Content Authoring Tools Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.76 Billion |

| Market Size (2031) | USD 2.89 Billion |

| Growth Rate (2026 - 2031) | 10.39% CAGR |

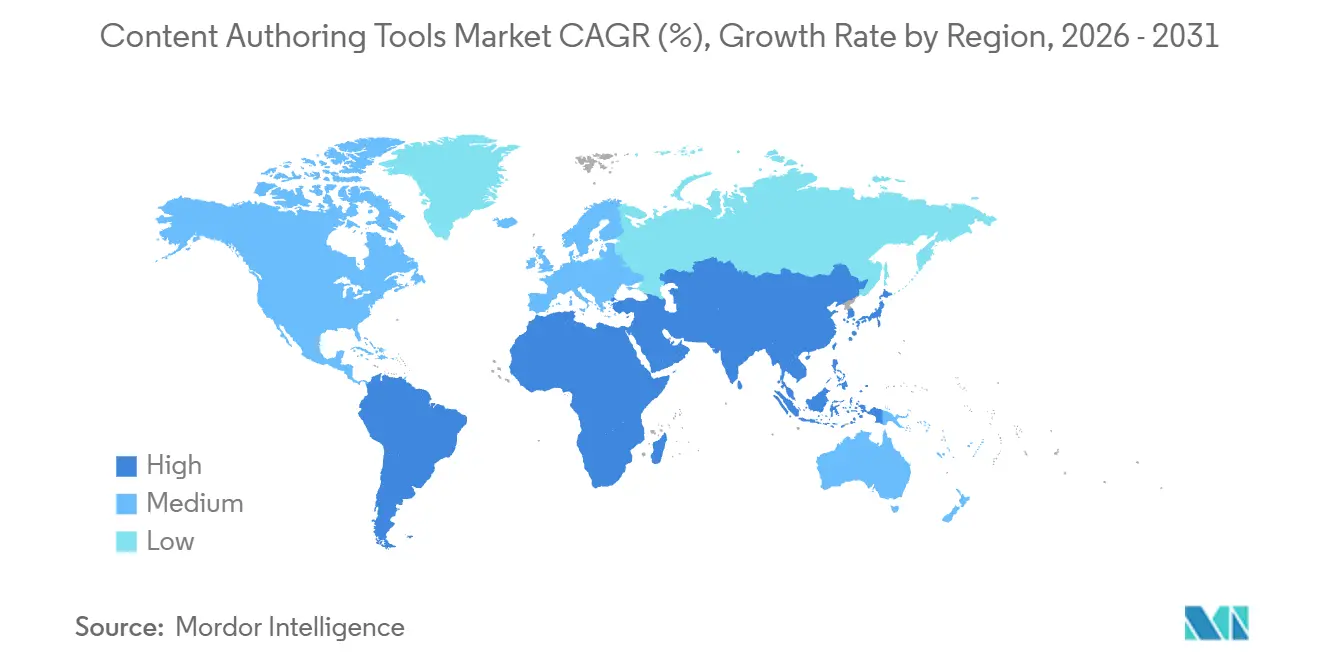

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Content Authoring Tools Market Analysis by Mordor Intelligence

The content authoring tools market size is projected to expand from USD 1.60 billion in 2025 and USD 1.76 billion in 2026 to USD 2.89 billion by 2031, registering a CAGR of 10.39% between 2026 and 2031. Widespread adoption of generative AI has shortened production cycles, enabling organizations to personalize digital assets at scale while reducing redundant licensing costs. Hybrid deployment models are now mainstream among regulated enterprises because they keep sensitive data on-premises yet enable cloud-scale collaboration. Demand for video-first learning and omnichannel marketing drives platform convergence, pushing vendors to bundle creation, analytics, and distribution within a single workspace. Competitive tactics increasingly revolve around ecosystem lock-in, with leading providers embedding adjacent functions such as SEO, digital asset management, and work management to discourage customer churn.

Key Report Takeaways

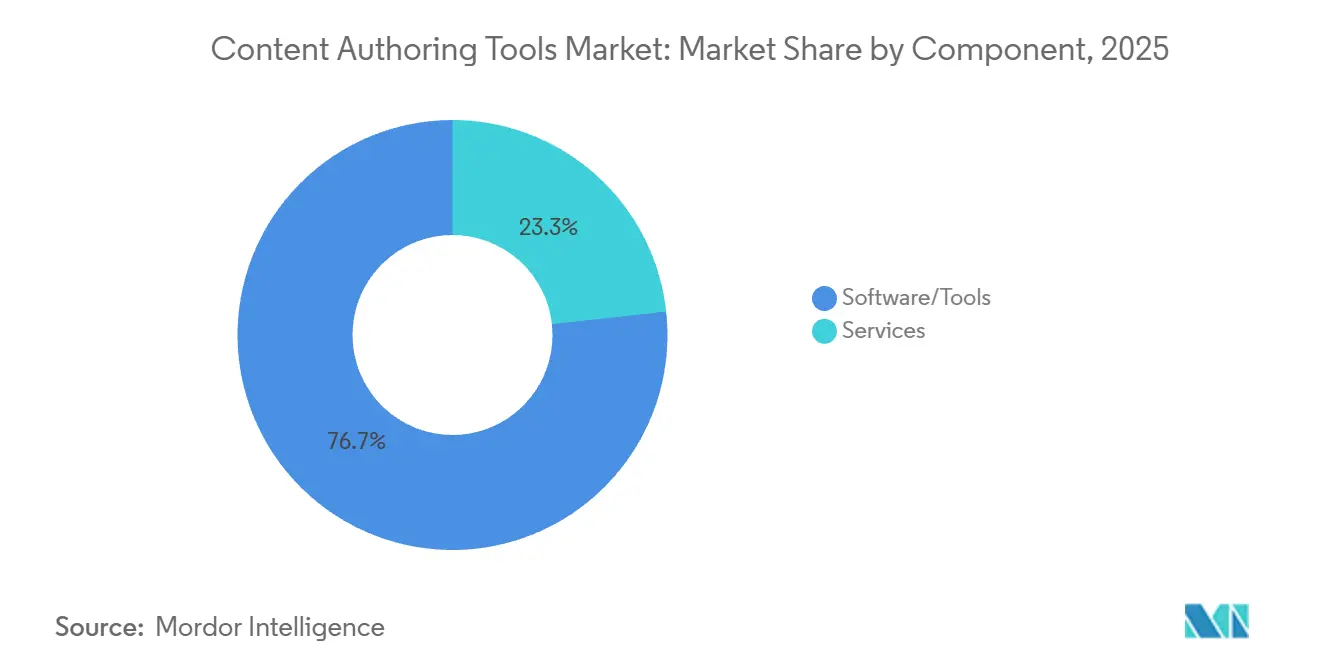

- By component, software and tools held 76.74% revenue share of the content authoring tools market in 2025, while services are advancing at an 11.48% CAGR through 2031.

- By deployment model, cloud deployments captured 54.62% of spending in 2025, and hybrid architectures are forecast to grow at an 11.92% CAGR to 2031.

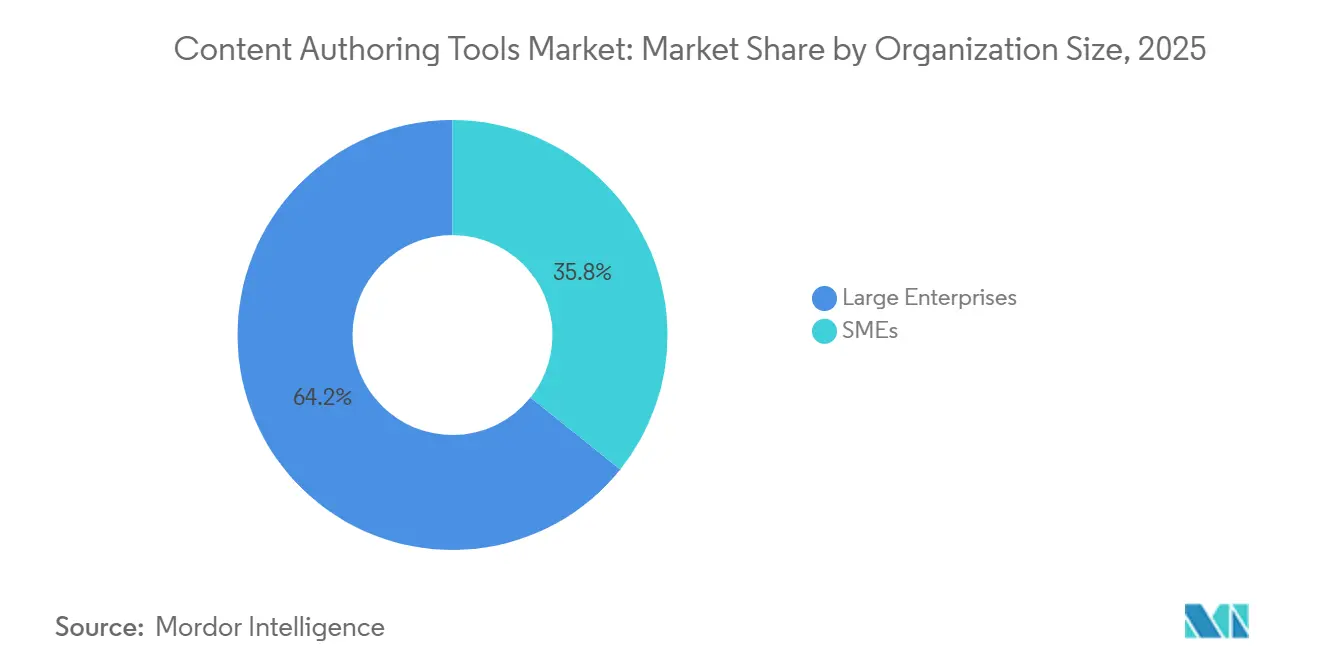

- By organization size, large enterprises represented 64.18% of 2025 spending, whereas SMEs are projected to rise at a 12.21% CAGR up to 2031.

- By end-user industry, e-learning and education accounted for 29.12% revenue of the content authoring tools market in 2025, and marketing and advertising agencies are set to register an 11.36% CAGR over 2026-2031.

- By geography, North America commanded 40.36% revenue in 2025, while Asia-Pacific is on track for a 12.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Content Authoring Tools Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generative AI-Powered Authoring Enhancements | +2.1% | Global, early uptake in North America and Europe | Medium term (2-4 years) |

| Growing Demand for Video-Based E-Learning Content | +1.8% | Global, strong in Asia-Pacific and North America | Short term (≤ 2 years) |

| Rapid Adoption of SaaS Content Suites Among SMEs | +1.5% | Global, faster in Asia-Pacific and South America | Medium term (2-4 years) |

| Expansion of Remote and Hybrid Workflows | +1.3% | Global | Long term (≥ 4 years) |

| Increasing Investment in Interactive Marketing Experiences | +1.1% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Emergence of Headless CMS Integrations for Omnichannel Delivery | +0.9% | North America and Europe, rising in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Generative AI-Powered Authoring Enhancements

Adobe embedded the Gemini, Veo, and Imagen models in Creative Cloud in October 2025, enabling text-to-video generation and intelligent tagging inside existing workflows. Microsoft deployed Copilot across Office 365 in 2025, automating slide decks, document summaries, and emails, which pilot programs reported cut production time by 30%.[1]Microsoft, “Copilot Across Office 365 Reduces Authoring Time,” microsoft.com Canva absorbed Leonardo.ai, MangoAI, Cavalry, Simtheory, and Ortto between 2024 and 2026, translating AI breakthroughs into a 40% upswing in premium subscribers by early 2026. As a result, platforms that lag in credible generative AI risk price pressure when customers consolidate vendors. The compliance landscape remains fluid, so vendors that deliver content provenance tools and granular model settings gain an edge with regulated buyers.

Growing Demand for Video-Based E-Learning Content

Corporate learning teams increasingly choose video because completion rates run 75% higher than text-only modules, according to several LMS providers. X-Pilot raised USD 18 million in January 2024 and tripled enterprise licenses within 18 months after sponsors cited 50% faster course development. Synthesia crossed 1,000 enterprise customers by 2025, including half of the Fortune 100, thanks to multilingual AI avatars that replace expensive studio shoots.[2]Synthesia, “Enterprise Customer Milestone,” synthesia.io The pivot pressures legacy e-learning authoring vendors to integrate native video or risk displacement by specialist platforms. Balancing speed with script quality remains critical because poorly produced AI video can erode learner trust.

Rapid Adoption of SaaS Content Suites Among SMEs

Canva surpassed 265 million users by early 2026, driven by SME teams that prefer USD 12.99 per user monthly pricing over perpetual licenses. Notion’s valuation hit USD 10 billion in 2025 as it expanded from note-taking into a unified content workspace appealing to resource-constrained firms. Subscription models convert capital outlay into operating expenses, but also spark subscription fatigue because the average business now juggles 130 SaaS tools. Vendors that bundle modular features and expose open APIs are better positioned to withstand consolidation cycles.

Expansion of Remote and Hybrid Workflows

Atlassian brought Confluence whiteboards to general availability in 2025, prompting a 25% increase in paid seats among existing clients by enabling remote teams to sketch and co-author documents in real time. Figma’s USD 1.056 billion fiscal-2025 revenue, up 41% year over year, underscored the strategic migration toward live prototypes that engineering can inspect centrally. Organizations that invested in cloud collaboration during 2020-2021 now optimize those investments, solidifying cloud authoring as the default architecture. Legacy tools that depend on VPNs face attrition as remote workers expect browser-native, low-latency editing everywhere.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership for Enterprise-Grade Platforms | -0.8% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Data-Privacy and IP Leakage Concerns in Cloud Workflows | -0.7% | Europe, North America, Asia-Pacific | Short term (≤ 2 years) |

| Skills Gap in Rich-Media Template Development | -0.5% | Global, sharper in emerging markets | Long term (≥ 4 years) |

| Vendor Lock-In Due to Proprietary File Formats | -0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership for Enterprise-Grade Platforms

Annual licensing for Adobe Experience Manager often reaches USD 200,000 to USD 500,000, with professional services adding comparable expense, pushing budgets 40% to 60% above initial estimates. Sitecore deployments can exceed USD 1 million in year one once infrastructure and customization are considered. As vendors retire perpetual licenses, subscription renewals can outpace budget growth, prompting buyers to demand transparent calculators and ROI metrics tied to engagement lift.

Data-Privacy and IP Leakage Concerns in Cloud Workflows

GDPR requires E.U. data to remain in the region, yet multi-tenant SaaS platforms routinely replicate files for latency gains, exposing enterprises to penalties. Adobe’s December 2025 ChatGPT integration sparked questions about whether prompts fuel model retraining, prompting Adobe to publish stricter contractual assurances. Industries such as defense often insist on hybrid or on-premises deployments, so vendors offering regional hosting and audit trails earn preferential evaluation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Expand as Deployments Grow Complex

In 2025, software and tools controlled a 76.74% content authoring tools market share, yet professional and managed services are forecast to outpace the overall content authoring tools market at an 11.48% CAGR through 2031. Services demand has accelerated because enterprises seldom possess the specialized skills required to integrate headless CMS architectures with analytics and martech stacks. High-touch onboarding for Adobe Experience Manager or Sitecore typically spans 6-12 months, covering API integrations, role-based access configuration, and user training, driving increasing reliance on certified integrators.

Managed services appeal to SMEs that lack IT staff by delivering turnkey environments with automated backups, uptime monitoring, and template libraries. North America and Europe account for most service spending, whereas Asia-Pacific buyers still emphasize lower-cost licenses and self-service documentation. Vendors that treat implementation as a core revenue stream rather than an adjunct will capture recurring revenue and mitigate churn.

By Deployment Model: Hybrid Gains Momentum on Security and Flexibility

Cloud installations retained a 54.62% share of the content authoring tools market in 2025, as SMEs prefer instant provisioning and no infrastructure overhead. Hybrid configurations, however, are advancing at an 11.92% CAGR as large enterprises adopt architectures that keep sensitive data on-premises while enabling real-time collaborative editing in the cloud. Microsoft allows selective synchronization between Office 365 and on-premises SharePoint, enabling enterprises to maintain governance without sacrificing usability.

Regulatory drivers, notably GDPR and emerging AI governance rules, reinforce hybrid adoption because regional hosting satisfies cross-border data mandates. Vendors that unify monitoring, identity management, and version control across cloud and data-center sites reduce operational complexity. Strong hybrid orchestration has become a decisive factor in RFP evaluations for contracts exceeding USD 500,000.

By Organization Size: SME Growth Fueled by No-Code Interfaces

Large enterprises commanded 64.18% of 2025 spending, yet SMEs are the growth engine, expanding at a 12.21% CAGR as no-code authoring democratizes content creation. Canva’s drag-and-drop layouts and AI-driven design suggestions feed a USD 4 billion annualized revenue run rate in early 2026 by removing the need for specialist designers. Apple's January 2026 launch of Creator Studio, a USD 12.99-per-month subscription that bundles video editing, graphic design, and web publishing, targets this segment explicitly.[3]Apple Newsroom, “Creator Studio Launch,” apple.com

Small and medium-sized enterprises value predictable operating costs and rapid onboarding, but as subscription counts rise, vendor consolidation is likely. Platforms offering freemium tiers, modular billing, and open Application programming interfaces retain customer loyalty when budgets tighten. Enterprise buyers, by contrast, still prioritize audit trails, custom roles, and deep martech integrations, sustaining premium license tiers.

By End-User Industry: Agencies Accelerate Interactive Content Investment

E-learning and education accounted for 29.12% of the 2025 content authoring tools market, driven by corporate reskilling agendas and academic digitization. Marketing and advertising agencies lead growth with an 11.36% CAGR through 2031 as brands pursue interactive quizzes, calculators, and data visualizations that outperform static landing pages. Ceros reported 60% revenue growth in 2025 by supplying no-code interactive content for agency campaigns.

Video-centric platforms such as Kaltura deepened marketing appeal by acquiring PathFactory in March 2026 to embed personalization and analytics.[4]Kaltura Press Release, “Kaltura Acquires PathFactory,” corp.kaltura.com Healthcare and manufacturing are steady adopters, leveraging authoring suites for patient education and technical documentation, respectively. Government agencies modernize slowly due to procurement rules, but are nudged forward by mandates for mobile-first public services.

Geography Analysis

North America controlled 40.36% of 2025 revenue, aided by deep SaaS penetration and early enterprise experimentation with AI authoring. Adobe’s USD 1.9 billion Semrush acquisition in April 2026 cements Silicon Valley’s leadership by connecting SEO analytics directly to Creative Cloud workflows. U.S. state privacy statutes such as California’s CPRA spur hybrid adoption, while Canada benefits from bilingual content mandates that expand authoring volume. Market maturity forces vendors to focus on upsell and cross-sell because net-new logo growth is limited.

Asia-Pacific is the fastest-expanding region, set to log a 12.67% CAGR through 2031. India’s Digital India initiative allocated USD 1.2 billion for digital infrastructure in 2025, spurring domestic cloud adoption.[5]Government of India, Ministry of Electronics and Information Technology, “Digital India Initiative Budget,” digitalindia.gov.in China’s preference for domestic software following tightened data sovereignty rules benefits local cloud vendors. Southeast Asia’s digital economy reached USD 218 billion gross merchandise value in 2025, energizing demand for omnichannel content tools. Australia and New Zealand mirror North American adoption patterns, emphasizing cloud orchestration and compliance certifications.

Europe’s tightly enforced GDPR drives preference for hybrid deployments that restrict cross-border data flows. Germany prioritizes technical documentation linked to manufacturing lifecycles, while the United Kingdom remains an innovation hub despite post-Brexit regulatory divergence. Southern Europe shows slower adoption due to legacy systems and budget constraints. The Middle East and Africa remain emerging opportunities, with smart-city initiatives in Saudi Arabia and multilingual education programs in South Africa shaping early demand for collaborative authoring.

Competitive Landscape

The top five vendors, Adobe, Microsoft, Canva, Google, and Atlassian, held a moderate content authoring tools market share in 2025, leaving considerable room for niche challengers. Incumbents defend their share by integrating AI features and bundling adjacent capabilities such as analytics and work management, raising switching costs. Adobe’s Semrush purchase embeds SEO insights inside Creative Cloud, positioning the suite against HubSpot and Salesforce for marketing operations.

Challengers grow via freemium land-and-expand tactics, demonstrated by Canva’s conversion of free users to paid plans at rates above 10%. Headless CMS specialists such as Contentful and Contentstack win enterprises pursuing composable technology stacks. Generative AI remains the primary battleground; however, buyers are wary of intellectual-property leakage, pressuring vendors to offer model transparency. Compliance certifications such as ISO 27001 and SOC 2 have become default requirements for enterprise procurements.

White-space opportunities cluster around three axes: vertical-specific workflows (healthcare patient education, manufacturing technical documentation, government plain-language compliance), emerging formats (3D content for metaverse applications, interactive AR/VR experiences), and underserved geographies (localized platforms for Southeast Asia, Africa, and South America). Headless CMS vendors like Contentful, Sanity, and Contentstack are disrupting traditional monolithic architectures by enabling omnichannel content delivery through API-first designs, a shift that resonates with enterprises pursuing composable technology stacks.

Content Authoring Tools Industry Leaders

Adobe Inc.

Microsoft Corporation

Canva Pty Ltd

Squarespace, Inc.

Quark Software, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Adobe completed its USD 1.9 billion acquisition of Semrush, integrating SEO analytics into Creative Cloud workflows.

- April 2026: Canva acquired Simtheory and Ortto, following February 2026 pick-ups of Cavalry and MangoAI, to deepen video generation and marketing automation.

- April 2026: Adobe launched CX Enterprise, combining Experience Manager, Workfront, and Marketo with pre-built integrations to halve deployment time.

- March 2026: Adobe and NVIDIA partnered to embed GPU acceleration for real-time 3D and video rendering in Creative Cloud.

Global Content Authoring Tools Market Report Scope

The content authoring tools market refers to the revenue generated from software platforms and associated services used to create, design, edit, and publish digital content for various use cases, including e-learning modules, marketing assets, documentation, and multimedia experiences. These tools enable users to develop content in formats such as text, video, interactive presentations, simulations, and web-based experiences without requiring advanced programming skills.

The Content Authoring Tools Market Report is Segmented by Component (Software/Tools, and Services), Deployment Model (On-Premises, Cloud, and Hybrid), Organization Size (SMEs, and Large Enterprises), End-User Industry (Media and Entertainment, E-Learning and Education, Marketing and Advertising Agencies, Government and Public Sector, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software/Tools |

| Services |

| On-Premises |

| Cloud |

| Hybrid |

| SMEs |

| Large Enterprises |

| Media and Entertainment |

| E-Learning and Education |

| Marketing and Advertising Agencies |

| Government and Public Sector |

| Others End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Component | Software/Tools | |

| Services | ||

| By Deployment Model | On-Premises | |

| Cloud | ||

| Hybrid | ||

| By Organization Size | SMEs | |

| Large Enterprises | ||

| By End-User Industry | Media and Entertainment | |

| E-Learning and Education | ||

| Marketing and Advertising Agencies | ||

| Government and Public Sector | ||

| Others End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the content authoring tools market today?

The content authoring tools market size reached USD 1.76 billion in 2026 and is forecast to climb to USD 2.89 billion by 2031, according to Mordor Intelligence.

What is the projected growth rate through 2031?

The market is expected to grow at a 10.39% CAGR between 2026 and 2031, with Asia-Pacific advancing the fastest.

Which component segment is growing the quickest?

Services are expanding at an 11.48% CAGR as enterprises seek integration, customization, and training support, per Mordor Intelligence.

Which end-user vertical will outpace others?

Marketing and advertising agencies are set to post an 11.36% CAGR to 2031, the highest among verticals, driven by interactive content demand.

What deployment model will enterprises prefer?

Hybrid architectures are forecast to increase at an 11.92% CAGR because they balance on-premises security with cloud scalability.

Page last updated on: