Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

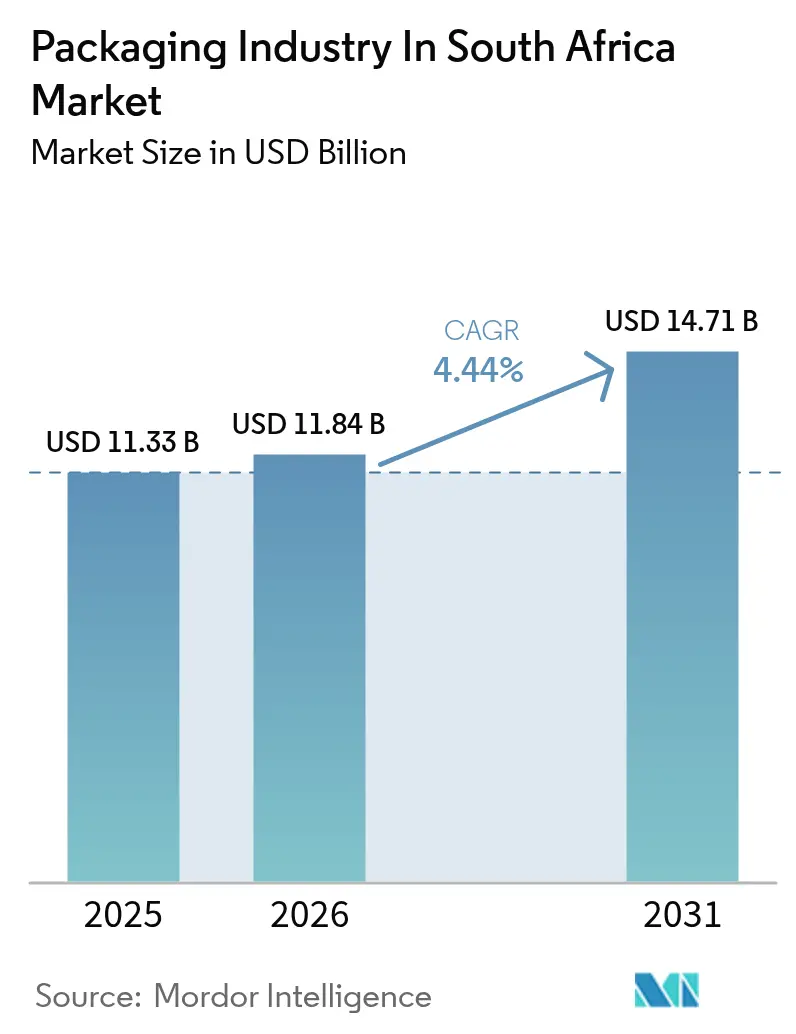

| Base Year Market Size (2025) | USD 11.33 Billion |

| Market Size (2026) | USD 11.84 Billion |

| Market Size (2031) | USD 14.71 Billion |

| Growth Rate (2026 - 2031) | 4.44% CAGR |

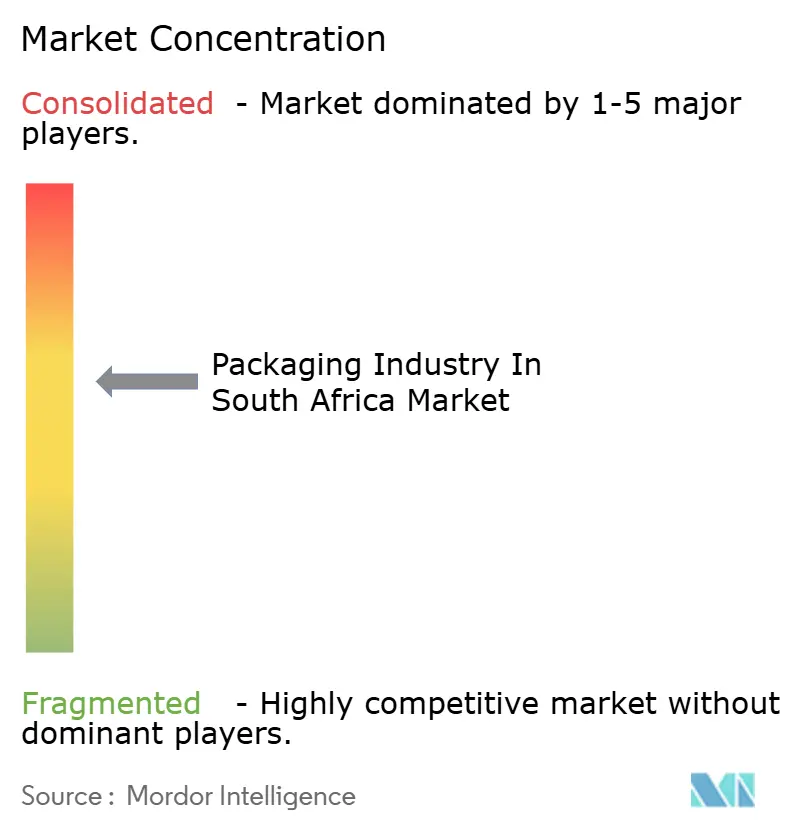

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Analysis of Packaging Industry In South Africa Market by Mordor Intelligence

The Packaging industry in South Africa market size is projected to expand from USD 11.33 billion in 2025 and USD 11.84 billion in 2026 to USD 14.71 billion by 2031, registering a 4.44% CAGR between 2026 and 2031.COM. E-commerce parcel growth, pharmaceutical localization rules, and government-backed Extended Producer Responsibility (EPR) fees are lifting structural demand even as energy costs and polymer price swings squeeze converter margins. Brand owners are rushing to mono-material flexible films that meet recyclability thresholds, while cold-chain upgrades for biologics spur rigid vial and blister volumes. Domestic mills are pivoting toward containerboard capacity as print-grade demand erodes, and on-site solar installations are becoming a standard hedge against Eskom load-shedding. Alliances among mid-tier converters for joint recycled-resin sourcing point to a more integrated supply chain, although talent shortages in packaging engineering remain a brake on expansion.

Key Report Takeaways

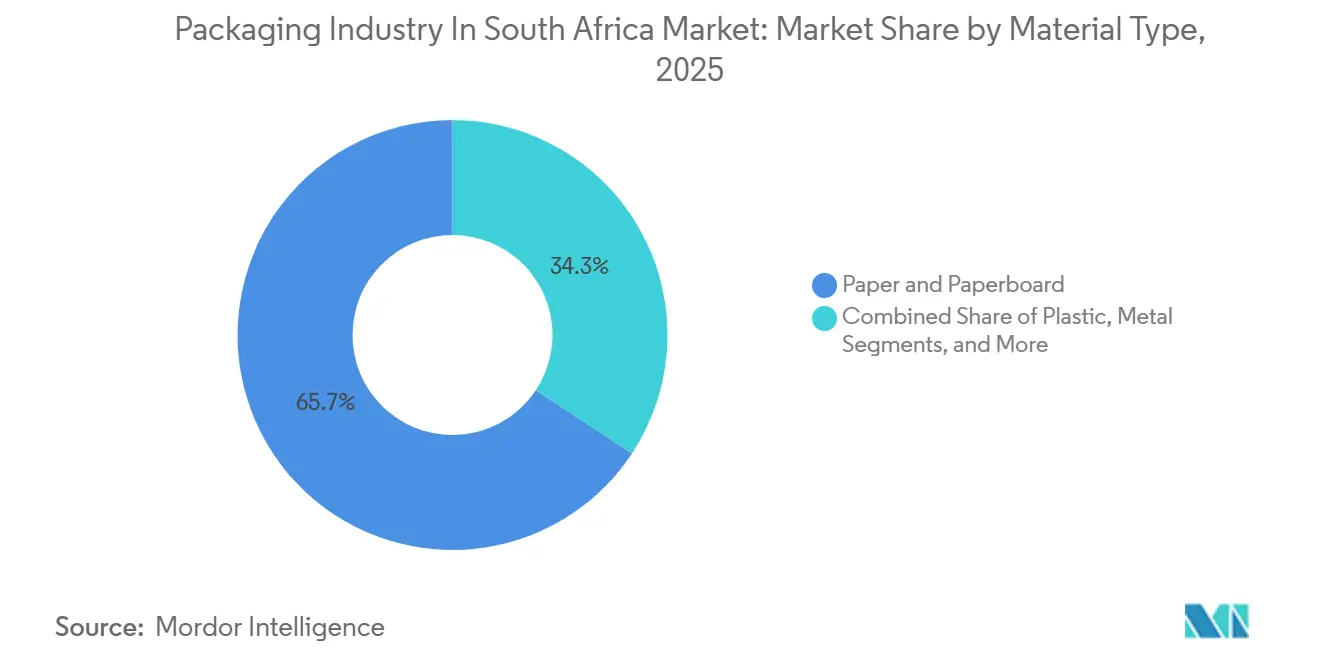

- By material type, paper and paperboard led with 65.72% revenue share in 2025, while plastic is projected to record the fastest 4.47% CAGR through 2031.

- By product type, paper and paperboard product type captured 41.94% share of the Packaging industry in South Africa market size in 2025, whereas plastic product type is set to expand at a 5.11% CAGR to 2031.

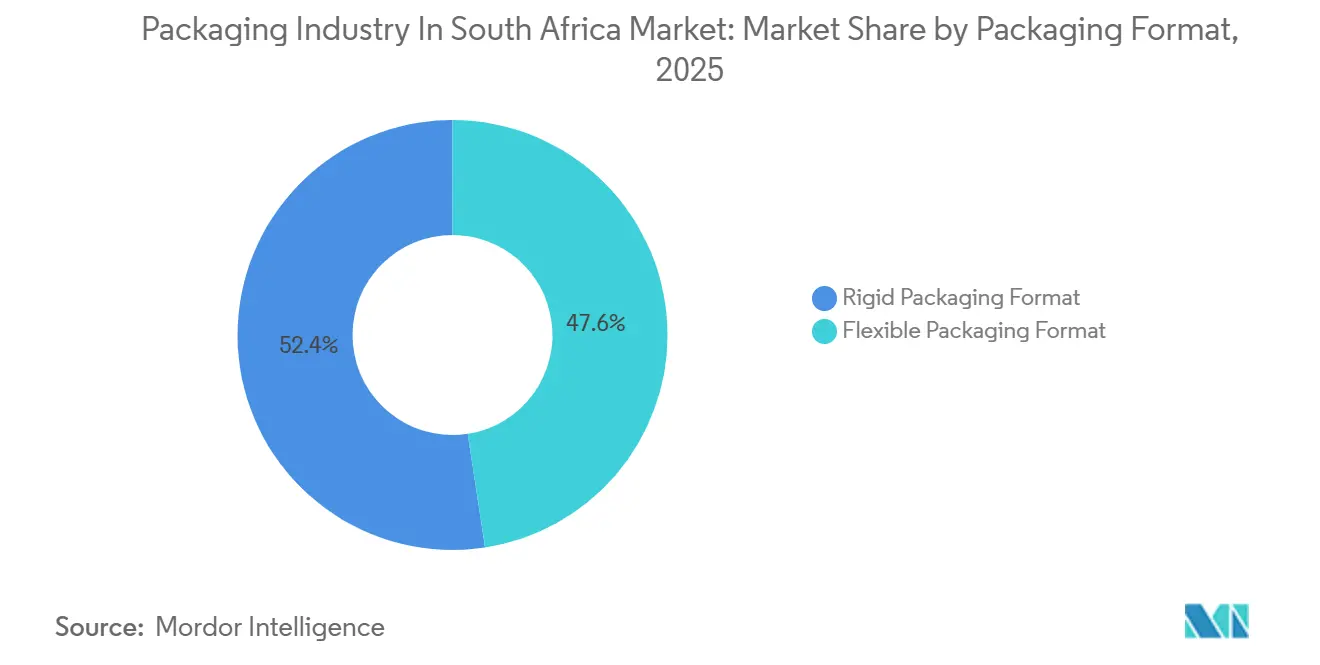

- By packaging format, flexible packaging commanded 47.58% revenue share in 2025, and rigid packaging is forecast to grow at a 4.97% CAGR during 2026-2031.

- By end-user industry, food accounted for 29.17% share in 2025, yet pharmaceutical and medical applications are advancing at a 5.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Insights and Trends of Packaging Industry In South Africa Market

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand From Food and Beverage Industry | +0.9% | National, with concentration in Western Cape (citrus, wine) and Gauteng (processed foods) | Medium term (2-4 years) |

| Rising Demand From Organised Retail Chains | +0.6% | National, led by Gauteng, Western Cape, KwaZulu-Natal metro corridors | Short term (≤ 2 years) |

| Surge In E-Commerce and Last-Mile Delivery Packaging | +1.1% | National, with early gains in Johannesburg, Cape Town, Durban fulfillment hubs | Medium term (2-4 years) |

| Expanding Pharmaceutical and Medical Packaging Needs | +0.8% | National, anchored by Gauteng pharmaceutical manufacturing clusters | Long term (≥ 4 years) |

| Government Incentives For Localisation of Packaging Manufacturing | +0.5% | National, prioritizing Special Economic Zones in Eastern Cape, KwaZulu-Natal | Long term (≥ 4 years) |

| Adoption of Tamper-Evident and Smart Packaging Solutions | +0.4% | National, with pharmaceutical and premium food segments leading | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from Food and Beverage Industry

Corrugated-box orders climbed after citrus exports hit 163 million cartons in the 2024-2025 season, forcing linerboard imports and prompting Sappi to add 220,000 metric tons of containerboard capacity by late 2026.[1]Sappi. "Sappi Announces Somerset Mill Conversion to Containerboard." November 2024 Premium glass bottles gained favor as craft-beer launches sought shelf differentiation, and retailer mandates for recyclable substrates accelerated mono-material film uptake. Converter profit, however, stayed under pressure because raw-material surcharges could not be passed on immediately. Many players now consider vertical integration into pulp or resin recycling to defend margins. The driver will keep the Packaging industry in South Africa market on an upward volume trajectory even if pricing remains volatile.

Surge in E-Commerce and Last-Mile Delivery Packaging

Online retail penetration reached 7.2% of sales in 2025, translating into 42 million parcel shipments that all needed lightweight mailers. Mpact responded with fluting grades that shave 18% off box weight while preserving edge-crush strength, and parcel shippers welcomed the savings on dimensional-weight fees. Temperature-controlled biologic drugs ordered online amplified demand for insulated cartons lined with phase-change panels. Certification under SANS 289 tightened oversight of food-contact materials used in direct-to-consumer meal kits, nudging converters to invest in compliant inks and coatings. Although parcel-return loops for EPR compliance remain sub-economic for low-value orders, deposit trials now underway could unlock cost advantages for frequent shoppers. The e-commerce driver reinforces the Packaging industry in South Africa market as a resilient growth pocket even in sluggish retail cycles.

Expanding Pharmaceutical And Medical Packaging Needs

Domestic drug output expanded 11% in 2025, lifting blister and vial volumes that rely on polypropylene, polyvinyl chloride and aluminum foil.[2]Constantia Flexibles. "Constantia Flexibles Acquires Afripack." September 2024 Serialization deadlines of January 2027 forced carton printers to install digital presses capable of unique codes, while cold-chain infrastructure built for COVID-19 vaccines now services routine immunization. Converters supplying this segment gain pricing power because stringent stability and regulatory requirements limit quick supplier substitution. Local active-pharmaceutical-ingredient capacity remains tight, yet packaging demand decouples from that bottleneck as imports still need compliant secondary packs when filled domestically. Pharmaceutical uptake therefore adds a long-run tailwind for the Packaging industry in South Africa market.

Government Incentives For Localisation Of Packaging Manufacturing

The Department of Trade, Industry and Competition paid out ZAR 1.2 billion (USD 67 million) in 2024-2025 to spur recycling and energy-efficient upgrades.[3]Department of Trade, Industry and Competition (DTIC). "Production Incentive Programme 2024-2025." ALPLA’s Gauteng recycling plant secured a 15% grant and a 12-year tax holiday, while Huhtamaki’s molded-fiber line obtained 50% grant co-funding. EPR fees ranging from ZAR 0.08 to ZAR 0.15 per kilogram make high recycled-content packs economically attractive, especially when import duties raise virgin resin costs. The chief bottleneck is a shortfall of 2,500 skilled technologists, which slows deployment of new equipment. Still, incentives cut payback periods and have begun to reshape the Packaging industry in South Africa market toward a domestic circular-economy model.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Environmental Concerns and Stricter Waste Regulations | -0.7% | National, with enforcement concentrated in metropolitan municipalities | Medium term (2-4 years) |

| Volatile Polymer and Paper Raw-Material Prices | -1.2% | National, affecting all converter segments reliant on imported feedstock | Short term (≤ 2 years) |

| Power-Supply Instability Inflating Production Costs | -0.9% | National, with acute impact on Gauteng, KwaZulu-Natal industrial zones | Short term (≤ 2 years) |

| Shortage of Skilled Packaging Technologists and Engineers | -0.5% | National, with critical gaps in Gauteng, Western Cape manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Polymer And Paper Raw-Material Prices

Polypropylene prices climbed 12% in early 2025 as oil reached USD 88 per barrel, while rand weakness magnified import costs. Chemical pulp imports grew 9% expensive when Brazilian mills diverted output to tissue grades. Converter contracts that reset quarterly lagged spot prices by up to 90 days, slicing 150-200 basis points off margins at Nampak. With future crude unpredictability, converters hedge by locking recycled-resin supply, which now runs 8-12% below virgin pricing. Raw-material volatility therefore, tempers the Packaging industry in the South Africa market CAGR, even while volume outlooks stay positive.

Power-Supply Instability Inflating Production Costs

Stage 2 and Stage 3 load shedding reached 87 days in 2025, disrupting continuous extrusion and thermoforming lines. April 2025 tariffs jumped 15.5%, lifting energy to 12-14% of converter cost for rigid plastics. Mpact installed 6 MW of lithium-ion storage across Gauteng plants and cut downtime by 40%. ALPLA’s 8 MW rooftop solar meets 40% of its Lanseria daytime load. Firms lacking backup lose 5-8% productivity each outage restart. Capital for energy retrofits diverts funds from capacity expansion, slowing the Packaging industry in the South Africa market even as efficiency gains accumulate over time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Fiber Dominance Meets Polymer Innovation

Paper and paperboard contributed 65.72% of 2025 revenue, underpinned by corrugated shipping boxes for agriculture and e-commerce. The Packaging industry in the South Africa market size for paperboard will still rise, yet plastics will post the quickest 4.47% CAGR through 2031, as mono-material polyethylene films meet both moisture-barrier and recyclability requirements. Polypropylene leads rigid packs for food and household chemicals, while polyethylene terephthalate gains share in beverage bottles because of lightweighting and 25% recycled-content commitments. Metal packaging accounted for a considerable share of revenue, benefits from lightweighting, and container glass holds a niche but premium wine and craft-beer volumes. Plastic’s climb is anchored in pharmaceutical blister demand, and in snack pouches that use solvent-free barrier coatings. Fiber producers are adding linerboard machines, such as Sappi’s 220,000-ton project, reflecting a pivot away from graphic papers. Overall, raw-material substitution will rebalance inputs but leave paperboard structurally dominant in the Packaging industry in the South Africa market.

Continued energy inflation nudges converters to glass and metal, where electric-furnace or smelting efficiencies offset power costs. Recycled-content mandates under the 2027 EPR phase compel polyethylene terephthalate bottle makers to lock up post-consumer bales at premiums of 15-20% over virgin. In contrast, linerboard now benefits from domestic forestry integration, holding a safeguard against forex swings. With municipal collection at 60-80% for metal and glass yet limited for flexibles, fiber and rigid substrates could expand share if sorting infrastructure remains uneven. Still, brand owner aesthetic demands and shipping weight economics ensure a multiboard mix, cementing material-diversified growth for the Packaging industry in South Africa market.

By Product Type: Flexible Films Gain Ground

Paper and paperboard products accounted for 41.94% of 2025 turnover, driven by folding cartons for pharmaceuticals and corrugated containers for produce. Flexible plastic pouches, though, are projected to record a 5.11% CAGR to 2031, the swiftest in the Packaging industry in South Africa market. Mpact’s lighter fluting grades let e-commerce shippers lower freight fees, and molded-fiber trays from Huhtamaki replace polystyrene in foodservice. Rigid plastic bottles still dominate dairy and home-care uses, with ALPLA’s Lanseria plant churning out 2.4 billion preforms a year that already contain 25% recycled content. Metal cans enjoy higher recycling rates and thus lower EPR fees, positioning them as a hedge against rising virgin polymer costs.

Converters adapt high-barrier mono-material films, such as Amcor’s AmPrima, which achieved 10% recycled content in 2025 and targets 30% by 2030. Carton board printers integrate digital features for serialization, pushing value growth faster than volume. Single-use paper cups and clamshells grow as municipal plastic bans widen. Because flexibles offer 30-40% material savings over rigids, brand owners will keep switching as barrier tech improves. The product-type mix will therefore tilt gradually toward pouches and films, yet corrugated and carton formats remain irreplaceable for heavy or fragile SKUs, sustaining a balanced Packaging industry in South Africa market.

By Packaging Format: Rigid Structures Accelerate

Flexible packaging held 47.58% of 2025 revenue by leveraging film efficiency and form-fill-seal speed. Rigid formats, however, are forecast to advance at a 4.97% CAGR because vial, can and premium glass demand grow faster than the base, giving them momentum inside the Packaging industry in South Africa market. Lightweight aluminum cans are now 8-10% lighter, saving brewers material costs. Glass enjoys brand-enhancement appeal for craft beverages. Rigid polyethylene terephthalate bottles with 25% recycled content meet beverage carbon reduction pledges and qualify for lower EPR rates.

Rigid adoption is strongest in regulated pharma, where barrier integrity and tamper evidence trump weight savings. Solar-powered furnaces at Consol Glass reduce emissions intensity, helping offset power-grid shocks. Meanwhile, flexibles maintain volume leadership in snacks and frozen food because pouches stack and ship efficiently. Shoprite’s switch to recyclable potato bags demonstrates how mono-film technology can protect flexible packaging. The coexistence of both formats anchors supply-chain resilience, allowing the Packaging industry in the South Africa market to respond swiftly to raw-material or regulatory shifts.

By End-User Industry: Pharma Outpaces Food

Food absorbed 29.17% of demand in 2025 due to citrus, wine, and processed meals, but pharmaceutical and medical users will deliver the steepest 5.07% CAGR to 2031. Cold-chain investments from the pandemic era linger, pushing uptake of indicator labels and insulated cartons. Beverage end-users, encompassing carbonated soft drinks, bottled water, beer, wine, and spirits, experienced robust demand.

Pharmaceutical and Medical applications grew in 2025, reaching ZAR 38 billion (USD 2.1 billion) in manufacturing output, as Aspen Pharmacare and Adcock Ingram expanded local production to satisfy SAHPRA's localization targets for essential medicines. Personal Care and Cosmetics end-users drove revenue, influenced by premium skincare and haircare launches that favor glass jars and aluminum tubes for brand differentiation. Industrial and Chemical applications, including lubricants, paints, and agrochemicals, contributed significantly, with bulk-grade rigid plastics and steel drums dominating. Other End-User Industries, including electronics, construction, and consumer durables, collectively contributed to the 2025 revenue.

Geography Analysis

Gauteng, Western Cape and KwaZulu-Natal hosted nearly 80% of 2025 production and roughly three-quarters of consumption. Gauteng’s Johannesburg hub combines logistics corridors with proximity to Sasol feedstock, but frequent load-shedding pushes converters toward solar and battery hybrids. Western Cape’s packaging growth mirrors wine and citrus exports; corrugated demand climbed 6% during the 2024-2025 season, prompting linerboard imports amid congestion at the Cape Town port. KwaZulu-Natal links sugar and automotive chains through the Durban port, where Transnet's digitization cut dwell time by 15-20%, lowering converter inventory costs.

Special Economic Zones in Eastern Cape and KwaZulu-Natal offer 12-year tax holidays and 10-15% capital grants, enticing new entrants. ALPLA’s Gauteng recycling plant handles 1.8 billion bottles a year, feeding beverage lines concentrated in the province. Huhtamaki’s fiber expansion in KwaZulu-Natal supplies quick-service restaurants shifting from foam trays.

Cross-border exports to Botswana, Namibia, Zimbabwe, and Mozambique take an 8-10% share, yet currency swings and tariffs in Mozambique limit further rise. Rail bottlenecks remain a constraint that may ease as public-private partnerships invest in wagon fleets. Skill shortages cluster in Gauteng and Western Cape, reinforcing the need for training programs if the Packaging industry in South Africa market is to capture its full growth potential.

Competitive Landscape

The top five converters hold a considerable revenue share, giving the Packaging industry in South Africa a moderate concentration profile. Multinationals leverage global resin contracts that run 5-8% cheaper than domestic spot, yet quarterly pass-through lags still expose them to temporary margin compression. Amcor’s April 2025 merger with Berry Global created a USD 24 billion entity that is now rationalizing South African flexible-film lines and eyeing USD 650 million in global synergies. Mpact’s 6 MW battery installation cut outage downtime in half, signaling that energy resilience is a core differentiator.

ALPLA filled a supply gap of 80-100 thousand tons in food-grade recycled polyethylene terephthalate, easing brand-owner stress over 25-30% recycled-content pledges. Smaller converters form procurement consortia to pool EPR compliance and compete for supermarket tenders, though many lack capital for serialization or machine-vision upgrades.

Private equity scouts mid-tier firms with robust customer lists but thin balance sheets, expecting three to five acquisitions by 2028 at six-to-eight-times. Technology investments around inline inspection, digital printing and energy management will widen the gap between leaders and laggards, shaping the next phase of the Packaging industry in South Africa market.

Leaders of Packaging Industry In South Africa Market

-

Mondi plc

-

Nampak Limited

-

Mpact Limited

-

Consol Glass (Pty) Ltd.

-

Smurfit Kappa Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Amcor completed its merger with Berry Global, forming a USD 24 billion packaging group and beginning capacity rationalization in South Africa.

- March 2025: Shoprite rolled out 100% recyclable low-density-polyethylene potato bags across 3,000 stores, adding 15,000 metric tons of mono-film demand.

- February 2025: Nampak reported ZAR 16.2 billion (USD 900 million) revenue with beverage-can volumes up 4% despite margin pressure from polymer inflation.

- January 2025: ALPLA commissioned a USD 60 million polyethylene terephthalate recycling plant in Gauteng that processes 1.8 billion bottles annually and runs on 8 MW rooftop solar.

Scope of Report on Packaging Industry In South Africa Market

The market is tracked based on the analysis of materials, products, and end-user industries, providing a detailed assessment of all types of packaging based on factors related to the different packaging product's demand and supply. The study also covers the packaging industry limited to South Africa and the vendors operating in the country.

The South Africa Packaging Market Report is Segmented by Material Type (Paper and Paperboard, Plastic, Metal, and Container Glass), Product Type (Paper and Paperboard Product Type, Plastic Product Type, Metal Product Type, and Container Glass Product Type), Packaging Format (Rigid Packaging Format and Flexible Packaging Format), End-User Industry (Food, Beverage, Pharmaceutical and Medical, Personal Care and Cosmetics, Industrial and Chemical, Agriculture, Automotive, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Paper and Paperboard | |

| Plastic | Polypropylene (PP) |

| HDPE and LDPE | |

| PET | |

| PVC | |

| Polystyrene (PS) | |

| Other Plastics | |

| Metal | |

| Container Glass |

By Product Type

| Paper and Paperboard Product Type | Folding Carton and Rigid Boxes | |

| Corrugated Boxes and Containers | ||

| Single-use Paper Products | ||

| Other Paper and Paperboard Types | ||

| Plastic Product Type | Rigid Plastics | Bottles and Jars |

| Caps and Closures | ||

| Bulk-grade Products | ||

| Other Rigid Plastics | ||

| Flexible Plastics | Pouches | |

| Bags | ||

| Films and Wraps | ||

| Other Flexible Plastics | ||

| Metal Product Type | Cans | |

| Caps and Closures | ||

| Aerosol Containers | ||

| Other Metal Types | ||

| Container Glass Product Type | Bottles | |

| Jars | ||

By Packaging Format

| Rigid Packaging Format |

| Flexible Packaging Format |

By End-user Industry

| Food |

| Beverage |

| Pharmaceutical and Medical |

| Personal Care and Cosmetics |

| Industrial and Chemical |

| Agriculture |

| Automotive |

| Other End-user Industries |

| By Material Type | Paper and Paperboard | ||

| Plastic | Polypropylene (PP) | ||

| HDPE and LDPE | |||

| PET | |||

| PVC | |||

| Polystyrene (PS) | |||

| Other Plastics | |||

| Metal | |||

| Container Glass | |||

| By Product Type | Paper and Paperboard Product Type | Folding Carton and Rigid Boxes | |

| Corrugated Boxes and Containers | |||

| Single-use Paper Products | |||

| Other Paper and Paperboard Types | |||

| Plastic Product Type | Rigid Plastics | Bottles and Jars | |

| Caps and Closures | |||

| Bulk-grade Products | |||

| Other Rigid Plastics | |||

| Flexible Plastics | Pouches | ||

| Bags | |||

| Films and Wraps | |||

| Other Flexible Plastics | |||

| Metal Product Type | Cans | ||

| Caps and Closures | |||

| Aerosol Containers | |||

| Other Metal Types | |||

| Container Glass Product Type | Bottles | ||

| Jars | |||

| By Packaging Format | Rigid Packaging Format | ||

| Flexible Packaging Format | |||

| By End-user Industry | Food | ||

| Beverage | |||

| Pharmaceutical and Medical | |||

| Personal Care and Cosmetics | |||

| Industrial and Chemical | |||

| Agriculture | |||

| Automotive | |||

| Other End-user Industries | |||

Key Questions Answered in the Report

What is the size of the Packaging Industry in South Africa?

The Packaging Industry in South Africa reached USD 11.33 billion in 2025, is projected to attain USD 11.84 billion in 2026, and is forecast to expand to USD 14.71 billion by 2031.

Which material type holds the largest market share?

Paper and Paperboard commanded 65.72% of material-type revenue in 2025. However, Plastic is forecast to grow at the fastest 4.47% CAGR through 2031.

What are the fastest-growing segments in the market?

Pharmaceutical and Medical end-users are forecast to post the steepest 5.07% CAGR through 2031, followed by Plastic Product Type at 5.11% CAGR, Rigid Packaging Format at 4.97% CAGR, and Plastic materials at 4.47% CAGR.

Which companies are leading the South African packaging market?

The top converters include Mondi, Nampak, Mpact, Amcor and Consol Glass.

What is the outlook for pharmaceutical packaging in South Africa?

Pharmaceutical packaging is the fastest-growing end-user segment at 5.07% CAGR through 2031.

Page last updated on: