Cornstarch Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 284.62 Million |

| Market Size (2031) | USD 372.91 Million |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cornstarch Packaging Market Analysis by Mordor Intelligence

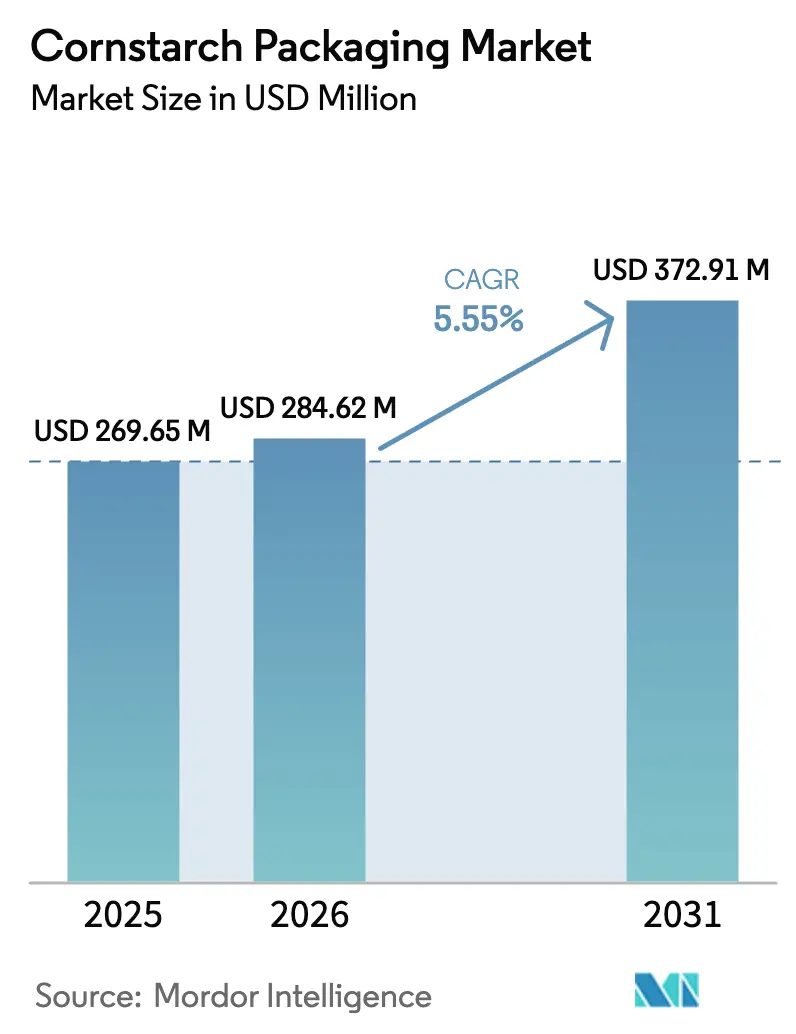

The Cornstarch Packaging Market size is expected to grow from USD 269.65 million in 2025 to USD 284.62 million in 2026 and is forecast to reach USD 372.91 million by 2031 at 5.55% CAGR over 2026-2031. The cornstarch packaging market is benefiting from national bans on single-use plastics, the spread of Extended Producer Responsibility (EPR) laws, and steady gains in composting infrastructure that collectively raise demand for bio-based formats. Continuous improvements in polylactic acid (PLA) processing and thermoplastic starch (TPS) compounding have closed historical performance gaps with conventional plastics, enabling wider substitution in food service, e-commerce, and personal-care applications. Asia-Pacific remains the pivotal production hub and end-market thanks to generous “green bond” subsidies for bio-plants and the commissioning of NatureWorks’ 75,000 tpa Ingeo PLA complex in Thailand. South America posts the fastest regional CAGR at 7.3% as abundant feedstock and circular economy funding unlock new capacity. Meanwhile, North American ethanol oversupply keeps corn prices subdued, lowering PLA feedstock costs and improving margins for the cornstarch packaging market.

Key Report Takeaways

- By product type, bags dominated with 35.72% of the cornstarch packaging market share in 2025, while containers are projected to expand at a 6.95% CAGR by 2031.

- By packaging format, flexible packaging held 60.55% revenue share in 2025; semi-rigid packaging records the fastest 7.46% CAGR through 2031.

- By material composition, PLA-starch blends accounted for 41.62% share of the cornstarch packaging market size in 2025, whereas TPS leads growth at 7.24% CAGR.

- By end-user industry, food and beverage led with a 37.05% share in 2025; retail and e-commerce exhibit the highest 6.78% CAGR to 2031.

- By geography, Asia-Pacific commanded a 38.12% share in 2025, while South America is set to rise at a 7.08% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cornstarch Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Single-use-plastic bans and EPR laws | +1.2% | North America, EU | Medium term (2-4 years) |

| Food brands’ switch to compostable flexible packs | +0.8% | North America, Europe | Short term (≤ 2 years) |

| Retail demand for clear carbon-labelled packaging | +0.6% | Asia-Pacific, North America | Medium term (2-4 years) |

| Corn-ethanol oversupply lowering PLA feedstock cost | +0.9% | North America (global effect) | Short term (≤ 2 years) |

| Asia-Pacific “green-bond” subsidies for bio-plants | +0.7% | Asia-Pacific | Long term (≥ 4 years) |

| IoT-enabled smart bins certifying compostability | +0.4% | Global urban hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Single-use-plastic bans and EPR laws

Regulators are rewriting packaging economics by shifting end-of-life costs to producers. California’s SB 54 requires a 25% cut in single-use plastic packaging by 2032, and Minnesota’s newly approved EPR scheme launches Producer Responsibility Organizations in 2025. [1]“Key EPR for Packaging Dates in 2025: United States,” Packaging School, packagingschool.com In the EU, the forthcoming Packaging and Packaging Waste Regulation obliges all packaging to be recyclable by 2030 and stipulates industrial compostability for items such as coffee pods and fruit labels. These converging mandates reward the cornstarch packaging market because cornstarch-based formats can deliver dual compliance—recyclability and compostability—across jurisdictions.

Food brands’ switch to compostable flexible packs

Global food leaders are accelerating compostable rollouts to meet internal sustainability pledges. Mars introduced plant-based, industrial-compostable wrapping for M&M’s and aims for 100% compliant packaging by 2030. KFC Canada targets full home-compostable packaging by 2025, replacing 200 million pieces annually with corn- and sugarcane-derived materials. [2]“KFC Canada Announces 100% Home Compostable Consumer Packaging by 2025,” KFC Canada, global.kfc.com Starbucks is piloting compostable fiber cups in the U.K. that match conventional performance metrics. Brand-led shifts are translating directly into incremental volumes for the cornstarch packaging market in food service.

Retail demand for clear carbon-labelled packaging

Consumer studies show a 29.73% price premium for carbon-labelled agri-products in China, indicating widespread readiness to reward transparent environmental claims. Retailers are, therefore, requesting packaging that displays authenticated life-cycle metrics. Producers able to pair cornstarch substrates with third-party carbon labels gain shelf differentiation and higher margins, especially across Asia-Pacific, where sustainability cues are gaining weight in purchase decisions.

Corn-ethanol oversupply lowering PLA feedstock cost

The U.S. generated 25.22 billion RINs in 2024 as ethanol output exceeded mandated volumes, depressing corn pricing and shaving PLA raw-material costs. Average 2024 ethanol margins slipped to USD 0.08 per gallon, reinforcing abundant corn supply and positioning the cornstarch packaging market for improved cost competitiveness versus petro-plastics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High unit cost vs. fossil plastics | -1.8% | Global | Short term (≤ 2 years) |

| Limited industrial-composting infrastructure | -1.1% | Developing markets | Medium term (2-4 years) |

| Corn-price volatility from biofuel policy shifts | -0.7% | North America | Short term (≤ 2 years) |

| Marine-degradation labelling gap delaying uptake | -0.5% | Coastal regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High unit cost vs. fossil plastics

Cornstarch formats still carry a price premium. PLA resin prices tracked upward through early 2025 because of energy-intensive processes and restricted scale, widening the spread against low-density polyethylene in price-sensitive markets. Without regulatory incentives or consumer-funded premiums, uptake may stall in cost-focused segments.

Limited industrial-composting infrastructure

Only a fraction of global waste facilities provide the heat, humidity, and residence times needed to degrade PLA or TPS. The Biodegradable Products Institute reports acceptance of compostable packaging at merely 185 U.S. facilities, leaving large geographic gaps. Until infrastructure scales, claims of biodegradability can underdeliver in practice, curbing the expansion of the cornstarch packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Containers Drive Innovation Momentum

Bags retained 35.72% of the cornstarch packaging market share in 2025, anchored in grocery, produce, and carry-out channels. Demand stability comes from their lightweight and cost profile. Containers, however, are projected to grow 6.95% annually to 2031, fuelled by collaborations such as NatureWorks-IMA’s compostable coffee pod compatible with Keurig brewers. This shift illustrates how rigid PLA bodies can now match brewing pressure and barrier requirements, unlocking fresh volume.

In parallel, advances from the Fraunhofer Institute in multilayer PLA films with in-line recyclability enhance cross-category potential. As a result, the cornstarch packaging market is blurring traditional boundaries: pouches integrate spouts, boxes adopt water-resistant coatings, and cups incorporate TPS-based lids. Containers’ rising share within the cornstarch packaging market size signals the sector’s pivot toward higher-margin, performance-critical niches.

By Packaging Format: Semi-Rigid Gains Traction

Flexible formats captured 60.55% of revenue in 2025, extending the cornstarch packaging market’s early success in wraps, liners, and mailers. Yet semi-rigid variants are forecast to expand 7.46% annually as brands hunt for middle-ground solutions that combine form retention with material savings. Upfield’s plastic-free, recyclable plant-butter tub exemplifies this hybrid value and points to substitution potential for yogurt pots, deli trays, and salad bowls.

Research into PLA/PCL blends with antimicrobial additives shows semi-rigid packs can achieve food-safety shelf-life extensions previously reserved for PET or PS. Consequently, semi-rigid packaging’s growing contribution to the cornstarch packaging market size indicates that structural performance is no longer a barrier to broader adoption.

By Material Composition: TPS Emerges as Growth Leader

PLA-starch blends held a 41.62% share in 2025 due to balanced mechanical and processing properties. Thermoplastic starch is on track for a 7.24% CAGR, buoyed by breakthroughs such as the University of Copenhagen’s barley-based material that biodegrades in two months yet retains water resistance. These gains lower reliance on petro-derived co-polymers and enhance price competitiveness for the cornstarch packaging market.

Concurrently, novel PLA/PBAT films that pair high oxygen barriers with fast compostability broaden the appeal of snack and coffee packs. The evolution underscores how R&D is propelling the cornstarch packaging market from early-generation blends toward high-performance bio-polymer families.

By End-user Industry: Retail and E-commerce Acceleration

The food and beverage channel comprised 37.05% of demand in 2025 as hygiene rules and chilled-chain growth favored certified compostable wraps. Retail and e-commerce are slated for a 6.78% CAGR, underpinned by high-velocity order fulfillment that seeks curb-side recyclable or compostable dunnage. Vital Proteins cuts 4 million lb of plastic per year by shifting collagen-powder canisters from PET to 80% paperboard with cornstarch linings.

With 60% of consumers stating stronger climate concerns and favoring third-party certified packaging, online brands exploit the cornstarch packaging market to reinforce eco-branding while softening regulatory risk under emerging EPR schemes.

Geography Analysis

Asia-Pacific anchored the cornstarch packaging market with 38.12% revenue in 2025, sustained by Thai, Japanese, and Korean incentives that compress financing costs for PLA assets. Regional governments also link bio-packaging uptake to marine litter reduction targets, accelerating public procurement of compostable service ware. Public–private initiatives, such as the ADB-backed USD 500 million Indonesia program, add further momentum.

South America is the fastest-growing zone, expected to post 7.08% CAGR as Brazil, Argentina and Colombia leverage abundant corn and sugarcane residues to scale TPS and PLA production. Policy moves toward EPR in Chile and Colombia, plus emerging carbon-credit revenues for the bio-material displacement of petro-plastics, create a strong pull for the cornstarch packaging market across the continent.

North America enjoys stable growth, buoyed by state-level EPR laws and consistent corporate sustainability commitments. Ranpak’s 16% sales jump to USD 105 million in Q4 2024 exemplifies switching from bubble wrap to paper and cornstarch fillers among e-commerce accounts. Europe expands steadily as the pending Packaging and Packaging Waste Regulation tightens design-for-recycling and compostability thresholds. The Middle East and Africa remain nascent but show rising pilot programs in Gulf Cooperation Council countries exploring biomass conversion.

Competitive Landscape

The cornstarch packaging market is moderately fragmented. NatureWorks, Total Corbion, and Novamont leverage integrated feedstock-to-resin footprints; their collective share keeps leadership but leaves space for nimble entrants. TIPA Corp pioneers home-compostable films for dry goods, while Danimer Scientific targets PHA-starch hybrids for marine-degradable applications. Traditional converters such as Stora Enso are restructuring toward renewable divisions, announcing a new board line in Finland capable of processing starch composites by 2027. [4]“Stora Enso Interim Report January–March 2025,” Stora Enso, storaenso.com

Investment flows validate the sector’s upside. B’Zeos attracted EUR 5 million to scale seaweed-based films, Eco-Vative raised USD 184 million for mycelium-based rigid forms, and Bpacks secured EUR 1 million for bark-fiber technologies. As substitution accelerates, incumbents are streamlining portfolios and entering joint ventures to fortify raw-material access, mitigate feedstock risk, and widen downstream market presence.

Cornstarch Packaging Industry Leaders

NatureWorks LLC

Total Corbion PLA bv

Novamont S.p.A.

Plantic Technologies (Kuraray)

Vegware Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: EPA proposed RFS volumes for 2026-2027, retaining corn-ethanol support that stabilizes PLA resin supply.

- May 2025: Closed Loop Partners launched grants up to USD 50,000 to expand compostable packaging programs, tackling infrastructure gaps.

- May 2025: Washington passed EPR legislation, becoming the seventh U.S. state to adopt producer-funded waste schemes.

- March 2025: Stora Enso reorganized around renewable packaging, with a new consumer board line slated for 2027.

- January 2025: NatureWorks appointed Erik Ripple as CEO to guide PLA expansion in Thailand.

- December 2024: Bpacks closed a EUR 1 million seed round to commercialize bark-based rigid packaging.

- November 2024: B’Zeos raised EUR 5 million for compostable seaweed films.

- October 2024: AlterPacks secured USD 1.6 million to convert food by-products into rigid plant-fiber packs.

Global Cornstarch Packaging Market Report Scope

Cornstarch packaging utilizes polylactic acid (PLA), derived from cornstarch, to create a plastic-like material known as bioplastics. The rising demand for cornstarch-based packaging reflects a broader movement towards sustainable and eco-friendly alternatives to conventional petroleum-based plastics. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The cornstarch packaging market is segmented by product type (Containers, Bags, Pouches and Boxes), by end- user industry (Food, Personal Care & Cosmetics, Pharmaceuticals, Retail and Other End-User Industries) and by geography (North America, Europe, Asia Pacific, South America and Middle East and Africa), The market sizing and forecasts are provided in terms of value (USD) for all the above segments.

| Containers |

| Bags |

| Pouches |

| Boxes |

| Cups and Cutlery |

| Flexible Packaging |

| Rigid Packaging |

| Semi-Rigid Packaging |

| Pure PLA (Corn-derived) |

| PLA-Starch Blends |

| Thermoplastic Starch (TPS) |

| Starch-Cellulose Composites |

| Food and Beverage |

| Personal Care and Cosmetics |

| Pharmaceuticals |

| Retail and E-commerce |

| Industrial and Institutional |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Singapore | ||

| Malaysia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Containers | ||

| Bags | |||

| Pouches | |||

| Boxes | |||

| Cups and Cutlery | |||

| By Packaging Format | Flexible Packaging | ||

| Rigid Packaging | |||

| Semi-Rigid Packaging | |||

| By Material Composition | Pure PLA (Corn-derived) | ||

| PLA-Starch Blends | |||

| Thermoplastic Starch (TPS) | |||

| Starch-Cellulose Composites | |||

| By End-user Industry | Food and Beverage | ||

| Personal Care and Cosmetics | |||

| Pharmaceuticals | |||

| Retail and E-commerce | |||

| Industrial and Institutional | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Singapore | |||

| Malaysia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the cornstarch packaging market?

The cornstarch packaging market size stands at USD 284.62 million in 2026 and is projected to reach USD 372.91 million by 2031.

Which region is the largest consumer of cornstarch packaging?

Asia-Pacific leads the market with 38.12% share in 2025, supported by policy incentives and new PLA capacity.

Which product type is growing fastest?

Containers are forecast to grow at a 6.95% CAGR through 2031 thanks to improved rigid PLA designs suitable for coffee pods and meal trays.

What is the biggest restraint to market growth?

High unit costs versus fossil plastics remain the primary barrier, shaving an estimated 1.8 percentage points off forecast CAGR.

How do EPR laws influence demand?

EPR schemes transfer disposal costs to producers, making compostable and recyclable cornstarch solutions financially attractive and accelerating adoption.

Which material blend shows the most promise?

Thermoplastic starch (TPS) is the growth leader with a 7.24% CAGR due to cost advantages and rapid biodegradability improvements.

Page last updated on: