2026 - 2031) | 5.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sensors In Oil And Gas Market Analysis by Mordor Intelligence

Sensors in oil and gas market size in 2026 is estimated at USD 11.18 billion, growing from 2025 value of USD 10.57 billion with 2031 projections showing USD 14.77 billion, growing at 5.74% CAGR over 2026-2031. This uptrend reflects operators’ rapid shift toward digital‐first asset strategies that cut downtime, curb emissions, and improve worker safety. North America anchors global revenue on the back of shale automation mandates, while Asia-Pacific shows the quickest climb as governments tie new capacity approvals to digital-readiness metrics. Demand favors platform-agnostic sensor suites that merge edge AI with secure wireless protocols, reducing brownfield retrofit costs and delivering enterprise-wide visibility. Established automation majors defend share through global service networks and IECEx-certified portfolios, yet niche innovators are succeeding with purpose-built, harsh-environment solutions that streamline methane quantification and deepwater integrity checks. Because digital twins now underpin maintenance scheduling, operators increasingly embed multi-parameter sensors in rotating equipment, pipelines, and flare stacks to realize real-time risk scoring and energy-efficiency gains.

Key Report Takeaways

- By sensor type, pressure devices held 26.35% of the sensors in oil and gas market share in 2025; ultrasonic designs are projected to grow at a 6.5% CAGR through 2031.

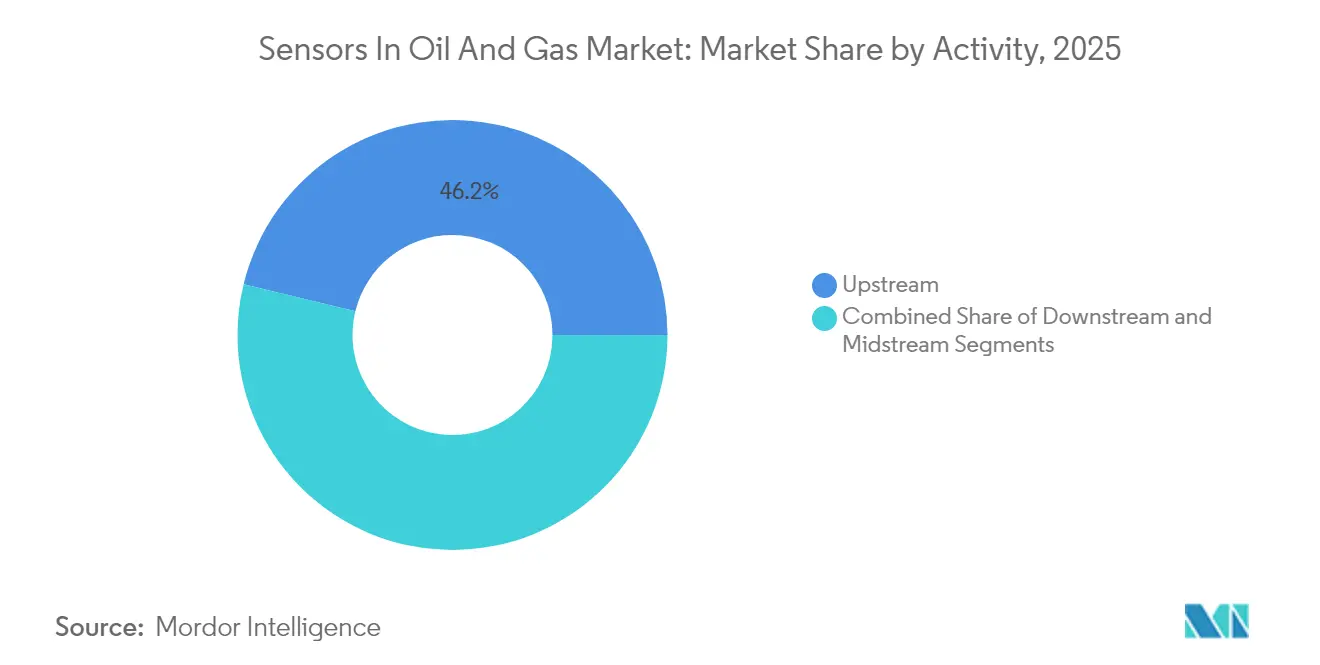

- By activity, upstream accounted for 46.20% share of the sensors in oil and gas market size in 2025, while midstream is poised to expand at a 6.92% CAGR to 2031.

- By application, process safety and emergency shutdown platforms captured 34.35% of 2025 revenue in the sensors in oil and gas market; emissions monitoring is advancing at a 6.6% CAGR through 2031.

- By connectivity, wired networks retained 71.10% share in 2025 in the sensors in oil and gas market; wireless deployments are forecast to post a 7.12% CAGR between 2026-2031.

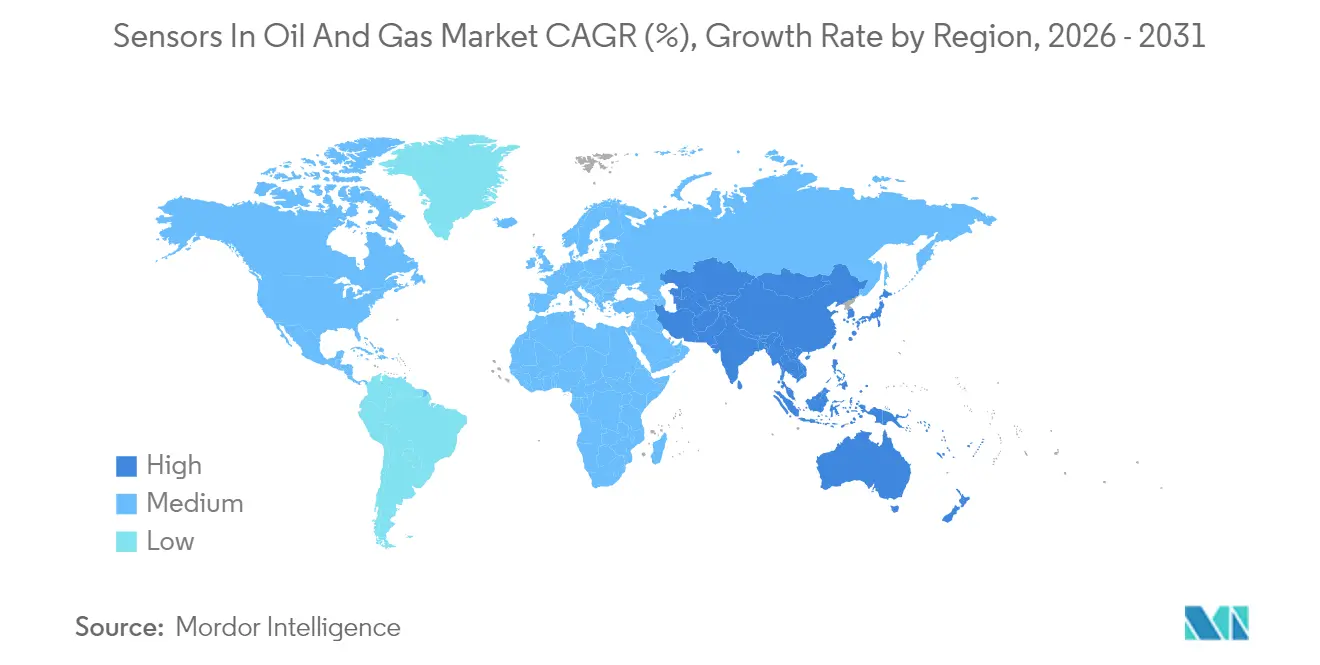

- By geography, North America retained 38.40% share in 2025 in the sensors in oil and gas market; Asia-Pacific is forecast to post a 6.95% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sensors In Oil And Gas Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-twins-enabled predictive maintenance | +1.2% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Rising demand for integrated safety-instrumented systems | +1.0% | Global, regulatory-driven in North America and EU | Short term (≤ 2 years) |

| Acceleration of deep-water and subsea projects post-COVID | +0.8% | Global offshore regions, concentrated in Gulf of Mexico, North Sea, Brazil | Medium term (2-4 years) |

| Increasing shale automation in North America | +0.7% | North America, primarily US Permian Basin | Short term (≤ 2 years) |

| Edge-AI sensor fusion for real-time asset integrity | +0.9% | Global, with advanced deployment in developed markets | Long term (≥ 4 years) |

| Methane-leak detection mandates (OGMP 2.0, EPA, EU) | +1.1% | Global, regulatory focus in North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Digital-twins-enabled Predictive Maintenance

Global majors now pair cloud-hosted twins with edge analytics to pre-empt pump, compressor, and turbine failures. Saudi Aramco trimmed power needs 18% and slashed inspection times 40% at Khurais by embedding thousands of sensors linked to AI models.[1]Saudi Aramco, “数字化油气行业及油田技术创新,” ARAMCO.COM Rotating equipment downtime, historically costing millions of USD per day, is falling as operators schedule repairs based on anomaly scores instead of calendar intervals. Adoption spreads fastest in offshore assets where logistics costs multiply unscheduled stoppages. Because these projects demand multi-physics simulation, vendors that bundle sensors with modeling software gain cross-sell leverage. Early ROI evidence is shifting budget lines from time-based to condition-based maintenance, locking in long-term demand for resilient, self-diagnosing devices.

Rising Demand for Integrated Safety-Instrumented Systems

IEC 61511 compliance now favors unified platforms that converge gas, flame, and shutdown loops. MSA’s S5000 detector, locally assembled in Saudi Arabia, extends calibration intervals to two years while retaining SIL 2 certification.[2]Oil & Gas News, “MSA improves workers’ safety with local gas detectors,” OGNNEWS.COM Operators report fewer site visits and faster startup testing when disparate safety layers run over a common protocol. Investment momentum is highest in refineries and LNG plants undergoing debottlenecking, as tying safety to real-time alarms satisfies both insurers and regulators. Solution providers with local build centers speed up hazardous-area approvals, a decisive advantage in Gulf states mandating in-country value. Heightened risk awareness after recent flaring incidents further cements budget priority for expandable safety backbones that scale with brownfield expansions.

Acceleration of Deep-water and Subsea Projects Post-COVID

Deferred FIDs are now closing, reviving demand for sensors rated beyond 1,000 bar. Shell’s 2024 pact with Baker Hughes on the VitalyX platform underscores operators’ appetite for analytics-ready subsea instrumentation that ships with dual redundancy and digital redundancy paths for 25-year life cycles. Survivability in wide thermal windows pushes suppliers toward silicon-on-insulator MEMS and exotic alloy housings. Because topside bandwidth is scarce, embedded microcontrollers preprocess high-frequency vibration and chemistry signals before uplink, cutting data loads by up to 70%. Early adopters in Brazil and Norway confirm that such architectures cut ROV intervention trips, shaving OPEX by low‐single-digit percentages annually. As subsea production moves to remote power hubs, the business case for autonomous, AI-enabled sensors scales quickly.

Increasing Shale Automation in North America

Permian operators now deploy measurement-while-drilling arrays linked to cloud geosteering engines that recalibrate bit trajectory in seconds. Fiber-optic DAS strings log fracture hits along laterals, letting engineers taper proppant schedules on the fly. University of New Mexico prototypes achieved 5 ppm methane detection with 97% classification accuracy in field pilots, illustrating how academia accelerates cost-effective leak monitoring.[3]University of New Mexico, “Solid-State Mixed-Potential Electrochemical Sensors,” DOI.ORG Tight-budget independents adopt edge devices with subscription analytics to bypass capex cycles, supporting broader fleet adoption. As pad drilling intensifies, drill-to-mill sensors extend to artificial lift gearboxes, creating a contiguous data thread from spud to abandonment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in upstream CAPEX cycles | -0.9% | Global, particularly pronounced in North America shale plays | Short term (≤ 2 years) |

| Cyber-security vulnerabilities in wireless sensor networks | -0.6% | Global, heightened concern in critical infrastructure regions | Medium term (2-4 years) |

| Scarcity of IECEx-certified component suppliers | -0.4% | Global, most acute in emerging markets | Medium term (2-4 years) |

| Harsh-environment survivability limits for MEMS | -0.3% | Subsea, Arctic, and high-temperature applications globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Upstream CAPEX Cycles

Sensor rollouts often sit at the mercy of commodity swings. During 2020-2023 price dips, many independents trimmed instrumentation budgets by up to 25%, deferring brownfield upgrades until WTI stabilized above USD 70/bbl. Because sensors in oil and gas market growth relies on multi-year programs, turbulence hampers volume ramps for new platforms, elongating supplier breakeven horizons. Larger IOCs shield projects by rolling OPEX into digital transformation line items, yet even they staged procurement in phases to preserve cash. Vendors counteract by offering leasing models and outcome-based contracts that spread costs, but uptake remains uneven across regions.

Cyber-security Vulnerabilities in Wireless Sensor Networks

Expanding attack surfaces attract sophisticated adversaries targeting operational technology. Incidents surged 70% between 2020 and 2023, spurring North American pipeline operators to adopt zero-trust architectures and IEC 62443 assessments. Patch management complicates remote well pads where bandwidth drops below 256 kbps. Insurance underwriters now factor cyber posture into premiums, nudging asset owners to invest in encrypted protocols and endpoint detection. Nonetheless, talent shortages in OT security impede rollout speed, especially among NOC-led ventures in developing economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Pressure Dominates Amid Ultrasonic Innovation

Pressure devices owned 26.35% of 2025 revenue, underscoring their omnipresence from wellhead choke monitoring to custody transfer skids across the sensors in oil and gas market. Ultrasonic meters, while smaller in base, are expanding at 6.5% CAGR as non-intrusive designs cut maintenance and simplify calibration loops, a critical advantage in LNG and multiphase pipelines. Temperature, flow, and level instruments maintain stable trajectories, protected by their foundational role in mass-energy balance calculations. Vibration sensors enjoy renewed interest as predictive maintenance programs proliferate, while multi-gas arrays ride emissions mandates.

Buyers increasingly favor consolidated transducer suites that blend pressure, temperature, and vibration into one housing, shrinking penetration points and lowering fugitive emission risks. Suppliers respond with ASIC-based signal chains that linearize multiple elements simultaneously, slashing drift across a 10-year horizon. For remote heads, battery-optimized MEMS pressure cells now boast sub-1 µA sleep currents, extending field life beyond five years in wireless nodes. Integrators leverage these gains to present unified dashboards, easing correlation of process excursions and chronic equipment fatigue in a single pane of glass.

By Connectivity: Wireless Transformation Accelerates

Although wired backbones still represent 71.10% of installed endpoints, wireless nodes are climbing at a 7.12% CAGR, double the baseline sensors in oil and gas market growth. Operators prioritize WirelessHART and ISA100 mesh topologies for brownfield retrofits where trenching costs eclipse sensor outlays. Early 5G private networks in Gulf mega-refineries showcase deterministic latency under 5 ms, enabling closed-loop control in non-critical loops.

Battery chemistry strides plus energy harvesting cut maintenance truck rolls; smart power management extends node duty cycles from months to years. Security remains the gating factor, yet chip-level root-of-trust modules paired with over-the-air firmware updates now satisfy IEC 62443 auditors. As real-time location services piggy-back on the same spectrum, operators gain dual workforce safety benefits without extra infrastructure. These combined advantages underpin wireless’ climb from edge monitoring to core control layers by the decade’s close.

By Activity: Midstream Momentum Builds

Upstream still anchors 46.20% of 2025 takings, reflecting heavy drilling activity and reservoir complexity. Completions technology relies on acoustic and pressure sensors resilient to sand erosion and 25,000 psi bursts, reinforcing the segment’s baseline demand. Yet pipeline operators are signing multi-year integrity monitoring contracts that lift midstream revenue at a 6.92% CAGR, outpacing the total sensors in oil and gas market.

Regulators stipulate high-frequency leak surveys, prompting adoption of distributed fiber optics and airborne laser systems integrated with ground-based nodes. Compression stations add vibration and emissions arrays, enabling predictive repair of dry-gas seals. Storage terminals digitalize floating roof tank gauging to curb slop losses, driving level and radar orders. Downstream retains steady spending for process optimization and flaring control, but incremental gains pale beside midstream’s infrastructure boom in Asia and South America

By Application: Safety Systems Lead Growth

Process safety and emergency shutdown solutions captured 34.35% of 2025 billings, underscoring the life-critical priorities that govern procurement in hazardous plants. Because insurance premiums tie directly to incident metrics, SIL-rated sensors offer quantifiable ROI. Emissions monitoring, however, now traces the steepest curve at 6.6% CAGR as carbon pricing spreads across jurisdictions, inserting continuous methane detection clauses into operating licenses.

Pipeline monitoring capitalizes on machine-learning pattern recognition, flagging pressure waves indicative of third-party strikes within seconds. Drilling optimization platforms integrate downhole acoustics with surface torque-and-drag sensors, unlocking drilling performance indexes that shorten vertical sections by double-digit percentages. Cross-application synergies emerge as edge AI engines process safety and environmental data concurrently, reducing hardware overhead while raising situational awareness. Vendors that map these convergent use cases stand to gain outsized wallet share per facility.

Geography Analysis

North America held 38.40% of 2025 revenue, reflecting shale’s appetite for real-time formation and production data and strict EPA leak rules that elevate advanced gas sensing. U.S. supermajors spearhead enterprise-wide digital rollouts, while Canadian operators retrofit oil-sands upgraders with extreme-cold pressure and level instruments. Mexico’s liberalized acreage adds selective demand, tempered by financing hurdles and pipeline bottlenecks.

Asia-Pacific is the sensors in oil and gas market’s fastest-rising arena at 6.95% CAGR, buoyed by China’s policy to embed intelligent sensing across new green- and brownfield facilities and India’s refinery upgrades that require Ethernet-APL-ready instrumentation. LNG import terminals in Indonesia and the Philippines adopt custody-transfer ultrasonic meters to cut imbalance disputes. Vietnam’s 2024 digital plan for energy vaults entails 90% online permitting, indirectly stimulating sensor procurement for live data feeds.

Europe sustains moderate gains as North Sea operators grapple with aging platforms that demand high-spec vibration and corrosion solutions. EU Green Deal legislation cements the switch to continuous emissions monitoring, widening addressable spend. Middle East producers embrace lighthouse refinery concepts, proven by Aramco facilities that showcase 18% energy savings via dense sensor grids. Africa’s nascent basins weigh in with greenfield orders that leapfrog legacy hard-wired layouts in favor of wireless-first, edge-analytics designs, preparing their assets for long-term carbon accountability regimes.

Regulatory Landscape

Methane rules are a key regulatory driver for sensor deployments across upstream, midstream, and downstream assets. In the United States, the EPA finalized performance-based pathways for advanced methane detection under 40 CFR 60.5398b(d) (final rule published March 8, 2024). The framework enables approved alternative test methods (MATM) that support continuous monitoring and periodic screening using sensor-based technologies, rather than relying only on legacy manual approaches. Facilities using alternative monitoring technologies also face structured reporting requirements through EPA systems such as CEDRI, reinforcing demand for sensors that can generate auditable, time-stamped datasets and fit into compliance workflows.

In Europe, EU Methane Regulation (EU) 2024/1787 sets out LDAR, measurement, quantification, and site-level reporting requirements for oil and gas operators, including independent third-party verification and defined technology acceptance criteria. The regulation also extends obligations into the supply chain through import-related reporting beginning in 2025, with equivalency verification timelines reaching 2027. Offshore operations add an additional layer, with the US Bureau of Safety and Environmental Enforcement (BSEE) incorporating updated production measurement and safety standards by reference into 30 CFR Part 250 effective August 10, 2026, which supports higher-spec instrumentation and verification practices on the Outer Continental Shelf.

Value Chain Analysis

The value chain starts with specialized components, including MEMS sensing elements, lasers and optics for optical gas sensing, ASICs/MCUs, radios, power management, high-temperature ceramics, and hazardous-area housings. It then moves through sensor OEM design and certification (IECEx, SIL/IEC 61511), manufacturing, and integration into DCS/SCADA, safety-instrumented systems, and emissions-management platforms. Deployment is shaped by service coverage and calibration capability, with large automation suppliers and oilfield service companies bundling sensors with lifecycle services, analytics, and compliance reporting to reduce integration complexity for IOCs and NOCs.

Supply risk and qualification bottlenecks remain concentrated in niche, high-reliability categories. Downhole fiber-optic sensor programs are constrained by specialized fiber draw tower capacity and lengthy (often 12 to 18 months) qualification cycles for cable designs, while high-temperature ceramic substrates for downhole pressure transducers have single-source exposure concentrated in Japan and Germany. On the demand side, collaborations and long-duration contracts are increasingly influencing procurement and integration: Emersons May 2026 R&D agreement with Saudi Aramco targets next-generation corrosion management, including wireless ultrasonic monitoring, while SLB expanded edge and IIoT enablement through its June 2026 collaboration with Qualcomm Technologies and a June 2026 seven-year Kuwait Oil Company award under the Ahmadi Innovation Valley initiative. These arrangements reinforce that platforms, cybersecurity, and field service ecosystems can be as important to value-chain control as sensor hardware alone.

Competitive Landscape

Market concentration sits in the mid-range: Honeywell, Emerson, ABB, and Siemens together account for under half of 2024 turnover, leveraging global repair hubs, end-to-end suites, and deep certification queues. They emphasize lifecycle contracts that bundle sensors, analytics, and remote condition monitoring, an attractive proposition for resource-constrained NOCs. Multinational incumbents also co-invest in regional assembly, Honeywell’s USD 1.81 billion LNG equipment acquisition broadened its cryogenic sensing catalog and fortified its installed base in Qatar and the U.S. Gulf Coast.

Challenger firms carve footholds by specializing. Sensirion’s optical methane nodes received EPA equivalency, validating newcomer technology in a compliance-critical niche.[4]Sensirion Connected Solutions, “Overview,” SENSIRION-CONNECTED.COM Blackline Safety’s EXO 8 added gamma detection to portable hubs, capturing emergency response budgets. Academic-industry consortia like the University of New Mexico’s electrochemical sensor project inject disruptive IP into the product pipeline, particularly where ultra-low PPM sensitivity is mandatory. Edge-AI software startups partner with hardware OEMs to supply firmware-level anomaly detection, shortening time-to-market for integrated offerings.

Barriers to entry remain material: IECEx audits, safety integrity certification, and after-sales footprints deter pure-play software firms without hardware lineage. Yet operators’ push for open standards pries open proprietary ecosystems, encouraging modular platforms that let buyers mix best-of-breed transducers. Consequently, competitive dynamics hinge on who masters secure data orchestration across multivendor fleets rather than on transducer specs alone.

Sensors In Oil And Gas Industry Leaders

Honeywell International Inc

TE Connectivity Ltd

Robert Bosch GmbH

ABB Ltd

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity area is compliance-grade methane detection and quantification that can support performance-based regulatory pathways and structured reporting. This is pushing demand toward sensor suites that combine continuous monitoring, validation workflows, and secure data pipelines. The EPAs alternative test method framework under 40 CFR 60.5398b(d) and the EU Methane Regulation (EU) 2024/1787, including imports-related reporting starting 2025, create space for vendors that can deliver auditable sensor data, automated QA/QC, and integration into enterprise compliance systems. There is also product-level momentum behind this shift, such as Sensirion Connected Solutions obtaining US EPA approval for its Nubo Sphere wireless methane monitor (April 2025), which reinforces procurement preference for solutions aligned to regulator-recognized methods.

Another opportunity involves scaling autonomous and remote operations that require larger volumes of multi-parameter sensing, especially for offshore and hard-to-access assets where labor and logistics constraints raise the value of closed-loop control and remote integrity management. Recent deployments show how controls modernization, edge analytics, and data platforms increase sensor utilization: Halliburton and Eni reported an industry-first closed-loop rig automation deployment offshore Indonesia using the LOGIX platform (July 2026), and Schneider Electric and Bilfinger deployed EcoStruxure Automation Expert on a normally unmanned installation buoy in the North Sea (June 2026). Longer-cycle procurement also shows up in project awards, including Yokogawas selection as main automation contractor for the USD 13 billion Commonwealth LNG project in Louisiana (July 2026), which supports pull-through for certified sensors across safety, metering, and condition monitoring. Partnerships such as Emerson and Saudi Aramcos corrosion-monitoring R&D (May 2026) point to continuing spend on wireless ultrasonic and integrity-focused instrumentation for brownfield and subsea reliability programs.

Recent Industry Developments

- March 2026: Honeywell launched its 4-Series NDIR Hydrocarbon Gas Sensor designed for monitoring flammable gases such as methane, propane, and butane in industrial environments. The product targets higher reliability in harsh conditions through design features intended to reduce condensation effects, supporting more continuous gas detection use cases in refineries and processing facilities.

- December 2025: Robert Bosch GmbH confirmed implementation of Integrated Asset Performance Management (IAPM) and hybrid digital twins for ADNOC Offshore to unify machinery intelligence across offshore operations. This strengthens the linkage between field sensors and enterprise performance layers, increasing the value of interoperable sensing and contextualized asset data in offshore maintenance workflows.

- September 2024: TE Connectivity completed the acquisition of Sense Eletronica Ltda, a Brazilian manufacturer of factory and process automation sensors. The deal expands TE Connectivitys regional footprint and local product capability for industrial sensing, supporting closer-to-customer supply, service, and customization for process industries including oil and gas.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers sensors used in oil and gas operations to measure, detect, and monitor physical or chemical parameters that support safety, control, and asset performance across onshore and offshore facilities.

Scope exclusions: We exclude general-purpose IT hardware and software platforms that do not primarily function as sensing devices (including standalone analytics tools).

Segmentation Overview

- By Sensor Type

- Gas

- Temperature

- Ultrasonic

- Pressure

- Flow

- Level

- Vibration

- By Connectivity

- Wired

- Wireless

- By Activity

- Upstream

- Midstream

- Downstream

- By Application

- Process Safety and ESD

- Pipeline Monitoring

- Drilling Optimization

- Emissions Monitoring

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial structure of the model and to set practical boundaries for what counts as an oil and gas sensor versus adjacent automation items. We referenced public sources such as the US Energy Information Administration (EIA), International Energy Agency (IEA), and US Bureau of Labor Statistics (for industrial pricing and wage signals), along with OSHA and similar safety guidance, and trade bodies that publish instrumentation and process safety notes.

In parallel, we reviewed company annual reports, 10-K style filings, investor presentations, product catalogs, and credible press coverage to understand where sensors are being deployed, how purchasing cycles work, and what drives replacement demand. Select paid subscriptions were used only to speed up company financial checks, patent lookups, and shipment or trade-level cross-checks when a public series was incomplete. This source list is not exhaustive, and additional references were used during the study for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with sensor suppliers, system integrators, EPC participants, and asset operators across upstream, midstream, and downstream activity. We covered major demand centers across APAC, EMEA, and the Americas so adoption-rate assumptions, replacement cycles, and average selling price movement could be stress-tested and then adjusted when responses consistently pointed to different market behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 20% | APAC: 46% |

| Mid tier: 43% | Functional/Unit leaders: 25% | EMEA: 35% |

| Smaller Players: 22% | Managers: 55% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where oil and gas activity indicators are converted into an addressable sensing demand pool, and then split by where sensors are used in the field. To keep totals realistic, we corroborate the outputs with selective bottom-up approximations, such as sampled supplier revenue splits, channel checks with integrators, and simple ASP times volume ranges for common sensor categories.

Inputs are chosen because they are visible and explainable, even when company disclosures are uneven. The model uses indicators such as upstream capex and rig activity, pipeline additions and integrity programs, refinery and petrochemical throughput trends, safety and emissions monitoring needs, and the observed shift toward wireless and multi-parameter sensing. Forecasts are generated using scenario analysis supported by expert views on oil price sensitivity and project timing, then paired with a light regression check on a few macro and activity variables to avoid overreacting to one-year spikes. Where a bottom-up view is missing for a niche sensor type or geography, we apply a proxy based on similar use-cases, and we keep the adjustment only after it passes interview-based reasonability checks.

Data Validation & Update Cycle

Validation is done in steps so the final number does not depend on one assumption. We compare outputs against independent signals like oil and gas capex direction, automation spend cues, and the expected maintenance and replacement rhythm for field instrumentation, then revisit any large variances by re-checking the driver series and re-contacting sources when needed.

Before sign-off, the model is reviewed by another analyst to catch unit issues, currency timing mismatches, and unusual jumps across regions or activities. Reports are refreshed annually, and interim updates are triggered when material events change near-term demand, such as large project delays, regulatory shifts tied to safety or emissions, or sustained commodity price moves. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Oil and Gas Sensors Market Size Measured Against Other Published Estimates

Published market sizes for sensors in oil and gas can look far apart because each publisher sets its own counting rules and timing for prices and conversions. The differences usually come from what gets included as a sensor, how upstream and downstream activity is weighted, and whether the number is anchored to a recent demand signal or a longer average.

The biggest gap drivers tend to be scope and the treatment of adjacent automation items, such as transmitters bundled inside control systems, full condition monitoring packages, or broader IIoT hardware that is not primarily a sensing device. Results can also shift when firms apply aggressive growth assumptions for wireless adoption, use different average selling price progression methods, or convert currencies using a different month or annual average, which changes the reported USD value.

In Mordor Intelligence's model, the total is built around sensor devices deployed across upstream, midstream, and downstream activities, and adjacent automation hardware is only counted when it is primarily serving a sensing function, which helps keep the number traceable to clear demand drivers.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 11.18 B (2026) | |

| Global Consultancy A | USD 11.41 B (2025) | Uses a different base year and is presented with a broader application lens that can blend sensor revenue with condition monitoring and remote monitoring packages, which shifts the counted value even when the sensor type list looks similar. |

| Regional Consultancy B | USD 4.80 B (2024) | Appears to treat the market as a narrower set of sensor revenues, with limited clarity on whether upstream, midstream, and downstream are all fully counted and whether multi-parameter and safety certified sensors are included consistently across regions. |

The table shows that the spread is mainly explained by what is treated as a sensor-only revenue pool versus bundled monitoring solutions, and by the base year used for pricing and currency timing.

Key Questions Answered in the Report

What is the forecast value for global sensor deployments in oil and gas by 2031?

The sensors in oil and gas market is projected to reach USD 14.77 billion by 2031.

Which region is expected to grow fastest?

Asia-Pacific leads with a 6.95% CAGR through 2031, driven by refinery expansions and digital mandates.

Which sensor type is expanding most quickly?

Ultrasonic devices are forecast to grow at 6.5% CAGR due to their non-invasive flow measurement capability.

Why are wireless networks gaining traction?

Wireless nodes offer flexible retrofits, lower cabling costs, and now meet security and latency standards suitable for critical monitoring.

How are emissions regulations influencing adoption?

New methane-leak mandates require continuous monitoring, accelerating demand for advanced optical and electrochemical sensors.

Page last updated on: