Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 28.74 Billion |

| Market Size (2026) | USD 30.26 Billion |

| Market Size (2031) | USD 39.13 Billion |

| Growth Rate (2026 - 2031) | 5.30% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Packaging Market Analysis by Mordor Intelligence

The Mexico packaging market size is expected to grow from USD 28.74 billion in 2025 to USD 30.26 billion in 2026 and is forecast to reach USD 39.13 billion by 2031 at 5.3% CAGR over 2026-2031. Nearshoring-led factory migration from Asia, escalating e-commerce volumes, and mandatory sustainability disclosures under NIS A-1 and NIS B-1 are the primary forces that keep the Mexico packaging market on an expansionary track. Plastics continue to command scale, yet paper and flexible substrates capture incremental share as brands recalibrate specifications to satisfy consumer and regulatory demands for recyclability. Digital printing technology, growing at 6.23% CAGR, enables converters to serve shorter production runs tied to nearshoring, while energy-price volatility and anti-dumping measures on Asian substrates introduce cost uncertainty. Consolidation exemplified by the Smurfit Kappa–WestRock merger signals intensifying competition as global majors seek a foothold in the Mexico packaging market.

Key Report Takeaways

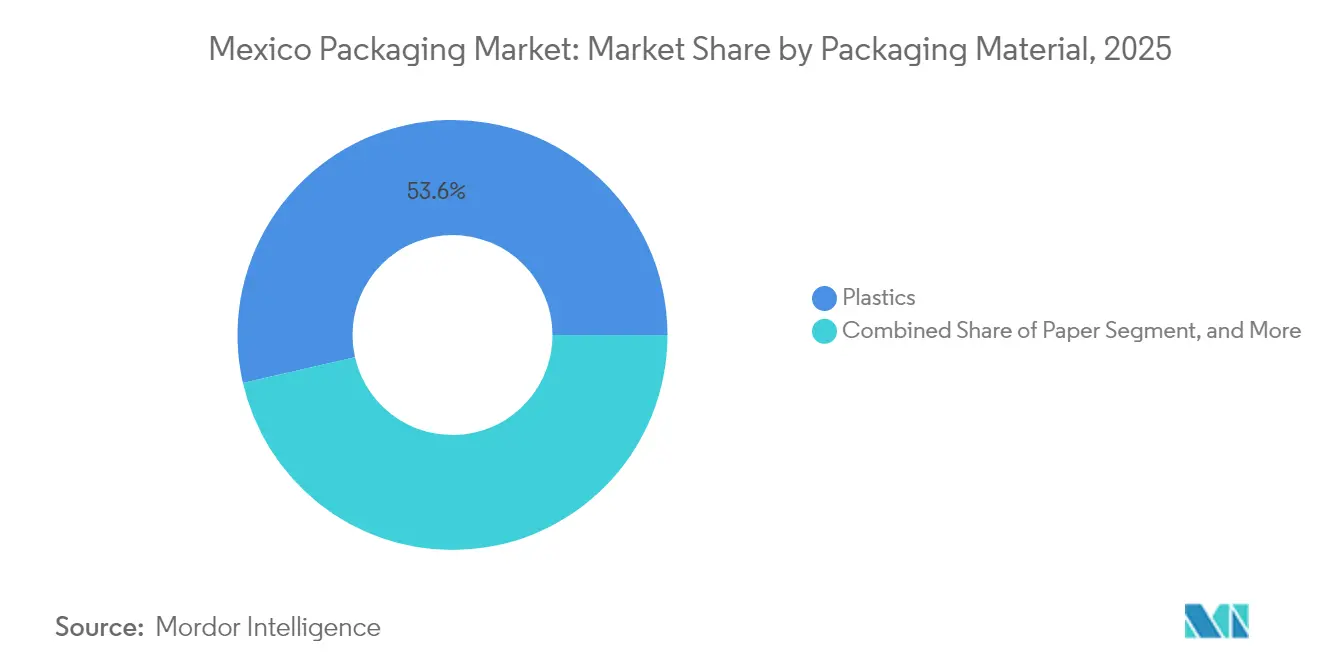

- By packaging material, plastics held 53.58% of Mexico packaging market share in 2025, while paper is projected to post the fastest 5.92% CAGR through 2031.

- By packaging type, rigid formats led with 51.88% revenue share in 2025; flexible solutions are forecast to expand at a 6.1% CAGR to 2031.

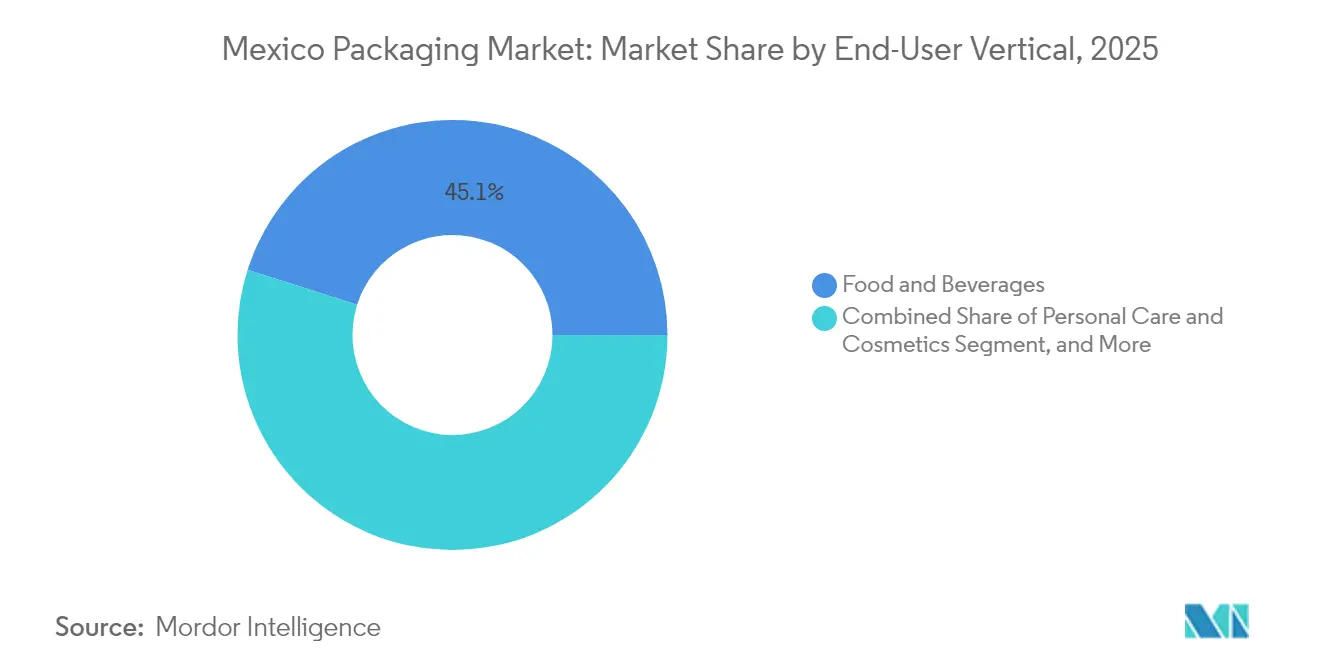

- By end-user vertical, food and beverages accounted for 45.10% of the Mexico packaging market size in 2025, whereas pharmaceutical applications are advancing at a 5.78% CAGR through 2031.

- By printing technology, flexography captured 38.55% of Mexico packaging market share in 2025; digital printing is growing at a 6.01% CAGR over the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nearshoring-driven capacity expansions | +1.2% | Northern border states; central manufacturing hubs | Medium term (2-4 years) |

| Boom in e-commerce fulfillment packaging | +0.8% | National; Mexico City, Guadalajara, Monterrey | Short term (≤ 2 years) |

| Surge in food-processing exports to the United States | +0.6% | Border zones; agricultural regions | Medium term (2-4 years) |

| Mandatory recycled-content targets | +0.4% | Nationwide; stricter in Mexico City | Long term (≥ 4 years) |

| Rapid adoption of digital package printing | +0.5% | Urban export-oriented plants | Short term (≤ 2 years) |

| Government incentives for PET recycling plants | +0.3% | Industrial states nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nearshoring-driven capacity expansions transform supply-chain architecture

Foreign direct investment into Mexico rose 30% in 2023 to USD 33 billion, almost half of which flowed to new entrants establishing lines that require packaging tailored for just-in-time cross-border shipments. Manufacturing’s 17% share of GDP and 5.2% annual growth amplify consumption of corrugated cases, pallets, and export-grade labels. Interconnected production where 40% of a finished product’s value is U.S.-origin calls for packaging engineered for mixed regulatory regimes and multi-modal transit. Industrial property demand is on an 80% up-swing, spurring build-outs of fully automated box plants and filling lines. Tax incentives under Plan Mexico permit 35%–91% accelerated depreciation on new fixed assets, lowering acquisition costs for converting machinery.

E-commerce fulfillment packaging surge reshapes material demand

Online retail penetration hit 15% of total sales in 2025 and is on track to reach USD 176.8 billion by 2026, accelerating the pivot from rigid corrugate to lightweight mailers and cushioning systems that reduce dimensional weight fees. Food-delivery platforms valued at USD 2.5 billion generated more than 300,000 tons of packaging waste in 2024, prompting Mexico City’s enforcement of single-use plastic bans that have levied over 70,000 fines. Retailers invested USD 2.1 billion in store expansion and hired 640,000 workers in 2024, translating into higher secondary and tertiary packaging volumes. With e-commerce forecast to grow 9.8% CAGR, converters deploy digital work-flows and recycled content to balance sustainability mandates with protective performance. Circular pilots such as Vytal’s returnable container network and Rappi’s 20,000-ton plastic recovery illustrate early-stage demand for reusable formats.

Food-processing export boom drives specialized packaging requirements

United States agricultural shipments to Mexico climbed 65% in four years to USD 31.4 billion in 2024, intensifying demand for packaging that satisfies FDA and COFEPRIS norms simultaneously. Dairy exports alone expanded 76% since 2020, spurring sales of multilayer pouches with high oxygen barriers. Domestic corn output dropped from 27.5 million tons in 2023 to 23.7 million tons in 2024 due to drought, raising imports and hence bulk-handling packaging volumes. The National Tortilla Council warns of 40% price hikes, elevating shelf-life extension priorities for flexible films. Meanwhile, meat-packing plants adopt high-performance trays and absorbent pads to preserve cold-chain integrity on extended U.S. routes.

Mandatory recycled-content targets reshape procurement

NIS A-1 and NIS B-1 standards effective 2025 compel publicly traded firms to disclose environmental metrics including recycled content and end-of-life recovery alongside financials. Brand owners now stipulate post-consumer resin thresholds of 30%–50% in bids, driving contract renegotiations with resin suppliers. PET recycling capacity receives a boost from government incentives offering a 25% deduction on training and innovation tied to circular projects, reinforcing facility expansions such as PetStar’s Toluca plant that processes 3.4 billion bottles annually. However, supply lags demand, leading to price premiums for certified PCR material that ripple through finished-goods quotations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-price volatility squeezing converter margins | -0.9% | National; pronounced in northern states | Short term (≤ 2 years) |

| Anti-dumping duties on Asian substrates | -0.6% | Import-dependent facilities; border zones | Medium term (2-4 years) |

| Shortage of certified post-consumer resin | -0.4% | Beverage and food packaging clusters | Medium term (2-4 years) |

| Growing consumer backlash against multilayer laminates | -0.3% | Mexico City; coastal states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy-price volatility pressures converter profitability

Electricity tariffs differ sharply across Mexico’s industrial corridors, complicating budgeting for extrusion, blow-molding, and printing assets . The National Energy Plan earmarks USD 23.4 billion for grid upgrades and renewable capacity, yet timelines place tangible relief beyond 2026. Petroleum-based raw-materials costs add another layer of fluctuation, as PEMEX recalibrates feedstock allocations toward low-carbon pathways. Converters counter volatility with on-site solar arrays and energy-efficient electric blow-molding lines, but upfront capex remains prohibitive for small and mid-size firms.

Anti-dumping measures disrupt Asian substrate supply chains

February 2025 investigations into Chinese cardboard and polycarbonate imports threaten duties of 5%–50% that would elevate input costs for corrugated and rigid plastic packaging. Parallel tariff reinstatements on 544 goods until April 2026 further tighten supply, with textiles and certain plastics losing IMMEX duty suspension benefits. Converters scramble to re-source substrates domestically or from USMCA partners, extending lead-times and inflating inventories. Price escalation risks intensify ahead of 2026 USMCA renegotiations as policymakers position local industries for leverage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Material: recyclability pushes paper uptake

Plastics dominated the Mexico packaging market with 53.58% Mexico packaging market share in 2025, underpinned by durability and barrier properties demanded by food, pharmaceutical, and industrial clients. Yet stringent single-use bans in Mexico City, Durango, Quintana Roo, Zacatecas, and Michoacán incentivize substitution, elevating paper’s 5.92% CAGR through 2031. Government procurements increasingly specify biodegradable or fiber-based solutions, prompting carton and molded-fiber capacity additions among converters.

Momentum also stems from technology gains in enzymatic and chemical recycling of PET that mitigate environmental pushback against plastics. Covestro, Braskem, and Carbios pilot depolymerization systems that promise lower energy intensity. For rigid glass and metal segments, growth remains stable but muted due to transport costs and weight. Composite and bio-based innovations like starch-lined corrugate and PLA blends inch toward commercial scale as material science advances.

By Packaging Type: flexible platforms capture e-commerce tailwinds

Rigid containers retained 51.88% share of the Mexico packaging market size during 2025, driven by beverage bottles, thermoformed trays, and pharmaceutical vials that require structural integrity. However, flexible formats are poised for 6.1% CAGR, propelled by courier networks favoring lightweight pouches and mailers that cut freight charges. Brands appreciate the high product-to-package ratio and shelf-appeal graphics achievable on laminates and monomaterial films.

Consumer backlash against unrecyclable multilayer wraps pushes R&D toward mono-PE and mono-PP architectures compatible with mechanical recycling streams. COFEPRIS front-of-pack regulations under NOM-051 drive label redesigns on flexible substrates, fostering demand for variable data printing. Supply shocks from anti-dumping actions on Asian plastics accelerate investment in domestic film extrusion lines, enhancing regional self-reliance.

By End-User Vertical: healthcare accelerates amid food leadership

Food and beverages commanded 45.10% Mexico packaging market share in 2025, reflecting sustained retail sales growth and Mexico’s emergence as the top U.S. agricultural export destination. Rising incomes and urbanization fuel demand for portion-controlled snacks and ready-to-eat meals that rely on modified-atmosphere packaging. Simultaneously, pharmaceutical applications expand at a 5.78% CAGR to 2031 as COFEPRIS’s updated NOM-137 enables electronic labeling and encourages localized fill-finish operations.

Personal-care and cosmetics benefit from premiumization trends, adopting airless pumps and recyclable mono-material tubes. Automotive and industrial sectors ride nearshoring momentum, specifying heavy-duty corrugated and engineered returnable trays for cross-border loops. Sustainability commitments Grupo Bimbo’s 94% recyclable packaging achievement in 2024 pressure all verticals to advance circularity targets

By Packaging Technology: digital printing rises on customization demand

Flexographic presses still hold 38.55% Mexico packaging market share thanks to cost advantages on long runs. Yet digital systems are clipping 6.01% CAGR as brands request SKU proliferation and serialized traceability, especially in pharmaceuticals. EXPO PACK México 2024 showcased HP Indigo and Xeikon units capable of short runs with zero plates, reducing time-to-market .

Converters integrate hybrid lines that marry flexo productivity with digital finishing for variable data, enabling versioned campaigns for export and domestic audiences. Imports of high-resolution inkjet heads from the United States and China expand capabilities beyond native supply. Offset lithography and gravure remain niche, serving luxury packaging that mandates extended color gamut and tactile embellishments.

Geography Analysis

Northern border states Nuevo León, Chihuahua, and Baja California anchor automotive and electronics packaging lines tailored for rapid cross-dock into the United States. Industrial property demand is projected to climb 80% as nearshoring projects advance, compelling packaging suppliers to co-locate near OEM clusters for just-in-sequence delivery. Higher wages and tight labor markets in these zones elevate automation investments, including robotic case erectors and palletizers that offset staffing gaps.

Central manufacturing corridors around Mexico City, Puebla, and Guadalajara balance export and domestic consumption flows. Robust highway and rail links, coupled with a dense supplier base, make the region attractive for flexible packaging converters serving food and personal-care brands. However, Mexico City’s stringent plastic-ban enforcement drives swift material pivots toward paper or compostables, forcing converters to diversify substrates.

The southeast gains strategic relevance through the Maya Train and Interoceanic Corridor projects that enhance connectivity between Pacific and Atlantic ports. Expected cargo rerouting encourages new corrugated and bulk-bag facilities to support agri-exports and mineral shipments. Still, infrastructure bottlenecks high electricity tariffs and water scarcity temper speed of build-outs. State tax surcharges on emissions and waste add compliance costs that favor large, vertically integrated groups with ESG reporting systems.

Regulatory Landscape

Mexico packaging is governed primarily by Official Mexican Standards (NOMs), administered through federal standardization and market-surveillance bodies such as the Secretaria de Economia and PROFECO. In practice, noncompliance can create customs and commercialization risk. For consumer goods, NOM-051-SCFI/SSA1-2010 sets mandatory commercial and sanitary labeling rules for pre-packaged food and non-alcoholic beverages, driving recurring label redesign and specification control across substrates.

In 2026, the General Law of Circular Economy (Ley General de Economia Circular) introduced a national framework that requires legal entities producing or importing goods to implement a circular management scheme registered with SEMARNAT. That change raises the bar for end-of-life planning and material compatibility. For industrial and logistics packaging, hazardous-goods transport requirements are anchored by SCT standards, including NOM-007-SCT-2-2022 for construction, UN marking, and testing of packages and receptacles, and NOM-002-1-SCT-SEMAR-ARTF/2023 covering instructions and use for packaging used in transporting hazardous substances.

Value Chain Analysis

Mexico's packaging value chain runs from upstream feedstocks (petrochemical resins, containerboard and paper inputs, glass and metal) through converting (film extrusion, thermoforming, blow molding, carton and corrugated conversion, closures, labels and printing) to brand owners and logistics users across food and beverage, personal care, pharma, and industrial end markets. Cross-border trade shapes specifications and procurement, with converters balancing Mexico requirements with export compliance for the United States. Packaging machinery and components also form a key enabling layer, particularly where coding and high-speed converting are needed for automation.

Midstream dynamics increasingly hinge on local capacity additions and input volatility management. Examples include SIG's announced investment to expand its Queretaro carton-packaging plant, with phased upgrades starting in 2026 and incorporating new finishing technologies and a printing line. Tetra Pak's Mexicali plant expansion, inaugurated in 2025, increased capacity and added technology upgrades, strengthening domestic supply nodes serving nearshoring-driven demand. On the materials side, containerboard availability and pricing swings, along with trade actions on imported substrates referenced in the report context, reinforce dual-sourcing and inventory strategies, while also pushing more domestic sourcing and recycling integration to secure supply and meet recycled-content requirements.

Competitive Landscape

Market concentration is moderate as global majors strengthen through mergers while a long tail of regional converters retains meaningful share. The Smurfit Kappa-WestRock union created a 40-country giant with 100,000 staff, deepening corrugated capabilities for U.S.-Mexico cross-border trade. The pending Amcor-Berry Global merger, targeting USD 650 million in synergies, will extend film and rigid packaging reach once final approvals clear in mid-2025.

Local innovators capitalize on sustainability and nearshoring. PetStar operates the world’s largest food-grade PET recycling plant in Toluca, processing 3.4 billion bottles annually to feed brand PCR mandates.[1]Waste to Energy Research & Technology Council, “Implementing a Circular Economy in Mexico through PET Recycling,” wtert.net UFlex commissioned a 15,000 MTPA post-consumer PET flake and 6,000 MTPA multilayer plastics recycling line, integrating into its Toluca pouch complex.[2]Ambekar Naveen, “PowerPoint Presentation,” UFlex Limited, uflexltd.com AGH Labels produces 14 billion digital labels annually and opened a Laredo, Texas hub to shorten delivery to U.S. clients.[3]James Quirk, “AGH Labels Targets US Market,” Labels & Labeling, labelsandlabeling.com

Strategic plays focus on closed-loop models and digital workflow adoption. Arca Continental’s PET collection expansion targets 380 million additional bottles each year and incorporates 30.3% recycled content in its packaging. Converters invest in inkjet and laser coding systems for serialization, anticipating pharmaceutical and food traceability mandates. Cost inflation and tariff risk reinforce dual-sourcing strategies, with many firms locking multiyear resin contracts with North American suppliers.

Mexico Packaging Industry Leaders

Grupo Gondi S.A. de C.V.

Smurfit Kappa México, S.A. de C.V.

Envases Universales de México, S.A. de C.V.

Vitro, S.A.B. de C.V.

Amcor Flexibles México, S. de R.L. de C.V.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The 2026 General Law of Circular Economy creates a commercialization pathway for packaging formats that simplify recovery and support auditable circular management schemes registered with SEMARNAT. That includes mono-material flexible structures, fiber-based solutions, and packaging designed for certified waste reintegration. As companies align reporting and documentation with SEMARNAT registrations, demand grows for traceable recycled inputs that can be substantiated within procurement requirements. It also builds on sustainability disclosures already embedded in corporate reporting under NIS A-1 and NIS B-1 effective 2025.

Nearshoring-linked manufacturing build-outs and automation investments are creating opportunities across industrial and transit packaging, high-throughput converting, and short-run customization. In northern hubs, PRONAL Corrugados inaugurated a 28,000-square-meter corrugated plant in Monterrey with initial capacity of 100,000 tonnes annually (January 2026). SIG's Queretaro expansion program then targets a step-up in carton output for North America, which pulls through liners, coatings, inks, and finishing services. Separately, EAM-Mosca's announced investment to expand its Monterrey manufacturing plant for strapping materials and automated packaging systems supports higher adoption of end-of-line automation that improves throughput and reduces damage rates in fast-moving export and e-commerce supply chains.

Recent Industry Developments

- May 2026: Envases Universales de Mexico sought an amparo (file 778/2026) at the Second District Court in Hidalgo to contest a technical site inspection at its recycling plant in the PLATAH industrial park in Apan, and the court denied provisional suspension. The case points to tighter scrutiny of recycling operations and can affect operational continuity, audit readiness, and compliance costs for packaging circularity assets.

- April 2025: Arca Continental and Coca-Cola Mexico invested MXN 56.5 million (USD 2.8 million) to expand a PET bottle collection plant in San Luis Potosi, targeting recovery of 380 million bottles annually. The expansion increases availability of post-consumer feedstock for food-grade PCR, a key constraint for brand owners stipulating recycled-content thresholds in packaging tenders.

- July 2024: ABB announced it was awarded a modernization project for a Smurfit Kappa Mexico board mill, covering machine PM5, with a 98.5% system uptime target for a three-month period following commissioning in 2025. Upgrades that lift uptime and performance on existing paperboard assets strengthen domestic corrugated and board supply and help converters manage lead times amid substrate volatility.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the Mexico packaging market is the value of packaging materials and packaging formats sold for use across consumer and industrial end uses within Mexico, measured at the market price level and reported in USD.

Scope exclusions: It excludes the value of packaged goods themselves, plus standalone packaging machinery, spare parts, and logistics services unless bundled as part of the packaging sold.

Segmentation Overview

- By Packaging Material

- Plastics

- Paper and Paperboard

- Metal

- Glass

- Other Materials

- By Packaging Type

- Flexible Packaging

- Pouches and Bags

- Films and Wraps

- Tubes

- Other Product Types

- Rigid Packaging

- Bottles and Jars

- Trays and Containers

- Other Product Types

- Flexible Packaging

- By End-user Vertical

- Food and Beverage

- Personal Care and Cosmetics

- Home Care

- Pharmaceutical

- Automotive and Industrial

- Other Verticals

- By Packaging Technology

- Flexographic Printing

- Digital Printing

- Gravure Printing

- Offset Lithography

- Other Technologies

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping what is being packaged in Mexico and how packaging demand moves with it, then aligning definitions across materials and formats so the same value is not double counted. We relied on public sources such as INEGI industrial output series, Banco de Mexico macro indicators, Mexico customs trade data, and customs statistics from UN Comtrade to understand import and export flows for key packaging materials.

To keep assumptions realistic, we also reviewed SEMARNAT publications and selected regulatory updates, plus industry association releases and reputed press coverage on resin, paperboard, and aluminum market conditions. Company annual reports, investor presentations, and audited financial statements were used to sanity check capacity additions and pricing commentary, and then a paid subscription focused on company financials and another focused on shipment-level trade helped with cross-checks where public series were too aggregated. These sources are illustrative and not exhaustive, and many other references were used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary validation was done through interviews and structured surveys with packaging converters, material suppliers, distributors, and large packaging buyers across food and beverage, personal care, home care, automotive, and pharmaceuticals. The respondent input also helped explain regional demand differences inside Mexico, especially plant utilization, mix shifts between rigid and flexible formats, and how sustainability requirements are tightening specifications and affecting pricing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 15% | |

| Mid tier: 58% | Functional/Unit leaders: 34% | |

| Smaller Players: 17% | Managers: 51% |

Market-Sizing & Forecasting

Market sizing was built using a top-down model where production, trade, and end-market activity in Mexico were used to reconstruct packaging demand by material and format, then translated into value using observed price ranges. To keep totals practical, we corroborated results with selective bottom-up approximations such as sampled converter revenues, channel checks, and volume-by-average-selling-price builds for high-share packs.

Key inputs included Mexico packaged food and beverage output trends, industrial production growth tied to nearshoring, resin and paperboard price direction, shifts between flexible and rigid packaging in major end uses, and packaging technology adoption indicators (for example, printing-related value add). Forecasts were developed using scenario analysis, with the base case adjusted using primary feedback on price pass-through timing, capacity additions, and demand sensitivity. When a bottom-up signal was missing for a niche material or format, the gap was handled using adjacent category ratios, then re-tested with interview-based checks before locking the final split.

Data Validation & Update Cycle

Validation was done by triangulating the model against independent signals, including trade balances for key inputs, output indicators for major packaged end markets, and realistic price bands discussed in primary calls. If a segment moved outside expected ranges, the assumptions were re-checked, and respondents were re-contacted when the variance could not be explained by seasonality or a one-time shock.

Before sign-off, the model goes through a multi-step analyst review that checks arithmetic, currency conversion timing, and consistency across materials, formats, and end-use demand pools. Reports are refreshed annually, with interim updates when major events materially change demand or pricing. Right before delivery, a fresh pass is completed so clients get the most current view available.

Mordor Intelligence's Mexico Packaging Market Size Versus Other Published Estimates

It is common to see different market sizes for Mexico packaging because publishers draw the boundary in their own way, then apply different pricing assumptions, currency timing, and forecast windows. The base year used, and whether an estimate is a full market value or only incremental growth, can also create large gaps.

By tracking core packaging demand drivers and refreshing price bands each cycle, Mordor Intelligence keeps the Mexico total anchored to Mexico-only consumption plus trade signals, which helps avoid mixing growth-only figures or narrower container-only scopes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 28.74 B (2025) | |

| Industry Analyst Brief A | USD 29.87 B (2024) | Uses a container packaging scope, which can exclude non-container formats and may apply a different product boundary for films, wraps, and paper-based packs, making the total not directly comparable year to year. |

| Research Bulletin B | USD 2.74 B (2026) | Reports market growth (value increase) over a forecast window rather than the full market value for a given year, which understates the market when read as a size figure. |

Taken together, the spread is mainly explained by scope and how the number is expressed, whether it is a total market value or only an incremental increase. When the scope is aligned to all packaging in Mexico and the year is held constant, the remaining differences come mostly from pricing assumptions and how materials and formats are grouped.

Key Questions Answered in the Report

How large is the Mexico packaging market in 2026?

The Mexico packaging market size stands at USD 30.26 billion in 2026.

What is the projected CAGR for Mexico’s packaging sector to 2031?

The market is forecast to grow at a 5.3% CAGR between 2026 and 2031.

Which material segment is expanding fastest?

Paper packaging is expected to post the quickest 5.92% CAGR through 2031 as sustainability mandates tighten.

Why is digital printing gaining traction?

Brand owners require shorter runs and variable data for nearshoring and serialization, pushing digital printing to a 6.01% CAGR.

How do nearshoring trends influence packaging demand?

Foreign factories relocating to Mexico raise demand for export-compliant corrugated, labels, and protective formats optimized for U.S. logistics.

What regulatory changes affect recycled content?

NIS A-1 and NIS B-1 standards effective 2025 obligate listed companies to report environmental metrics, intensifying recycled-content procurement.

Page last updated on: