Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

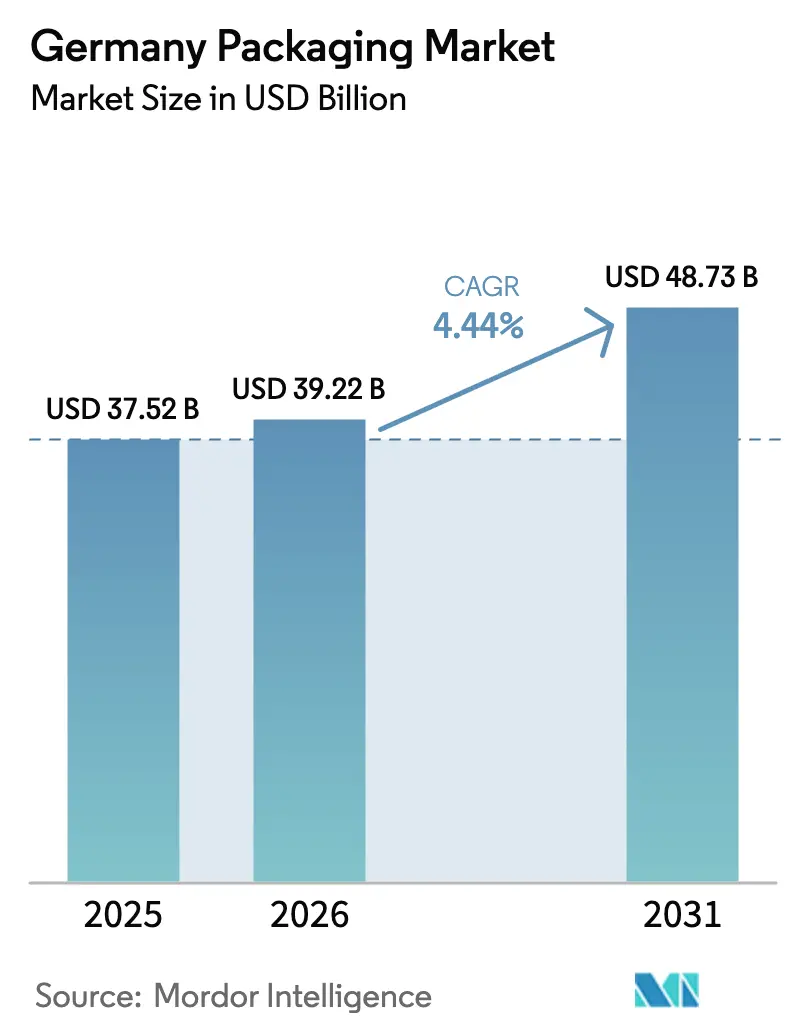

| Base Year Market Size (2025) | USD 37.52 Billion |

| Market Size (2026) | USD 39.22 Billion |

| Market Size (2031) | USD 48.73 Billion |

| Growth Rate (2026 - 2031) | 4.44% CAGR |

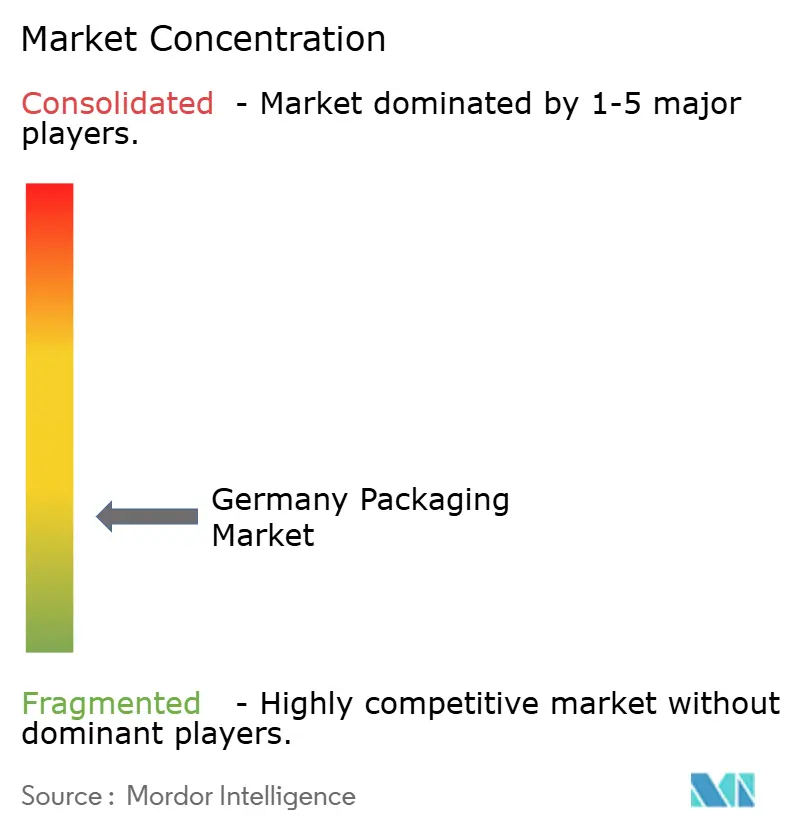

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Packaging Market Analysis by Mordor Intelligence

The Germany packaging market size is expected to increase from USD 39.22 billion in 2026 to USD 48.73 billion by 2031, growing at a 4.44% CAGR over 2026-2031. Strong demand from Germany’s diversified manufacturing base, resilient pharmaceutical exports, and entrenched circular-economy policies underpin this expansion. Industrial production swings, however, quickly translate into packaging order patterns that favor converters with flexible capacity scheduling. The deposit return system, or Pfandsystem, processed more than 20 billion containers in 2025 and maintained a 98% material return rate, reinforcing Germany’s reputation as the benchmark for extended producer responsibility. Post-Brexit realignment of European cold-chain flows is routing additional biologics volumes through Frankfurt and Hamburg airports, accelerating investment in insulated shippers and phase-change materials. Premiumisation trends in cosmetics, automotive accessories, and watches are driving demand for high-specification folding cartons and rigid boxes, though brand owners are shifting toward mono-material structures to meet recyclability thresholds. At the same time, additive manufacturing of molds and tooling is shrinking time-to-market for limited-edition launches, sharpening competition on responsiveness.

Key Report Takeaways

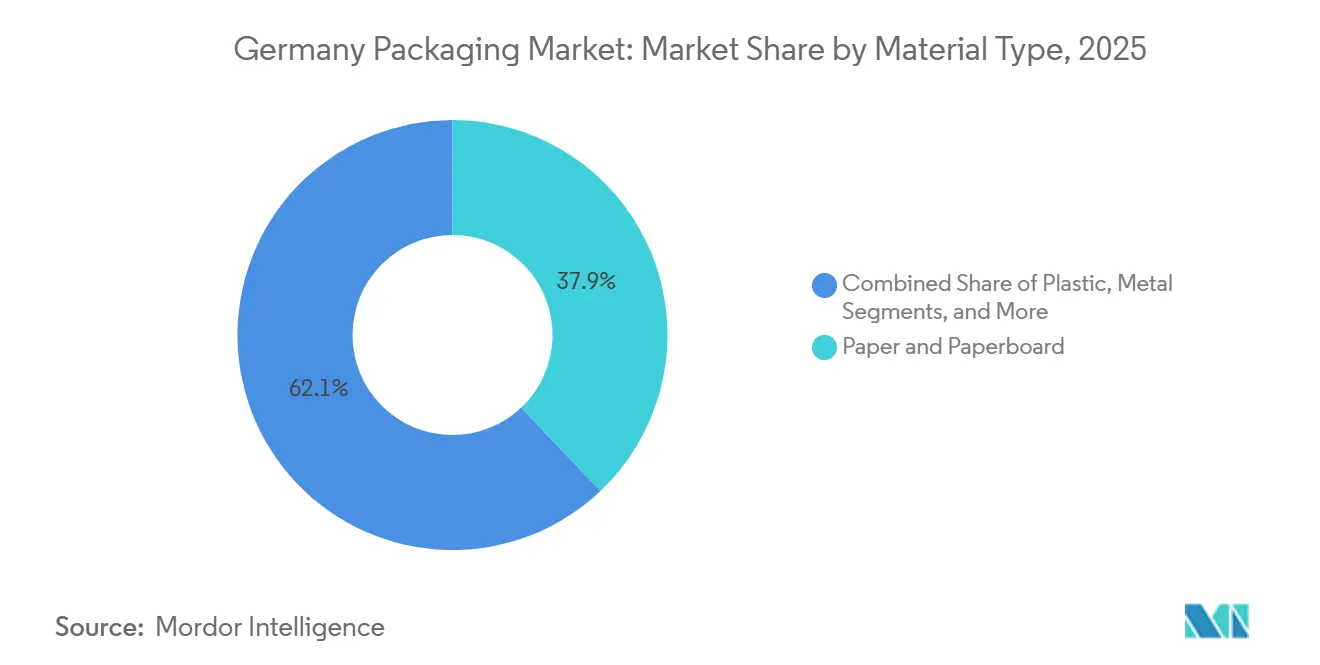

- By material type, paper and paperboard led with 37.91% of the Germany packaging market share in 2025. Biodegradable plastics are forecast to progress at a 4.83% CAGR through 2031, the fastest among all materials.

- By product type, corrugated boxes and containers accounted for 23.88% of the Germany packaging market size in 2025. Pouches are projected to expand at a 5.21% CAGR from 2026-2031, outpacing all other product formats.

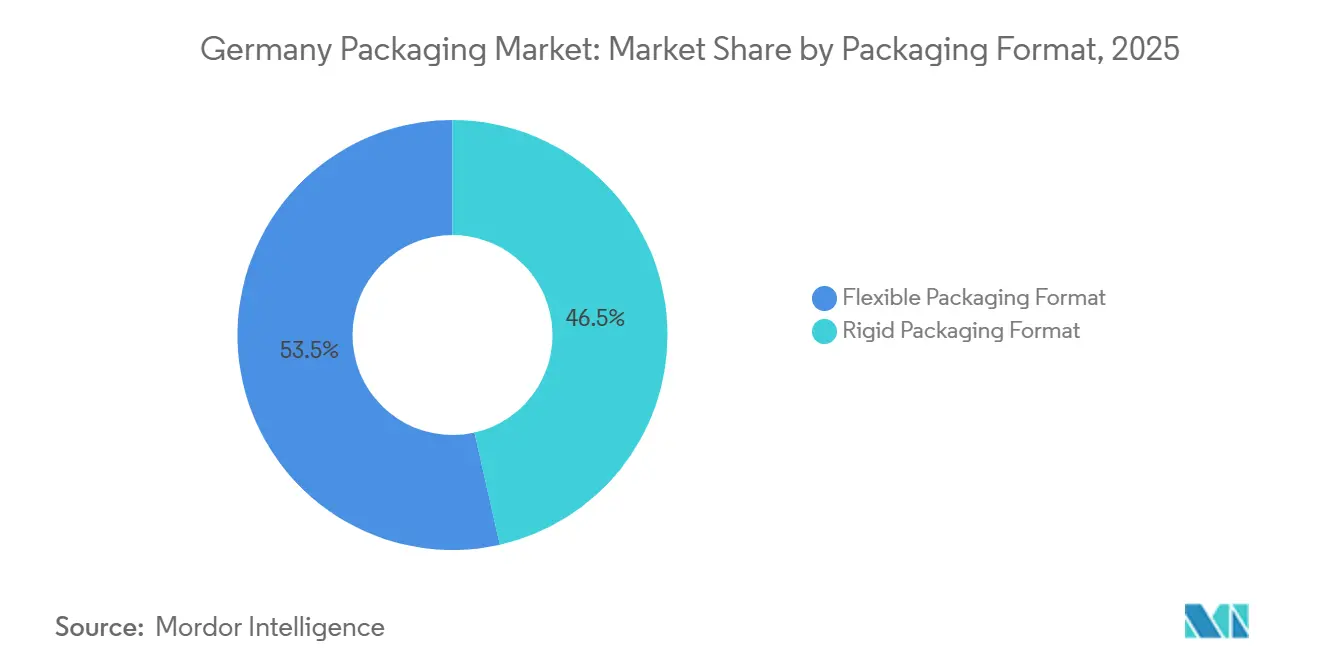

- By packaging form, flexible packaging accounted for 53.52% market share in 2025 and advanced at a 4.97% CAGR through 2031.

- By end-user, food accounted for 31.48% of the Germany packaging market size, and pharmaceutical and medical applications advanced at a 5.66% CAGR between 2026-2031, the quickest among user industries.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pharmaceutical Cold-Chain Expansion Post-Brexit | +0.8% | Germany, with spillover to Benelux and Central Europe | Medium term (2-4 years) |

| Regulatory Push For Deposit Return System Expansion | +1.2% | Germany, national implementation with regional pilot programs | Short term (≤ 2 years) |

| Luxury Goods Export Growth Fueling Premium Packaging | +0.5% | Germany, concentrated in Bavaria and Baden-Württemberg | Long term (≥ 4 years) |

| Surge In Craft Beverage Canning Facilities | +0.7% | Germany, with early gains in Bavaria, North Rhine-Westphalia, and Thuringia | Medium term (2-4 years) |

| 3D Printing Of Packaging Tooling Reducing Lead Times | +0.4% | Germany, national adoption with concentration in industrial clusters | Medium term (2-4 years) |

| Hydrogen-Powered Delivery Fleets Lower Scope 3 Emissions | +0.3% | Germany, pilot deployments in Saxony and Bavaria | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Pharmaceutical Cold-Chain Expansion Post-Brexit

European biologics traffic that once consolidated in the United Kingdom is increasingly staged through Frankfurt and Hamburg, lifting demand for temperature-controlled secondary packaging and pre-qualified pallet shippers. German converters that hold ISO 15378 certification for primary containers have secured multi-year supply agreements with vaccine producers, and Gerresheimer’s investment in hermetic blister capacity (EUR 2 billion, USD 2.26 billion) positions the company to capture higher value orders.[1]Gerresheimer AG, “Pharmaceutical Packaging Solutions,” gerresheimer.com Polymer syringes with integrated needle shields introduced by SCHOTT Pharma in 2024 further illustrate the migration toward break-resistant formats in automated fill-finish environments.

Regulatory Push for Deposit Return System Expansion

In 2025, Germany extended its deposit scheme to milk and juice cartons, adding an estimated 600 million additional units to reverse-logistics channels within the first year. Converters swiftly re-engineered bottles in polyethylene terephthalate to improve optical sorting efficiency, while machinery suppliers Krones and ALPLA retrofitted blow-molding lines for tethered-cap compliance. Because the EU Packaging and Packaging Waste Regulation mirrors Germany’s 90% collection benchmark, domestic producers enter the 2026-2031 horizon with a compliance head start, translating into lower contingency capital expenditure.

Luxury Goods Export Growth Fueling Premium Packaging

Luxury automotive accessories, high-end cosmetics, and horology products exported from Bavaria and Baden-Württemberg continue to favor rigid paperboard boxes with tactile varnishes. Cost-inflation in specialty pigments, however, is prompting a shift to mono-material cartonboard laminated with dispersion barriers developed by Mondi’s Steinfeld mill upgrade (EUR 50 million, USD 56.5 million).[2]Mondi Group, “Sustainable Solutions and Investments,” mondigroup.com These structures achieve comparable shelf impact yet qualify for existing fiber recycling streams, allowing luxury brands to meet recyclability pledges without diluting brand aesthetics.

3D Printing of Packaging Tooling Reducing Lead Times

Söhner Kunststofftechnik’s fused deposition modeling workflow produces prototype molds in a matter of days, cutting tooling lead times and costs by up to 50%. Faster iteration cycles are especially valuable for short-run promotional SKUs in fast-moving consumer goods. Heidelberger Druckmaschinen quantified a 40% reduction in time-to-market for folding cartons by combining digital presses with 3D-printed tooling, enabling brand owners to capitalize on seasonal demand spikes. Concentration of additive manufacturing capacity in Germany’s automotive clusters speeds knowledge spillover into packaging workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Labor Shortfall In High-Speed Automation | -0.9% | Germany, national with acute pressure in Bavaria and Baden-Württemberg | Short term (≤ 2 years) |

| Capital Expenditure Freeze Amid Interest Rate Volatility | -1.1% | Germany, affecting small and mid-sized converters disproportionately | Short term (≤ 2 years) |

| Fragmented Municipal Recycling Infrastructure | -0.5% | Germany, variability across 16 federal states | Medium term (2-4 years) |

| Cybersecurity Risks In Connected Packaging Lines | -0.3% | Germany, concentrated in Industry 4.0 adopters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortfall in High-Speed Automation

An aging workforce and tight vocational-training pipeline leave many converters struggling to staff mechatronics and PLC programming roles needed to operate multi-lane pouch fillers and rotary blow molders. Companies are installing operator-assist interfaces and remote-diagnostics modules to partially offset the talent gap, but these solutions cannot fully replace experienced technicians. As a result, planned speed increases on existing assets are slipping, curbing near-term throughput gains.

Capital Expenditure Freeze Amid Interest Rate Volatility

Borrowing costs remain elevated, and German GDP growth was flat in 2025, leading several mid-tier converters to defer purchases of flexographic presses and aseptic fillers. The pause is most acute in biodegradable-film lines, which entail a higher technical risk and require extensive product qualification trials. By contrast, multinationals such as Amcor (EUR 1 billion, USD 1.13 billion in sustainability R&D through 2025) continue to draw on internal capital, widening the technology gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Biodegradable Plastics Move From Niche to Mainstream

Paper and paperboard commanded 37.91% of the Germany packaging market size in 2025 due to corrugated demand from e-commerce shipments. Nevertheless, biodegradable plastics are expanding at a 4.83% CAGR and are on track to double European bioplastic capacity to 4.69 million tons by 2030, with Germany contributing the largest share.[3]European Bioplastics, “Bioplastics Market Data,” european-bioplastics.org Federal grants from the Ministry of Food and Agriculture accelerate R&D in bio-based polymers, encouraging converters to retrofit extrusion lines to run polylactic acid and polybutylene succinate blends.

Converters view bio-resins as a hedge against volatility in fossil-based polymers and looming recycled-content mandates. Stora Enso’s Maxau mill upgrade (EUR 120 million, USD 135.6 million) adds specialty barrier paperboard that enables dry food and frozen applications to displace polyethylene terephthalate laminates. Metal packaging, led by aluminum cans, benefits from the 98% return infrastructure, while container glass retains niche positions in pharmaceuticals where inertness outweighs weight penalties.

By Product Type: Pouches Capture Share Within Flexible Lines

Corrugated boxes held 23.88% share in 2025, yet pouches are forecast to expand at a 5.21% CAGR, leveraging consumer preference for resealable, lightweight formats. Mondi’s retortable pouch, commercialized in 2024, cut material use by 70% compared with steel cans while preserving shelf life, illustrating the substitution pathway for shelf-stable meals. Folding cartons continue to serve OTC pharmaceuticals and cosmetics, but order sizes are shortening as brands test seasonal graphics via digital print.

Within rigid plastics, bottle demand is stable, though closure makers are moving toward tethered designs to meet EU litter-prevention rules. Metal aerosol containers remain critical for industrial lubricants, and local beverage canners have added sleeving capability for small-batch craft drinks. Koenig and Bauer’s digital presses (EUR 1.27 billion, USD 1.44 billion in packaging machinery revenue, 2024) support rapid artwork swaps that align with micro-segmented marketing campaigns.

By Packaging Format: Flexible Leads on Carbon and Cost Metrics

Flexible formats represented 53.52% of the Germany packaging market share in 2025 and will grow at 4.97% CAGR to 2031 as brand owners emphasize transport efficiency. A typical stand-up pouch weighs up to 85% less than a comparable glass jar, lowering freight emissions and supporting corporate Net-Zero roadmaps. Amcor’s AmPrima recycle-ready polyethylene laminate, introduced in 2024, offers oxygen and moisture barrier performance comparable to older polyamide structures without compromising curbside sortability.

Rigid packaging maintains relevance where compression resistance or premium shelf presence is paramount. Beverage glass, for instance, endures in premium lagers, while molded pulp trays are displacing expanded polystyrene in fresh produce. The EU design-for-recycling deadline in 2030 is accelerating the development of mono-materials, and German research institutes are actively testing high-barrier coatings compatible with existing film-recycling lines.

By End-User: Pharmaceuticals Outpace Food and Beverage

Food applications accounted for 31.48% of the Germany packaging market size in 2025, reflecting the country’s large grocery and confectionery base. However, pharmaceutical and medical packaging is projected to log the highest CAGR of 5.66% through 2031, driven by the expansion of biologics and stricter serialization rules. Gerresheimer’s hermetic blister investment and SCHOTT Pharma’s polymer syringes illustrate the capital intensity required to meet ISO 15378 standards.

Beverage converters profit from aluminum-can momentum tied to deposit-return convenience, while personal-care brands sustain demand for high-gloss cartonboard with UV coatings. Industrial chemical drums-particularly intermediate bulk containers from Schütz, are looking at hydrogen-powered forklifts within plants, dovetailing with customer Scope 3 reduction targets. Agriculture and automotive remain smaller segments, but both benefit from Germany’s precision-engineering clusters, which favor protective dunnage solutions.

Geography Analysis

Germany’s federal structure shapes localized recycling performance, with some states operating near 100% optical-sort purity while others struggle with mixed-waste contamination. Bavaria and Baden-Württemberg generate outsized premium packaging demand because of dense luxury automotive and cosmetics ecosystems. North Rhine-Westphalia’s petrochemical heartland anchors intermediate bulk container usage, and Saxony’s Leipzig corridor- home to BMW’s hydrogen vehicle pilots- provides a proving ground for zero-emission intralogistics.

The extended deposit return system creates nationwide material loops that reduce virgin resin imports, buffering converters against polymer price spikes. Federal hydrogen funding of EUR 9 billion (USD 10.17 billion) through 2030 has so far upgraded only 100 public refueling sites, limiting over-the-road rollout but offering immediate gains on factory campuses. Frankfurt and Hamburg airports, already central to pharmaceutical exports, are courting cold-chain tenants with tax relief for ramp-side warehouses, further cementing Germany’s gateway status.

Proximity to end-use sectors is critical because just-in-time delivery norms leave little slack in supply chains. Corrugated producers in Cologne, for instance, allocate dedicated runs for next-morning shipment to adjacent e-commerce fulfillment centers. Freight bottlenecks during 2025 river-level lows on the Rhine reminded shippers of multimodal vulnerability, spurring contingency stock investments that temporarily lifted linerboard demand. As recycling harmonization progresses, southern states may lead pilot trials of digital watermarks to enable pack-level identification in material recovery facilities, a technology already under assessment by the Federal Office for Information Security.

Competitive Landscape

The Germany packaging market features a balance of global majors and agile mid-caps. Amcor’s Kreuzlingen upgrade dedicated to AmFiber paper-based barrier lines went live in December 2024 (EUR 40 million, USD 45.2 million) and increases dry-food capacity by 80 million m² per year. Mondi followed in January 2025 by finishing a EUR 50 million (USD 56.5 million) coating line at Steinfeld that produces fully recyclable pet-food wrap, adding 30,000 tons of annual output. The Smurfit WestRock merger, which closed in September 2024, pooled more than 500 plants worldwide and around 35 German sites, giving the group an unmatched corrugated reach.

Strategic moves cluster around vertical recycling integration and mono-material innovation. Stora Enso is spending EUR 120 million (USD 135.6 million) on barrier paperboard capacity at Maxau to chase liquid food cartons migrating away from polyethylene terephthalate layers. Additive-manufacturing specialist Söhner is carving out a niche by licensing rapid-tooling know-how to converters without internal 3D printers, shortening development cycles for seasonal SKUs. Digital printing ecosystems anchored by Heidelberger Druckmaschinen and Koenig and Bauer enable converters to offer personalized runs economically, a key differentiator as e-commerce brands test micro-targeted packaging concepts.

Cybersecurity has emerged as a board-level topic; the Federal Office for Information Security issued an Industry 4.0 guidance document in 2024 urging converters to harden programmable-logic-controller gateways and adopt blockchain traceability. Firms that can certify secure-by-design production lines are beginning to advertise this capability to pharmaceutical clients that require supply-chain assurance.

Germany Packaging Industry Leaders

Amcor PLC

Mondi PLC

Smurfit Westrock PLC

Ball Corporation

SIG Combibloc Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Mondi plc reported full-year 2024 revenue of EUR 7.97 billion (USD 8.49 billion). The company highlighted its German operations as a key contributor to its EUR 350 million sustainable solutions investment program, completed between 2021 and 2025.

- December 2025: Germany's Federal Ministry for the Environment expanded the deposit return system to include milk and juice cartons, previously exempt from the EUR 0.25 (USD 0.28)deposit mandate.

- November 2025: Stora Enso Oyj completed a EUR 120 million (USD 134 million) expansion at its Maxau Mill in Germany, increasing specialty paperboard capacity for food-contact applications by 50,000 tons annually.

- October 2025: Ball Corporation announced plans to optimize its European beverage can manufacturing footprint to serve the region's 47% growth in aluminum can consumption over the previous five years.

- September 2025: DS Smith plc reported that its German corrugated packaging operations achieved 100% renewable electricity usage across all facilities, aligning with the company's commitment to net-zero Scope 1 and 2 emissions by 2030.

Germany Packaging Market Report Scope

The packaging industry in Germany refers to the manufacturing and distribution of packaging materials and containers used to preserve, store, transport, and advertise a wide range of products, such as food, beverages, pharmaceuticals, electronics, and more. Packaging is an important component of the global supply chain because it ensures that items are transported and stored safely while retaining their quality and freshness.

The Germany Packaging Market Report is Segmented by Material Type (Paper and Paperboard, Plastic, Metal, and Container Glass), Product Type (Paper and Paperboard Products, Plastic Products, Metal Products, and Container Glass Products), Packaging Format (Rigid and Flexible), End-User (Food, Beverage, Pharmaceutical and Medical, Personal Care and Cosmetics, Industrial and Chemical, Agriculture, and Automotive), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Paper and Paperboard | |

| Plastic | Polyethylene Polypropylene (PP) |

| High-density Polyethylene (HDPE) and Low-density Polyethylene (LDPE) | |

| Polyethylene Terephthalate (PET) | |

| Polyvinyl Chloride (PVC) | |

| Polystyrene (PS) | |

| Other Plastics | |

| Metal | |

| Container Glass |

By Product Type

| Paper and Paperboard Product Type | Folding Carton and Rigid Boxes | |

| Corrugated Boxes and Containers | ||

| Single-use Paper Products | ||

| Other Paper and Paperboard Product Types | ||

| Plastic Product Type | Rigid Plastics | Bottles and Jars |

| Caps and Closures | ||

| Bulk-Grade Products | ||

| Other Rigid Plastics Product Types | ||

| Flexible Plastics | Pouches | |

| Bags | ||

| Films and Wraps | ||

| Other Flexible Plastics Product Types | ||

| Metal Product Type | Cans | |

| Caps and Closures | ||

| Aerosol Containers | ||

| Other Metal Product Types | ||

| Container Glass Product Type | Bottles | |

| Jars | ||

By Packaging Format

| Rigid Packaging Format |

| Flexible Packaging Format |

By End-user

| Food |

| Beverage |

| Pharmaceutical and Medical |

| Personal Care and Cosmetics |

| Industrial and Chemical |

| Agriculture |

| Automotive |

| Other End-users |

| By Material Type | Paper and Paperboard | ||

| Plastic | Polyethylene Polypropylene (PP) | ||

| High-density Polyethylene (HDPE) and Low-density Polyethylene (LDPE) | |||

| Polyethylene Terephthalate (PET) | |||

| Polyvinyl Chloride (PVC) | |||

| Polystyrene (PS) | |||

| Other Plastics | |||

| Metal | |||

| Container Glass | |||

| By Product Type | Paper and Paperboard Product Type | Folding Carton and Rigid Boxes | |

| Corrugated Boxes and Containers | |||

| Single-use Paper Products | |||

| Other Paper and Paperboard Product Types | |||

| Plastic Product Type | Rigid Plastics | Bottles and Jars | |

| Caps and Closures | |||

| Bulk-Grade Products | |||

| Other Rigid Plastics Product Types | |||

| Flexible Plastics | Pouches | ||

| Bags | |||

| Films and Wraps | |||

| Other Flexible Plastics Product Types | |||

| Metal Product Type | Cans | ||

| Caps and Closures | |||

| Aerosol Containers | |||

| Other Metal Product Types | |||

| Container Glass Product Type | Bottles | ||

| Jars | |||

| By Packaging Format | Rigid Packaging Format | ||

| Flexible Packaging Format | |||

| By End-user | Food | ||

| Beverage | |||

| Pharmaceutical and Medical | |||

| Personal Care and Cosmetics | |||

| Industrial and Chemical | |||

| Agriculture | |||

| Automotive | |||

| Other End-users | |||

Key Questions Answered in the Report

How large is the Germany packaging market in 2026?

It stands at USD 39.22 billion and is projected to reach USD 48.73 billion by 2031.

What is the expected CAGR for packaging demand in Germany from 2026-2031?

The market is set to expand at a 4.44% compound annual growth rate.

Which material segment is growing the fastest?

Biodegradable plastics lead, advancing at a 4.83% CAGR on rising regulatory pressure for compostable formats.

Why are pouches gaining share over rigid formats?

Stand-up pouches cut material use by up to 70% and support lower freight emissions, aligning with sustainability goals.

Which end-user vertical will grow quickest through 2031?

Pharmaceutical and medical applications, supported by biologics cold-chain expansion and stringent serialization rules.

How does Germany’s deposit return system influence packaging design?

With a 98% container return rate, the system incentivizes mono-material, deposit-compatible formats that optimize automated sorting.

Page last updated on: