Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

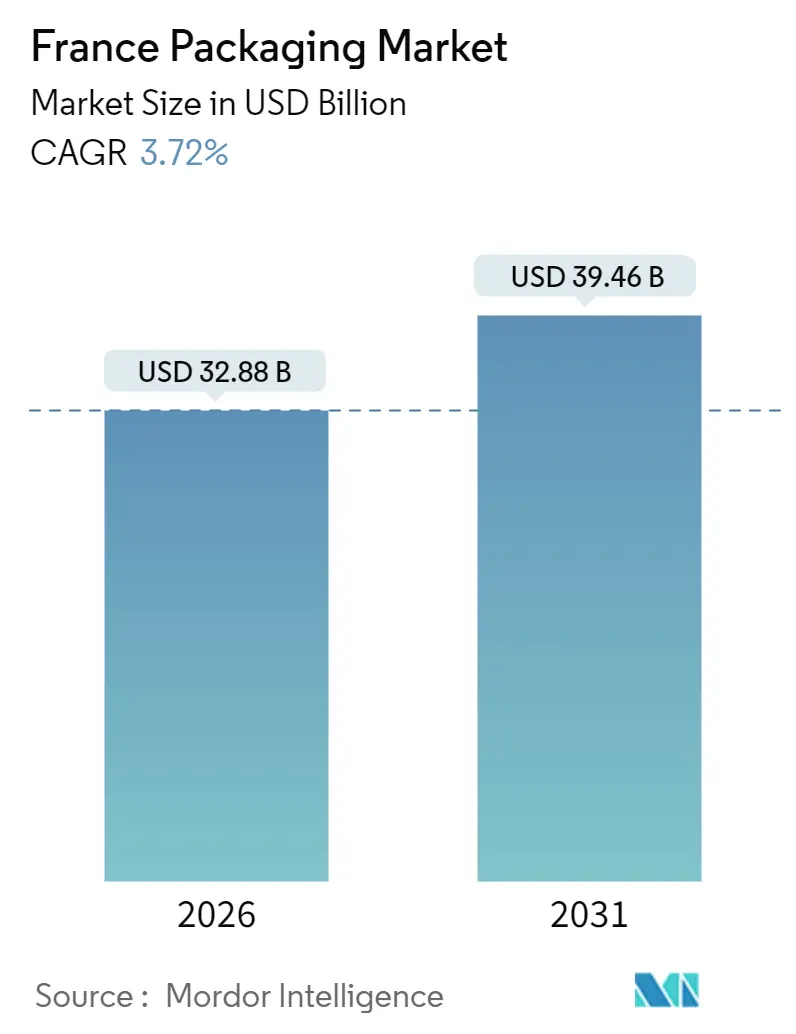

| Market Size (2026) | USD 32.88 Billion |

| Market Size (2031) | USD 39.46 Billion |

| Growth Rate (2026 - 2031) | 3.72% CAGR |

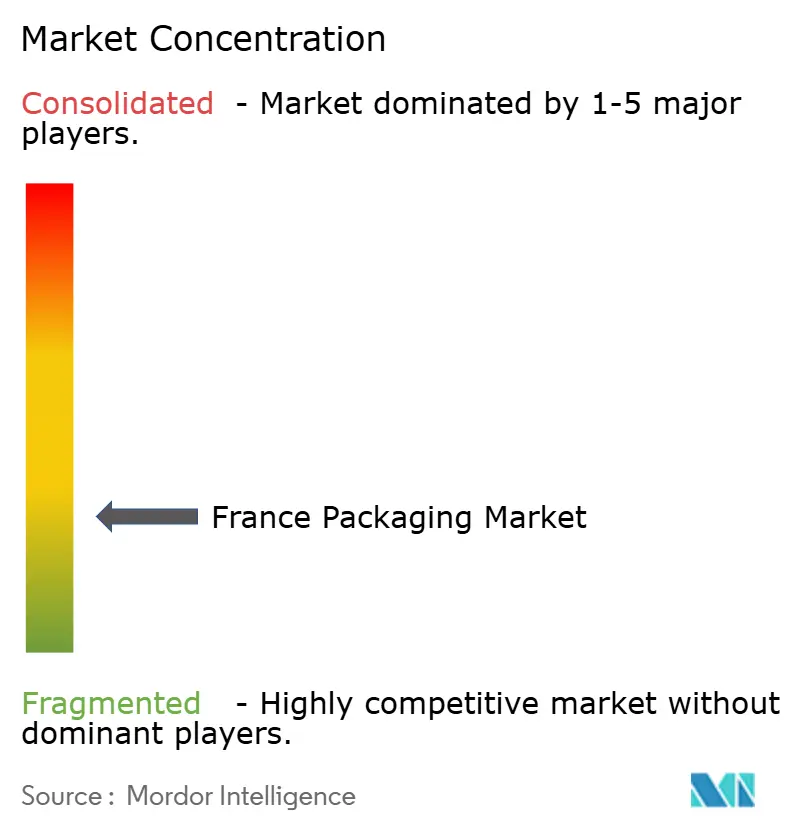

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Packaging Market Analysis by Mordor Intelligence

The France packaging market size is USD 32.88 billion in 2026 and it is projected to reach USD 39.46 billion by 2031, reflecting a 3.72% CAGR during the forecast period. This growth trajectory emerges despite higher Extended Producer Responsibility (EPR) fees, the single-use plastic curbs under the AGEC law, and the European Union Packaging and Packaging Waste Regulation (PPWR) that took effect in February 2025. Demand is anchored by France’s EUR 176.7 billion (USD 188.5 billion) food and beverage production base, strong e-commerce parcel volumes that surpassed 1 billion units in 2025, and steady brand investment in circular solutions such as Carrefour’s Loop refill network. At the same time, recycled polyethylene terephthalate (rPET) prices converged with virgin resin quotations in 2024, squeezing recycling economics and compelling converters to review compliance strategies. Corrugated-box manufacturers also face kraft-liner and energy prices that remain above pre-2021 norms, while talent shortages in packaging engineering slow innovation pipelines. Yet, continued government funding through ADEME’s Green Fund and France 2030 is catalyzing bio-based material scale-up and digital watermarking pilots for advanced sortation.

Key Report Takeaways

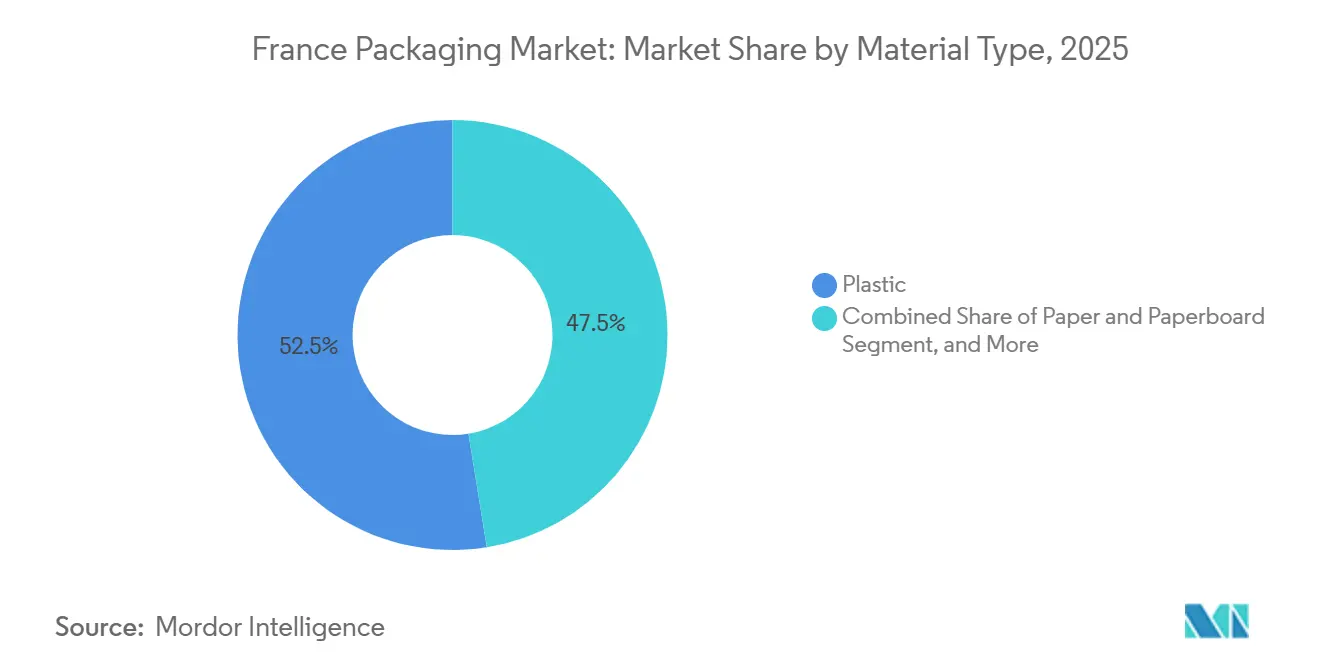

- By material type, plastic held 52.54% of the France packaging market share in 2025, while paper and paperboard are forecast to post the fastest 4.32% CAGR through 2031.

- By packaging format, flexible solutions led with 56.86% of the France packaging market size in 2025 and are projected to expand at a 4.75% CAGR to 2031.

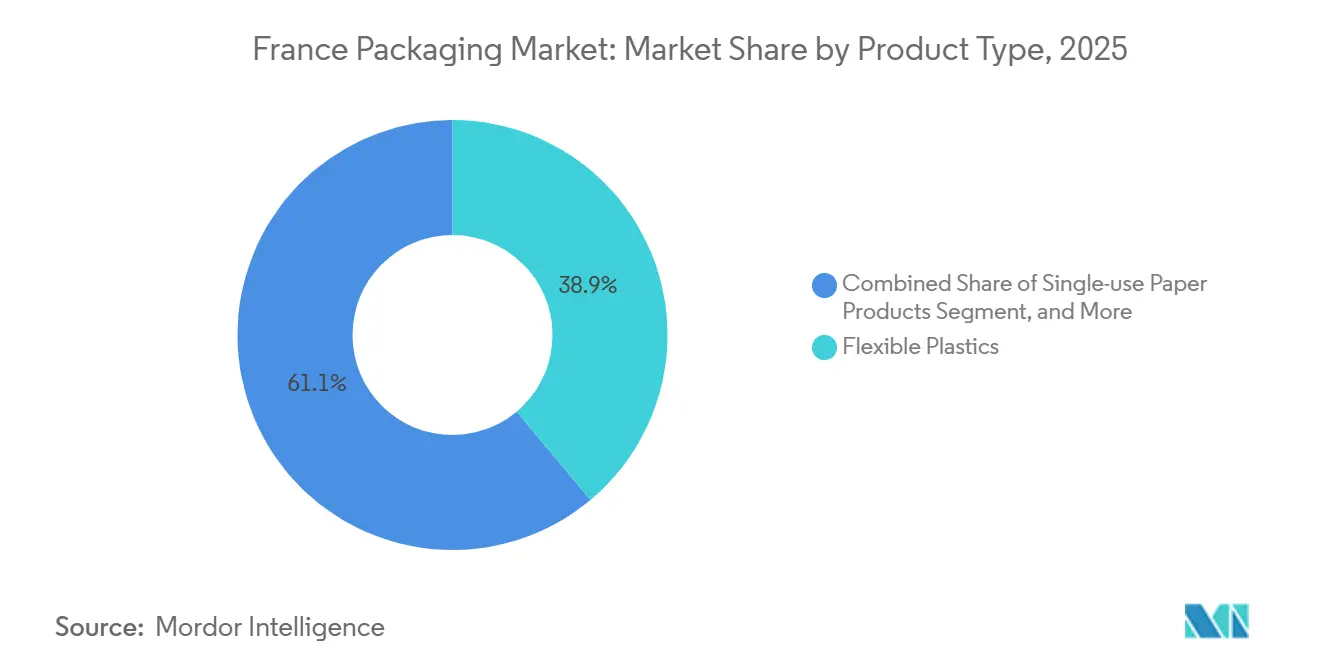

- By product type, flexible plastics captured 38.92% of the France packaging market share in 2025; single-use paper items are on track for the highest 5.28% CAGR through 2031.

- By end user, the food segment dominated with 28.81% of 2025 revenue, whereas personal care and cosmetics are anticipated to register the quickest 5.18% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Sustainable and Recyclable Packaging | +0.9% | National, led by Île-de-France and Auvergne-Rhône-Alpes | Medium term (2-4 years) |

| Growth of E-commerce and Parcel Logistics | +0.7% | Urban centers including Paris, Lyon, Marseille | Short term (≤ 2 years) |

| Robust Food and Beverage Production Base | +0.5% | Brittany, Pays de la Loire, Nouvelle-Aquitaine | Long term (≥ 4 years) |

| Expansion of Refill and Bulk Retail Stations | +0.4% | Paris, Lyon, Bordeaux metropolitan areas | Medium term (2-4 years) |

| Government-Led Funding for Smart Packaging R&D | +0.3% | Île-de-France, Grand Est pilot zones | Medium term (2-4 years) |

| Digital Watermarking Roll-out for Advanced Recycling | +0.3% | Citeo-affiliated material recovery facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand For Sustainable And Recyclable Packaging

Brand owners across dairy, personal care, and beverage categories are prioritizing recycled content and bio-based polymers to avoid surcharges on non-recyclable formats. Carrefour’s Loop network, active in 345 stores, targets removal of 15,000 tonnes of virgin plastic by 2030, pushing converters to design containers that tolerate 20-50 refill cycles without barrier loss.[1]Carrefour Group, “Loop Reusable Packaging System Expansion Announcement,” carrefour.com Polylactic acid capacity is projected to help lift global bioplastics output from 2.47 million tonnes in 2024 to 5.73 million tonnes in 2029, with 45% earmarked for packaging.[2]European Bioplastics, “Bioplastics Market Data 2024,” european-bioplastics.org Cost premiums and modest heat resistance confine polylactic acid to cold-fill and ambient goods, so hot-fill lines still rely on polyethylene terephthalate and polypropylene. EU recycled-content mandates tighten each review period, forcing even small converters to switch to mono-material structures. Early supply deals for bio-based resin therefore deliver strategic security in the France packaging market.

Growth of E-Commerce And Parcel Logistics

E-commerce accounted for 13% of French retail sales in 2025, generating more than 1 billion parcels that require corrugated outers, void fill, and tamper-evident tape. Each shipment endures extra handling, so packaging intensity per transaction exceeds in-store requirements by up to 60%. Kraft-liner mills still pay EUR 150-180 per megawatt-hour for power, about double the pre-2021 norm, lifting box costs. Integrated producers such as Smurfit WestRock leverage captive recycled-fiber loops to buffer volatility. Parcel carriers now specify lighter boxes, prompting converters to adopt micro-flute and high-performance adhesives that retain stacking strength at lower basis weight.

Robust Food And Beverage Production Base

France’s food and beverage sector generated EUR 176.7 billion (USD 188.5 billion) in 2025, anchoring steady demand for glass, metal, flexible, and rigid plastic formats. Wine and spirits bottlers have trimmed glass weight from 500 grams to 350 grams per bottle to cut freight emissions, requiring furnace adjustments to curb breakage. Dairy processors are switching to high-barrier polyethylene terephthalate for shelf-stable milk, displacing opaque high-density polyethylene. Aluminum can makers refine alloys and end-designs to reduce metal consumption while retaining carbonation safety margins. Retailer consolidation keeps price pressure high, so converters chase automation and material savings to protect margins.

Government-Led Funding For Smart Packaging R&D

ADEME’s Green Fund and France 2030 program awarded EUR 1.49 million in June 2024 to the ANR AgriBioPack project, supporting bio-based multilayer films aimed at matching the oxygen-barrier of ethylene vinyl alcohol copolymers. Horizon Europe calls in 2025 added grants for time-temperature indicators, freshness sensors, and digital product passports that trace packs from plant to shelf. Public funding reduces pilot risk, allowing converters to trial active labels and smart inks without full balance-sheet exposure. Pharmaceutical firms absorb the early cost premium, paving a path to wider food adoption as unit economics improve. These programs also stipulate open-data publication, accelerating cross-industry learning and shortening the innovation cycle in the France packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Single-Use Plastic Bans and EPR Fees | -0.6% | Île-de-France, Provence-Alpes-Côte d’Azur | Short term (≤ 2 years) |

| Volatile Raw-Material and Energy Prices | -0.5% | National, acute in glass and aluminum | Short term (≤ 2 years) |

| Recycling Feedstock Bottlenecks (rPET, rHDPE) | -0.3% | Hauts-de-France, Grand Est | Medium term (2-4 years) |

| Packaging-Engineering Talent Shortage | -0.2% | Île-de-France, Auvergne-Rhône-Alpes innovation hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Single-Use Plastic Bans And EPR Fees

France’s AGEC law prohibits polystyrene trays, single-use cutlery, and colored polyethylene terephthalate bottles, while the EU Packaging and Packaging Waste Regulation enforces minimum recycled-content thresholds and harmonized EPR fees. Eco-modulation penalties add up to 30% on non-recyclable formats, shrinking margins for converters that serve fresh produce and snack brands. Verallia saw Q3 2024 revenue fall 6.8% organically as beverage customers lightweighted bottles or shifted to aluminum cans to avoid glass surcharges. SMEs without R&D budgets struggle to reformulate adhesives and coatings quickly, fueling consolidation. Compliance spending crowds out growth capital, delaying new-line investments across the France packaging market.

Volatile Raw-Material And Energy Prices

rPET clear flakes traded at EUR 800-900 per tonne in 2024, overlapping virgin polyethylene terephthalate at EUR 900-1,000, erasing the cost edge once enjoyed by recycled feedstock. Food-grade rPET remains more expensive, fetching EUR 1,100-1,200, yet brand owners resist full price pass-through. Electricity averaged EUR 150-180 per megawatt-hour in 2024, doubling pre-2021 levels and squeezing energy-intensive glass furnaces and aluminum smelters. Crown Holdings reported lower European can volumes and unfavorable hedges, illustrating how input swings undermine profitability. Hedging and operational efficiency become defensive rather than offensive levers, slowing innovation spending in the France packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Paper and Paperboard Gain Momentum While Plastics Lead

Plastic maintained a 52.54% share of the France packaging market in 2025, owing to versatile polyethylene, polypropylene, and PET containers across dairy, sauces, and personal-care SKUs. Paper and paperboard, however, are set to outpace all materials with a 4.32% CAGR through 2031 as e-commerce corrugated boxes, folding cartons, and molded-pulp trays unlock eco-modulation discounts. Container glass remains entrenched in the wine and premium beverage markets, but the lightweighting of bottles reduces tonnage demand. Metal cans continue to serve hermetic or retort categories, offering infinite recyclability messaging.

Cost visibility in kraft liner production remains challenging due to fiber scarcity and elevated energy tariffs; however, integrated mill-converter players can offset input swings through captive recyclate loops. PET dominates beverage packaging due to its clarity and ready food-contact approvals, and its mono-material thermoforms now qualify for higher EPR discounts. High-density polyethylene and low-density polyethylene retain a significant share of the detergent market and are used to produce films, while polypropylene excels in closures and microwaveable containers. In contrast, PVC and polystyrene experience demand declines under AGEC restrictions and risks to consumer perception.

By Packaging Format: Flexible Solutions Extend Leadership

Flexible formats captured 56.86% of the France packaging market in 2025 and are projected to grow at a 4.75% CAGR through 2031, driven by stand-up pouches, multi-layer films, and e-commerce mailers that achieve up to 50% material savings compared to their rigid counterparts. Rigid solutions, although heavier, remain indispensable for carbonated beverages, pharmaceuticals, and premium cosmetics that need drop resistance and shelf impact. Lightweighting in flexible substrates now leverages high-barrier polyethylene or polypropylene blends that pass new recyclability tests, enabling converters to avoid EPR penalties.

Digital watermarking trials achieved 88-94% detection accuracy, paving the way for flexible mono-material sortation at scale. Rigid bottles are increasingly paired with refill pouches in Carrefour’s Loop, reducing net virgin plastic use by up to 70%. E-commerce brands demand bubble mailers and air pillows that trim dimensional weight, which favors converters with in-line extrusion and pouch-forming capabilities. While rigid glass and metal keep a share in flavor-critical or regulatory niches, the relative cost advantage of flexible laminates secures their expansion.

By Product Type: Flexible Plastics Retain Dominance as Single-Use Paper Accelerates

Flexible plastics held 38.92% of product demand in 2025 across snack pouches, produce films, and pet-food bags. France packaging market size for single-use paper plates, bowls, and wraps is forecast to post a 5.28% CAGR, benefiting from quick-service restaurant transitions away from polystyrene and foam. Rigid plastics, such as PET bottles and PP jars, provide clarity, tamper-evidence, and compatibility with hot-fill lines; yet, mono-material mandates push converters toward simplified structures.

Regulation-driven demand for paper straws and molded-fiber clamshells accelerates capital spending in specialized pulp-molding lines. Converters supplying flexible pouches are redesigning laminates to remove aluminum layers and increase polyethylene content, thereby enhancing recyclability without compromising the oxygen barrier. Metal cans and closures maintain niches where shelf life and hermetic sealing are paramount. Container glass maintains prestige branding but faces freight and EPR cost headwinds despite successful 30% weight-reduction programs.

By End User: Personal Care and Cosmetics Gain Pace Over Food

Food applications represented 28.81% of 2025 demand, driven by dairy, bakery, and fresh-produce packaging. However, personal care and cosmetics are set for the fastest growth, with a 5.18% CAGR through 2031. Premium brands now deploy refillable glass jars, aluminum tubes, and rPET bottles with tactile finishes that justify higher shelf prices and meet brand sustainability claims. Beverage brands focus on lightweight glass and aluminum innovations to reduce carbon footprints, while pharmaceuticals rely on blister packs and child-resistant closures governed by stringent traceability rules.

Advanced digital watermarks, rolled out across shampoo and lotion bottles, enable Citeo-affiliated facilities to sort by polymer and brand, facilitating higher-purity recycling and attracting lower EPR fees. Industrial and chemical users emphasize durability and hazard compliance, often selecting drums and intermediate bulk containers that resist corrosive loads. Agriculture remains a smaller but stable segment, consuming stretch-film for silage and woven sacks for feed.

Geography Analysis

France packaging market dynamics vary across regions. Île-de-France and Auvergne-Rhône-Alpes host research clusters funded by ADEME and France 2030, including the EUR 1.49 million AgriBioPack bio-based film program launched in June 2024. Brittany, Pays de la Loire, and Nouvelle-Aquitaine provide the bulk of food and beverage output, underpinning steady glass, flexible, and rigid-plastic demand. Paris, Lyon, and Marseille account for the highest parcel density, thereby increasing the consumption of corrugated and protective mailers.

Hauts-de-France and Grand Est report rPET feedstock shortages that hinder the achievement of the PPWR’s 50% recycling target for 2025, keeping France’s plastic recycling rate close to 25% in 2022. Provence-Alpes-Côte d’Azur imposes strict single-use bans, incentivizing the use of molded-fiber trays in tourism hotspots. Nationwide energy prices, although lower than 2022 peaks, remain double pre-crisis averages and weigh on energy-intensive glass and aluminum producers.

Digital watermarking pilots in Suez-operated and Wellman Verdun facilities proved scalable but will require EUR 50-100 million to retrofit France’s 100-plus material recovery facilities. Collectively, regional policy diversity and infrastructure gaps position France as a live laboratory for next-generation packaging solutions that balance cost, performance, and environmental impact.

Competitive Landscape

The France packaging market exhibits fragmentation. The July 2024 Smurfit Kappa-WestRock merger created Smurfit WestRock, a USD 34 billion revenue entity with a 40-country reach, enabling mill optimization and fiber procurement synergies that shelter margins from kraft-liner volatility.[3]Smurfit Kappa, “Smurfit WestRock Merger Completion Announcement,” smurfitkappa.com Amcor reported FY 2024 sales of USD 12.4 billion, a 5% decrease, yet achieved earnings growth by trimming costs and reinforcing its commitment to 30% recycled content. Verallia’s Q3 2024 revenue slipped 6.8% organically as clients lightweighted bottles or shifted to cans to avoid glass EPR fees, pressuring furnace utilization rates.

Regional specialists such as Groupe Guillin, Albea, and Sleever International occupy niches in thermoformed trays, cosmetics tubes, and shrink sleeves, respectively. Carrefour’s Loop initiative compels converters to supply durable, reusable containers, a capability that benefits injection molders with expertise in impact modifiers and scuff-resistant labeling.

Chemical recycling start-ups like Carbios and Loop Industries are piloting enzymatic depolymerization plants, positioning themselves as future feedstock providers once rPET economics tighten further. Talent shortages in barrier coatings, adhesive science, and life-cycle assessment add intangible entry barriers, solidifying incumbent advantage across the France packaging market.

France Packaging Industry Leaders

Tetra Pak International SA

Smurfit WestRock

Amcor plc

International Paper Company

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Carrefour expanded Loop reusable-packaging to 345 stores, covering 370 products and pledging to cut 15,000 tonnes of virgin plastic by 2030.

- May 2025: The French government confirmed the roll-out of a nationwide deposit-return system for beverage containers, setting the framework for reverse-logistics infrastructure and unified labeling requirements.

- April 2025: Carrefour reaffirmed its target to reduce virgin plastic by 15,000 tonnes across private-label and national brands.

- February 2025: EU Packaging and Packaging Waste Regulation entered force, tightening recycled-content mandates and EPR harmonization

France Packaging Market Report Scope

Packaging is described as providing a protective and informative covering for the product that protects it during its handling, storage, and movement, and also usefully informs consumers about the contents of the package. The study tracks the demand for the packaging market through the revenue derived from plastic, glass, and metal.

The France Packaging Market Report is Segmented by Material Type (Paper and Paperboard, Plastic, Metal, and Container Glass), Packaging Format (Flexible, and Rigid), Product Type (Paper and Paperboard Product Type, Plastic Product Type, Metal Product Type, and Container Glass Product Type), End-user (Food, Beverage, Pharmaceuticals and Medical, Personal Care and Cosmetics, Industrial and Chemical, Agriculture, Automotive, and Other End-users). The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Paper and Paperboard | |

| Plastic | Polyethylene Polypropylene (PP) |

| High-density Polyethylene (HDPE) and Low-density Polyethylene (LDPE) | |

| Polyethylene Terephthalate (PET) | |

| Polyvinyl Chloride (PVC) | |

| Polystyrene (PS) | |

| Other Plastics | |

| Metal | |

| Container Glass |

By Product Type

| Paper and Paperboard Product Type | Folding Carton and Rigid Boxes | |

| Corrugated Boxes and Containers | ||

| Single-use Paper Products | ||

| Other Paper and Paperboard Product Types | ||

| Plastic Product Type | Rigid Plastics | Bottles and Jars |

| Caps and Closures | ||

| Bulk-Grade Products | ||

| Other Rigid Plastics Product Types | ||

| Flexible Plastics | Pouches | |

| Bags | ||

| Films and Wraps | ||

| Other Flexible Plastics Product Types | ||

| Metal Product Type | Cans | |

| Aerosol Containers | ||

| Caps and Closures | ||

| Other Metal Product Types | ||

| Container Glass Product Type | Bottles | |

| Jars | ||

By Packaging Format

| Rigid Packaging Format |

| Flexible Packaging Format |

By End-user

| Food |

| Beverage |

| Pharmaceuticals and Medical |

| Personal Care and Cosmetics |

| Industrial and Chemical |

| Agriculture |

| Automotive |

| Other End-users |

| By Material Type | Paper and Paperboard | ||

| Plastic | Polyethylene Polypropylene (PP) | ||

| High-density Polyethylene (HDPE) and Low-density Polyethylene (LDPE) | |||

| Polyethylene Terephthalate (PET) | |||

| Polyvinyl Chloride (PVC) | |||

| Polystyrene (PS) | |||

| Other Plastics | |||

| Metal | |||

| Container Glass | |||

| By Product Type | Paper and Paperboard Product Type | Folding Carton and Rigid Boxes | |

| Corrugated Boxes and Containers | |||

| Single-use Paper Products | |||

| Other Paper and Paperboard Product Types | |||

| Plastic Product Type | Rigid Plastics | Bottles and Jars | |

| Caps and Closures | |||

| Bulk-Grade Products | |||

| Other Rigid Plastics Product Types | |||

| Flexible Plastics | Pouches | ||

| Bags | |||

| Films and Wraps | |||

| Other Flexible Plastics Product Types | |||

| Metal Product Type | Cans | ||

| Aerosol Containers | |||

| Caps and Closures | |||

| Other Metal Product Types | |||

| Container Glass Product Type | Bottles | ||

| Jars | |||

| By Packaging Format | Rigid Packaging Format | ||

| Flexible Packaging Format | |||

| By End-user | Food | ||

| Beverage | |||

| Pharmaceuticals and Medical | |||

| Personal Care and Cosmetics | |||

| Industrial and Chemical | |||

| Agriculture | |||

| Automotive | |||

| Other End-users | |||

Key Questions Answered in the Report

What is the current size of the France packaging market?

The market is valued at USD 32.88 billion in 2026, with a forecast to reach USD 39.46 billion by 2031.

How fast is sustainable packaging demand growing in France?

Paper and paperboard packaging is expected to post a 4.32% CAGR through 2031 as brands switch from single-use plastics.

Which packaging format is expanding the quickest?

Flexible formats, led by stand-up pouches and e-commerce mailers, are projected to grow at a 4.75% CAGR through 2031.

What regional factors shape packaging demand most in France?

Île-de-France and Auvergne-Rhône-Alpes drive R&D investments, while Brittany and Nouvelle-Aquitaine sustain food-related demand.

How are EPR fees impacting packaging design choices?

Eco-modulation surcharges on non-recyclable or multilayer items are pushing converters toward mono-material structures and refill models.

Which end-user segment is set to outpace others?

Personal care and cosmetics should grow fastest at a 5.18% CAGR as premium brands adopt refillable and rPET solutions.

Page last updated on: