Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

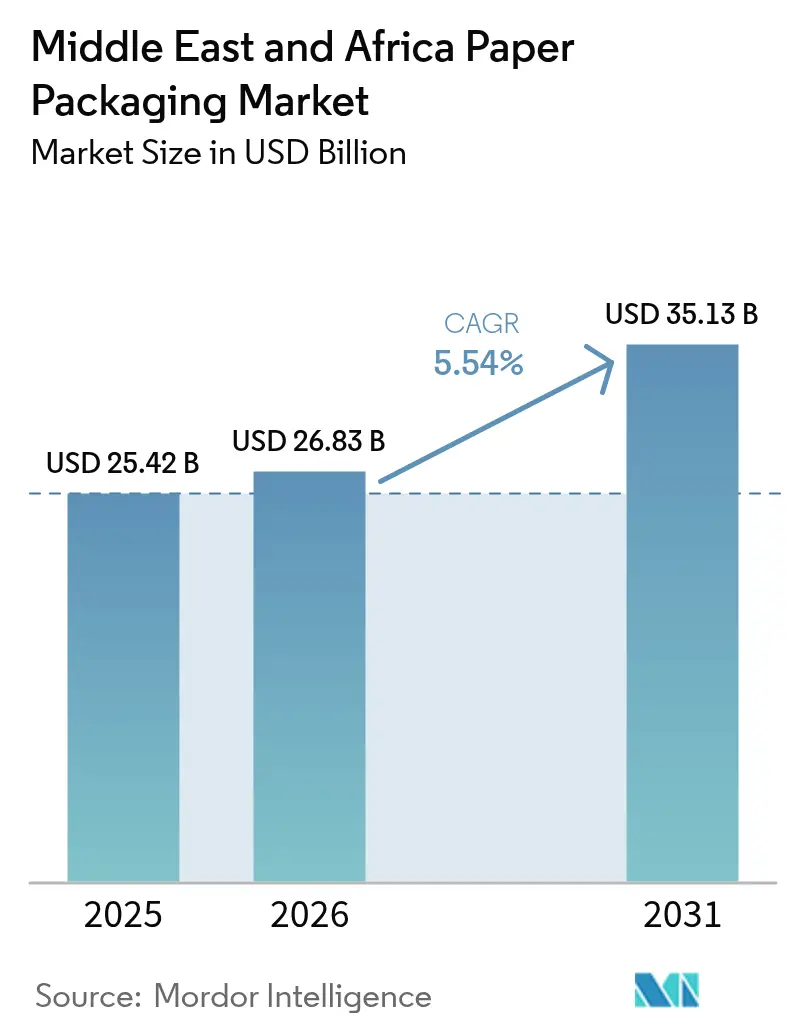

| Base Year Market Size (2025) | USD 25.42 Billion |

| Market Size (2026) | USD 26.83 Billion |

| Market Size (2031) | USD 35.13 Billion |

| Growth Rate (2026 - 2031) | 5.54% CAGR |

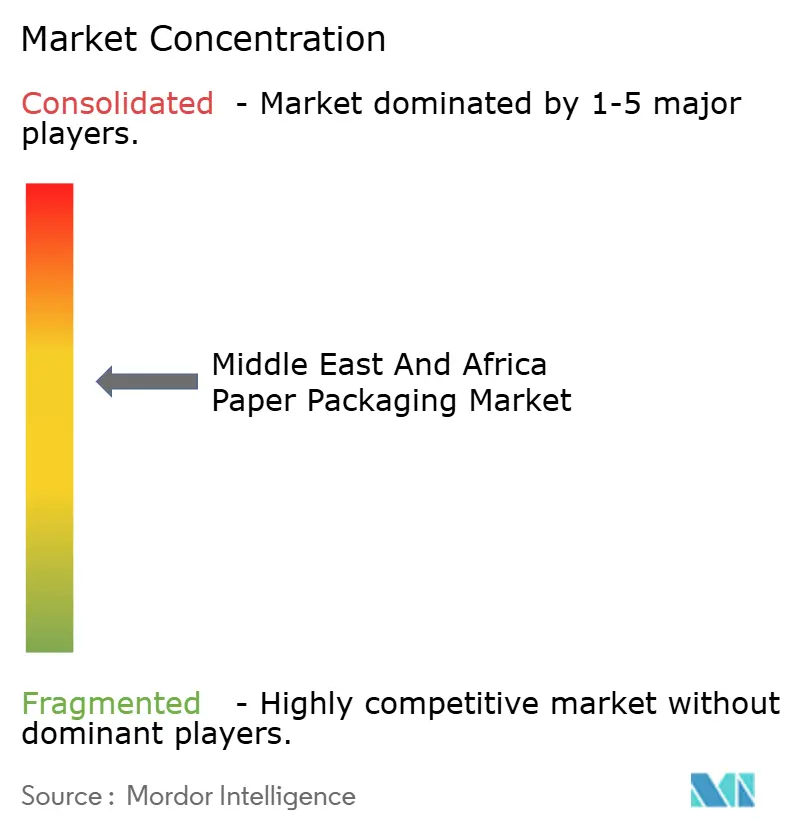

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Paper Packaging Market Analysis by Mordor Intelligence

Middle East and Africa paper packaging market size in 2026 is estimated at USD 26.83 billion, growing from 2025 value of USD 25.42 billion with 2031 projections showing USD 35.13 billion, growing at 5.54% CAGR over 2026-2031. Structural shifts are accelerating as plastic-phase-out mandates coincide with e-commerce parcel volumes that doubled after 2024, prompting brand owners to favor fiber-based formats for regulatory compliance and fulfillment efficiency. Demand is tempered by the volatility of imported recycled-fiber prices and chronic power interruptions in Sub-Saharan hubs, which raise the cost of goods sold, prompting converters to secure long-term pulp contracts, invest in dual-fuel boilers, and digitize asset scheduling. Saudi Arabia remains the revenue anchor, while South Africa leads growth in Extended Producer Responsibility rules that stimulate the use of recycled content. Competitive tension intensifies as global integrated producers leverage vertical supply chains and sustainability credentials, whereas regional converters counter with Industry 4.0 automation and on-site digital presses. These factors collectively steer the Middle East and Africa paper packaging market toward optimized capacity deployment, innovation in water-barrier coatings, and renewed focus on feedstock security.

Key Report Takeaways

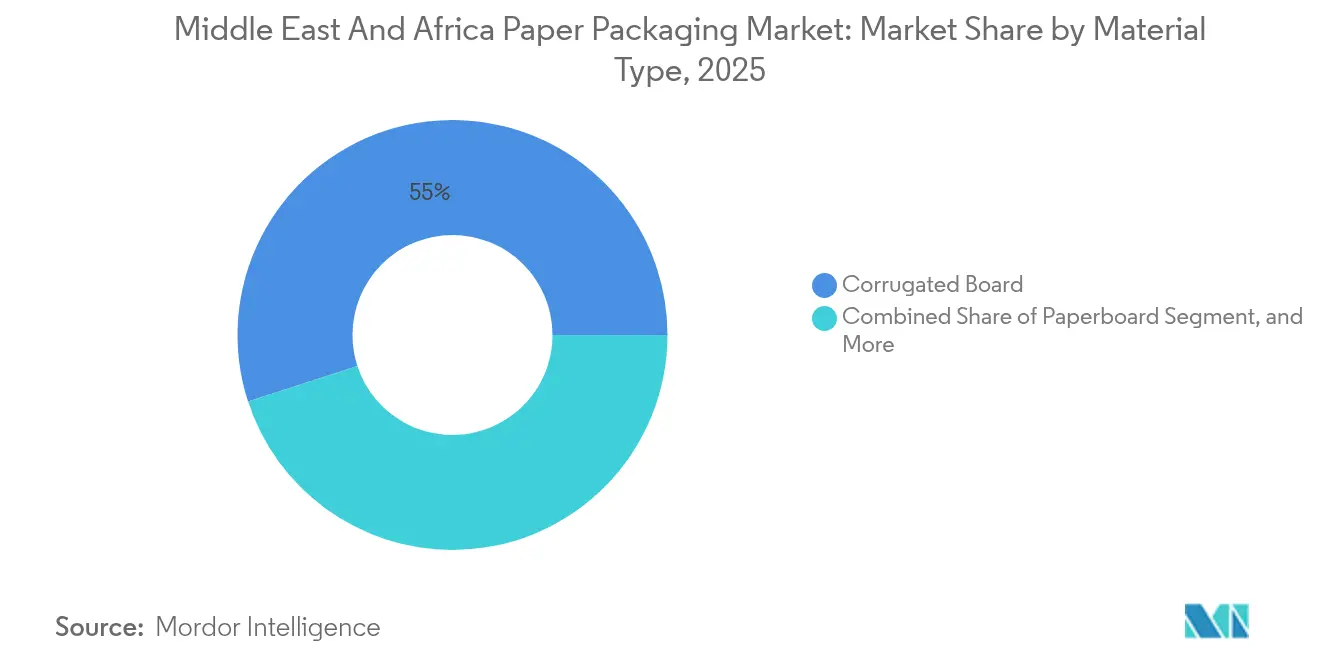

- By material type, corrugated board accounted for 55.01% of the Middle East and Africa paper packaging market share in 2025; paperboard is forecast to expand at a 7.32% CAGR through 2031.

- By product type, rigid paper packaging captured a 65.85% of the Middle East and Africa paper packaging market share in 2025, while flexible paper packaging is expected to advance at a 6.63% CAGR through 2031.

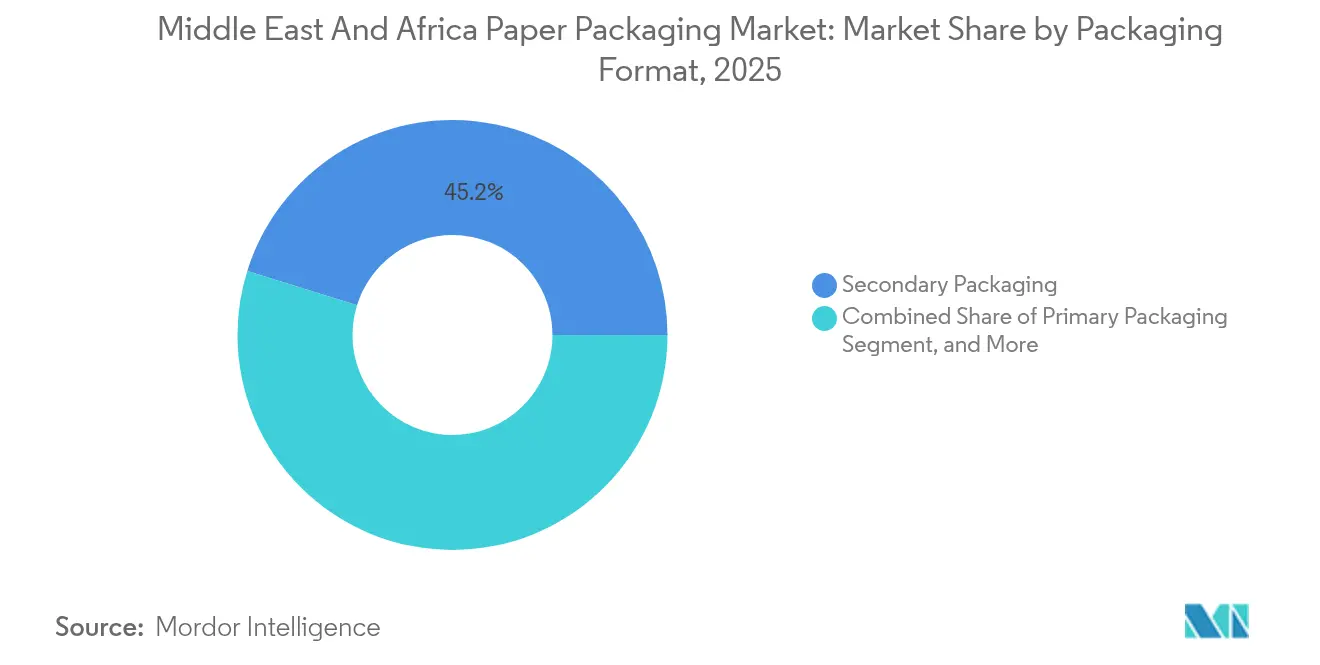

- By packaging format, secondary packaging accounted for 45.18% of the Middle East and Africa paper packaging market share in 2025, whereas primary packaging is projected to grow at a 7.12% CAGR through 2031.

- By end-use industry, food led with a 33.05% share of the Middle East and Africa paper packaging market in 2025; personal care and cosmetics aree forecast to expand at an 8.02% CAGR between 2025 and 2031.

- By geography, Saudi Arabia commanded a 35.05% of the Middle East and Africa paper packaging market share in 2025; South Africa is expected to record an 7.86% CAGR from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating E-Commerce Fulfillment Volumes | +1.2% | Saudi Arabia, UAE, South Africa, Kenya | Short term (≤ 2 years) |

| Government Plastic Phase-Out Regulations | +1.5% | Nigeria, Kenya, UAE, Ethiopia, South Africa | Medium term (2-4 years) |

| Rising Fresh Produce Exports Requiring Corrugated Solutions | +0.8% | South Africa, Kenya, Morocco, Egypt | Medium term (2-4 years) |

| Rapid Expansion of Quick Service Restaurants | +0.7% | Saudi Arabia, UAE, Egypt, Nigeria | Short term (≤ 2 years) |

| Growing Adoption of Smart Water-Barrier Coated Papers | +0.6% | Saudi Arabia, UAE, South Africa | Long term (≥ 4 years) |

| On-Site Digital Printing on Corrugated for Brand Localization | +0.5% | Saudi Arabia, UAE, South Africa, Kenya | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating E-Commerce Fulfillment Volumes

Mobile-enabled shopping, same-day delivery promises, and digital marketplaces have driven parcel counts sharply higher in major consumer corridors since 2024. Every additional shipped box raises corrugated demand, but rising SKU complexity now favors converters that integrate hybrid digital-flexo print lines capable of on-demand graphics. Order cycles have shortened from weeks to days, compelling plants to adopt AI-based planning tools that squeeze idle time and release working capital. Brand owners are increasingly specifying box formats that eliminate void-fill plastics and utilize lightweight containerboard to meet carrier weight thresholds and Extended Producer Responsibility fees. Converters can maintain consistent flute profiles while running variable graphics and capturing above-market margins by reducing clients’ inventory carry costs.

Government Plastic Phase-Out Regulations

Nigeria’s 2024 single-use ban, Kenya’s expanded restrictions, the UAE’s degradability rules, and Ethiopia’s Addis Ababa mandates have triggered a measurable shift to fiber solutions across food service and retail. Compliance accelerates the demand for dispersion-coated paper that withstands grease and moisture while remaining recyclable in existing mills. Enforcement inconsistencies create arbitrage opportunities: converters with ISO 14001 certifications secure public-sector tenders, whereas their non-certified peers face ad-hoc audits and contract penalties. Equipment upgrades to curtain-coating lines and inline barrier inspection systems are required investments; however, converters recover their costs through premium prices on certified mono-material formats. Regional chemical suppliers gain a pipeline of bio-based coating volumes that displace polyethylene laminations.[1]United Nations Environment Programme, “How African Countries Are Taking Action to Beat Plastic Pollution,” unep.org

Rising Fresh Produce Exports Requiring Corrugated Solutions

Record citrus and avocado harvests in Southern Africa demand ventilated, moisture-controlled cartons that survive chilled reefer voyages to Europe. Kenyan floriculture exporters prioritize low grammage yet high stacking strength to cut airfreight charges while meeting shelf-life specs. Corrugated converters co-locate warehouses in farm clusters to synchronize with harvest windows and run just-in-time production, minimizing inventory spoilage risk. Molded-pulp corner protectors are gaining traction to curb transit damage, creating incremental fiber demand and new revenue streams. As United Kingdom supermarkets toughen bruising tolerance limits, carton stiffness testing and ethylene-absorbing pads become differentiators for suppliers.[2]MDPI Editors, “Sustainability and Life Cycle Assessment of Corrugated Packaging for Fresh Produce,” mdpi.com

Rapid Expansion of Quick Service Restaurants

More than 200 new QSR outlets opened across Saudi Arabia, the UAE, Egypt, and Nigeria in 2024, each requiring grease-resistant wraps, folding cartons, and beverage carriers. The shift to delivery-first formats means that every meal occasion comes with incremental packaging, with lightweight cartons replacing plastic clamshells. Short-run seasonal artwork drives the adoption of digital presses that can swap graphics within minutes, feeding localized marketing campaigns. Grease-proof dispersion coatings now command a 15% price premium while reducing composting contamination, thereby aiding restaurant ESG targets. Suppliers able to preload inventory data into client ERP systems win multi-country master service agreements, signaling deeper integration in the Middle East and Africa paper packaging market.[3]Huhtamäki Oyj, “Huhtamaki Annual Report 2023,” huhtamaki.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Frequent Cost Volatility in Recycled Fiber Import Feedstock | -0.9% | Nigeria, Kenya, Egypt | Short term (≤ 2 years) |

| Chronic Power Supply Instability in Sub-Saharan Manufacturing Hubs | -0.7% | Nigeria, Kenya, Tanzania, Ghana | Medium term (2-4 years) |

| Limited Regional Forestry Resources Increasing Virgin Pulp Dependence | -0.6% | Saudi Arabia, Egypt, Ethiopia | Long term (≥ 4 years) |

| Maritime Logistics Disruptions and Currency Fluctuations Extending Lead Times | -0.5% | GCC, East Africa, Egypt | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Frequent Cost Volatility in Recycled Fiber Import Feedstock

European export restrictions and Asian buying spikes drove recycled fiber prices to EUR 1,380 per metric ton in April 2024, inflating raw-material costs for Middle East and African mills that import more than 70% of their feedstock. Gross margin compression of 200-300 basis points followed as converters absorbed surges to preserve long-term contracts. Buyers began requesting quarterly price-adjustment clauses, but smaller converters lacked the leverage to counter these demands and risked losing orders. Vertically integrated players with captive OCC collection offset volatility and gained share, widening the cost gap versus spot purchasers. Working-capital pressure forced some independents to temporarily shutter their lines, underscoring the feedstock risk premium inherent in the Middle East and Africa paper packaging market.

Chronic Power Supply Instability in Sub-Saharan Manufacturing Hubs

Grid uptime below 60% in Nigeria, Kenya, and Tanzania compels converters to run diesel gensets that lift energy costs by up to 18%, negating carbon advantages over plastics. Outages disrupt process consistency, elevate scrap, and extend lead times, eroding service-level scores. Capital-intensive solar-battery retrofits, typically USD 500,000-1.5 million per plant, pose funding hurdles for smaller firms. Hybrid systems deliver payback in four years but still require a diesel backup due to cloudy seasons, which locks in dual-fuel complexity. Policy focus on residential electrification leaves industrial users to self-fund resilience, reinforcing market consolidation around well-capitalized operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Corrugated Dominates but Paperboard Surges in Consumer-Facing Cartons

Corrugated board generated 55.01% of 2025 material revenue thanks to sturdy, low-cost secondary and tertiary transit roles across food and industrial supply chains. The Middle East and Africa paper packaging market size for corrugated paper is projected to trail paperboard through 2031, as carton demand in the QSR and personal care sectors outpaces bulk shipping volumes. Paperboard’s 7.32% CAGR reflects lightweight substrates that support high-definition graphics, portion control, and shelf impact, enabling brand segregation in crowded retail aisles. Kraft paper continues to serve bakery wraps, yet faces substitution by coated paperboard, which delivers superior moisture barriers.

Converters installing inline coating and digital print stations on paperboard lines lock in higher margins by catering to premium cosmetic SKUs. MEPCO’s SAR 1.78 billion fifth line will add 450,000 metric tons of recycled containerboard, reinforcing corrugated supply, while molded-pulp niches rise in electronics protection. Integrated mills that optimize furnish recipes between testliner and medium grades can flex their output around e-commerce spikes, thereby buffering the Middle East and Africa paper packaging market against pulp shocks.

By Product Type: Flexible Formats Accelerate on Mono-Material Recyclability

Rigid formats accounted for 65.85% of 2025 revenue, primarily driven by folding cartons and corrugated cases. However, flexible paper pouches, bags, and wraps are expected to post a 6.63% CAGR through 2031, as regulators increasingly clamp down on multilayer plastics. The Middle East and Africa paper packaging market size for flexible grades remains smaller but benefits from bio-dispersion coatings that enable high-moisture foods to shift away from laminated films without sacrificing shelf life. Bakery and confectionery packs are already shifting to paper-based pouches, which reduce system costs, as Extended Producer Responsibility fees penalize plastics.

Huhtamaki’s South African molded-fiber expansion signals demand for rigid trays that displace PET. Meanwhile, converters with gravure-coating towers introduce barrier wraps for frozen foods, adding premium throughput. Integrating digital presses on flexible lines enables suppliers to quickly batch-code promotions and language versions, which is vital in multi-lingual markets. Rigid corrugated will still dominate bulk transit, but flexible formats provide a double-digit margin opportunity where weight reduction, source reduction, and recyclability converge.

By Packaging Format: Primary Packs Rise as SKU Proliferation Shifts Shelf Economics

Secondary packs represented 45.18% of the 2025 format share as corrugated shippers remained the distribution workhorse. Yet primary packs will rise at a 7.12% CAGR as personal-care and ready-meal brands increase the number of variants that require direct branding. The Middle East and Africa paper packaging market share for primary packs grows whenever retailers launch private labels that demand shelf differentiation and portioned formats. Tertiary pallets track overall market growth but face substitution from reusable plastic crate pools in grocery chains.

UCIC, controlling nearly 40% of Saudi corrugated, files for an IPO to fund the diversification of folding cartons, mirroring the market realignment toward consumer-facing packs. Converters with auto-platen die-cutters and gluing lines, capable of micro-flute and micro-perforation, win contracts for shelf-ready cartons. Primary formats with QR codes for authentication also support emerging anti-counterfeit policies in the pharmaceutical industry, increasing print complexity and value capture across the Middle East and Africa paper packaging market.

By End-Use Industry: Personal Care Outpaces Food on Premiumization

Food accounted for 33.05% of 2025 demand, but personal care and cosmetics are projected to post an 8.02% CAGR to 2031, overtaking beverages and matching export-grade produce in absolute growth. Carton designs with foil stamping and tactile varnishes command higher unit prices and lower order volumes, aligning with the economics of digital presses. The Middle East and Africa paper packaging market size expansion in personal care stems from regional influencer brands launching limited SKUs that rotate quarterly.

Tetra Pak’s Egypt recycling joint venture demonstrates closed-loop interest from beverage players; however, competition from PET and aluminum restrains carton share in single-serve drinks. Industrial and electronics brands are increasingly specifying molded pulp and honeycomb inserts to meet corporate plastic reduction targets. Segment diversification highlights the versatility of fiber and entices investors to support new converting capacity in niche formats across the Middle East and Africa paper packaging market.

Geography Analysis

Saudi Arabia contributed 35.05% of the revenue in 2025, driven by Vision 2030 industrial policies that incentivize local containerboard production and import substitution. MEPCO’s forthcoming 450,000 metric-ton line and Arabian Paper Products’ expansion reinforce domestic supply, securing pulp imports via long-term offtakes and hedging currency swings. Industrial clusters around Jeddah offer access to feedstock through MSW collection rates exceeding 45% and port connectivity for intra-GCC exports. The Middle East and Africa paper packaging market benefits from these large-scale investments that anchor regional pricing.

The UAE accounts for 15-18% of regional demand and positions itself as a specialty carton hub serving the personal care and pharmaceutical sectors. Hotpack Global’s SAR 1 billion mega plant, set to be operational in 2025, bolsters its flexible packaging capability and adds 4,500 tons per month of coated paperboard extrusion. Free-zone infrastructure and zero-tariff re-export routes make Dubai an attractive consolidation point for multinational FMCG supply chains shipping into East Africa. Sustainable fiber branding resonates with hotel and airline groups pursuing zero-plastic commitments.

South Africa, forecast at an 7.86% CAGR, leads growth on Extended Producer Responsibility rules requiring recycled-content thresholds. Integrated majors Mondi, Mpact, Huhtamaki, Nampak, and Smurfit Kappa collectively command over 70% of the national output, enabling economies of scale in pulp integration and renewable energy retrofits. The Middle East and Africa paper packaging market size benefits from South Africa’s export-oriented citrus, wine, and forestry products, which utilize efficient rail-port corridors.

Nigeria (8-10% share) shows rapid corrugated uptake as e-commerce scales, but power instability and forex devaluation deter heavy capital expenditure. Kenya (5-7%) capitalizes on horticulture exports and strict plastic bans, with converters installing high-speed digital presses for short-run localized labels. The rest of Africa remains underpenetrated, yet it offers white space for agile entrants able to deploy modular converting lines near seaports and leverage mobile collection technology for OCC feedstock. Multi-country operators that flex production between plants to offset currency shocks and energy costs will capture outsized gains in the Middle East and Africa paper packaging market.

Competitive Landscape

The top 10 suppliers account for an estimated 50-60% of regional revenue, indicating moderate concentration. Mondi, Smurfit WestRock, and International Paper integrate pulp through converting, offering one-stop procurement and sustainability reporting for multinational FMCG accounts. Regional champions Nampak, MEPCO, and UCIC defend turf with proximity advantages and agile line-change scheduling to serve emerging brands. Consolidation pressures mount: Smurfit WestRock targets EUR 400 million in synergies via network rationalization, and MEPCO’s fifth line shifts cost curves in the GCC toward lightweight containerboard.

Technology investments distinguish leaders: inline water-barrier coating, closed-loop wastewater, and predictive maintenance sensor arrays elevate operating margins. Digital printing on corrugated reaches 150 m per minute, letting converters offer variable SKUs without plate inventory, a decisive service edge. New entrants focus on molded pulp and mono-material pouches, segments that incumbents’ legacy assets cannot switch to economically. Sustainability credentials now rank alongside price in bid evaluations, compelling smaller converters to publish LCA data and secure FSC-certified fiber.

Specialty-chemical innovators and press OEMs dilute traditional boundaries, as Siegwerk, Solenis, and EFI partner directly with converters to embed barrier chemistries and workflow software. The Middle East and Africa paper packaging market thus evolves toward a segmented competitive schema: scale-driven corrugated giants on one side, and high-margin niche players on the other, both chasing differentiated ESG value propositions.

Middle East And Africa Paper Packaging Industry Leaders

Amcor Plc

International Paper Company

Mondi Plc

Smurfit WestRock

Tetra Laval International S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Hotpack Global initiated construction of its SAR 1 billion (USD 266 million) sustainable-packaging mega plant in Dubai, designed to expand specialty-carton and flexible-paper output for personal-care and pharmaceutical clients across the UAE and East Africa.

- April 2025: United Carton Industries Company (UCIC) disclosed plans to float 30% of its share capital on the Saudi stock exchange, aiming to raise funds for GCC expansion into folding cartons and containerboard.

- March 2025: Crown Paper Mill’s new tissue machine in the Dammam area of Saudi Arabia is scheduled to commence operations, bringing 70,000 metric tons of added hygienic-paper capacity to the region.

- March 2025: MEPCO broke ground on its SAR 1.78 billion (USD 474.6 million) PM5 recycled-containerboard line at the Jeddah mill, a project that will add 450,000 metric tons of annual capacity when fully commissioned.

Middle East And Africa Paper Packaging Market Report Scope

Paper packaging materials can be easily reused and recycled compared to other materials, such as metals and plastics. It is a versatile and cost-efficient method to protect, preserve, and transport a wide range of products. Attributes, such as lightweight, biodegradability, and recyclability, are the advantages of this packaging that make it an essential component in modern life.

The Middle East and Africa Paper Packaging Report is Segmented by Material Type (Kraft Paper, Paperboard, Corrugated Board, Other Material Types), Product Type (Flexible Paper Packaging, Rigid Paper Packaging), Packaging Format (Primary Packaging, Secondary Packaging, Tertiary Packaging), End-Use Industry (Food, Beverage, Healthcare and Pharmaceuticals, Personal Care and Cosmetics, Industrial and Electronic, Other End-Use Industries), and Geography (Saudi Arabia, United Arab Emirates, Rest of Middle East, South Africa, Nigeria, Kenya, Rest of Africa). Market Forecasts are in Value (USD).

By Material Type

| Kraft Paper |

| Paperboard |

| Corrugated Board |

| Other Material Types |

By Product Type

| Flexible Paper Packaging |

| Rigid Paper Packaging |

By Packaging Format

| Primary Packaging |

| Secondary Packaging |

| Tertiary / Transit Packaging |

By End-Use Industry

| Food |

| Beverage |

| Healthcare and Pharmaceuticals |

| Personal Care and Cosmetics |

| Industrial and Electronic |

| Other End-Use Industries |

By Middle East and Africa

| By Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| By Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Material Type | Kraft Paper | |

| Paperboard | ||

| Corrugated Board | ||

| Other Material Types | ||

| By Product Type | Flexible Paper Packaging | |

| Rigid Paper Packaging | ||

| By Packaging Format | Primary Packaging | |

| Secondary Packaging | ||

| Tertiary / Transit Packaging | ||

| By End-Use Industry | Food | |

| Beverage | ||

| Healthcare and Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Industrial and Electronic | ||

| Other End-Use Industries | ||

| By Middle East and Africa | By Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| By Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of the Middle East and Africa paper packaging market by 2031?

The market is projected to reach USD 35.13 billion by 2031 based on current growth trajectories.

Which material type is expected to grow fastest through 2031?

Paperboard is forecast to expand at a 7.32% CAGR as quick-service restaurants and personal-care brands adopt lightweight folding cartons.

Why is South Africa the fastest-growing country in regional paper packaging?

Extended Producer Responsibility regulations and rising export-grade corrugated demand push South Africa’s market to an 7.86% CAGR.

How are power outages affecting converters in Sub-Saharan Africa?

Unreliable grids force investment in diesel or hybrid power systems, adding up to 18% to energy costs and impacting production stability.

Which end-use sector is outpacing food in packaging demand growth?

Personal care and cosmetics will grow at an 8.02% CAGR as premiumization and localized brand launches multiply carton SKUs.

What strategic moves are large companies making to secure feedstock?

Integrated producers are locking in long-term pulp contracts, investing in recycling plants, and expanding containerboard lines to stabilize raw-material supply.

Page last updated on: