Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.44 Billion |

| Market Size (2026) | USD 3.55 Billion |

| Market Size (2031) | USD 4.14 Billion |

| Growth Rate (2026 - 2031) | 3.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Packaging Industry Analysis by Mordor Intelligence

The packaging industry in Italy market size is expected to grow from USD 3.44 billion in 2025 to USD 3.55 billion in 2026 and is forecast to reach USD 4.14 billion by 2031 at 3.12% CAGR over 2026-2031. The measured expansion reflects Italy’s alignment with the European Union’s Packaging and Packaging Waste Regulation (PPWR) that entered force in February 2025, steering converters toward materials that meet mandatory recycled-content thresholds. Growth is amplified by a EUR 58.8 billion (USD 64.1 billion) domestic e-commerce sector that rose 4% in 2024, creating sustained demand for shipping-ready formats. Competitive strategies now prioritize mono-material designs, lightweighting, and AI-enhanced recycling, while opportunities emerge for suppliers that can bridge the North–South recycling-infrastructure gap and insulate customers from raw-material price volatility.

Key Report Takeaways

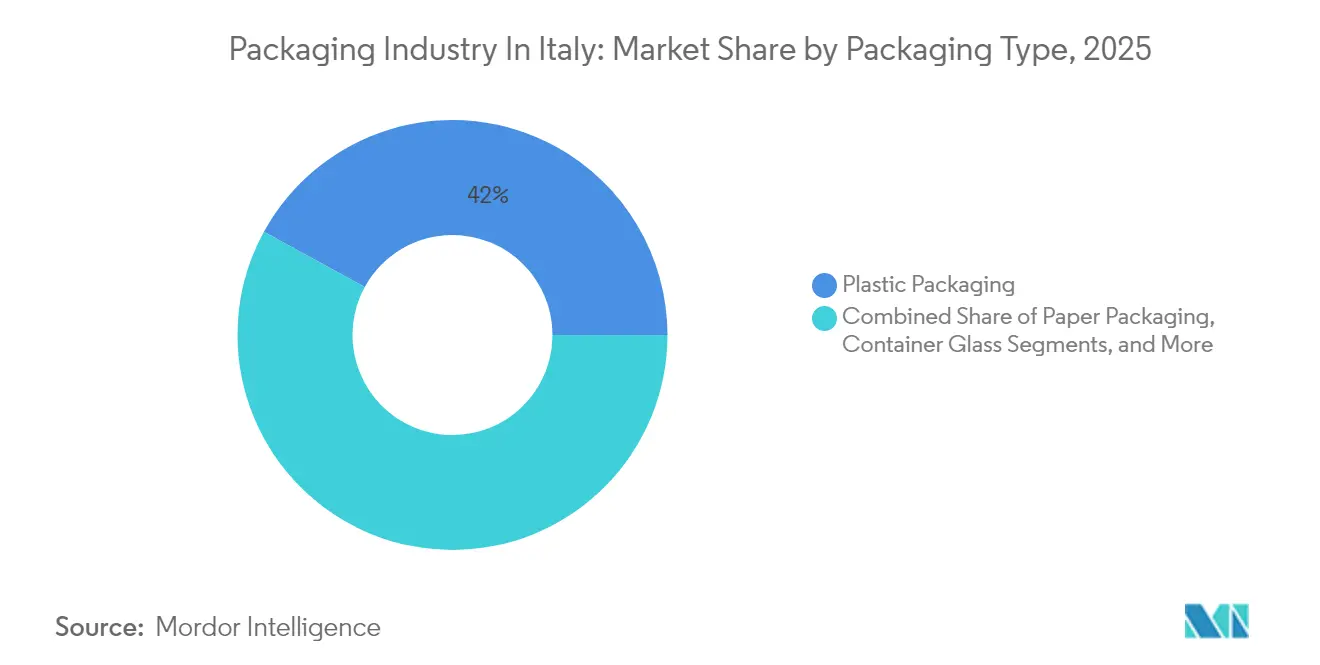

- By packaging type, plastic retained a 42.03% share of the packaging industry in Italy market in 2025, whereas paper is forecast to expand at a 4.55% CAGR through 2031.

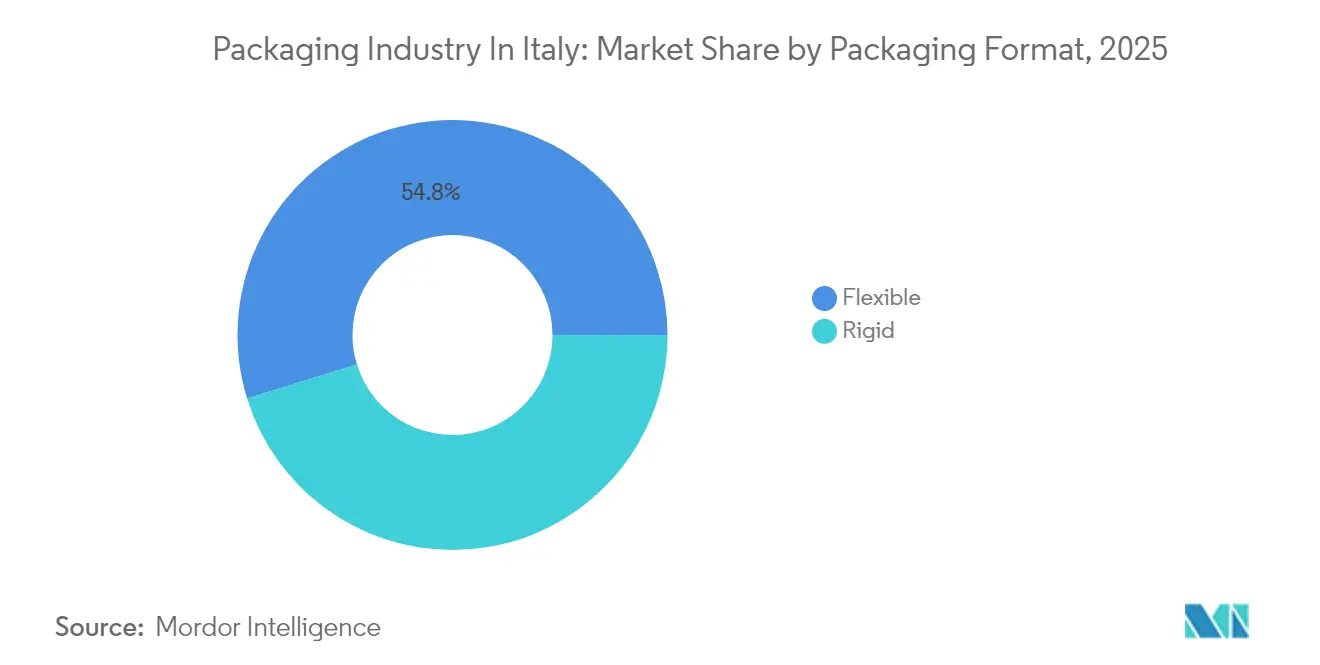

- By packaging format, flexible solutions accounted for 54.78% of the packaging industry in Italy market size in 2025 and are expected to grow at a 4.87% CAGR to 2031.

- By end-use industry, food led with 30.12% of the packaging industry in Italy market share in 2025, while e-commerce packaging shows the fastest 5.85% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Packaging Industry Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of lightweight and recyclable materials | +0.8% | Italy; spillover to EU markets | Medium term (2-4 years) |

| Surge in e-commerce parcel volumes | +1.2% | National; Northern Italy logistics hubs | Short term (≤ 2 years) |

| EU PPWR and EPR compliance accelerating sustainable packaging | +0.9% | Nationwide within EU framework | Long term (≥ 4 years) |

| AI-driven sorting and quality control in recycling facilities | +0.4% | Initially Northern Italy, expanding southward | Medium term (2-4 years) |

| Heat-pump manufacturing boom driving EPS demand | +0.6% | Northern industrial districts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Lightweight and Recyclable Materials

Converters accelerate material innovation as the EUR 0.45/kg plastic tax and brand-owner sustainability scorecards converge. Lavazza achieved 76% recyclable packaging in 2023 and targets full recyclability by 2025, illustrating food-sector leadership. Casa Optima commercialized 100% recyclable polypropylene packs in 2024, showcasing the technical viability of mono-material solutions. Investments in barrier coatings that remove multilayer complexity enable drop-in replacements without sacrificing shelf life. Retail penalties for non-recyclable formats now influence upstream product-development decisions, creating measurable competitive advantages for firms with R&D capabilities that shorten qualification cycles. As national retailers elevate recyclability thresholds annually, lightweight and recyclable designs become prerequisites for shelf access and export clearance.

Surge in E-commerce Parcel Volumes

Online retail worth EUR 58.8 billion (USD 64.1 billion) in 2024 has redefined shipment profiles, especially for food and grocery, which reached EUR 4.6 billion (USD 6.39 billion) with 8% year-over-year growth. Corrugated suppliers see spikes around Northern logistics hubs, prompting capacity expansions and just-in-time satellite plants that lower transit costs. Dimensional-weight pricing pushes right-sizing software, expandable mailers, and cushioning that tolerates two-way journeys under circular commerce models. Return-ready designs for electronics and apparel add new revenue lines for converters specializing in tear-strip and reseal features. These packaging requirements increasingly dictate upstream material choice, favoring lightweight paper and mono-polyolefin films that align cost, protection, and recyclability.

EU PPWR and EPR Compliance Accelerating Sustainable Packaging

Effective February 2025, the PPWR obliges companies to meet recycled-content floors and design-for-recycling targets verified under EN 13432 standards.[1]European Commission, “PPWR Implementation,” ec.europa.eu Italian brand owners already face higher EPR fees when specifications fall short, elevating the cost of non-compliance. Verallia’s 2024 EBITDA uptick to EUR 326 million (USD 384.20 million) partly stems from higher recycled glass content in response to the new rules. Early movers that exceed thresholds secure multi-year supply contracts as customers rush to prequalify packaging that will remain market-compliant through 2030. Regional disparities in infrastructure make compliance easier in the North, yet PNRR funding is earmarked to lift Southern recycling capacity above 70%, strengthening national supply chains over the forecast horizon.

AI-Driven Sorting and Quality Control in Recycling Facilities

A2A reported 95% sorting accuracy after rolling out Greyparrot vision systems in 2024, raising polypropylene recovery and lowering contamination below 2%.[2]A2A Group, “AI Sorting Deployment,” a2a.eu TOMRA’s GAINnext platform achieved 97% purity for food-grade PP streams, permitting closed-loop reuse that fulfills stringent EU food-contact rules. Northern plants piloting the technology recover investment within two years through higher bale prices and reduced landfill levies. Algorithms learning from packaging design features create feedback that informs converters on optimal color, label, and adhesive choices, ultimately closing the loop between design and recycling. Competitive advantages accrue to waste managers that can supply traceable, high-purity recyclate at contracted volumes during virgin-material price spikes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in virgin polymer and paper pulp prices | -0.7% | Italy; linked to global commodity markets | Short term (≤ 2 years) |

| Plastic packaging tax (EUR 0.45/kg) squeezing margins | -0.5% | National; regional variations | Medium term (2-4 years) |

| North–South disparities in recycling infrastructure | -0.3% | Primarily affecting Southern Italy | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Virgin Polymer and Paper Pulp Prices

Global petrochemical swings raised polymer quotes above five-year averages in 2024, while pulp costs held firm after Nordic supply disruptions. Versalis shuttered cracking units in Brindisi and Priolo, lifting import reliance and exposing converters to freight and FX risk. Smaller operators with limited hedging absorb immediate EBITDA erosion, triggering M&A as firms seek scale procurement power. Paper converters face certification ceilings that curb raw-fiber availability, reinforcing recycled-fiber investment but tying prices to virgin-pulp trajectories. Buyers now request indexed contracts or mixed-material packs to buffer volatility, occasionally delaying innovation rollouts until cost stability returns.

Plastic Packaging Tax Squeezing Converter Margins

Italy’s plastic tax, active since January 2023, levies EUR 0.45/kg on single-use plastics, instantly trimming margins on films, wraps, and pouches. Converters shift toward paper or ultra-thin mono-polypropylene yet incur extra capex for new machinery and qualification. Northern plants, benefiting from 80% recycling rates, partially offset costs via recycled content credit, while Southern peers pay higher net levies due to 60% recovery, widening regional cost gaps.[3]CONAI, “Recycling Statistics 2024-2025,” conai.orgBrands diversify supplier bases to maintain continuity, strengthening companies with cross-material portfolios. Ultimately, the tax accelerates lightweighting but compresses short-term profitability, especially for SMEs financed on thin operating cash flows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Paper Gains Ground Despite Plastic Dominance

Plastic retained a 42.03% share of the packaging industry in the Italian market in 2025, anchored by the barrier performance sought in food and personal-care categories. The segment’s expansion remains steady, though the packaging industry in the Italian market for paper alternatives is projected to grow at a 4.55% CAGR to 2031 on the back of e-commerce and PPWR-driven substitution.

Paper converters win orders from online retail, corrugated boxes, and molded-fiber containers exempt from the plastic tax. Hybrid innovations, such as water-based coatings that replace polyethylene liners, shorten the payback for brand owners seeking recyclable claims. Glass maintains premium niches in beverages and cosmetics; Verallia’s Italian division posted EUR 1.53 billion (USD 1.80 billion) H1 2024 revenue, aided by recycled-glass surcharges passed onto buyers. Metal cans, prized for infinite recyclability, benefit from consumer trust in shelf-stable food during geopolitical supply disruptions. Firms straddling multiple materials hedge policy risks while servicing customers migrating between substrates.

By Packaging Format: Flexible Solutions Drive Market Evolution

Flexible packs dominated with 54.78% share in 2025 and are forecast to grow at a robust 4.87% CAGR, underscoring the format’s coexistence of leadership and momentum. In volume terms, the packaging industry in the Italian market size for flexible applications outpaces rigid competitors as brands convert tubs and jars into stand-up pouches to reduce shipping weight.

Energy-price volatility strengthens the case for film-based formats that lower freight loads, particularly for household cleaners and condiments distributed via omnichannel networks. Rigid formats remain entrenched in glass bottles for wine and aluminum aerosols under stringent pressure standards, yet their growth trails flexible variants. Lavazza’s Tablì dispenser even sidesteps packaging, but most of its SKUs move toward mono-material films slated for 2025 recyclability targets. Dimensional-weight fees in parcel delivery reinforce flexible mailers equipped with gussets that expand during packing but ship flat inbound, illustrating how e-commerce redefines format economics.

By End-use Industry: E-commerce Reshapes Traditional Hierarchies

Food products accounted for 30.12% of the packaging industry in the Italian market in 2025, bolstered by Italy’s globally renowned processed-food and specialty-pasta sectors. Yet the e-commerce channel posts the fastest 5.85% CAGR through 2031 as Italian consumers migrate to online grocery and direct-to-consumer luxury exports.

Beverages sustain glass and aluminum demand as DOC-certified wine exports depend on perceived authenticity. Pharmaceutical packs enjoy recession-proof status, aided by EU serialization mandates that drive uptake of tamper-evident closures. Personal-care labels chase recyclable aesthetics; Guala Closures invested EUR 60 million to develop premium, recyclable whisky closures serving both on-trade and e-commerce gifting. Industrial users adopt tailored crates and EPS cushions aligned with heat-pump manufacturing clusters in the North, where safe transit of fragile compressors justifies higher unit costs.

Geography Analysis

Northern regions such as Lombardy, Veneto, and Emilia-Romagna host 70% of national packaging capacity and boast recycling rates above 80%, giving local converters a compliant feedstock loop. These industrial corridors link seamlessly with Central European highways, easing the export of corrugated and flexible rolls to Germany and France.

Southern Italy, while lagging at roughly 60% recycling, is set to receive PNRR-backed MRF upgrades, potentially injecting 1.2 million tonnes of recovered material annually by 2027. The gap creates arbitrage for converters locating near new facilities to secure recycled feedstock before Northern incumbents. Sardinia and Sicily leverage port access for Mediterranean exports, shipping canned tuna and specialty wines in Italian-made Glass.

Italy’s geographic mid-Mediterranean position positions the packaging industry in Italy market as a conduit to North African growth economies seeking EU-compliant packaging. EPS demand clusters around Northern heat-pump factories, consuming a third of the 155,000-tonne national EPS market and generating consistent orders for molded-foam boxes.

Competitive Landscape

The packaging industry in Italy market comprises multinationals such as Mondi, Sealed Air, and Verallia alongside domestic specialists like Carton Pack and Zignago Vetro. Capital-intensive glass and aluminum segments lean toward oligopoly, whereas flexibles and corrugated remain fragmented with family-owned firms under EUR 200 million (USD 235.71 million) turnover.

Sustainability credentials now decide tender outcomes; Mondi’s EUR 200 million (USD 235.71 million) Duino containerboard mill adds 420,000 tonnes of recycled capacity, winning e-commerce box contracts from fashion platforms. A2A’s AI-backed recyclate supply grants converters traceable PCR resin, differentiating their bids to FMCG giants.

Technology suppliers also shape rivalry: TOMRA’s 97% PP purity ensures compliance with food-contact loops, while IMA sells high-speed pouch lines to converters pivoting from rigid cups. SMEs seek niche insulation by offering bespoke design services or rapid tooling for seasonal SKUs, yet rising EPR fees may trigger horizontal consolidation as compliance costs climb toward EUR 150/tonne by 2026.

Italy Packaging Market Leaders

Tetra Pak International SA

International Paper Company

Mondi plc

Stora Enso Oyj

Smurfit WestRock

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The European Union PPWR came into force, setting recycled-content mandates and PFAS restrictions that overhaul Italian packaging specifications.

- January 2025: Mondi launched operations at its EUR 200 million Duino recycled containerboard mill with 420,000 tonnes.

- December 2024: A2A achieved 95% sorting accuracy after deploying Greyparrot AI across Italian facilities.

- November 2024: Verallia reported EUR 1.53 billion (USD 1.80 billion) revenue and EUR 326 million (USD 384.20 billion) EBITDA for H1 2024 on higher recycled-glass volumes.

Italy Packaging Industry Report Scope

Packaging provides a protective and informative covering to the product. It also keeps the product protected during handling, storage, and movement. Furthermore, covering provides useful information about the content of the package. The study tracks the demand for the packaging market through the revenue derived from sales of plastic, glass, paper, and metal packaging products. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The packaging industry in Italy is segmented by material (paper, plastic, metal, and glass), packaging type (rigid and flexible), and end-user industry (food, beverages, pharmaceuticals, and personal care). The market sizes and projections are provided in terms of value (USD) for all the mentioned segments.

By Packaging Type

| Plastic Packaging | By Type | Rigid Plastic Packaging | By Material Type | Polyethylene (PE) |

| Polypropylene (PP) | ||||

| Polyethylene Terephthalate (PET) | ||||

| Polyvinyl Chloride (PVC) | ||||

| Polystyrene (PS) and Expanded Polystyrene (EPS) | ||||

| Other Material Types | ||||

| By Product Type | Bottles and Jars | |||

| Caps and Closures | ||||

| Trays and Containers | ||||

| Other Product Types | ||||

| By End-use Industry | Food | |||

| Beverage | ||||

| Pharmaceutical | ||||

| Cosmetics and Personal Care | ||||

| Industrial | ||||

| Other End-use Industry | ||||

| Flexible Plastic Packaging | By Material Type | Polyethylene (PE) | ||

| Biaxially Oriented Polypropylene (BOPP) | ||||

| Cast Polypropylene (CPP) | ||||

| Other Material Types | ||||

| By Product Type | Pouches and Bags | |||

| Films and Wraps | ||||

| Other Product Types | ||||

| By End-use Industry | Food | |||

| Beverage | ||||

| Pharmaceutical | ||||

| Cosmetics and Personal Care | ||||

| Industrial | ||||

| Other End-use Industry | ||||

| By Product Type | Bottles and Jars | |||

| Pouches and Bags | ||||

| Bulk-Grade Products | ||||

| Other Product Types | ||||

| By End-use Industry | Food | |||

| Beverages | ||||

| Cosmetics and Personal Care | ||||

| Pharamceuticals | ||||

| Industrial | ||||

| Other End-use Industry | ||||

| Paper Packaging | By Product Type | Folding Carton | ||

| Corrugated Boxes | ||||

| Liquid Paperboard | ||||

| Other Product Type | ||||

| By End-use Industry | Food | |||

| Beverages | ||||

| E-commerce | ||||

| Other End-use Industry | ||||

| Container Glass | By Color | Green | ||

| Amber | ||||

| Flint | ||||

| Other Colors | ||||

| By End-use Industry | Food | |||

| Alcoholic | ||||

| Non-Alcoholic | ||||

| Personal Care and Cosmetics | ||||

| Pharmaceuticals (excluding Vials and Ampoules) | ||||

| Perfumery | ||||

| Metal Cans and Containers | By Material Type | Steel | ||

| Aluminum | ||||

| By Product Type | Cans | |||

| Drums and Barrels | ||||

| Caps and Closures | ||||

| Other Product Type | ||||

| By End-use Industry | Food | |||

| Beverage | ||||

| Chemicals and Petroleum | ||||

| Industrial | ||||

| Paints and coatings | ||||

| Other End-use Industry | ||||

By Packaging Format

| Flexible |

| Rigid |

By End-use Industry

| Food |

| Beverage |

| Pharmaceuticals and Healthcare |

| Personal Care and Cosmetics |

| Industrial |

| E-commerce |

| Other End-use Industry |

| By Packaging Type | Plastic Packaging | By Type | Rigid Plastic Packaging | By Material Type | Polyethylene (PE) |

| Polypropylene (PP) | |||||

| Polyethylene Terephthalate (PET) | |||||

| Polyvinyl Chloride (PVC) | |||||

| Polystyrene (PS) and Expanded Polystyrene (EPS) | |||||

| Other Material Types | |||||

| By Product Type | Bottles and Jars | ||||

| Caps and Closures | |||||

| Trays and Containers | |||||

| Other Product Types | |||||

| By End-use Industry | Food | ||||

| Beverage | |||||

| Pharmaceutical | |||||

| Cosmetics and Personal Care | |||||

| Industrial | |||||

| Other End-use Industry | |||||

| Flexible Plastic Packaging | By Material Type | Polyethylene (PE) | |||

| Biaxially Oriented Polypropylene (BOPP) | |||||

| Cast Polypropylene (CPP) | |||||

| Other Material Types | |||||

| By Product Type | Pouches and Bags | ||||

| Films and Wraps | |||||

| Other Product Types | |||||

| By End-use Industry | Food | ||||

| Beverage | |||||

| Pharmaceutical | |||||

| Cosmetics and Personal Care | |||||

| Industrial | |||||

| Other End-use Industry | |||||

| By Product Type | Bottles and Jars | ||||

| Pouches and Bags | |||||

| Bulk-Grade Products | |||||

| Other Product Types | |||||

| By End-use Industry | Food | ||||

| Beverages | |||||

| Cosmetics and Personal Care | |||||

| Pharamceuticals | |||||

| Industrial | |||||

| Other End-use Industry | |||||

| Paper Packaging | By Product Type | Folding Carton | |||

| Corrugated Boxes | |||||

| Liquid Paperboard | |||||

| Other Product Type | |||||

| By End-use Industry | Food | ||||

| Beverages | |||||

| E-commerce | |||||

| Other End-use Industry | |||||

| Container Glass | By Color | Green | |||

| Amber | |||||

| Flint | |||||

| Other Colors | |||||

| By End-use Industry | Food | ||||

| Alcoholic | |||||

| Non-Alcoholic | |||||

| Personal Care and Cosmetics | |||||

| Pharmaceuticals (excluding Vials and Ampoules) | |||||

| Perfumery | |||||

| Metal Cans and Containers | By Material Type | Steel | |||

| Aluminum | |||||

| By Product Type | Cans | ||||

| Drums and Barrels | |||||

| Caps and Closures | |||||

| Other Product Type | |||||

| By End-use Industry | Food | ||||

| Beverage | |||||

| Chemicals and Petroleum | |||||

| Industrial | |||||

| Paints and coatings | |||||

| Other End-use Industry | |||||

| By Packaging Format | Flexible | ||||

| Rigid | |||||

| By End-use Industry | Food | ||||

| Beverage | |||||

| Pharmaceuticals and Healthcare | |||||

| Personal Care and Cosmetics | |||||

| Industrial | |||||

| E-commerce | |||||

| Other End-use Industry | |||||

Key Questions Answered in the Report

How large is the packaging industry in Italy market today?

The packaging industry in Italy market size equals USD 3.55 billion in 2026 and is set to reach USD 4.14 billion by 2031.

What CAGR is expected for Italian packaging through 2031?

Forecasts call for a 3.12% CAGR between 2026 and 2031, driven by PPWR compliance and e-commerce growth.

Which packaging format grows fastest across Italian applications?

Flexible formats show the highest 4.87% CAGR, owing to lightweight designs that cut transport costs.

How is the PPWR affecting Italian converters?

The PPWR mandates recycled-content floors and design-for-recycling, pushing firms toward mono-material solutions and chemical-recycling partnerships.

Why is AI important in Italian recycling plants?

AI-based vision systems raise sorting accuracy above 95%, improving recyclate quality and lowering contamination fees for converters.

What role does e-commerce play in shaping packaging demand?

A EUR 58.8 billion e-commerce market fuels demand for right-sized corrugated boxes and protective flexibles suited to parcel delivery.

Page last updated on: