Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Mobile Content Management Market Report Segments the Industry Into Solution (Software, and Services), Deployment (Cloud, On Premise), Organization Type (Large Enterprises, and Small and Medium Enterprises), End User Industry (BFSI, IT and Telecom, Retail, Healthcare, Education, Media and Entertainment, Government, and Others), and Geography.

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

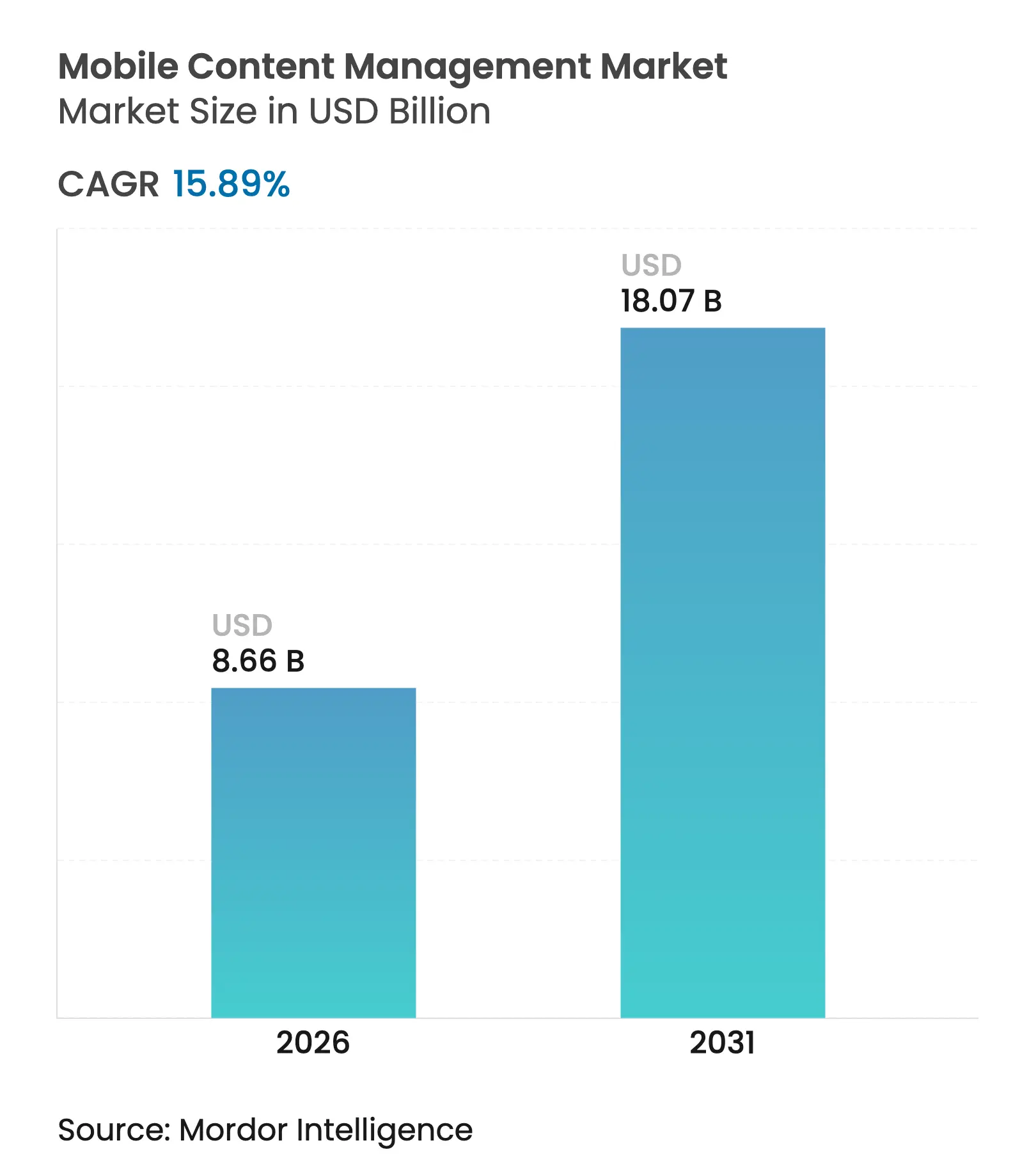

| Market Size (2026) | USD 8.66 Billion |

| Market Size (2031) | USD 18.07 Billion |

| Growth Rate (2026 - 2031) | 15.89 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The mobile content management market size was valued at USD 7.47 billion in 2025 and estimated to grow from USD 8.66 billion in 2026 to reach USD 18.07 billion by 2031, at a CAGR of 15.89% during the forecast period (2026-2031). Enterprises continue to prioritize unified endpoint oversight as hybrid work arrangements become permanent, with bring-your-own-device (BYOD) policies intersecting with strict audit mandates that require secure yet friction-free content access. Cloud-first strategies gain momentum because artificial intelligence (AI) workloads demand elastic infrastructure, while governance frameworks such as SOX, GDPR and HIPAA mandate continuous monitoring. Competitive dynamics pivot on cloud-native and AI-powered entrants that challenge established enterprise mobility vendors. Headwinds persist in the form of data-breach anxiety, legacy system integration complexity and rising data-center energy costs, prompting many organizations to adopt managed services for operational continuity.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

BYOD acceleration

across regulated verticals

BYOD acceleration

across regulated verticals

| +2.8% | North America and Europe | Medium term (2-4 years) |

(~) % Impact on

CAGR Forecast

:

+2.8%

|

Geographic

Relevance

:

North America and

Europe

|

Impact Timeline

:

Medium term (2-4

years)

|

Cloud-first

enterprise content strategies

Cloud-first

enterprise content strategies

| +3.2% | North America and Asia-Pacific | Long term (≥ 4 years) | |||

Remote and hybrid

work normalized post-2024

Remote and hybrid

work normalized post-2024

| +2.1% | Developed markets | Short term (≤ 2 years) | |||

Audit and governance

mandates

Audit and governance

mandates

| +2.4% | North America and European Union | Long term (≥ 4 years) | |||

Gen-AI

auto-classification improves ROI

Gen-AI

auto-classification improves ROI

| +1.9% | Early adopters in North America and Europe | Medium term (2-4 years) | |||

ESG reporting needs

traceable content chains

ESG reporting needs

traceable content chains

| +1.1% | European Union leading | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

BYOD Acceleration Across Regulated Verticals

Financial institutions now view employee-owned devices as productivity assets rather than security liabilities. American National Bank of Texas deployed Hyland’s OnBase cloud platform to automate check holds and achieve Regulation CC compliance while enabling staff to work from personal smartphones[1]Hyland Software, “American National Bank of Texas Automates Check Holds,” hyland.com. Healthcare providers face similar imperatives because telehealth accelerates mobile data flows that must be secured under HIPAA. This convergence forces organizations to adopt solutions that balance granular access controls with seamless user experiences. The result is sustained demand within the mobile content management market as firms seek unified platforms that align security frameworks with workforce mobility requirements.

Cloud-First Enterprise Content Strategies

Enterprises increasingly prioritize cloud-native repositories that scale with AI augmentation. Roche applied millions of AI-generated labels to content in Google Drive, demonstrating rapid classification and policy enforcement impossible in legacy on-premise systems[2]Google Workspace Blog, “Roche Scales AI-Driven Labels in Drive,” google.com. Elastic storage combined with automated governance reduces administrative overhead and accelerates collaboration. As infrastructure modernizes, vendors integrate real-time analytics for proactive risk detection, reinforcing strategic interest in cloud-based offerings across the mobile content management market.

Audit and Governance Mandates

Updated GDPR provisions released in 2025 elevate consent management and breach notification obligations, compelling continuous monitoring rather than periodic audits. Warba Bank digitized branch workflows with OpenText Extended ECM to maintain full audit trails that satisfy KYC and anti-money-laundering requirements while shortening customer onboarding times. Similar imperatives extend to SOX in financial services and HIPAA in healthcare, ensuring that regulatory frameworks remain a primary catalyst for solution deployment across the mobile content management market.

Gen-AI Auto-Classification Improves ROI

High-volume unstructured data previously required extensive manual tagging. Netflix operationalized AI-driven content recommendations that dynamically personalize user experiences and cut churn rates, a model now mirrored in enterprise document ecosystems[3]Netflix Technology Blog, “Personalized Recommendations with Machine Learning,” netflixtechblog.com. Automated classification curtails labor costs, enforces policy consistency and surfaces actionable insights. Adoption of these capabilities amplifies the value proposition of advanced platforms within the mobile content management market while setting new benchmarks for return on investment.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Persistent

data-breach concerns

Persistent

data-breach concerns

| -1.8% | Regulated industries worldwide | Short term (≤ 2 years) |

(~) % Impact on

CAGR Forecast

:

-1.8%

|

Geographic

Relevance

:

Regulated industries

worldwide

|

Impact Timeline

:

Short term (≤ 2

years)

|

Integration

complexity with legacy ECM/ERP

Integration

complexity with legacy ECM/ERP

| -2.1% | North America and Europe | Medium term (2-4 years) | |||

Rising energy cost

of hyperscale storage

Rising energy cost

of hyperscale storage

| -1.2% | Data-center intensive regions | Long term (≥ 4 years) | |||

Open-source headless

CMS cannibalization

Open-source headless

CMS cannibalization

| -1.4% | Cost-sensitive markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Persistent Data-Breach Concerns

A security defect at Mobile Guardian enabled remote device wipes on 13,000 endpoints, illustrating how compromised mobility controls can cause operational disruption and reputational damage. Such incidents highlight residual vulnerabilities that deter risk-averse enterprises from rapid adoption. Vendors now emphasize zero-trust architecture, threat analytics and continuous patching, yet apprehension continues to subtract incremental growth from the mobile content management market.

Integration Complexity with Legacy ECM/ERP

Many organizations still run decade-old ECM and ERP stacks that were never architected for cloud or mobile channels. Middleware investments, data-format normalization and phased migrations are required to avoid workflow interruptions. Mold-based migration frameworks outline stepwise approaches but demand specialized skills and protracted timelines, creating budgetary strain and delaying enterprise rollouts. Resulting complexity remains a pronounced inhibitor to broader penetration of the mobile content management market.

By Solution: Services Accelerate Despite Software Dominance

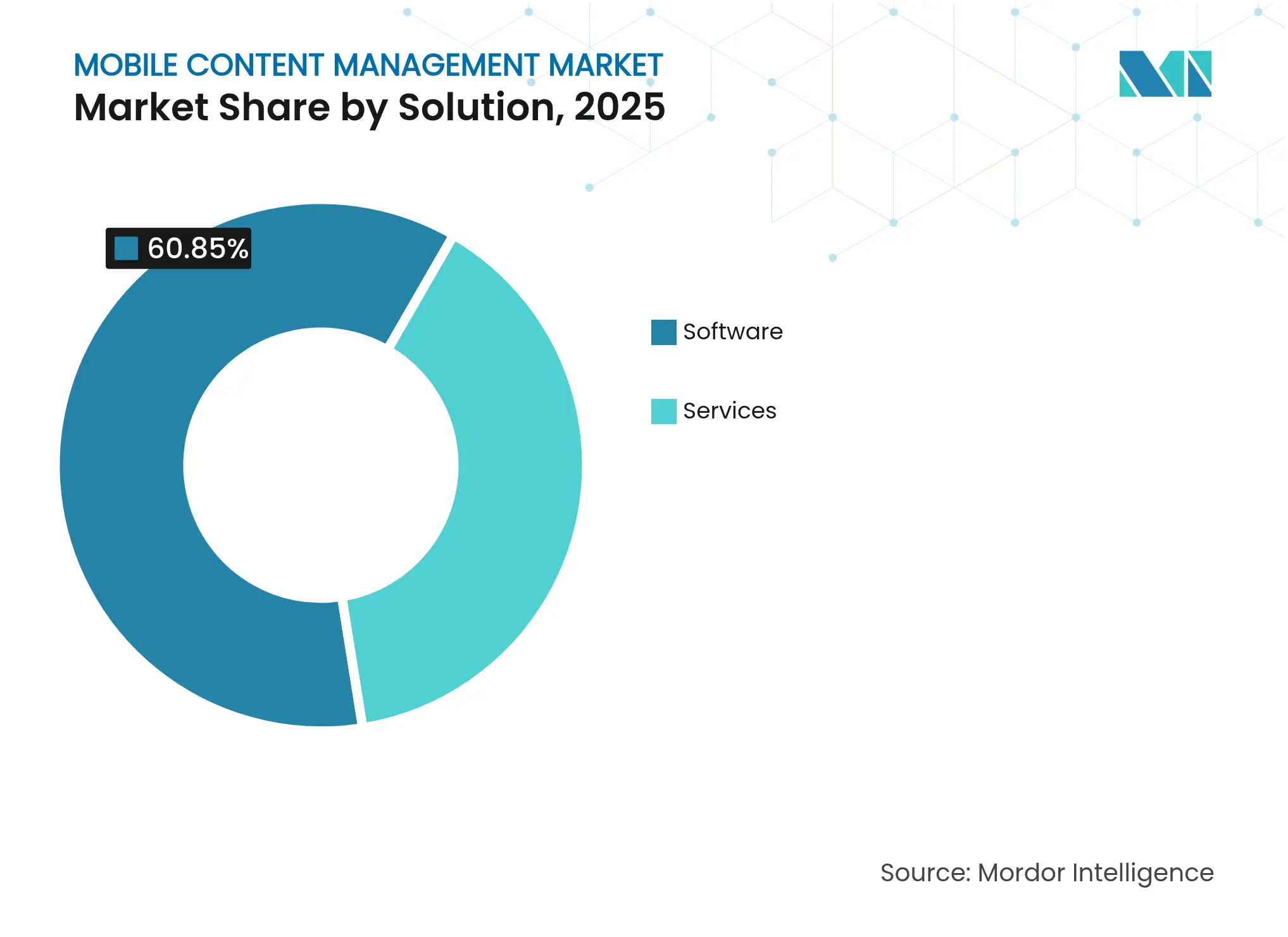

Software solutions generated the largest portion of revenue in 2025, securing 60.85% of the mobile content management market share as enterprises opted for integrated platforms combining device, application and content functions. However, services posted an impressive 14.05% CAGR that outpaced software growth, signalling rising demand for implementation, customization and ongoing optimization. The mobile content management market size attached to service engagements is projected to expand steadily as organizations outsource compliance auditing, AI training and system fine-tuning.

Integrated enterprise mobility suites remain the primary avenue for large deployments because they streamline vendor relationships and reduce management overhead. Stand-alone products retain niches where specialized workflows dominate but confront mounting pressure from bundled alternatives. Service providers gain traction by packaging regulatory frameworks and industry templates that accelerate return on investment, further reinforcing a services-led momentum across the mobile content management market.

Note: Segment shares of all individual segments available upon report purchase

By Deployment: Cloud Transformation Accelerates Infrastructure Modernization

On-premise environments held 52.80% of the mobile content management market size in 2025, reflecting legacy investments and data-sovereignty rules within finance and government. Cloud offerings, however, recorded an 17.9% CAGR, drawing momentum from scalable AI toolsets and global collaboration needs. Public cloud dominates early transitions, while private and hybrid models serve organizations that must localize sensitive datasets.

The shift underscores recognition that cloud-native architectures deliver features such as real-time content analytics, automated governance and rapid disaster recovery. Vendors report shorter implementation cycles and lower total cost of ownership when customers migrate workloads, prompting sustained adoption curves. Potential obstacles remain in cross-border compliance, but the trajectory signals that the mobile content management market will continue its pivot toward flexible cloud deployments.

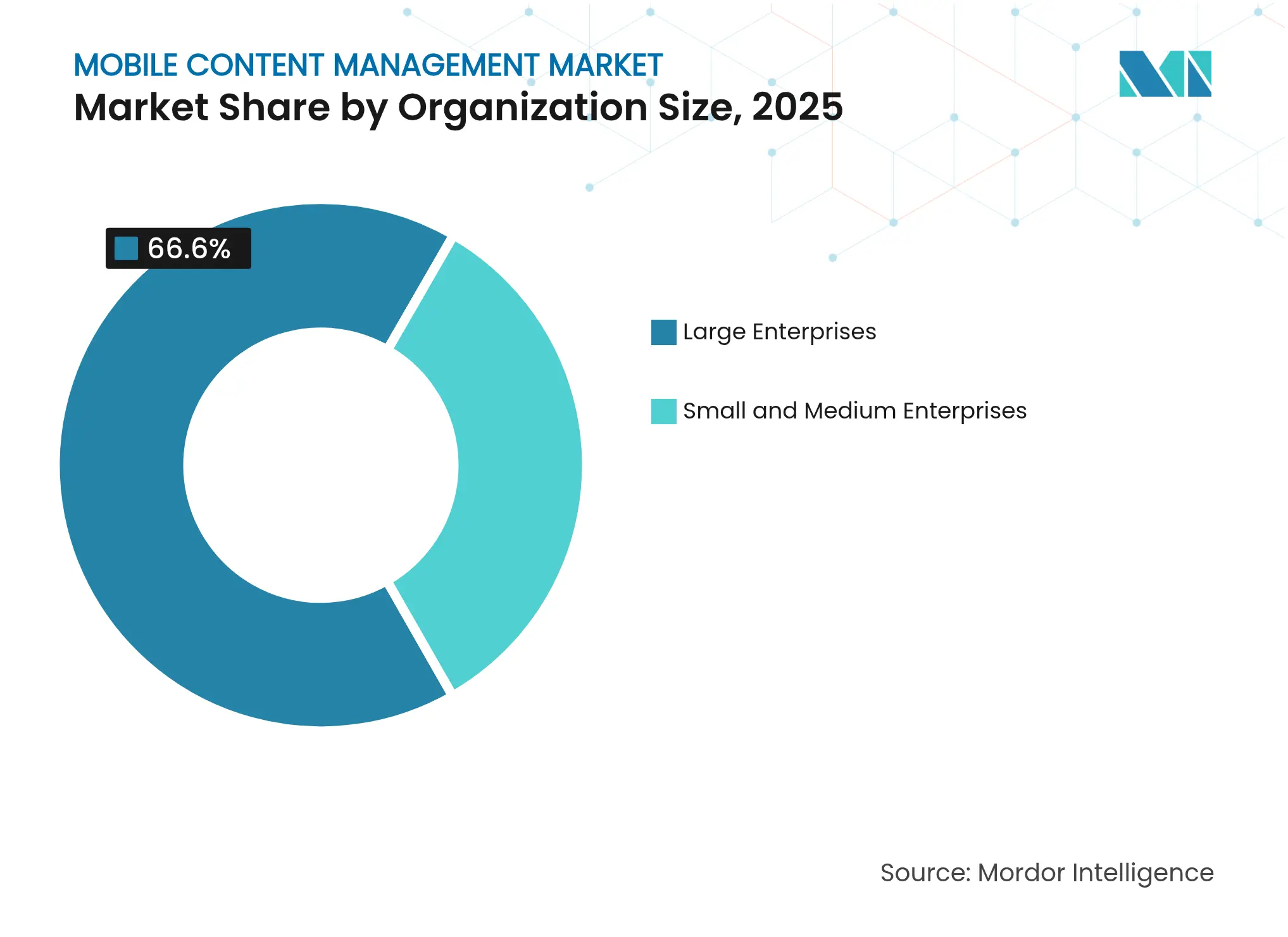

By Organization Size: SME Adoption Democratizes Enterprise Capabilities

Large enterprises collectively accounted for 66.60% of revenue yet face slower unit growth as expansion saturates. Their complex footprints require advanced customization, dedicated support and multi-layer security, characteristics well matched by leading platforms. In contrast, small and medium enterprises generated the fastest expansion, recording a 15.2% CAGR. Subscription pricing and no-code configuration now permit SMEs to deploy features once reserved for global corporations, broadening the addressable base of the mobile content management market.

Cloud delivery eliminates hardware procurement and accelerates rollout, while intuitive dashboards reduce the learning curve. Vendors targeting SMEs introduce preconfigured compliance packs and industry-specific templates, compressing time to value. These dynamics enable widespread democratization and reinforce volume growth within the mobile content management market.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Healthcare Growth Outpaces Financial Services Leadership

BFSI institutions maintained leadership with a 24.55% share in 2025 due to stringent documentation and audit requirements that mandate complete chain-of-custody capabilities. The segment relies on encrypted repositories, granular role-based access and tamper-evident audit trails that integrated suites deliver. Nonetheless, healthcare is forecast to post the strongest trajectory at 14.3% CAGR. Mobile telehealth sessions, remote diagnostics and electronic health records create continuous content flows that require HIPAA-compliant management.

The Rochelle Center adopted AT&T connectivity and IBM MaaS360 to protect personal health data while digitizing care documentation, demonstrating operational efficiency gains and regulatory adherence in one deployment. Similar initiatives underscore how patient-centric models depend on secure mobile channels, propelling healthcare demand across the mobile content management market.

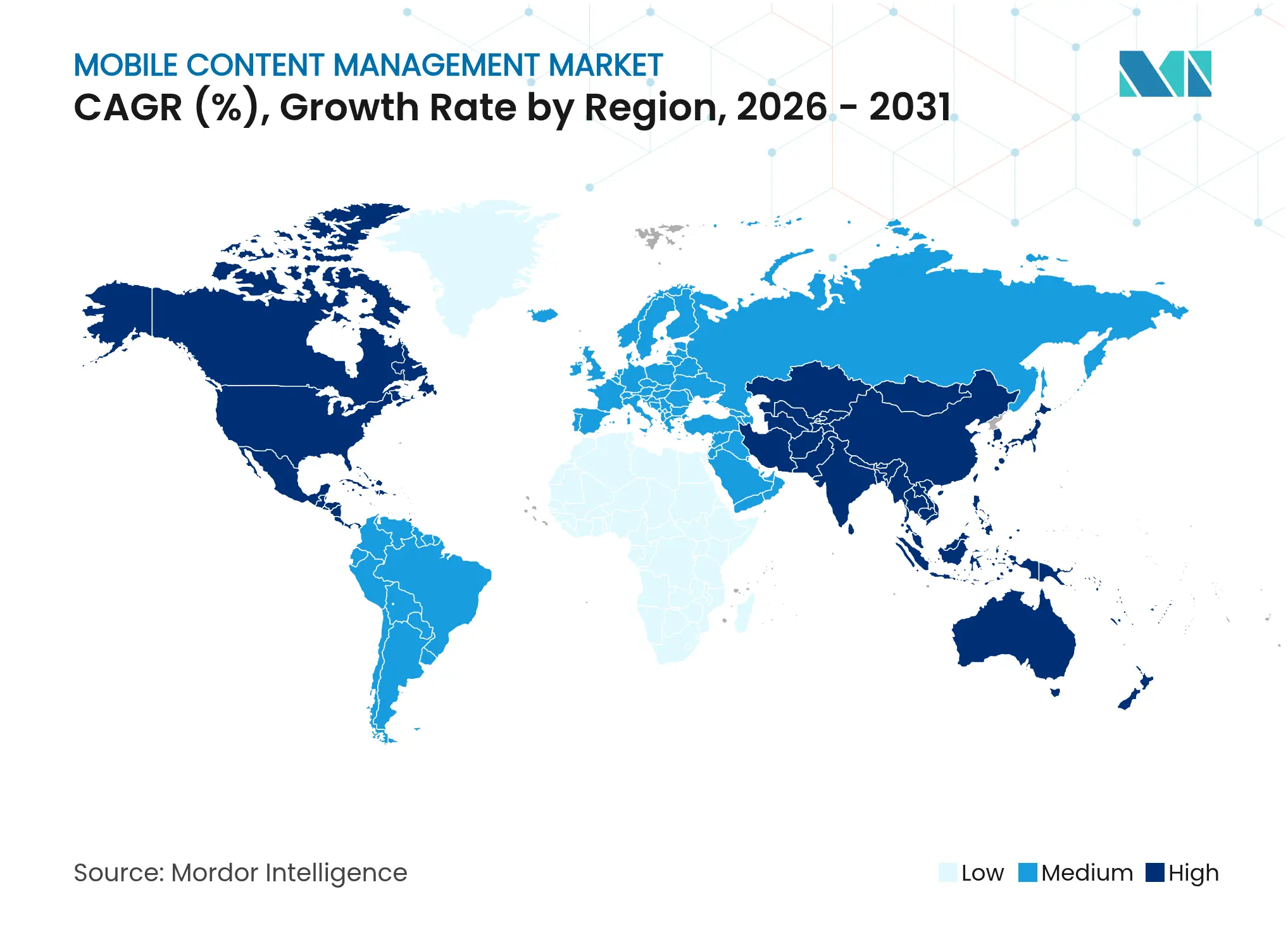

North America accounted for the largest regional slice at 36.05% in 2025, buoyed by early enterprise mobility adoption, mature cloud infrastructure and rigorous compliance regimes that favor comprehensive governance solutions. Vendor ecosystems are well established, allowing seamless integration with CRM, ERP and emerging AI services, which sustains premium pricing. Investments in zero-trust architecture further cement regional leadership within the mobile content management market.

Asia-Pacific, however, is forecast to grow at a 20.6% CAGR through 2031. Government-sponsored digital initiatives, expanding startup ecosystems and the proliferation of 5G networks collectively accelerate demand. Enterprises in Singapore, Indonesia and Vietnam roll out cloud-native suites to support cross-border supply chains and mobile retail channels, driving outsized volume gains across the mobile content management market.

Europe continues moderate growth anchored by GDPR enforcement and data-sovereignty legislation that require processors to demonstrate real-time compliance. Public-sector modernization programs in Germany and the Nordics prioritize secure mobile collaboration, while ESG reporting norms push traceable content chains. Middle East and Africa display nascent potential, particularly in Gulf Cooperation Council states that invest in smart-city projects. Latin America remains an emerging opportunity as businesses modernize document workflows to compete in increasingly digital regional trade blocs.

Market Concentration

The mobile content management market features moderate fragmentation. Enterprise software incumbents such as Microsoft, IBM and VMware leverage broad product suites and reseller channels to secure large-scale contracts. Box, Citrix and Hyland differentiate through vertical specialization, delivering healthcare- or finance-specific compliance workflows. Cloud-native challengers integrate AI-first design, emphasizing automated classification, predictive governance and simplified user experiences.

Strategic movement centers on three themes. First, platform consolidation: Salesforce agreed to acquire Zoomin to ingest unstructured content into its Data Cloud, signaling momentum toward multi-modal data platforms. Second, vertical expansion: OpenText, Hyland and Jamf deepen healthcare and education focus to capture regulatory niches. Third, AI infusion: ServiceNow and Google augment repositories with large-language-model powered assistants that recommend metadata and remediate access anomalies autonomously.

Pricing pressure rises as open-source headless CMS options mature, prompting proprietary vendors to bundle analytics and managed services. Partnerships with telecom operators and device manufacturers extend distribution reach, while managed security providers embed content governance within broader zero-trust offerings. These firm-level maneuvers collectively intensify rivalry yet also stimulate innovation that enlarges the total addressable mobile content management market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SEGMENTATION

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Market Definitions and Key Coverage

Our study treats the mobile content management (MCM) market as all software and associated services that let enterprises securely create, store, sync, and distribute business files to smartphones, tablets, and modern desktops while enforcing policy controls and audit trails across iOS, Android, and Windows endpoints. Demand emerging from bring-your-own-device workplaces and hybrid workstyles remains central to scope.

Devices shipped with simple consumer cloud drives, standalone document viewers, and traditional web-only content platforms are excluded.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed mobile security architects, workplace-apps product managers, and regional channel partners across North America, Europe, Asia-Pacific, and the Middle East. These conversations helped us confirm spend drivers, typical seat counts, license renewal cycles, and cloud-migration speeds, refining our price-volume curves.

Desk Research

We began by gathering baseline indicators from sources such as the US National Institute of Standards and Technology, Eurostat ICT surveys, India's MeitY mobility dashboards, and the Association for Intelligent Information Management. Company 10-Ks, earnings calls, patent filings, and tender portals supplemented adoption metrics and average selling prices.

Our team then mined paid databases, D&B Hoovers for supplier revenues, Dow Jones Factiva for deal flow, and Volza for cross-border license shipments to anchor historical data. Numerous additional public and proprietary references also informed validation beyond the list above.

Market-Sizing & Forecasting

A top-down installed-base model converts enterprise smartphone and tablet counts into an addressable seat pool, applies authenticated penetration ratios by industry, and multiplies results by blended annual license and support fees. Supplier roll-ups and sampled channel checks provide a bottom-up sense check that adjusts totals where gaps emerge. Input variables include BYOD adoption rate, remote-worker share, average cloud MCM price premium, regional data-protection enforcement actions, and mobile-OS refresh cadence. Forecasts to 2030 rely on multivariate regression linking these drivers plus GDP-per-employee to seat growth, with scenario analysis around stricter privacy rules.

Data Validation & Update Cycle

Outputs pass a three-layer review comprising analyst, senior peer, and research manager before sign-off. We reconcile anomalies against independent metrics each quarter, and the model is rebuilt every twelve months or sooner when material events such as landmark breach fines shift demand patterns.

Why Our Mobile Content Management Baseline Commands Confidence

Benchmark comparison

Published estimates often diverge because providers select different service baskets, apply varied currency dates, and refresh at unequal speeds. Clients regularly ask us why totals never align.

Key gap drivers are: some publishers fold broader enterprise mobility suites into MCM, others count only software fees and omit implementation, several rely on vendor-declared shipments without user-side validation, and many update projections biennially, whereas Mordor refreshes annually with live interviews.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 7.47 B (2025) | Mordor Intelligence | Anonymized source:Mordor Intelligence | Primary gap driver: | |

USD 4.46 B (2025) | Regional Consultancy A | Counts perpetual software licenses only; limited primary validation | ||

USD 9.30 B (2024) | Trade Journal B | Bundles device-management and app-wrapping revenue; uses vendor disclosures; older currency base |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.